Natural Gas Compressor Market Size, Share & Industry Analysis, By Compressor Type (Centrifugal, Reciprocating, Rotary, and Others), By Displacement (Dynamic Displacement and Positive Displacement), By Lubrication (Oil-based and Oil-free), By Pressure Rating (Low, Medium, and High), By End User (Oil & Gas, Power Generation, Chemical & Petrochemical, Manufacturing, Mining, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

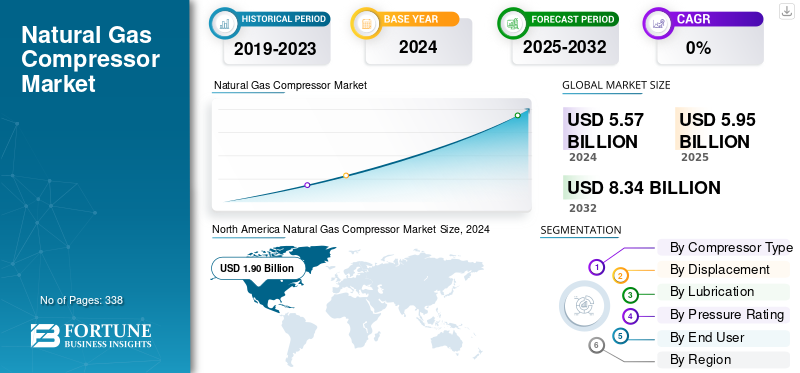

The global natural gas compressor market size was valued at USD 5.95 billion in 2025. It is projected to grow from USD 6.33 billion in 2026 to USD 8.95 billion by 2034, exhibiting a CAGR of 4.43% during the forecast period. North America dominated the natural gas compressor market with a market share of 34.13% in 2025.

A natural gas compressor is a mechanical device designed to increase the pressure of natural gas by reducing its volume. This process is essential for efficient transportation, storage, and processing of gas across various stages of the energy value chain. Compressors are commonly used in production facilities, gas gathering systems, transmission pipelines, and storage sites to maintain optimal flow and pressure levels. Depending on the application, they can operate using different mechanisms such as reciprocating, centrifugal, rotary screw, or diaphragm compression. These units are typically powered by gas turbines, electric motors, or internal combustion engines. By ensuring the continuous and safe movement of natural gas from production wells to end users, compressors play a critical role in the reliability and efficiency of the global natural gas infrastructure.

Atlas Copco has established itself as a global leader through continuous innovation in energy-efficient and oil-free gas compression technologies. The company focuses on developing compressors that reduce environmental impact by lowering emissions and improving energy recovery systems. Atlas Copco has expanded its product range to serve diverse applications from natural gas processing and pipeline transportation to storage and industrial gas solutions. The company invests heavily in R&D for digital monitoring and smart compressor systems, enabling predictive maintenance and higher operational reliability. Additionally, through acquisitions of specialized gas and vacuum solution providers, Atlas Copco strengthens its global presence and offers end-to-end solutions that enhance performance, safety, and sustainability across the natural gas value chain.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Natural Gas in Power Generation and Industrial Applications to Drive Market Growth

The global shift toward cleaner energy sources has led to a significant increase in natural gas consumption, especially in power generation and industrial sectors. Natural gas emits approximately 50% less CO₂ than coal when used for electricity production, making it a preferred choice for countries transitioning to low-carbon energy. This surge in demand has driven the need for efficient gas compression systems to transport and store gas over long distances. For instance, the U.S. Energy Information Administration (EIA) reported that natural gas accounted for about 40% of U.S. electricity generation in 2023, up from 35% in 2019. This increasing usage directly boosts the requirement for compressors in pipelines, storage facilities, and LNG terminals, positioning them as critical infrastructure components for ensuring energy supply reliability.

Expansion of Natural Gas Infrastructure and Pipeline Networks to Propel Market Growth

Another major factor that drives the demand for natural gas compressors is the rapid development and expansion of natural gas infrastructure, particularly pipelines and LNG terminals, across emerging and developed markets. Countries in Asia Pacific, such as India and China, are heavily investing in new pipeline networks to meet rising urban and industrial gas demand. For example, India’s Pradhan Mantri Urja Ganga project aims to expand over 2,540 km of pipeline to deliver natural gas to eastern regions of the country in 2020. Similarly, global LNG trade has grown steadily, with world LNG imports reaching 450 million tonnes in 2022, necessitating compressors for both transport and storage. The growing infrastructure requires high-capacity, reliable compressors to maintain pipeline pressure and ensure efficient gas distribution, directly driving demand for natural gas compressor systems.

MARKET RESTRAINTS

Stringent Safety and Regulatory Requirements to Constrain Market Growth

The natural gas compressor industry faces strict safety, environmental, and operational regulations, which can act as a restraint on market growth. Compressors must comply with standards related to pressure containment, emissions, and noise, such as ASME, API, and ISO certifications. Non-compliance can result in fines, operational shutdowns, or reputational damage. For instance, in the U.S., Pipeline and Hazardous Materials Safety Administration (PHMSA) enforces rigorous pipeline and compression station regulations, adding complexity and cost to projects. These regulatory pressures can limit rapid deployment, especially in regions with evolving or strict standards.

MARKET OPPORTUNITIES

Growth in LNG and Offshore Gas Projects to Offer Lucrative Opportunities for Market Players

The increasing global demand for liquefied natural gas (LNG) and offshore gas production presents significant opportunities for natural gas compressors. LNG facilities require large-scale compression systems for gas liquefaction and storage, while offshore projects need compact, high-performance compressors suitable for remote and harsh environments. For example, the Golden Pass LNG terminal in the U.S. and the Ichthys LNG project in Australia involve extensive use of high-capacity compressors to maintain continuous gas flow. Expanding LNG trade, which reached 450 million tonnes globally in 2022, creates a sustained need for advanced compressor technologies, allowing companies to introduce innovative solutions such as modular, high-efficiency, and low-maintenance compressors.

MARKET CHALLENGES

High Capital and Maintenance Costs to Hinder Market Growth

One of the key challenges in the natural gas compressors market is the high initial investment and ongoing maintenance costs. Compressors, especially high-capacity or specialized oil-free units, require significant capital outlay for purchase, installation, and commissioning. In addition, maintenance involves skilled labor, spare parts, and periodic overhauls to ensure reliability, particularly in harsh environments such as offshore or desert pipelines. For example, a large reciprocating compressor for a major pipeline can cost several million dollars, with annual maintenance expenses reaching 5–10% of the initial cost. These high costs can slow adoption, especially for smaller operators or projects in emerging markets.

NATURAL GAS COMPRESSOR MARKET TRENDS

Adoption of Energy-Efficient and Oil-Free Compressors to Lead Market Growth

The natural gas compressor industry is increasingly moving toward energy-efficient, oil-free compressors to reduce operational costs and environmental impact. Oil-free compressors prevent contamination in gas pipelines and storage systems, which is critical for industries such as LNG processing and petrochemicals. Leading companies, such as Atlas Copco and Ingersoll Rand, are incorporating variable speed drives (VSDs) and advanced monitoring systems to optimize energy usage. According to the International Energy Agency (IEA), industrial energy efficiency improvements could reduce global electricity demand up to 10% by 2030, highlighting the importance of adopting energy-efficient equipment. This trend reflects a growing industry focus on sustainability and cost-effective operation in compressor technologies.

Download Free sample to learn more about this report.

IMPACT OF TARIFF ON THE MARKET

The imposition of tariffs on imported natural gas compressors can significantly affect the global market by influencing pricing, supply chains, and competitiveness. Higher import duties increase the cost of compressors for end-users, particularly in regions that rely on imported equipment, which may slow down infrastructure expansion and delay new projects. For instance, countries with ambitious pipeline or LNG projects may face budgetary constraints if tariffs raise the cost of acquiring high-capacity or specialized compressors. Additionally, tariffs can prompt manufacturers to shift production closer to key markets or seek local partnerships to avoid extra costs, potentially altering global trade dynamics. While domestic manufacturers may benefit from reduced foreign competition, end-users could face higher operational costs and limited choices, ultimately impacting market growth and investment decisions.

SEGMENTATION ANALYSIS

By Compressor Type

Growing Requirement in Large-Scale Gas Transmission Pipelines Boosted the Centrifugal Segment Growth

By compressor type, the market is segmented into centrifugal, reciprocating, rotary, and others. The centrifugal segment is projecteed to dominate the market with a share of 46.45% in 2026. driven by their suitability for large-scale gas transmission pipelines, midstream processing facilities, and LNG applications where high flow rates and continuous operation are required. These compressors have fewer moving parts and comparatively lower maintenance needs, making them cost‐efficient over long operating periods. Their scalability and efficiency in handling large gas volumes make them the preferred choice for major energy infrastructure projects.

Rotary segment is growing at the fastest rate of 6.41% in the global market, favored for their use in low‐pressure and low‐flow applications such as small industrial natural gas fueling stations, on-site processing units, and localized distribution systems. Rotary screw and scroll variants offer compact design, stable continuous output, and quiet operation. However, they are not typically used in large pipeline transmission or long-haul gas networks due to their capacity limitations, which keeps their market share moderate.

By Displacement

Increasing Demand in Midstream and Downstream Applications Boosted Dynamic Displacement Segment's Growth

Based on displacement, the market is divided into dynamic displacement and positive displacement. The dynamic displacement segment is projecteed to dominate the market with a share of 56.24% in 2026 driven by their extensive use in midstream and downstream applications such as long-distance pipeline transmission, large gas processing plants, and LNG facilities. These compressors operate by continuously accelerating gas and converting its velocity into pressure, allowing them to handle very high flow volumes efficiently. They also benefit from lower maintenance demands over long operating cycles due to fewer mechanical contact points. Their strong performance in large-scale, continuous-duty environments supports their leading position in the market.

The positive displacement segment hold a smaller share but are expanding at the fastest rate of 5.38%. The segment is gaining traction as these compressors work by physically trapping gas in a chamber and mechanically reducing its volume to increase pressure, making them well-suited for upstream operations, gas gathering systems, and localized distribution needs. These compressors are valued for their ability to deliver high pressure across variable flow ranges, performing reliably in both intermittent and continuous operations. Although they generally require more frequent maintenance due to a higher number of moving components, their flexibility, lower initial cost, and adaptability to fluctuating field conditions ensure consistent demand, particularly in exploration, production, and smaller industrial gas applications.

By Lubrication

Heavy-duty Workloads Boosts the Oil-based Segment's Growth

As per lubrication, the global natural gas compressor market is broadly segmented into oil-based, and oil-free. The oil-based segment is projecteed to dominate the market with a share of 81.36% in 2026, as these systems rely on lubricating oil to reduce friction between moving parts, which enhances durability and efficiency. They are widely used in upstream extraction sites, gas gathering systems, and transmission pipelines where reliability under high pressure and continuous operation is essential. The ability of oil-based compressors to handle heavy-duty workloads and variable gas compositions makes them the preferred choice in harsh field environments. However, they require periodic maintenance and monitoring to prevent oil carryover into the gas stream, especially in sensitive applications.

Oil-free is experiencing fastest growth rate of 6.21% due to their growing adoption in downstream segments and applications where gas purity is crucial, such as LNG processing, chemical feedstock handling, and specialty industrial gas use. These compressors eliminate the risk of oil contamination, which reduces the need for additional gas treatment units and improves product quality consistency. While oil-free compressors generally have higher initial costs and may require more advanced materials to prevent wear, their benefits in cleanliness, reduced filtration requirements, and compliance with stringent purity standards are supporting increased penetration, particularly in regulated and high-specification gas processing environments.

By Pressure Rating

Stable Compression Ability Boost the Medium Segment's Growth

Based on pressure rating, the global natural gas compressor market is segmented into low, medium, and high. Medium segment will account for 50.24% market share in 2026, as they are widely deployed across midstream transportation systems, processing plants, and industrial supply networks where gas is moved between regional hubs or conditioned for end-use. Their ability to provide stable compression across sustained duty cycles makes them essential for maintaining pipeline pressure and ensuring distribution efficiency. The versatility of medium-pressure compressors-balancing output performance, energy efficiency, and maintenance practicality, supports their broad adoption in both onshore and offshore natural gas infrastructure.

High is growing at a cagr of 5.55% and is considered the fastest-growing segment as these are essential in operations requiring significant pressure build-up, such as gas re-injection into reservoirs, LNG processing, CNG fueling stations, and storage applications. These compressors are engineered to handle demanding environments and compress gas to very high pressures safely and efficiently. While they entail higher capital and maintenance costs due to the advanced materials and safety mechanisms required, their critical role in maximizing gas recovery and supporting high-demand applications ensures consistent use in specialized segments of the natural gas value chain.

By End User

To know how our report can help streamline your business, Speak to Analyst

Growth in Unconventional Gas Production Spurred Oil & Gas Segment’s Growth

In terms of end user, the market is segmented into oil & gas, power generation, chemical & petrochemical, manufacturing, mining, and others. The oil & gas segment holds the largest market share, approximately 56.30%. Compressors are integral across the upstream, midstream, and downstream stages for gas lifting, gathering, processing, transmission, and re-injection. Growth in unconventional gas production, pipeline network expansion, and LNG infrastructure continues to support strong compressor deployment in this sector. The need for continuous operation under high pressures also drives the preference for durable and efficient compressor systems in oil & gas applications.

Power generation is the fastest-growing segment, surging at a rate of 6.20% in the global market. Natural gas-fired power plants use compressors to regulate gas flow and pressure for turbines and combined-cycle power units. As more regions shift from coal to gas-based power to meet emission reduction goals, this segment is expected to expand steadily. The emphasis on stable load operation and efficiency in gas-fired electricity generation continues to support strong compressor demand in this category.

NATURAL GAS COMPRESSOR MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, and Latin America, and the Middle East & Africa.

North America Natural Gas Compressor Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America represented USD 2.03 Billion, accounting for 34.13% of the worldwide market, and is projected to grow to USD 2.17 Billion in 2026. The U.S. alone produced over 1,000 billion cubic meters of natural gas in 2023, driven by shale basins such as the Permian, Marcellus, and Haynesville. This high production volume requires extensive compression for gas gathering, processing, and pipeline transmission. Additionally, the U.S. has emerged as a major global LNG exporter, with liquefaction capacity exceeding 90 million tonnes per year, further increasing compressor demand in midstream and LNG facilities. Continuous upgrades of inter-state gas pipeline networks and rising natural gas-fired power generation also reinforce compressor deployment across the region. The U.S. holds a market value of USD 1.78 billion in 2026.

Asia Pacific

Asia Pacific contributed 28.37% to the global market in 2025, with a valuation of USD 1.69 Billion, and is projected to reach USD 1.81 Billion in 2026. The Asia Pacific region is the fastest-growing region, expected to expand at a CAGR of 5.91% during the forecast period. This growth is driven by rising natural gas consumption in China, India, and Southeast Asia as these economies shift toward cleaner fuels. China alone has expanded its natural gas pipeline network to over 120,000 kilometers, requiring large-scale compressor installations. Meanwhile, India’s city gas distribution expansion has led to a rapid increase in CNG stations (now over 5,000 nationwide), directly supporting demand for high-pressure gas compressors. LNG import growth across Japan, South Korea, and emerging ASEAN markets further adds to midstream compressor requirements. Leading countries such as China, India, and Japan represents USD 0.73 billion, USD 0.38 billion, and USD 0.17 billion in 2025.

Europe

The Europe market generated USD 0.76 Billion in 2025, representing 12.76% of the global market landscape, and is expected to reach USD 0.8 Billion in 2026. Europe is expected to grow at a considerable rate, driven by the expansion of gas storage and LNG import infrastructure aimed at diversifying supply sources away from Russian pipeline gas. For example, several new LNG regasification terminals were commissioned in Germany, Poland, and the Netherlands since 2022. Many European countries are also modernizing aging transmission pipelines to improve efficiency and reduce methane leakage, which increases the requirement for performance-oriented compressors. Moreover, natural gas still accounts for about 20% of Europe’s total energy mix, supporting stable industrial and power-sector demand. Leading countries such as U.K., Germany, and France holds a market value of USD 0.08 billion, USD 0.14 billion by 2026 and USD 0.06 billion, respectively, in 2025.

Latin America

The market in Latin America reached USD 0.99 Billion in 2025, representing 16.54% of total market revenue, and is projected to reach USD 1.04 Billion in 2026. In Latin America, natural gas compressor adoption is still in its early stages but is gaining momentum. Countries such as Brazil and Argentina are increasing natural gas utilization for power generation and industrial feedstock. Argentina’s Vaca Muerta shale development is expanding natural gas output, leading to new pipeline and processing facility installations that require compressors. Brazil’s offshore pre-salt gas fields also rely heavily on compression systems for subsea gas lifting, processing, and reinjection. While infrastructure development is advancing, the pace of investment varies by country, keeping the regional share modest but gradually rising.

Middle East

The Middle East & Africa market was valued at USD 0.49 Billion in 2025, capturing 8.20% of global revenue, and is estimated to reach USD 0.51 Billion in 2026. The Middle East holds some of the world’s largest natural gas reserves, with compression systems are widely used for gas reinjection in enhanced oil recovery (EOR) and long-distance transmission. Qatar’s LNG expansion program, which is projected to increase liquefaction capacity to over 130 million tonnes per year, is a major driver of high-capacity compressor demand. In Africa, countries such Algeria, Egypt, and Mozambique are developing gas fields and export infrastructure, supporting gradual natural gas compressor market growth as new pipelines and processing hubs come online. The combined region is likely to hold a market value of USD 0.49 billion in 2025, with the GCC countries alone accounting for about USD 0.27 billion.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Strategic Efforts to Optimize Operational Efficiency

Atlas Copco has established itself as a leading player in the natural gas compressor market through a combination of innovation, technological advancements, and global reach. The company focuses on developing energy-efficient, oil-free, and high-performance compressors that meet the stringent requirements of gas transportation, processing, and storage applications. Its efforts include integrating advanced digital monitoring, predictive maintenance, and variable speed drive technologies to optimize operational efficiency and reduce downtime for clients. Atlas Copco also emphasizes sustainability, designing compressors that minimize emissions and energy consumption. Moreover, the company has expanded its global footprint through strategic acquisitions and localized manufacturing, enabling it to serve diverse markets efficiently while maintaining strong after-sales support. These combined efforts in innovation, reliability, sustainability, and customer-centric solutions have solidified Atlas Copco’s leadership position in the natural gas compressor industry.

List of the Key Natural Gas Compressor Companies Profiled

- Baker Hughes (U.S.)

- Siemens Energy (Germany)

- Solar Turbines (U.S.)

- MAN Energy Solutions (Germany)

- Atlas Copco (Sweden)

- Burckhardt Compression (Switzerland)

- Ariel Corporation (U.S.)

- Mitsubishi Heavy Industries (MHI) (Japan)

- Elliott Group (U.S.)

- Howden (U.K.)

- Ingersoll Rand (U.S.)

- Kobelco (Japan)

- BORSIG (Germany)

- Bauer Compressors (Germany)

- Shaanxi Blower Group (China)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Everllence entered into an agreement with MT Group to supply a 5 MW hermetically sealed MOPICO motor-driven pipeline compressor that features integrated magnetic bearing technology. The unit is planned for installation at the Jauniunai compressor station in Lithuania, where it would be operated by AB Amber Grid, the national operator responsible for managing the country’s natural gas transmission network.

- In October 2025, Knox Western, a long-established U.S. producer of reciprocating gas compressors, formed a new strategic partnership with KB Delta. Under this agreement, KB Delta would manufacture all Knox Western-designed valves and valve internals used in its compressor units. The partnership supports Knox Western’s broader efforts to modernize its production capabilities, strengthen its footprint in the North American market and enhance its competitiveness in both the traditional natural gas sector and emerging energy transition applications.

- In April 2025, Burckhardt Compression received a contract in Sweden from a major gas operator to supply its MD10-L compressor package for hydrogen trailer filling operations. The order supports the company's ongoing efforts to advance hydrogen mobility and related infrastructure. The MD10-L system is a standardized, containerized solution designed for high-pressure hydrogen use, offering a pre-tested, plug-and-play setup that simplifies installation and deployment. Delivery of the package is planned for 2025, in line with the project’s timeline.

- In March 2025, Archrock, Inc. announced that it has signed definitive agreements to acquire Natural Gas Compression Systems, Inc. (NGCSI) in a cash-and-stock deal valued at about USD 357 million. The transaction would expand Archrock’s contract compression service capabilities with the addition of NGCSI’s high-quality equipment and operational footprint.

- In January 2025, Petrofac received more than USD 330 million contract from ADNOC Gas to build a new gas compressor facility at the Habshan Complex in Abu Dhabi. The project would help increase output and supply pre-conditioned gas to the Ruwais LNG project. This marks Petrofac’s third EPC award at Habshan. The scope includes installing two compressor trains and supporting utilities, with completion targeted for 2028.

REPORT COVERAGE

The report delivers a detailed insight into the market and focuses on key aspects, such as leading companies. Besides, it offers insights into the market trends & technologies and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors and challenges that have contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.43% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Compressor Type

|

|

By Displacement

|

|

|

By Lubrication

|

|

|

By Pressure Rating

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 5.95 billion in 2025.

The market is likely to record a CAGR of 4.43% over the forecast period (2026-2034).

By end user, the oil & gas segment leads the market.

The North America market size was valued at USD 2.03 billion in 2025.

Rising Demand for natural gas in power generation and industrial applications is the key factor driving the markets growth.

Some of the key players in the market are Atlas Copco, Baker Hughes, Howde, Ingersoll Rand, and others.

The global market size is expected to reach a valuation of USD 8.95 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 338

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us