X Band Radar Market Size, Share & Industry Analysis, By Component (Transmitter, Antenna, Receiver, Duplexer, and Others), By Range (Long, Medium, Short, and Very Short), By Platform (Airborne Radar, Land Radar, and Naval Radar), and Regional Forecast Report, 2026-2034

KEY MARKET INSIGHTS

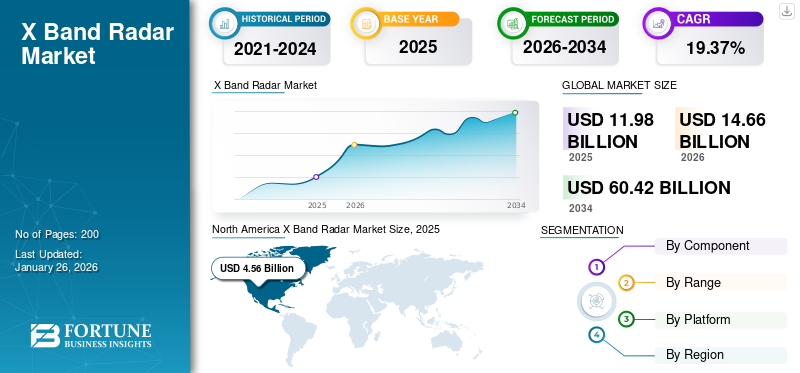

The global X band radar market size was valued at USD 11.98 billion in 2025 and is projected to grow from USD 14.66 billion in 2026 to USD 60.42 billion by 2034, exhibiting a CAGR of 19.37% during the forecast period. North America dominated the X band radar market with a market share of 38.09% in 2025.

Market Trends and Strategic Insights

- North America X band radar market held the largest share of 38.09% of the global market in 2025.

- By component, Antenna segment held the highest market share in 2024.

- By range, Short-range segment held the highest market share in 2024.

- By platform, Land radar segment held the highest market share in 2024.

Market Size and Growth Forecast

- 2025 Market Size: USD 11.98 Billion

- 2026 Market Size: USD 14.66 Billion

- 2034 Projected Market Size: USD 60.42 Billion

- CAGR (2026–2034): 19.37%

- North America: Largest market in 2025

- Asia Pacific: Fastest-growing region during the forecast period

The frequency band 8 to 12 GHz in the electromagnetic spectrum defines the parameters having a wavelength between 2.5 and 4 cm in the X band radar. It is ideally suited for high-resolution imaging that detects small details, making it highly significant for various applications. These include weather observation, air traffic monitoring, terrain-following radars, and military target tracking. Its precision and picture quality are extremely useful to the military, naval navigation, and aviation communities.

Download Free sample to learn more about this report.

The market share is dominated by the top players such as Leonardo S.p.A., Northrop Grumman Corporation, Raytheon Technologies Corporation, Hensoldt AG, and Saab AB, which cater to most end users in the market. Due to its precision and flexibility, the X band radar is heavily used in the military for various cases such as border patrol, perimeter defense, and missile guidance. It is used by ground systems and Unmanned Aerial Vehicles (UAVs) for force protection and extended-range surveillance. It can also be combined with next-generation platforms such as AESA and Gallium Nitride (GaN)-based to improve reliability and performance on most platforms. A rise in nations' defense budgets and high geopolitical tension is expected to boost product demand in the coming years.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Surveillance and Security to Boost Market Growth

The market is driven by increasing demand from the military, air, and sea sectors for state-of-the-art surveillance and security equipment. The radars can provide high-definition images and precise detection of targets, for which they are in demand for navigating missiles, border security operations, and aviation control.

Increasing spending on military modernization programs globally and growing requirements for weather monitoring systems because of global warming also drive market growth. Technological developments such as Active Electronically Scanned Array (AESA) technology and artificial intelligence integration make radar more effective and increase its usage in autonomous vehicles and disaster management.

MARKET RESTRAINTS

High Production Costs and Technological Challenges to Limit Market Expansion

The market faces high production costs and technological challenges that limit its applications. Atmospheric absorption of the radar signal hinders the range of operation, particularly during adverse weather, which undermines performance dependability. Regulatory limitations about frequency spectrum allocation also severely impede the X band radar market growth. Moreover, the highly competitive and dominant market with large and well-established aerospace and defense firms also presents entry obstacles to small or niche firms interested in innovating within this industry.

MARKET OPPORTUNITIES

Technological Advancements and Expanding Applications to Positively Impact Market Growth

The market has tremendous scope driven by technology and expanding applications. Integrating AESA technology and artificial intelligence provides enhanced target detection, energy efficiency, and predictive analysis opportunities in defense, weather monitoring, and autonomous systems. Expanding needs for lightweight, compact radar systems also create opportunities for portable applications in Unmanned Aerial Vehicles (UAVs) and automotive market segments.

Additionally, Asia Pacific and other modernizing militaries offer growth opportunities. Growth opportunities are also expanded via naval trade growth and the utilization of X band radars in naval navigation.

X BAND RADAR MARKET TRENDS

Miniaturization of Radar Systems to Act as a Major Trend and Lead to Substantial Market Growth

The X band radar industry is also experiencing gigantic technological developments shaping its growth and applications. Miniaturization of radar technology is one trend fueled by the need for smaller size, weight, and power without sacrificing equivalent performance. The technology enables Unmanned Aerial Vehicles (UAVs), drones, and portable equipment to increase their applications in defense, aviation, and disaster management.

Deployment of Gallium Nitride (GaN) technology improves radar performance through higher power efficiency and ruggedness. Also, advancement in Active Electronically Scanned Array (AESA) technology leads to improved resolution, range, and multi-target tracking. Artificial Intelligence (AI) deployment is also a game-changing trend that leads to greater signal processing, predictive analysis, and autonomous operation. These technologies are also broadening the application of these radars to defense, maritime navigation, weather surveillance, and even auto safety gadgets. Dual-use technology focus and global collaboration further speed up innovation in the area.

Impact of Russia-Ukraine War

Supply & Demand Transformation and Geopolitical & Strategic Shifts are Reshaping X Band Radar Procurement Priorities

Supply & Demand Transformation: The conflict triggered severe supply chain disruptions, notably Russia’s neon gas/palladium export bans and Ukrainian wiring harness shortages, which spiked production costs by 15–20% and delayed deliveries for Western manufacturers such as Hensoldt and/or Raytheon. Concurrently, NATO’s defense surge is driven by Ukrainian drone/artillery tactics, which reoriented procurement toward mobile, rapid-deployment X band radars such as Saab’s Giraffe 1X and HENSOLDT SPEXER, with Eastern European orders rising 200%. The war also validated the need for counter-drone integration and AI-driven electronic warfare resilience, forcing 60% of new contracts to include these features.

Geopolitical & Strategic Shifts: Geopolitically, sanctions collapsed Russia’s radar export revenue, which is creating a USD 400 million void filled by Turkish/Israeli firms and fragmented markets. The EU’s sovereignty push, such as the EDIRPA fund, prioritized homegrown AESA systems manufactured by Indra and/or HENSOLDT, while U.S. suppliers gained Eastern European market share via Foreign Military Sales. Long-term, the conflict compressed procurement cycles from 5–7 years to less than 3 years for modular systems and pivoted R&D toward cost-effective, attrition-replaceable radars. This realignment emphasized open architecture, coalition interoperability, such as EU Sky Shield, and stricter export controls, permanently altering defense industrial priorities.

Segmentation Analysis

By Component

Increased Demand for Accurate Surveillance Systems to Foster Antenna Segment Growth

Based on component, the market is classified into transmitter, antenna, receiver, duplexer, and others.

The antenna segment accounted for a dominating market share and is expected to grow at the highest CAGR in the coming years. Component development within the market is driven by expanding demand for high-performance radars in weather observation systems, aviation, and defense. Rising request for lightweight and compact antennas in versatile frameworks and Unmanned Aerial Vehicles (UAVs) drives market growth. Antennas are responsible for transmitting and receiving electromagnetic waves, which enable the detection of exact targets and high-definition images.

The transmitter segment is expected to witness steady growth over the forecast period. The demand for X band radar system transmitter components is increasing since they play a vital role in the production of high-frequency electromagnetic waves needed for radar operation. Developments in transmitters, such as GaN-based systems, have enhanced energy efficiency and power signal, making radars operate efficiently in harsh environments. Increasing military modernization programs and sophisticated surveillance technologies spur demand for reliable transmitters to ensure long-range detection and accurate targeting. Transmitters in miniature radar systems also have broader applications in UAVs and mobile X band radar. These technologies span industries, including border patrol, weather surveillance, and air traffic control.

By Range

Surging Need for Secure and Effective Management of Airspace Boosted Short Segment Growth

Based on range, the market is divided into long, medium, short, and very short.

The short segment accounted for the larger share of the market in 2024. Short-range X-band radar development is necessitated by the high-resolution image capability needed in air traffic control, weather observation, and security perimeter applications. The radars are suited for small object detection and high-resolution imaging at short ranges, which can be used in urban monitoring and disaster management applications. Expanded airport development globally and air traffic expansion also necessitate short-range systems for secure and effective airspace management. Miniaturization technologies and phased arrays promise to integrate small packages, such as UAVs and drones, with expanding applications across various industries.

The long segment is expected to continue to account for a considerable share of the market and is expected to grow at the highest CAGR in the forthcoming years. The long-range X-band radar development is driven by its key usage in defense operations such as missile detection, border patrol, and naval battles. Such radars provide high-range and precise tracking, pivotal to national security following increasing geopolitical tensions. Military modernization expenditures globally have primarily driven demand for next-generation long-range radar systems. Apart from that, their use in weather forecasting allows real-time tracking of menacing weather patterns over wide areas. Among technologies, Gallium Nitride (GaN)-based transmitters enhance signal power and dependability to perform at optimal levels under difficult conditions.

By Platform

Rising Geopolitical Tensions and Surge in Defense System Applications Propelled Land Radar Segment Growth

Based on platform, the market is divided into airborne radar, land radar, and naval radar.

The land radar segment accounted for the largest market share in 2024, driven by its intrinsic position in defense systems such as missile defense systems, border surveillance, and ground air traffic controllers. Radars facilitate short- to medium-range high-intensity target detection and tracking, a necessity for national security and situational awareness. Geopolitical tensions and military modernization have triggered record spending on ground radar systems worldwide. Additionally, the greater use of land-based radars in weather forecasting and disaster relief missions makes it necessary to utilize them in civilian applications. Greater emphasis on development in infrastructure in emerging economies also creates greater demand for rugged and multi-mission land-based radar systems for multiple applications.

The airborne radar segment is projected to account for a considerable market share and is expected to grow at the highest CAGR in the forthcoming years. Airborne radar growth is driven by increasing demand for advanced surveillance and reconnaissance systems from the aerospace and defense industries. Radars are commonly used in manned and unmanned aerial vehicles (UAVs) for border patrol, threat detection, and missile guidance. Applications of UAVs with lightweight and compact radars have been responsible for increased market growth. Technological innovation, such as AESA technology, enhances airborne radar performance with high-definition images and multiple target tracking capabilities. Additionally, the growing investment in military modernization programs worldwide and the need to offer solutions to air safety measures, such as collision avoidance, propel the growth in the market. Its application in weather watch and disaster relief applications also implies that the radars operate with zero downtime under adverse conditions.

X Band Radar Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America X Band Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 38.09% to the global market in 2025, with a valuation of USD 4.56 billion, and is projected to reach USD 5.57 billion in 2026, owing to colossal defense modernization spending, mostly in the U.S. The Department of Defense for the U.S. continually advances research for cutting-edge radar technology with investments in air sensing, missile protection, and safeguarding of frontiers. Large employers such as Raytheon and Northrop Grumman create professional opportunities for specialized individuals and opportunities for exposure to newer systems. Apart from this, X band radars are also extensively used in non-defense sectors such as meteorology, aviation security, and relief after disasters. The region's ambitions toward technical superiority and strong security machinery also fuel further market growth.

Europe

Europe accounted for USD 3.64 billion in 2025, representing 30.35% of the global market share, and is projected to reach USD 4.46 billion in 2026. Europe registers the second-largest position in the market due to enormous expenditure on defense technology and systems. France, Germany, and the U.K. use X band radars to defend against missiles, manage airplane traffic flow, and aid naval operations. Saab and Thales are two of the firms that improve radar performance by creating radar efficiency using technologies such as AESA. Weather forecasting and aviation security also drive it. The European regional security and infrastructure development interest guarantees stable market growth.

Asia Pacific

The Asia Pacific market was valued at USD 2.43 billion in 2025, capturing 20.27% of global revenue, and is estimated to reach USD 3.03 billion in 2026. The growth is due to the defense program modernization of China, India, and Japan. Geopolitical tensions are increasing, calling for investment in naval monitoring radar systems, border defense, and disaster relief systems. The application of lightweight radars in UAVs is also fueling the demand. Also, the region's focus on advanced weather observation networks is fueling growth. Asia Pacific's focus on technology and economic development places it in the vanguard of the world market leaders.

Rest of the World

The Rest of the World market is expected to witness considerable growth in the near future. Market expansion in the region is driven by increased adoption of naval navigation, border surveillance, and disaster preparedness. Emerging nations spend on radar technology to support defense systems and offset climate concerns with weather observation systems. Expansion in naval trade increases demand sea sea-based X band radars for secure navigation. Strategic partnerships with leading manufacturers ensure access to high-tech solutions for regional specifications, contributing to constant market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Technological Innovations by Key Companies Resulted in Their Dominating Positions in Market

Key players such as Raytheon Technologies, Thales Group, Northrop Grumman, and Leonardo SpA possess positive experience in the defense and aerospace sectors. They spend massively on R&D for radar capability development and maintain market dominance. Small companies and new players are drawn in by the market development potential and thus pump in competition. Furuno Electric Co., Ltd. and Japan Radio Co., Ltd. provide market diversification. Business corporations in product innovation and global domination are rising. Collaboration, for instance, expands the volume of products and market access and makes the market competitive.

LIST OF KEY X BAND RADAR COMPANIES PROFILED

- BAE Systems plc. (U.K.)

- Hanwha Systems Co. Ltd. (South Korea)

- Hensoldt AG (Germany)

- Honeywell International Inc. (U.S.)

- Israel Aerospace Industries Ltd. (Israel)

- L3Harris Technologies, Inc. (U.S.)

- Leonardo S.p.A (Italy)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Saab AB (Sweden)

KEY INDUSTRY DEVELOPMENTS

- December 2024: Saab AB received a contract of USD 41.6 million from Försvarets materielverk (FMV - Swedish Defence Materiel Administration) to supply Sea Giraffe 1X X-Band radar system to the Swedish Naval Forces. The deliveries expected between 2024 and 2026 will include radars in various configurations for training and installation on naval vessels.

- September 2024: Raytheon, an RTX business, delivered the first AN/TPY-2 radar for the Kingdom of Saudi Arabia. The AN/TPY-2 is a missile defense radar that can distinguish, track, and segregate ballistic missiles in multiple stages of flight.

- August 2024: The Tamil Nadu government announced the installation of two additional Doppler radars in Chennai. The radar installation is expected to bring clarity in terms of preparations for the early detection of potential cyclones at the coast.

- June 2024: Terma, a worldwide leading supplier of radar systems, unveiled a critical contract to supply four SCANTER 6002 maritime surveillance radars for the 2 Belgian and 2 Netherlands Naval Force Anti-Submarine Warfare frigates.

- June 2024: GalaxEye Space, a space-tech startup at the forefront of multi-sensor imaging satellites, unveiled a partnership with SkyFi, a leading platform that simplifies access to Earth observation imagery and enables users with effective analytics tools. GalaxEye's technology prepares satellites with Synthetic Aperture Radar (X-band) and Optical/Multispectral Imaging (MSI) capabilities.

REPORT COVERAGE

The global market analysis provides market size & forecast by all the segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the prevalence of malocclusion in key regions/countries, key industry developments, new product launches, details on partnerships, and mergers & acquisitions. It covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 19.37% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Range

|

|

|

By Platform

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.98 billion in 2025 and is projected to record a valuation of USD 60.42 billion by 2034.

In 2025, the market value stood at USD 11.98 billion.

The market is projected to exhibit a CAGR of 19.37% during the forecast period of 2026-2034.

The land radar segment led the market by platform.

Rising demand for advanced surveillance and security is anticipated to lead to substantial growth.

Raytheon Technologies, Thales Group, and Northrop Grumman are major companies operating in the market.

North America holds the largest market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us