Location Intelligence Market Size, Share & Industry Analysis, By Component (Solution and Services), By Technology (GPS, GIS, Beacons & RFID, Wi-Fi & Bluetooth-based Positioning, and Satellite Imagery & Remote Sensing), By Application (Mapping & Visualization, Spatial Analytics, Geofencing & Geotargeting, Asset Tracking & Management, Workforce & Resource Management, and Others), By End User (Retail & E-commerce, BFSI, IT & Telecom, Healthcare, Government & Defense, Transportation & Logistics, Energy & Utilities, and Others), and Regional Forecast, 2026-2034

LOCATION INTELLIGENCE MARKET SIZE AND FUTURE OUTLOOK

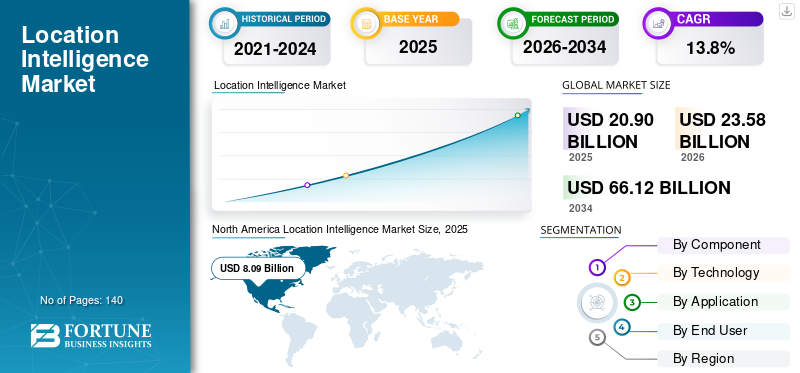

The global location intelligence market size was valued at USD 20.90 billion in 2025. The market is projected to grow from USD 23.58 billion in 2026 to USD 66.12 billion by 2034, exhibiting a CAGR of 13.8% during the forecast period. North America dominated the location intelligence market with a market share of 38.70% in 2025.

Location intelligence refers to the use of geospatial data and location-based analytics to derive actionable insights that help organizations optimize business processes, improve decision-making, and enhance customer experiences. By making use of geographical patterns, Global Information System (GIS) provides a wide variety of organizations, such as retail, distribution, transportation, healthcare, public safety, and real estate industries, with the tools necessary to manage resources, enhance productivity, and obtain forecast information. A major driving factor is the increasing reliance by businesses on data-driven decision-making through the introduction of GIS. GIS assists organizations in improving their operational performance, better targeting potential customers, and managing risk by providing real-time geospatial analytics for improving productivity of their operations. This factor plays an important role in fueling the market growth.

Furthermore, many key industry players, such as Google LLC, Esri, HERE Technologies, TomTom International BV, and Microsoft, operating in the market, are increasingly focusing on expanding into emerging regions such as Southeast Asia, Latin America, and the Middle East. The growing demand for data-driven decision-making in industries such as retail, logistics, urban development, and agriculture presents a significant opportunity.

Download Free sample to learn more about this report.

Location Intelligence Market Key Takeaways

- 2025 Market Size: USD 20.90 billion

- 2026 Market Size: USD 23.58 billion

- 2034 Forecast Market Size: USD 66.12 billion

- CAGR: 13.8% from 2026–2034

- North America dominated the location intelligence market with a market share of 38.70% in 2025.

- The services segment is expected to witness the fastest growth, registering a CAGR of 18.3% during the forecast period.

- The Wi-Fi & Bluetooth-based positioning segment is projected to grow at the highest CAGR of 17.7% through 2034.

North America

North America led the market with a value of USD 8.09 billion in 2025, supported by strong adoption of cloud- and AI-enabled geospatial analytics across industries.

Europe

Europe is projected to reach USD 6.07 billion in 2026, driven by growing demand for interoperable geospatial data, sustainability initiatives, and spatial analytics applications.

Asia Pacific

Asia Pacific is estimated to attain USD 5.28 billion in 2026 and is expected to record the highest regional CAGR due to rapid urbanization, infrastructure development, and smart city projects.

U.S.

The U.S. market is estimated at approximately USD 7.24 billion in 2026, accounting for around 30.7% of global revenue, supported by extensive enterprise adoption and digital transformation initiatives.

Japan

The Japan market is estimated to reach around USD 1.00 billion in 2026, accounting for roughly 4.2% of global revenues.

Read More

IMPACT OF GENERATIVE AI

Integration of Generative AI to Enhance Spatial Analytics Capabilities and Drive Market Growth

The market is experiencing significant acceleration due to generative AI (GenAI), which is enabling faster and easier access to geospatial work for non-experts as well as improving organizations’ ability to derive insights from a variety of sources, including maps, sensor feeds, and images. Instead of requiring specialist geographic information systems (GIS) workflows, GenAI enables the natural-language querying of spatial datasets, faster creation of maps and spatial analyses, automated feature extraction from satellite or street-level imagery, and quicker production of decision-ready narratives for operations teams. As a result, GenAI expands the range of organizations that adopt geospatial capabilities through areas such as supply chain management, marketing, risk management, field service, and public sector planning, thereby expanding platform usage, data consumption, and demand for implementation services. For instance,

- In October 2025, Microsoft introduced Maps in Fabric for geospatial insights inside its analytics stack, reinforcing the trend of embedding geospatial and AI-driven workflows directly into enterprise BI and real-time intelligence environments.

Overall, generative AI is strengthening the market by providing greater accuracy via synthetic data creation, enabling real-time and contextually aware spatial analyses. It also enables easier user access to geospatial systems and provides additional applications in the smart city, logistics, public safety, and infrastructure planning areas.

LOCATION INTELLIGENCE MARKET TRENDS

Growth in Logistics, Delivery, and Last-mile Optimization to Create New Market Opportunities

The logistics, delivery, and last-mile optimization growth trends have driven the widespread usage of location intelligence as the economics of delivery depends on precision at the street level. Location analytics are being used by companies to refine ETA accuracy, decrease failed deliveries, redesign delivery zones, and optimize multi-stop routes based on traffic patterns, customer densities, and service time variations. For instance,

- In July 2025, Flipkart announced that it would expand its 10-minute rapid commerce service, Flipkart Minutes, into tier II and tier III cities with the backing of USD 393 million in funding. It intends to increase its dark store count from 400 to 800, take advantage of AI-driven logistics, utilize location intelligence, and provide multi-speed delivery options to compete with non-metro markets.

Micro-fulfilment and dark store placement decisions are contributing to an increased product demand for high-density ordering clusters and balancing speed and the cost of order fulfilment. Rising fuel and labor prices, as well as higher customer expectations for same-day/by-time-slot deliveries, are driving logistics companies to use continuous and real-time geospatial decision-making methods versus static route planning forms.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand in Retail and Store Expansion to Drive the Market

The growth in retail demand coupled with a number of store expansion programs have driven the demand for location intelligence solutions in part owing to the tight capital environment and increased scrutiny of retailer performance. Retailers are no longer using historical brand presence or regional averages to make expansion decisions. Instead, they are evaluating true demand pockets, consumer movement patterns, and competition at the street and neighborhood levels. For instance,

- In June 2025, according to industry experts’ survey, 58% of retail professionals believe that sharing customer location data with partners boosts revenue.

Location intelligence will allow retailers to expand more consistently and develop a business case that justifies the profitability and financial sustainability of future expansion opportunities. The technology enables retailers to quantify true catchment area strength, identify white space locations versus over-served areas, and help reduce the potential for competition to cannibalize sales from one outlet to another within the same area. In addition, the use of this solution will allow retailers to assess how close they are to office buildings, residential developments, schools, and lifestyle centers, driving location intelligence market growth. This enables them to understand how each of those components affects the daily and weekly demand for that facility, which will result in more accurate site scoring and format selection. For instance,

- In November 2025, Taptap Digital launched Retail Origins, a location intelligence driven solution that uses consented mobility data to reveal where store visitors live and work and where they overlap with competitors. The tool helps physical retailers sharpen targeting, improve omnichannel campaign performance, and make smarter location-based investment decisions.

MARKET RESTRAINTS

Data Privacy and Regulatory Constraints May Hinder the Market Growth

Solutions data utilizes a combination of collection, processing, and analysis of highly sensitive geospatial and mobility data. Due to the increasing control over data protection and privacy, this area of technology has faced a surge in governing legislation and regulations for how geospatial and mobility data is handled globally around the world. Legislative and regulatory frameworks experienced in the U.K. through the EU's General Data Protection Regulation (GDPR), in the U.S. through the CCPA and CPRA, and numerous federal and state-level data laws and regulations across the global landscape are placing significant restrictions on the collection, retention and processing of user data with strict requirements on areas heavily relied upon by users. For instance,

- In December 2024, California Privacy Protection announced an increase in fines and penalties under the California Consumer Privacy Act (CCPA). The revised fines and penalties were effective from 1st January 2025.

These requirements significantly add to the burden on organizations looking to deploy location-based analytics technologies, slowing decision-making processes and extending implementation timelines.

MARKET OPPORTUNITIES

Smart Cities and Public Sector Resilience Programs to Create New Market Opportunities

Location intelligence provides municipalities with the tools to develop and implement smart cities and resilient public sector programs by allowing them to leverage spatial data in aiding efforts such as traffic management, improving public transportation, enhancing emergency response capabilities, and minimizing disaster risk. The use of location-based analytics gives municipalities the ability to profile at-risk locations, deploy resources efficiently in times of emergency, and make informed decisions on which infrastructure improvements to invest in based on actual utilization and exposure data. For instance,

- In May 2025, Ecopia AI released ready-to-use 3D land cover data for the 400 largest U.S. cities, created from Nearmap’s high-resolution aerial imagery. The data supports urban planning, infrastructure, climate resilience, and geospatial analytics, with plans to expand coverage to 87% of the U.S. population.

Collectively, publicly funded efforts to digitize as well as restore and build urban communities and resilience, coupled with longstanding relationships with cities and transit authorities, provide the foundation necessary for the widespread and sustainable implementation of location intelligence systems on a national scale.

Segmentation Analysis

By Component

Growing Enterprise Investment in Core Platforms to Drive Solutions Segment Dominance

Based on component, the market is divided into solution and services.

The solution segment is anticipated to account for the largest market share. This is owing to enterprises increasingly investing in core location intelligence platforms for mapping, spatial analytics, geofencing, and real-time tracking to enhance operational and strategic decision-making directly. This has driven an increasing trend for organizations to place greater importance on scalable, cloud-based software applications integrated into their enterprise data environment. As a result, organizations are generating greater revenues from their platform licenses/subscriptions than from services.

The services segment is anticipated to grow at the highest CAGR of 18.3% over the forecast period. The segment is expanding as organizations increasingly require consulting, integration, data management, and managed support to operationalize complex, cloud-based, and AI-enabled location intelligence tools across enterprise environments.

By Technology

Widespread Integration of GPS Technology in Various Sectors to Drive GPS Segment Growth

Based on technology, the market is categorized into GPS, GIS, beacons & RFID, Wi-Fi & Bluetooth-based positioning, and satellite imagery & remote sensing.

The GPS segment dominated the global market share in 2025 as it has been critical for providing global, real-time outdoor positioning for most areas in transportation/logistics/fleet management/mobility. Widespread integration into smartphones, connected vehicles, and IoT devices put these sources into the hands of consumers/users at all levels creating significant demand for GPS-enabled devices through multiple enterprise and consumer-supported use cases.

The Wi-Fi & Bluetooth-based positioning segment is projected to grow at the highest CAGR of 17.7% over the forecast period. The demand for accurate indoor location tracking in malls, airports, hospitals, warehouses, and smart buildings continues to rise where traditional GPS signals are ineffective, propelling segment growth.

By Application

Widespread Enterprise Reliance on Visual Spatial Insights to Drive the Dominance of Mapping & Visualization Segment

Based on application, the market is categorized into mapping & visualization, spatial analytics, geofencing & geotargeting, asset tracking & management, workforce & resource management, and others (risk management & emergency response).

The mapping & visualization segment led the global location intelligence market share in 2025 as these technologies provide organizations with a way to interpret location-based data in easy-to-understand dashboards and maps that aid in decision-making. The broad use cases of mapping and visualization across different industries, from retail to logistics, government, and utility, have enabled their greater adoption, when compared to more sophisticated and specialized uses of spatial data analysis.

The asset tracking & management segment is projected to grow at the highest CAGR of 16.1% over the forecast period. The segment is expanding as organizations increasingly prioritize the real-time visibility of vehicles, equipment, and inventory to improve operational efficiency, reduce losses, and enhance supply chain transparency.

By End User

Rapid Expansion of Retail Analytics and Last-Mile Optimization to Drive Retail & E-commerce Segment Leadership

Based on end user, the market is classified into retail & e-commerce, BFSI, IT & telecom, healthcare, government & defense, transportation & logistics, energy & utilities, and others (media & entertainment).

The retail & e-commerce segment recorded a dominating market share in 2025. This is owing to the strong demand for location intelligence in store network optimization, hyperlocal marketing, and customer behavior analysis. The rapid increase of online shopping as well as a rise in last mile delivery has increased the demand for real time geospatial analytics to enhance supply chain effectiveness and to improve how businesses interact with their customers.

The healthcare segment is anticipated to grow at the highest CAGR of 16.4% during the forecast period. This is owing to providers increasingly adopting location intelligence for patient flow optimization, asset tracking, emergency response planning, and population health analytics to improve operational efficiency and service accessibility.

To know how our report can help streamline your business, Speak to Analyst

Location Intelligence Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America held the largest market share in 2024, valuing at USD 7.27 billion, and also maintained the leading share in 2025, with a value of USD 8.09 billion. The market in North America is expected to increase, owing to the early widespread enterprise adoption of cloud and AI-enabled geospatial analytics, with a highly developed ecosystem of leading platform providers and significant investment across use cases in logistics, retail, BFSI, and government. This leadership has been bolstered by large-scale integrations and investments into platforms. For instance,

North America Location Intelligence Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

- In January 2025, HERE Technologies and AWS announced a 10-year, USD 1 billion cloud infrastructure agreement to support AI-powered map and location services, underlining investment behind AI-driven location platforms.

These factors play a significant role in fueling the market growth.

U.S. Location Intelligence Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 7.24 billion in 2026, accounting for roughly 30.7% of global sales.

Europe

The Europe market is projected to record a growth rate of 13.2% over the forecast period, which is the second highest among all regions, and reach a valuation of USD 6.07 billion by 2026. The market is observing significant growth across the region, owing to strong demand for consistent geospatial data that can be easily shared between different agencies and used in public service, as well as for the purpose of sustainability projects. There is also an increasing amount of enterprise-level utilization of spatial analytics to assist in mobility, utilities, logistics, and climate risk planning. Another factor contributing to this trend is the recent introduction of data space initiatives to improve data availability and interoperability as regulations across the EU align, thereby reducing barriers to entry for organizations that operate across borders. For instance,

- In January 2025, TomTom partnered with Esri to integrate TomTom’s maps and traffic data into the ArcGIS platform to deliver advanced location data analytics for businesses and governments.

U.K. Location Intelligence Market

The U.K. market is estimated to touch around USD 1.23 billion in 2026, representing roughly 5.2% of global revenues.

Germany Location Intelligence Market

The Germany market is projected to reach approximately USD 1.10 billion in 2026, equivalent to around 4.7% of global sales.

Asia Pacific

The Asia Pacific market is estimated to reach USD 5.28 billion in 2026 and expected to grow at the highest CAGR during the forecast period. The advancing buildings and growth of cities in the region are creating the increasing demand for location intelligence throughout the region through the development of large area development, infrastructure, geospatial planning, improved transportation, and ability to provide public services based upon location.

Japan Location Intelligence Market

The Japan market is estimated to reach around USD 1.00 billion in 2026, accounting for roughly 4.2% of global revenues. Japan's industry is experiencing rapid growth as both national and municipal digital twin initiatives add to national supply and improve access to high-quality three-dimensional (3D) urban and geospatial datasets to support planning, resiliency, and smart city operations. Additionally, there is a demand from mobility/logistics and automotive ecosystems that require accurate maps and location analytics to improve navigation, routing, and operational effectiveness.

China Location Intelligence Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.22 billion, representing roughly 5.2% of global sales.

India Location Intelligence Market

The India market is estimated to reach around USD 0.66 billion in 2026, accounting for roughly 2.8% of global revenues.

South America

South America is expected to witness moderate growth in the market during the forecast period. The South America market is set to reach a valuation of USD 1.24 billion in 2026. This is owing to the rising adoption of geospatial analytics in logistics, urban mobility, retail expansion, and government smart city initiatives aimed at improving infrastructure planning and operational efficiency.

Middle East and Africa

The Middle East and Africa market is estimated to reach USD 1.95 billion in 2026 and expected to grow at a prominent growth rate in the coming years. This is owing to government-led smart city and digital transformation programs that require geospatial planning, real-time mobility monitoring, and location-enabled public services. The governmental initiatives also drive the growth of logistics and energy infrastructure across Gulf and African Cities respectively, where location intelligence is increasingly being used for asset tracking, network optimization and public safety operations. In the Middle East & Africa, the GCC is set to reach a value of USD 0.62 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Platform Capabilities and Strategic Partnerships to Accelerate the Market Growth

The global location intelligence market holds a semi-consolidated market structure, with prominent players such as Google LLC, Esri, HERE Technologies, TomTom International BV, and Microsoft holding significant positions. These companies are driving market growth through continuous platform innovation, including AI-enabled spatial analytics, cloud-native geospatial services, real-time mobility data integration, and advanced visualization tools. Strategic partnerships with cloud providers, telecom operators, automotive companies, and enterprise software vendors are playing a critical role in expanding use cases across logistics, retail, smart cities, and public safety. For instance,

- In October 2025,Esri collaborated with Google Maps Platform to integrate high-quality photorealistic 3D tiles into ArcGIS, enhancing digital twin and urban planning capabilities for enterprises and government agencies both onboard communication systems and ground-based operations from emerging threats.

Other notable players in the global market include Precisely, Hexagon AB, Mapbox, Trimble, and KDDI Corporation. These companies are increasingly focusing on AI-driven geospatial analytics, high-resolution satellite and mobility data integration, industry-specific location solutions, and scalable cloud deployments to strengthen their competitive positioning and expand their global footprint throughout the forecast period.

LIST OF KEY LOCATION INTELLIGENCE COMPANIES PROFILED

- KDDI Corporation (Japan)

- HERE Technologies (Netherlands)

- Google LLC (Alphabet, Inc.) (U.S.)

- Esri (U.S.)

- TomTom International BV (Netherlands)

- Precisely (U.S.)

- Microsoft (U.S.)

- Hexagon AB (Sweden)

- Mapbox (U.S.)

- Trimble (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Mapbox launched a public preview of door-level entrance data, enabling delivery logistics and ride-hailing companies to guide drivers to the exact building entrance within 5 meters. The new location intelligence capability improves arrival accuracy for over 100 million U.S. addresses, reducing failed deliveries, driver search time, and last-mile inefficiencies.

- February 2026: Trimble integrated its PC Miler commercial fleet mapping technology into the Fleetsafe.ai platform, giving fleet managers and drivers access to fleet-optimized maps that improve routing accuracy, compliance, and real-time visibility.

- January 2026: Precisely added TomTom to its Data Link program, bringing authoritative map and street data into a pre-linked data ecosystem that simplifies integration. The move strengthens location intelligence by helping organizations access ready-to-use data faster.

- November 2025: Google unveiled new AI-powered features and tools that will be available on the Google Maps Platform, including AI coding assistance and contextual map experiences.

- August 2025: HERE Technologies became the first location data company to achieve ISO/IEC 42001 certification, setting a new benchmark for responsible AI in location intelligence.

- May 2025: Precisely launched Dynamic Neighborhoods and Signal Engine to strengthen location intelligence by turning demographic audiences and first-party data into privacy-safe, actionable insights.

- July 2024: Microsoft extended its long-term alliance with TomTom, embedding TomTom maps into Azure Maps and first-party Microsoft products, with joint AI innovation.

REPORT COVERAGE

The global location intelligence market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Application, End User, and Region |

| By Component |

|

| By Technology |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 20.90 billion in 2025 and is projected to reach USD 23.58 billion by 2034.

In 2025, the North America market value stood at USD 8.09 billion.

The market is anticipated to grow at a CAGR of 13.8% during the forecast period of 2026-2034.

By end user, the retail & e-commerce segment led the market in 2025.

The rising demand in retail and store expansion is a key factor driving the market.

Google LLC, Esri, HERE Technologies, TomTom International BV, and Microsoft are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us