Cryogenic Insulation Market Size, Share & Industry Analysis, By Form (Foam, Bulk Fill, MLI (Multilayer Insulation), and Others), By Type (Perlite Insulation, Polyurethane (PU), Fiberglass, Polyisocyanurate (PIR), Cellular Glass, and Others), By End-Use Industry (Oil & Gas, Chemical & Fertilizer, Transportation, Food & Beverage, Electronics, and Others), and Regional Forecast, 2026-2034

Cryogenic Insulation Market Size and Future Outlook

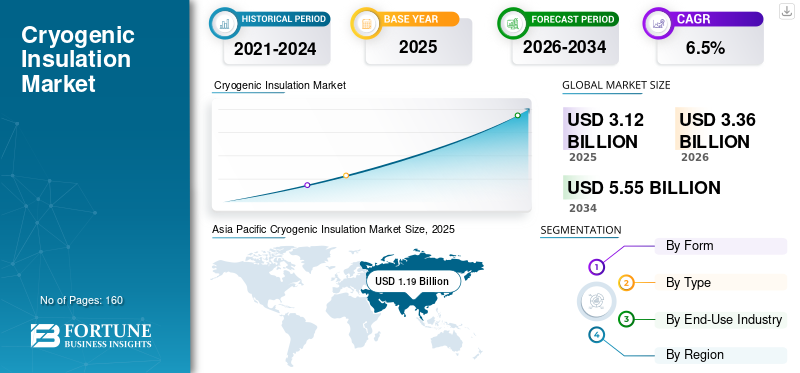

The global cryogenic insulation market size was valued at USD 3.12 billion in 2025. The market is projected to grow from USD 3.36 billion in 2026 to USD 5.55 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. Asia Pacific dominated the cryogenic insulation market with a market share of 38.14% in 2025.

Cryogenic insulation refers to thermal insulation systems engineered to minimize heat ingress, condensation, and boil-off in equipment operating at very low temperatures, typically below -50°C and extending to LNG (-161°C) and liquid hydrogen regimes. These systems combine insulation materials (e.g., perlite, cellular Polyurethane (PU), fiber Polyurethane (PU), PU/PIR foams, and multilayer/vacuum solutions) with vapor barriers, jacketing, and application know-how to protect cryogenic tanks, piping, valves, cold boxes, and associated infrastructure.

The market growth is driven by build-out and debottlenecking of LNG import/export infrastructure, higher specification requirements for safety and condensation control in industrial gases and petrochemical assets, and the early scaling of hydrogen and ammonia value chains, where low-temperature storage and transfer become critical. Suppliers are also differentiating through faster-installing systems, better moisture resistance, and solutions that reduce contraction-joint complexity and maintenance risk in long pipe runs.

Furthermore, the market comprises several major players, including Armacell, Aspen Aerogels, Owens Corning, Saint-Gobain, and Knauf Insulation. Competitive positioning is shaped by product reliability under thermal cycling, vapor barrier integrity, installation productivity, and the ability to support EPC qualification and global project execution.

Download Free sample to learn more about this report.

Cryogenic Insulation Market Key Takeaways

- 2025 Market Size: USD 3.12 billion

- 2026 Market Size: USD 3.36 billion

- 2034 Forecast Market Size: USD 5.55 billion

- CAGR: 6.5% from 2026-2034

- Asia Pacific dominated the cryogenic insulation market with a 38.14% share in 2025.

- The foam segment accounted for the largest market share of 44.4% in 2025.

- The perlite insulation segment held a 37.2% share in 2025.

North America

North America is projected to reach USD 0.66 billion in 2026, supported by growing LNG and industrial gas infrastructure investments.

Asia Pacific

Asia Pacific accounted for USD 1.19 billion in 2025 and is projected to reach USD 1.29 billion in 2026.

Europe

Europe is projected to grow at a CAGR of 6.9% and reach USD 0.73 billion in 2026.

U.S.

The market was valued at USD 0.50 billion in 2025.

Japan

Rising investments in LNG infrastructure and clean energy projects are supporting market growth.

Read More

CRYOGENIC INSULATION MARKET TRENDS

LNG Capacity Additions and Hydrogen-Ready Cold Infrastructure are Significant Market Trends

Cryogenic insulation demand continues to rise as LNG terminals, storage expansions, and gas processing assets prioritize schedule certainty and reliability under thermal cycling. EPCs increasingly evaluate insulation options not only on thermal conductivity but also on installation speed, damage tolerance, and the ability to maintain vapor barrier performance over long operating periods. In parallel, early hydrogen liquefaction and liquid hydrogen logistics are increasing interest in multilayer and vacuum-adjacent solutions where boil-off control is a core design requirement. Across regions, tighter safety expectations are also supporting the adoption of non-absorptive or fire-resilient insulation systems for spill-prone zones.

- For instance, suppliers are publishing LNG-focused application guides and system designs that emphasize faster installation, reduced contraction-joint needs, and improved durability for cryogenic piping and equipment.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

LNG and Industrial Gas Infrastructure Expansion and Reliability Requirements are Driving Market Growth

Cryogenic insulation is a non-discretionary requirement for LNG, industrial gas (oxygen, nitrogen, argon), and low-temperature petrochemical services, where heat ingress directly affects boil-off losses, process stability, and safety. As LNG capacity additions and terminal upgrades continue, the installed base of cryogenic tanks and long-pipe networks expands, boosting both project demand and follow-on maintenance needs. In industrial gases, cold boxes, cryogenic storage, and distribution systems require insulation solutions that withstand repeated thermal cycling while maintaining low permeability to prevent icing and corrosion beneath the insulation.

- For instance, LNG projects increasingly specify insulation systems that shorten installation time on complex piping and fittings, helping EPCs reduce schedule risk.

MARKET RESTRAINTS

Complex Installation, Moisture-Ingress Risk, and Qualification Requirements Can Limit Adoption

Cryogenic insulation performance depends on workmanship and system integrity, particularly for vapor barriers, joints, and jacketing. Projects may face constraints from skilled labor availability, complex detailing around valves and supports, and the need for rigorous inspection to avoid water ingress that can lead to icing and corrosion under insulation. Higher-performance options such as aerogel blankets, multilayer systems, and vacuum-adjacent designs can carry higher upfront cost, and many end users require qualification evidence across thermal cycling, mechanical robustness, and long-term aging before full-scale deployment.

MARKET OPPORTUNITIES

Hydrogen Liquefaction, Ammonia and CO2 Cold Chains, and Retrofit Programs Create Lucrative Growth Opportunities

The cryogenic insulation market growth is expected in hydrogen and hydrogen-derived fuels, where cryogenic storage and transfer infrastructure will be necessary for export/import, mobility, and industrial decarbonization pathways. Retrofit programs that target boil-off reduction, condensation control, and insulation integrity in existing LNG and industrial-gas assets can also expand addressable demand, as operators seek reliability improvements without full asset replacement. In addition, cold energy recovery concepts and more stringent safety design in spill-prone zones can support higher-value insulation system upgrades.

MARKET CHALLENGES

Project Cyclicality, Supply Chain Constraints, and Substitution Risk May Affect Growth

Demand is linked to large capital projects such as LNG terminals and industrial gas plants, creating exposure to permitting timelines, financing cycles, and EPC scheduling. Supply chains for specialized materials and accessories can become tight during peak build years, and logistics constraints can be material for bulky insulation products and jobsite packaging. Finally, customers may switch among insulation types (e.g., foam, perlite, cellular Polyurethane (PU), or aerogel-based systems) depending on total installed cost, moisture performance, fire and spill requirements, and contractor familiarity.

Segmentation Analysis

By Form

Foam Segment Led the Market Owing to Wide Usage of PU/PIR-Based Systems

Based on form, the market is segmented into foam, bulk fill, MLI (Multilayer Insulation), and others.

The foam segment accounted for the largest cryogenic insulation market share in 2025. The segment is driven by widespread use of PU/PIR-based systems for piping, equipment, and cold-service applications where installation productivity and consistent thermal performance are valued. Furthermore, the segment is set to hold a 44.4% share in 2025.

The growth of the bulk fill segment is supported by the push to reduce boil-off losses, tighter efficiency requirements, and increased use of vacuum systems where MLI delivers strong performance per thickness. The bulk fill segment is projected to grow at a 6.4% CAGR during the study period.

By Type

Perlite Insulation Segment is Expected to Remain Prominent Due to Broad Applicability in Various End-Use Industries

Based on type, the market is segmented into perlite insulation, polyurethane (PU), fiberglass, polyisocyanurate (PIR), cellular glass, and others.

The perlite insulation segment accounted for the largest share in 2025, driven by its long-established use in large cryogenic enclosures and tank-related applications where loose-fill systems are advantageous. The growth follows LNG capacity additions and terminal expansions, as well as recurring maintenance needs, such as drying or replenishment after moisture ingress. Furthermore, the segment is set to hold a 37.2% share in 2025.

The polyurethane (PU) segment is expected to grow favorably throughout the forecast period, driven by extensive use in rigid foam systems for cryogenic piping, equipment, and modular insulation, where high insulating value and ease of fabrication support faster project execution. It is widely used in LNG plants, terminals, and industrial gas installations and benefits greatly from retrofit and maintenance work to reduce heat leaks.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Oil & Gas Segment Dominates Market Due to Extensive Use of Product

By end-use industry, the market is categorized into oil & gas, chemical & fertilizer, transportation, food & beverage, electronics, and others.

The oil & gas segment accounted for the largest share in 2025, driven by new LNG terminals, tank additions, debottlenecking, and retrofit programs focused on reducing boil-off and improving safety. Large insulated surface areas in tanks and piping create high material volumes, while maintenance cycles sustain recurring demand across the installed base. Furthermore, the segment is set to hold a 57.9% share in 2025.

The chemical & fertilizer segment is also expected to grow favorably over the projected period. The segment's growth is supported by increased use of industrial gases and cryogenic services across large chemical complexes, including air separation, cryogenic separation, and low-temperature processing steps. Insulation demand rises with plant expansions, reliability upgrades, and energy-efficiency initiatives aimed at reducing heat leaks and controlling condensation. The segment is expected to grow at a CAGR of 6.6% over the forecast period.

Cryogenic Insulation Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Cryogenic Insulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 1.19 billion, and is expected to maintain its leading share in 2026, valued at USD 1.29 billion. The region’s growth is supported by a large LNG import and regasification footprint, continued terminal upgrades, and the scale of industrial gas and downstream manufacturing activity. China remains the largest consumer, while Japan and South Korea contribute through established LNG infrastructure, advanced industrial manufacturing, and high specification insulation requirements.

China Cryogenic Insulation Market

In 2025, the China market size reached USD 0.31 billion. LNG receiving terminals, industrial gases, and expanding cryogenic logistics networks support steady demand for bulk-fill and foam-based insulation systems across tanks, piping, and equipment.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 0.66 billion by 2026. The region benefits from LNG and industrial gas infrastructure investment, a large installed base of process piping and storage assets, and a robust maintenance and retrofit cycle that supports ongoing insulation replacement and upgrades.

U.S. Cryogenic Insulation Market

In 2025, the U.S. market value reached USD 0.50 billion. In the U.S., the demand is supported by large-scale energy infrastructure, industrial gas consumption, and extensive cold-service piping and equipment networks in petrochemical and processing hubs.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at 6.9% and reach a valuation of USD 0.73 billion in 2026. The region's growth is driven by high-specification cold-service insulation in industrial clusters, insulation replacement cycles, and continued investments in low-temperature energy infrastructure.

U.K. Cryogenic Insulation Market

The U.K. market in 2025 was valued at around USD 0.14 billion, representing approximately 6.2% of the global market revenue.

Germany Cryogenic Insulation Market

Germany’s market reached approximately USD 0.16 billion in 2025, equivalent to around 7.7% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 reached a valuation of USD 0.29 billion. The demand in the region is linked to LNG import infrastructure in select markets, industrial gas distribution, and project-driven spending in energy and process industries.

Brazil Cryogenic Insulation Market

Brazil’s market reached approximately USD 0.12 billion in 2025, equivalent to around 6.0% of global sales.

Middle East & Africa

The Middle East and Africa region is gradually expanding, with sales recorded at around USD 0.38 billion in 2025. GCC countries account for a notable share of regional demand, driven by hydrocarbon processing and LNG-linked infrastructure that requires cryogenic tanks, loading systems, and low-temperature piping. Other demand is linked to industrial gas projects, processing industries, and imported high-performance insulation systems.

GCC Cryogenic Insulation Market

GCC reached USD 0.24 billion by 2025, accounting for approximately 5.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Adopting Business Expansion Strategies to Maintain Their Positions in Market

Competition is shaped by insulation performance under cryogenic thermal cycling, long-term vapor barrier integrity, fire and spill considerations, installation productivity, and the ability to support EPC qualification and global project execution. Diversified insulation manufacturers compete with specialists focused on aerogel-based blankets, cellular glass, and advanced cold-service system designs. Key competitive differentiators include consistent quality, technical support for system detailing, and reliable project supply across multiple regions. Some of the key market players include Armacell, Aspen Aerogels, Owens Corning, Saint-Gobain, and Knauf Insulation. Key competitive differentiators include consistent quality, technical support for system detailing, and reliable project supply across multiple regions.

LIST OF KEY CRYOGENIC INSULATION COMPANIES PROFILED

- Armacell (U.S.)

- Aspen Aerogels (U.S.)

- Owens Corning (U.S.)

- Saint-Gobain (France)

- Knauf Insulation (Germany)

- Johns Manville (U.S.)

- Kingspan (Ireland)

- Rockwool (Denmark)

- Ravago (Luxembourg)

- KAEFER (Germany)

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Form, Type, End-Use Industry, and Region |

| By Form |

|

| By Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 3.12 billion in 2025 and is projected to reach USD 5.55 billion by 2034.

Recording a CAGR of 6.5%, the market is slated to exhibit steady growth during the forecast period.

The oil & gas end-use industry segment led in 2025.

Asia Pacific held the highest market share in 2025.

Armacell, Aspen Aerogels, Owens Corning, Saint-Gobain, and Knauf Insulation are some of the prominent players in the market.

The growth driver is the rapid expansion and upgrades of LNG and industrial-gas cryogenic infrastructure (liquefaction, storage tanks, terminals, and cold boxes), which are increasing demand for high-performance insulation to reduce heat leaks and boil-off.

The major factors expected to favor product adoption are rising focus on energy efficiency/lifecycle cost, stricter safety and condensation/CIU control, and wider availability of advanced materials (aerogels/MLI) that simplify installation and deliver higher thermal performance in tight spaces.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us