Absorption Chillers Market Size, Share & Industry Analysis, By Technology Type (Single-Effect Absorption and Double-Effect Absorption), By Heat Source (Steam-Driven, Waste-Heat Driven, and Direct-Fired (Gas/Oil)), By Application (District Cooling, Industrial Process Cooling, and Commercial & Institutional), and Regional Forecast, 2026-2034

Absorption Chillers Market Size and Future Outlook

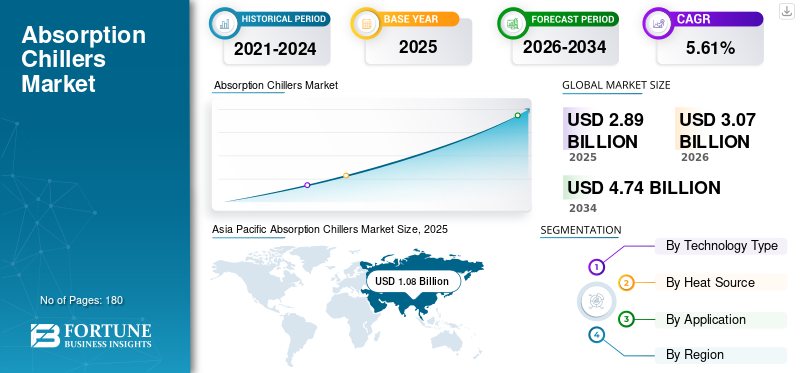

The global absorption chillers market size was valued at USD 2.89 billion in 2025 and is projected to grow from USD 3.07 billion in 2026 to reach USD 4.74 billion by 2034, exhibiting a CAGR of 5.61% during the forecast period. Asia Pacific dominated the absorption chillers market with a market share of 37.37% in 2025.

Absorption chillers are refrigeration systems that use thermal energy rather than mechanical energy to produce cooling. Unlike conventional compressor chillers that use electricity to run a motor, these chillers use a thermal-chemical process with a refrigerant and an absorbent to create a cooling effect. They are highly efficient in utilizing waste heat and are commonly used in industrial and large commercial applications to provide air conditioning and process cooling.

- In February 2026, Carrier Air Conditioning & Refrigeration Ltd announced plans to invest ~USD 100 million in a 39-acre manufacturing facility in Sri City, Andhra Pradesh, for sustainable AC production, creating 1,000 direct and 2,000 indirect jobs.

The Asia Pacific region holds the largest share in the market in terms of revenue. The surge in product demand is fueled by the need for cooling in hot climate countries, along with the adoption of combined heat and power (CHP) systems that utilize waste heat.

Johnson Controls International plc holds a prominent, top-tier position in the global market, frequently recognized alongside major competitors such as Thermax, Carrier, and LG Electronics. As of 2025, the company is recognized for driving sustainability through YORK-branded absorption chillers, particularly by leveraging waste heat, steam, and hot water for large-scale, energy-efficient cooling in industrial and commercial applications.

Download Free sample to learn more about this report.

Absorption Chillers Market Key Takeaways

- 2025 Market Size: USD 2.89 billion

- 2026 Market Size: USD 3.07 billion

- 2034 Forecast Market Size: USD 4.74 billion

- CAGR: 5.61% from 2026–2034

- Asia Pacific dominated the absorption chillers market with a 37.37% share in 2025.

- Double-effect absorption chillers held the largest product type share with 59.92% in 2025.

- Steam-driven absorption chillers accounted for the largest heat source share with 43.86% in 2025.

Asia Pacific

led the market with USD 1.08 billion in 2025 and is projected to reach USD 1.17 billion in 2026.

North America

North America was valued at USD 0.43 billion in 2025, making it the second-largest regional market.

Europe

reached USD 0.55 billion in 2025 and is projected to grow at a 4.20% CAGR during the forecast period.

U.S

The market reached USD 0.36 billion in 2025, accounting for 12.76% of global market revenues.

Japan

The market reached USD 0.12 billion in 2025, representing 4.41% of global market revenues.

Read More

ABSORPTION CHILLERS MARKET TRENDS:

Download Free sample to learn more about this report.

Growing Adoption of Trigeneration (CCHP) Systems to Shape the Market Trends

The rising adoption of trigeneration, or combined cooling, heat, and power (CCHP) systems, is profoundly shaping trends in the market. These integrated setups leverage waste heat from power generation to drive absorption chillers, boosting overall energy efficiency and slashing operational costs in commercial buildings, hospitals, and industrial facilities. As sustainability mandates intensify worldwide, businesses increasingly favor CCHP over traditional cooling methods, reducing carbon footprints while enhancing reliability. This shift spurs innovation in compact, high-efficiency chillers compatible with renewables such as biomass and solar thermal, alongside supportive policies promoting district energy networks, positioning absorption technology as a cornerstone of decentralized energy solutions.

MARKET DYNAMICS

MARKET DRIVERS:

Expansion of Industrial Waste Heat Recovery to Drive the Market

The expansion of industrial waste heat recovery is a key driver propelling the absorption chillers market growth. Industries such as chemicals, refineries, and food processing generate vast amounts of low-grade waste heat, traditionally vented or cooled inefficiently. These chillers capture this thermal energy to produce cooling, transforming waste into a valuable resource that enhances energy efficiency and cuts fuel consumption.

- For instance, in June 2023, Fortum announced plans to invest USD 200 million in Espoo Clean Heat projects, building heat pumps to recover waste heat from Microsoft's data centers in Espoo and Kirkkonummi, Finland, accelerating coal-free district heat by 2025.

Stricter environmental regulations and rising energy costs accelerate adoption, particularly in retrofits and new plants pursuing net-zero goals. Advancements in heat exchanger designs further improve integration, making these systems indispensable for sustainable operations and cost savings across heavy manufacturing sectors.

MARKET RESTRAINTS:

Limited Suitability for Small-Scale Applications to Restraint Market Growth

The limited suitability of absorption chillers for small-scale applications acts a restraint for the market. These systems excel in high-capacity environments such as district cooling and industrial complexes where abundant waste heat justifies their footprint and upfront costs, but they falter in compact residential or small commercial settings due to bulkiness, slower response times, and need for steady heat sources. This constraint channels investments toward scalable projects, spurring demand in mega-cities and heavy industries while prompting innovations in modular, compact designs to gradually penetrate smaller segments and broaden market accessibility.

MARKET OPPORTUNITIES:

Hydrogen & Energy Transition Projects to Create Lucrative Opportunities

Hydrogen and energy transition projects present compelling opportunities for the market. As green hydrogen production scales via electrolysis and reforming, excess process heat becomes available for absorption cooling, enabling efficient trigeneration in refineries, ammonia plants, and power-to-X facilities. These projects align with global decarbonization goals, integrating chillers into hybrid systems that utilize low-carbon heat from fuel cells or biomass gasification. Supportive incentives for clean energy infrastructure further boost adoption, particularly in regions such as Europe and the Middle East pursuing hydrogen economies, driving the demand for robust, high-temperature chillers compatible with emerging sustainable fuels.

MARKET CHALLENGES:

Competition from High-Efficiency Electric & Magnetic Bearing Chillers May Create Challenges for Market Growth

Intensifying competition from high-efficiency electric and magnetic bearing chillers poses a significant challenge for market players. These vapor-compression alternatives deliver superior part-load efficiency, faster startups, and compact designs, appealing to data centers, offices, and urban projects where space and electricity reliability prevail. Advances in variable-speed drives and low-GWP refrigerants further erode absorption's edge in moderate climates, while dropping renewable electricity costs diminish the appeal of heat-driven systems. Absorption chillers must embrace innovation in hybridization and controls to compete, particularly as grid modernization favors electric solutions over gas or waste-heat dependent technologies in electrifying economies.

Segmentation Analysis

By Technology Type

Double-Effect Absorption Segment Dominated Due to High Demand

Based on technology type, the market is classified into single-effect absorption and double-effect absorption.

In 2025, the double-effect absorption segment dominated the market with a 59.92% share. These chillers leverage higher thermal efficiency from cascaded cycles to capitalize on abundant high-temperature waste heat in industries and district cooling, which drives their demand. Additional key growth propellers include the rising demand for sustainable, low-maintenance HVAC systems in data centers, and increasing use of combined heat and power (CHP) systems.

Meanwhile, the single-effect absorption segment is poised for significant growth at a CAGR of 4.45% over the forecast period. The segment growth is driven by lower upfront costs, simpler integration in smaller-scale applications, and rising demand for affordable cooling in emerging markets and retrofits.

By Heat Source

Steam-driven Segment Led the Market Due to Reliability in High-demand Industrial Sector

Based on heat source, the market is classified into steam-driven, waste-heat driven, and direct-fired (gas/oil).

In 2025, the steam-driven segment dominated the global absorption chillers market share holding 43.86%, thriving on reliable boiler steam in large industrial and commercial setups for consistent high-capacity cooling. Integration with Combined Heat and Power (CHP) plants, utilization of waste heat for green cooling, avoidance of ozone-depleting refrigerants, and reliability in high-demand industrial sector are propelling the product demand.

Meanwhile, the waste-heat driven chillers segment is set for significant growth with a CAGR of 7.50% over 2026-2034. The segmental expansion is fueled by sustainability pushes to recover excess heat from processes, engines, and renewables, slashing energy costs in eco-focused facilities.

By Application

District Cooling Segment Emerged as Leading Segment Owing to the High Adoption

Based on application, the market is classified into district cooling, industrial process cooling, and commercial & institutional.

The district cooling segment dominated the market with a share of 39.94% in 2025, powering centralized networks in urban hubs with efficient, large-scale thermal energy for buildings and campuses. The segment growth is propelled by the need for energy-efficient, sustainable, and low-carbon cooling in urban areas. Driven by rapid urbanization and the utilization of waste heat (e.g., from industrial processes or incineration), these systems reduce electricity consumption, lower operating costs, and meet stringent environmental regulations.

Meanwhile, the industrial process cooling segment is poised for significant growth with a CAGR of 6.31% during the forecast period. The chillers harness waste heat recovery in manufacturing, chemicals, and food sectors to optimize operations and meet decarbonization targets.

To know how our report can help streamline your business, Speak to Analyst

Absorption Chillers Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific held the dominant share in 2025, valued at USD 1.08 billion, and is also poised to lead in 2026, with a value of USD 1.17 billion. The regional market is experiencing strong growth, driven by high demand for energy-efficient cooling in China, India, and Indonesia, alongside industrial adoption for waste heat recovery.

Asia Pacific Absorption Chillers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Absorption Chillers Market

The China market reached around USD 0.49 billion in 2025, accounting for roughly 45.36% of the global market revenues. China's market is a dominant force within the Asia Pacific region, driven by rapid industrialization, urbanization, and "Dual Carbon" policies favoring energy-efficient cooling.

India Absorption Chillers Market

The India market is projected to be one of the largest worldwide, with 2025 revenues touching around USD 0.20 billion, representing approximately 18.62% of the global market.

Japan Absorption Chillers Market

The Japan market reached a valuation of USD 0.12 billion in 2025, accounting for approximately 4.41% of global revenues.

North America

North America market touched a value of USD 0.43 billion in 2025, securing its position as the second largest regional market. The regional market is experiencing strong growth, driven by the demand for energy-efficient, sustainable HVAC systems in commercial buildings, data centers, and industrial applications. The market is expanding due to increased adoption of waste-heat recovery technologies and government incentives such as the Inflation Reduction Act.

U.S. Absorption Chillers Market

With North America’s strong contribution and the U.S. dominance in the region, the U.S. reached a value of around USD 0.36 billion in 2025, accounting for roughly 12.76% of the global market size. The U.S. market is experiencing steady growth, driven by demand for energy efficient, sustainable cooling in industrial and commercial sectors.

Europe

The Europe market reached a valuation of USD 0.55 billion in 2025 and is projected to record a growth rate of 4.20%, the third-highest among all regions, over the forecast period. The market is driven by stringent environmental regulations, decarbonization goals, and high energy efficiency needs. The demand is heavily fueled by the utilization of industrial waste heat in applications such as manufacturing, data centers, and district cooling, particularly in Germany.

Germany Absorption Chillers Market

In 2025, the Germany market touched a value of around USD 0.13 billion. It is projected to reach USD 0.14 billion by 2026, representing approximately 4.66% of the global industry revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The expansion is driven by industrialization, rising energy costs, and a need for sustainable, waste-heat-driven cooling solutions in Brazil, Mexico, and Chile. The market reached a valuation of USD 0.16 billion in 2025.

Brazil Absorption Chillers Market

The Brazil market reached a value of approximately USD 0.06 billion in 2025, accounting for a minor share of the global market.

Middle East & Africa

The Middle East & Africa market is expected to witness significant growth in this market during the forecast period. The market is driven by increased demand for energy-efficient, sustainable cooling in industrial, commercial, and district cooling sectors, particularly in the GCC region (Saudi Arabia, UAE). In 2025, this market reached a valuation of USD 0.06 billion.

GCC Absorption Chillers Market

The GCC market reached a value of approximately USD 0.43 billion in 2025, accounting for around 14.77% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players:

Vendors to Expand their Market Share through Partnerships and Technological Advancements

The global absorption chillers market is considered fragmented to moderately consolidated, featuring a mix of major global players and numerous regional, smaller manufacturers. While top-tier companies such as Thermax, Shuangliang, Johnson Controls, Trane, and LG Electronics hold significant market share, the market is competitive with high expansion, especially in Asia Pacific. Key strategies leading players are adopting include launching high-efficiency, corrosion-resistant models, expanding geographically into high-growth regions such as Asia Pacific and the Middle East, and offering comprehensive, long-term service agreements.

For instance, in September 2025, Yazaki Energy System Corporation launched the world's smallest class cooling system, integrating the "Aroace" hot water-fired absorption chiller-heater with cooling tower, heat storage tank, pumps, piping, and controls. Such developments are expected to fuel market growth during the forecast period.

LIST OF KEY ABSORPTION CHILLER COMPANIES PROFILED:

- Johnson Controls International plc (Ireland)

- World Energy Absorption Chillers Co., Ltd (South Korea)

- Broad Group (Broad Air Conditioning Co., Ltd.) (China)

- Thermax Limited (India)

- Trane Technologies plc (Ireland)

- Carrier Global Corporation (U.S.)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Hitachi, Ltd. (Japan)

- LG Electronics Inc. (South Korea)

- Yazaki Corporation (Japan)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Century Corporation (Century Refrigeration) (South Korea)

- Robur Corporation (Italy)

- Shuangliang Eco-Energy Systems Co., Ltd. (China)

- EAW Energieanlagenbau GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS:

- February 2026: Johnson Controls launched a Reference Design Guide Series for 1 Gigawatt AI data centers. These comprehensive guides detail thermal management solutions such as water-cooled chiller plants (with air-cooled and absorption chiller guides forthcoming), aligned with NVIDIA DSX architecture for scalable, energy-efficient, and sustainable cooling.

- September 2025: Panasonic, Osaka Gas, and Daigas Energy developed the industry's first absorption chiller compatible with 0–100% hydrogen-city gas co-firing. It suppresses NOx below 40 ppm via advanced combustion control and burner tech. Existing city gas units can be upgraded easily by replacing parts, aiding carbon neutrality.

- August 2024: Panasonic began a demonstration using 70°C waste heat from improved pure hydrogen fuel cell generators to power a new absorption chiller at H2 KIBOU FIELD. The chiller lowers minimum heat needs from 80°C via drip-type regeneration, achieving 95% energy efficiency for zero-carbon cooling.

- July 2024: EBARA Corporation and Tokuyama Corporation agreed on a pilot test for the hydrogen-powered absorption chiller-heater (Model RHDH) at Tokuyama Cultural and Sports Center. Using byproduct hydrogen, it achieves zero CO2 emissions, energy savings via advanced controls, and water refrigerant for carbon neutrality.

- August 2023: Bloom Energy launched its advanced CHP solution using the Bloom Energy Server in 2023, featuring >350°C exhaust for steam production and absorption chilling. Achieving over 90% combined efficiency, it surpasses traditional systems, cuts costs/emissions for industries, and supports net-zero heating/cooling with zero air pollution.

REPORT COVERAGE

The global absorption chillers market analysis provides an in-depth study of the market size & forecast by all the segments included in the report. It contains details on the market dynamics and industry trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.61% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology Type, Heat Source, Application, and Region |

|

By Technology Type |

|

|

By Heat Source |

|

|

By Application |

|

|

By Region |

North America (By Technology Type, By Heat Source, By Application, and Country)

Europe (By Technology Type, By Heat Source, By Application, and Country)

Asia Pacific (By Technology Type, By Heat Source, By Application, and Country)

Latin America (By Technology Type, By Heat Source, By Application, and Country)

Middle East & Africa (By Technology Type, By Heat Source, By Application, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.89 billion in 2025 and is projected to reach USD 4.74 billion by 2034.

In 2025, the market value stood at USD 1.08 billion.

The market is expected to exhibit a CAGR of 5.61% during the forecast period of 2026-2034.

The district cooling sector leads the market by application.

The expansion of industrial waste heat recovery is a key factor driving the market.

Thermax, Shuangliang, Johnson Controls, Trane, and LG Electronics are some of the prominent players in the Market.

Asia Pacific dominated the market in 2025.

The product adoption is primarily favored by the urgent global push for decarbonization and energy efficiency, allowing industries to convert wasted heat from industrial processes, cogeneration, or solar thermal sources into cooling.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us