Level Transmitter Market Size, Share & Industry Analysis, By Installation Type (Retrofit Installation and New Installation) By Technology Type (Differential Pressure, Hydrostatic, Ultrasonic, Radar, Capacitive, and Others) By End User (Food & Beverage, Water & Wastewater, Oil & Gas, Power & Utilities, Chemicals & Petrochemicals, and Others) and Regional Forecast, 2026-2034

Level Transmitter Market Size and Future Outlook

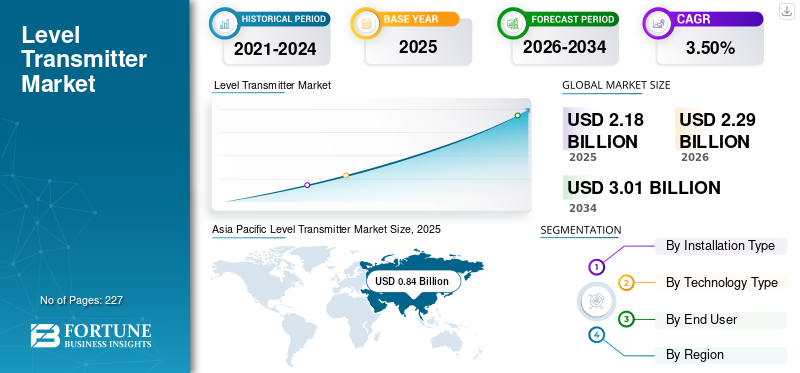

The global level transmitter market size was valued at USD 2.18 billion in 2025. The market is projected to grow from USD 2.29 billion in 2026 to USD 3.01 billion by 2034, with a CAGR of 3.50% over the forecast period. Asia Pacific dominated the level transmitter market with a market share of 38.53% in 2025.

A level transmitter is an industrial measurement instrument used to continuously monitor and transmit the level of liquids, slurries, or bulk solids within tanks, vessels, silos, or open channels. It converts the measured level into a standardized electrical signal (e.g., 4–20 mA or a digital communication protocol) for monitoring and control systems. Level transmitters enable accurate process control, inventory management, and safety monitoring across industries such as oil & gas, chemicals, water & wastewater, and power generation. They operate using various technologies, including radar, ultrasonic, hydrostatic, capacitive, and differential pressure, depending on the application and process conditions.

The growth of the level transmitter market is primarily driven by increasing industrial automation and process optimization across process industries, where accurate level measurement is critical for operational efficiency and safety. Rising investments in water and wastewater treatment infrastructure, especially in emerging economies, are driving demand for reliable, continuous level-monitoring solutions. Expansion of the oil & gas, chemicals, and petrochemicals sectors, including refinery upgrades and capacity additions, is further supporting market growth. In addition, the ongoing shift from conventional instruments to smart and digital transmitters with advanced diagnostics, remote monitoring, and IIoT compatibility is accelerating replacement demand. Stringent safety, environmental, and regulatory compliance requirements are also encouraging industries to adopt high-accuracy, non-contact level measurement technologies, such as radar and ultrasonic systems.

Leading players operating in the market are Emerson Electric, Endress Hauser, Siemens, ABB, and Yokogawa Electric. These companies play a pivotal role in the industry by offering a comprehensive portfolio of level measurement solutions, including advanced radar, guided wave radar, and differential pressure transmitters. These companies support critical sectors such as oil & gas, chemicals, and power with high-accuracy, SIL-rated instruments and strong digital integration capabilities, enabling safer operations and improved asset performance across complex process environments.

Download Free sample to learn more about this report.

Level Transmitter Market Trends

Digital and Smart Level Measurement Integration is a Key Market Trend

A prominent trend in the level transmitter market is the accelerated adoption of digital and innovative measurement solutions that integrate with industrial automation and analytics systems. Traditional analog 4-20 mA transmitters are increasingly being replaced with devices capable of two-way communication (e.g., HART, Fieldbus, Ethernet-based protocols) and built-in diagnostics. This shift is driven by industry needs for real-time data access, predictive maintenance, and seamless integration into Distributed Control Systems (DCS) and Supervisory Control and Data Acquisition (SCADA) platforms. For example, plants with multiple tanks or silos now prefer instruments that can continuously report level trends, detect failure modes, and provide early warnings of anomalies, reducing unplanned shutdowns. Smart transmitters also support remote configuration and calibration, lowering on-site maintenance time. As industries pursue Industry 4.0 and digital twin initiatives, the expectation is that a growing share of new level transmitters will be installed with digital interfaces and enhanced diagnostics, moving the market away from purely analog devices toward connected, intelligent measurement ecosystems. This trend fundamentally reshapes value propositions for manufacturers, integrators, and end users alike.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Infrastructure Expansion and Industrial Growth to Push the Market Growth

The primary driver of the level transmitter market growth is the ongoing expansion of industrial infrastructure and process facilities across key sectors, including energy, chemicals, municipal water services, and manufacturing. As countries invest in new refineries, petrochemical complexes, wastewater treatment plants, and utility upgrades, demand for continuous level measurement grows correspondingly. In many developing regions, rapid urbanization is driving municipal water and wastewater projects, where accurate level monitoring is essential for regulatory compliance and efficient operation of reservoirs, clarifiers, and lift stations. Similarly, expansions in liquid storage capacity in oil & gas terminals and chemical storage hubs require precise level instrumentation to manage inventory, prevent overfills, and support safety systems. Even in mature markets, replacement and modernization of aging infrastructure contribute significantly to demand, as older mechanical gauges and outdated electronics are upgraded to modern transmitters with better reliability and integration capabilities. This cumulative infrastructure growth in both greenfield and brownfield settings creates a sustained baseline demand for level transmitters globally, underpinning a steady increase in the level transmitter market.

Market Restraints

High Upfront Cost of Advanced Technologies to Limit the Market Expansion

A significant restraint on the market is the relatively high upfront cost of advanced measurement technologies, particularly non-contact and guided-wave radar systems. While these technologies offer superior performance, such as high accuracy in harsh environments, minimal maintenance, and immunity to factors, including vapor and foam, their capital cost per unit can be significantly higher than simpler alternatives, such as hydrostatic or ultrasonic transmitters. For small and medium-sized enterprises and price-sensitive applications (e.g., basic water tanks or non-critical storage), the higher purchase price can delay or limit adoption. Budget constraints may lead facilities to choose lower-cost options that sacrifice long-term reliability or smart functionality, perpetuating the use of older technology generations. Additionally, the cost of implementing associated communication and asset management infrastructure (e.g., gateways, network devices, software licenses) can further deter investment, particularly in brownfield plants where retrofit budgets are limited. This restraint tends to be more pronounced in regions with lower industrial automation penetration or where capital allocation favors essential process upgrades over instrumentation modernization, slowing broader adoption of high-end level transmitter solutions.

Market Opportunities

Services and Aftermarket Revenue Streams to Create New Growth Avenues

A compelling market opportunity lies in the growth of services and aftermarket revenue streams, including calibration, predictive maintenance, digital upgrades, and lifecycle support. As installed bases of level transmitters age, and as customers seek to maximize uptime and reliability, demand for scheduled calibration, field diagnostics, firmware updates, and performance optimization services is rising. Service contracts can generate recurring revenue for manufacturers and channel partners, extending customer relationships beyond the initial hardware sale. With the proliferation of digital and smart transmitters, there is also an opportunity to offer cloud-based monitoring dashboards, analytics subscriptions, and remote support that help end users detect drift, plan maintenance, and reduce unplanned outages. Retrofit services, replacing outdated analog instruments with modern smart devices and integrating them into digital plant architectures, present an additional growth avenue, particularly in mature industrial regions where new installation growth has slowed. By bundling hardware with value-added services, companies can increase customer stickiness and differentiate offerings in a market where product features are rapidly converging. This shift toward instrumentation-as-a-service can open new revenue streams and strengthen long-term profitability.

Market Challenges

Environmental and Process Condition Complexity to Limit Market Growth

A significant market challenge is the wide range of environmental and process conditions that can compromise measurement accuracy and instrument reliability. Level transmitters are deployed in highly diverse settings, from corrosive chemical reactors and high-pressure hydrocarbon separators to dusty bulk solids silos and wastewater sumps with foam and turbulence. Each of these environments presents its own set of measurement complications: vapor and condensation can distort radar reflections, foam layers can mimic liquid surfaces, dust and particulate matter can scatter ultrasonic waves, and extreme temperatures can affect sensor materials and electronics. In bulk solids applications, irregular surface profiles and varying dielectric properties make consistent measurement difficult for specific technologies. Manufacturers must therefore offer solutions with specialized configurations, coatings, compensation algorithms, and ruggedized designs to handle these conditions. This complexity increases the engineering, testing, and validation effort required to specify the correct transmitter for an application, and it raises the risk of performance shortfalls if instruments are not properly selected or installed. The challenge lies in developing versatile technologies and ensuring that end users have the expertise to effectively match devices to challenging process conditions effectively.

Segmentation Analysis

By Installation Type

Increasing Investments in New Projects to Lead the New Installation Segment Growth

Based on installation type, the market is segmented into retrofit installation and new installation.

New installation segment accounts for approximately 50.75% of the market share. This segment reflects demand generated by greenfield builds, plant expansions, and infrastructure development across a broad range of end-use sectors, including energy, water & wastewater, chemicals, food & beverage, and industrial manufacturing. In developing economies and rapidly industrializing regions, the pace of infrastructure spending on wastewater treatment plants, storage terminals, refineries, and production facilities drives the ongoing adoption of level transmitters as part of new process control architectures. New installations often involve specifying the latest technologies (such as high-frequency radar or wireless-enabled ultrasonic transmitters) and integrating with modern automation systems from project inception, leading to strong initial unit and value demand. While retrofit demand underpins replacement cycles, new installations remain the primary driver of global unit volume growth, anchoring long-term expansion in markets where industrial capacity is still increasing. As new installation projects often specify higher instrument counts per facility and incorporate digital communication capabilities, this segment contributes substantially to overall market revenue, especially in robust infrastructure investment environments.

Retrofit installation segment is expected to grow at a CAGR of 3.97% during the forecast period.

By Technology Type

Higher Accuracy Characteristics of the Radar Fuel the Segment Growth

Based on the technology type, the market is segmented into differential pressure, hydrostatic, filter, presses, radar, capacitive, and others.

Radar segment accounts for 34.16% of the market due to its high separation efficiency and suitability for large‑scale industrial and wastewater applications. Radar has become the preferred technology for a wide range of critical and demanding applications due to its high accuracy, independence from process conditions such as vapor, foam, dust, or turbulence, and strong suitability for both liquids and solids. In complex environments such as oil & gas, petrochemical processing, power generation, and bulk solids storage, radar transmitters deliver reliable and repeatable measurements that conventional technologies struggle to achieve. The segment’s leadership is also supported by robust adoption in new automation projects, elevated average selling prices relative to simpler technologies, and integration with digital communication networks that support asset management and predictive maintenance. As plants pursue digital transformation and safety compliance, radar technology’s share continues to grow, often capturing the largest level transmitter market share as customers are willing to invest in technology that assures performance under challenging conditions and reduces long-term maintenance costs.

The hydrostatic segment is expected to grow at a CAGR of 3.82% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Expanding Oil & Gas Exploration and Production Activities to Propel the Segment Growth

Based on end user, the market is segmented into food & beverage, water & wastewater, oil & gas, power & utilities, chemicals & petrochemicals, and others.

The oil & gas segment represents the largest share of the market. It captured a 23.13% share in 2025, driven by the industry’s extensive use of level measurement for inventory control, safety systems (such as high/low level alarms), and process optimization in upstream, midstream, and downstream operations. In refineries, storage terminals, and offshore platforms, level transmitters support critical functions such as tank gauging, separator control, and interface detection, where accuracy and reliability are essential for safety and compliance. The high average selling prices of advanced technologies, particularly radar, further amplify the sector's revenue contribution. Ongoing investments in maintaining, upgrading, and expanding hydrocarbon infrastructure in many regions sustain this segment’s dominance. Even amid volatile oil prices, operators continue to prioritize measurement upgrades to improve asset integrity and minimize environmental and safety risks, ensuring the oil & gas segment retains its leading position in the market.

The water & wastewater segment is estimated to grow with a CAGR of 4.81% over the forecast period.

Level Transmitter Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Level Transmitter Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest region, valued at USD 0.84 billion in 2025, accounting for approximately 38.28% of global market revenues. This dominant position stems from rapid industrial expansion, infrastructure development, and accelerated adoption of automation technologies across China, India, Southeast Asia, and other emerging economies. Massive investments in water & wastewater treatment plants, petrochemical complexes, power plants, and manufacturing facilities drive strong new installation demand. The region also witnesses a growing retrofit market as older assets are upgraded with more accurate, digitally capable transmitters. The sheer volume of projects, including urban water infrastructure, bulk storage terminals, and process facilities, ensures that both unit sales and revenue from technologies such as radar, ultrasonic, and hydrostatic are considerable. Fast-paced construction of industrial parks and export-oriented facilities further amplifies the Asia Pacific’s central role in global market growth, making it the fastest-growing regional market segment overall.

China Level Transmitter Market

China remains the dominant contributor in the Asia Pacific, valued at USD 0.37 billion in 2025 and expected to reach USD 0.40 billion in 2026, propelled by rapid industrial expansion, water & wastewater infrastructure development, and manufacturing growth. Both new installations and retrofit modernization projects contribute to a strong market presence.

India Level Transmitter Market

India was estimated at USD 0.155 billion in 2025 and is set to reach USD 0.164 billion in 2026, supported by investments in water treatment, energy facilities, and industrial automation. While cost sensitivity influences technology choices, expanding infrastructure and manufacturing drive rising transmitter demand.

Japan Level Transmitter Market

Japan was valued at USD 0.108 billion in 2025 and is expected to reach USD 0.114 billion in 2026. It maintains a solid share due to its advanced industrial sectors, including chemicals, electronics, and power utilities, with high levels of automation and quality control. Demand for precise, reliable measurement technology sustains its market contribution.

North America

The North America market was valued at USD 0.71 billion in 2025, accounting for approximately 32.43% of the market. This strong position is supported by its mature industrial base, particularly in oil & gas, chemicals, power generation, and water utilities, where accurate level measurement is critical for operational efficiency and safety. The region has also been at the forefront of digitalization and automation, with many brownfield plants retrofitting legacy transmitters to smart, connected devices that offer diagnostics and remote monitoring capabilities. The high adoption of wireless communication protocols and their integration with advanced control systems further enhances the value captured in North America. Even though new greenfield installations are relatively slower than in fast-growing regions, retrofit and modernization demand ensure a robust and steady share of the global market. Large average selling prices for advanced transmitters, especially radar and digitalized technologies, contribute disproportionately to revenue, reinforcing North America’s leading position.

U.S. Level Transmitter Market

The U.S. market was estimated at USD 0.61 billion in 2025 and is set to reach USD 0.64 billion in 2026, driven by its large industrial base, particularly in oil & gas, water utilities, chemicals, and power. Strong automation and retrofit demand amplify its contribution, as frequent upgrades to smart and digital transmitters drive demand.

Europe

Europe accounted for USD 0.41 billion in 2025, representing approximately 18.89% of global revenues, driven by strong industrial automation, stringent environmental and safety regulations, and widespread modern infrastructure. The chemicals, pharmaceuticals, and process manufacturing sectors in Western Europe are particularly strong adopters of advanced level measurement technologies such as radar and guided-wave transmitters. In addition, extensive water and wastewater networks across Europe generate a high demand for reliable level sensors in municipal and industrial applications. Retrofit projects are also prevalent, as aging

infrastructure is being upgraded to digital, innovative systems to improve energy efficiency and compliance with EU regulatory standards. Robust investments in renewable energy and smart grid technologies further support market demand. While growth in new installations may be more moderate than in emerging regions, Europe’s combination of retrofit intensity and high-value installations sustains its influential global market share.

Germany Level Transmitter Market

Germany was estimated at USD 0.10 billion in 2025 and is set to reach USD 0.11 billion in 2026. It holds a meaningful share driven by advanced manufacturing, the chemical and process industries, and stringent industrial standards. The country’s focus on precision instrumentation and digital integration supports strong adoption of radar and ultrasonic technologies.

U.K. Level Transmitter Market

The U.K. market was valued at USD 0.061 billion in 2025 and is expected to reach USD 0.064 billion in 2026. It contributes a notable portion of market revenue, backed by oil & gas infrastructure in the North Sea, water infrastructure projects, and chemical production. Retrofit activity and compliance upgrades further sustain steady demand for modern transmitters.

Latin America

Latin America accounted for USD 0.136 billion in 2025, or approximately 6.22% of global revenues. The region’s market is supported by investments in water & wastewater systems, oil & gas terminals, chemical plants, and mining operations, which require reliable level measurement. New installation demand is driven by expanding urban infrastructure and energy projects, while retrofit activity grows as companies modernize aging equipment and integrate smarter transmitters. The average selling prices in Latin America are typically lower than in North America and Europe, reflecting a higher proportion of cost-sensitive projects and greater adoption of basic technologies. Nevertheless, the region’s ongoing industrial modernization, particularly in the energy and water sectors, ensures consistent demand. Latin America’s market share is expected to grow steadily as regional economies expand and infrastructure projects remain a priority.

Middle East & Africa

The Middle East & Africa were valued at USD 0.091 billion in 2025, with their strength rooted mainly in energy, water, and industrial infrastructure projects. In the Middle East, substantial expenditures on oil & gas production, refining, petrochemicals, and water desalination fuel consistent demand for robust level measurement solutions, particularly radar and ultrasonic technologies. In Africa, urbanization and investments in water & wastewater treatment facilities further support market uptake, although the pace varies by country. Retrofit opportunities arise as older plants are modernized, and new installations are driven by expanding energy and water utilities. The Middle East & Africa market often witnesses a blend of high-value energy projects and cost-effective solutions in municipal applications, resulting in a diversified technology mix. While overall absolute volume is smaller than in Asia Pacific or North America, the Middle East & Africa’s market share reflects significant industrial growth trends and strategic infrastructure spending across the region.

GCC Level Transmitter Market

The GCC market was estimated at USD 0.041 billion in 2025 and is likely to reach USD 0.043 billion in 2026. The GCC region (Saudi Arabia, UAE, among others.) holds a significant share driven by oil & gas production, petrochemical complexes, and water desalination projects. High deployment of radar and ultrasonic transmitters for critical process control supports its strong market role.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Players Focus on Innovation and Integrated Automation to Gain Market Advantage

Emerson Electric, Endress+Hauser, Siemens, ABB, and Yokogawa Electric are key players in this market. These companies manufacture advanced level measurement solutions, including radar, guided wave radar, ultrasonic, capacitance, and hydrostatic transmitters, and position them within broader automation portfolios that include pressure, flow, and temperature instruments. They primarily serve large-scale process industries such as oil & gas, chemicals, power generation, water & wastewater, pharmaceuticals, and food & beverage. Their strength lies in product innovation and high measurement accuracy, as well as in integrating level transmitters into Distributed Control Systems (DCS), PLC platforms, and digital asset management solutions.

In October 2025, Emerson Electric launched the Rosemount 1408H non-contact level transmitter for hygienic applications in the food and beverage sector. The device delivers precise, reliable level measurement and is engineered to handle high-temperature cleaning cycles, including CIP and SIP processes, while reducing contamination risk and supporting product safety standards.

List of Key Level Transmitter Companies Profiled

- Emerson Electric (U.S.)

- Endress+Hauser (Switzerland)

- Siemens (Germany)

- ABB (Sweden)

- Honeywell (U.S.)

- Yokogawa Electric (Japan)

- Schneider Electric (France)

- VEGA Grieshaber (Germany)

- KROHNE Messtechnik (Germany)

- AMETEK (Magnetrol) (U.S.)

- WIKA Group (Germany)

- TE Connectivity (Switzerland)

- SICK AG (Germany)

- Dwyer Instruments (U.S.)

- Flowline Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: FourKites and Chorus entered into a strategic alliance to strengthen end-to-end supply chain visibility and digital inventory control. By combining Chorus’s item-level sensing and AI-driven orchestration with the FourKites Intelligent Control Tower, the partnership enables digital twins that link real-time supply chain events with detailed package-level data. This integrated approach addresses long-standing gaps in SKU-level tracking, helping enterprises lower inventory costs, avoid stock imbalances, reduce losses, and improve overall service reliability.

- May 2025: BinMaster, a recognized leader in bulk material level measurement technology, introduced a new range of ATEX-certified rotary level indicators engineered for use in hazardous and explosive environments. Selected variants of the BMRX-100, BMRX-200, and BMRX-300 are now compliant with Class I and Class II ATEX requirements, enabling dependable performance in areas containing combustible dusts and flammable gases. This certification reinforces safe operation and expands the suitability of these models for demanding industrial applications where strict explosion-protection standards are essential.

- May 2025: Aeva secured its initial commercial orders for the Aeva Eve™ 1 series of high-accuracy sensors, designed for high-volume, inline industrial automation. Following the recent launch of the product line, the company received purchase commitments for more than 1,000 units through collaborations with established automation players such as SICK AG and LMI Technologies. These early orders highlight Aeva’s successful move into factory and process automation, extending its sensing expertise beyond automotive 4D LiDAR applications.

- April 2025: Verizon teamed up with Hyfi and the Center for Neighborhood Technology to deploy 50 flood-monitoring sensors in high-risk areas across Chicago. Operating on Verizon’s 5G network, the solar-powered water level sensors deliver real-time data to city officials and local communities through a web-based mapping platform. The system enables continuous flood visibility while reducing the need for on-site calibration or manual intervention during severe weather events.

- October 2024 - KROHNE, Inc. introduced the OPTIWAVE 1500 series, expanding its radar level measurement portfolio with the OPTIWAVE 1520 and OPTIWAVE 1540 models. These new radar level transmitters are engineered to support a wide range of industrial and municipal applications, delivering reliable performance and precise level measurement across diverse operating conditions.

REPORT COVERAGE

The level transmitter market report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.50% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Installation Type

|

|

By Technology Type

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.18 billion in 2025 and is projected to reach USD 3.01 billion by 2034.

The market is likely to grow at a CAGR of 3.50% over the forecast period (2026-2034).

By technology type, the radar segment is leading the market.

The Asia Pacific market size stood at USD 0.84 billion in 2025.

Infrastructure expansion and industrial growth are the key factors driving the market.

Some of the leading players in the market include Emerson Electric, Endress+Hauser, Siemens, ABB, and Yokogawa Electric.

The global market size is expected to reach USD 3.01 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 227

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us