Sports Technology Market Size, Share & Industry Analysis, By Technology (Wearable Technology, AI and ML, GPS and Motion Tracking, VR/AR, Cloud & Big Data IoT, and Others), By Application (Performance Enhancement, Injury Prevention & Recovery, Talent Scouting & Recruitment, Fan Experience & Engagement, Broadcast & Media Analytics, Fitness & Health Monitoring, and Game Strategy & Tactical Analysis), By End-user (Sports Organizations & Leagues, Broadcasters and Media Companies, Sports Clubs, and Others), and Regional Forecast, 2026 – 2034

(Offer valid till 15th Aug 2026)

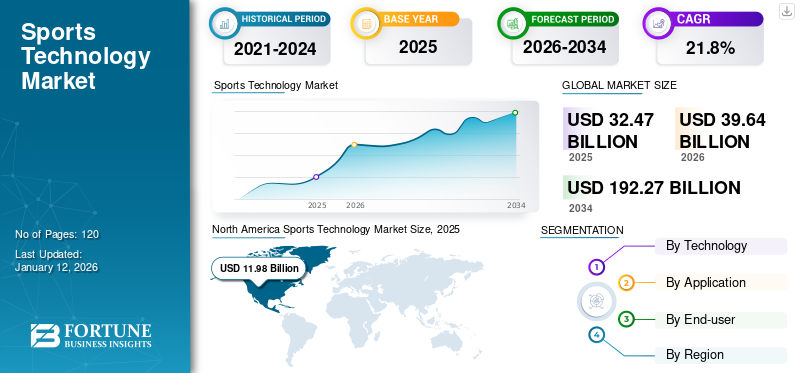

SPORTS TECHNOLOGY MARKET SIZE AND FUTURE OUTLOOK

The sports technology market size was valued at USD 32.36 billion in 2025. The market is projected to grow from USD 39.34 billion in 2026 to USD 200.83 billion by 2034, exhibiting a CAGR of 22.6% during the forecast period. North America dominated the sports technology market with a market share of 36.86% in 2025.

Sports technology includes advanced digital tools, platforms, and connected solutions that help sports organizations improve athlete performance, fan engagement, broadcasting, venue operations, data analytics, and commercial monetization. These solutions include wearables, athlete-tracking systems, smart-stadium technologies, video analytics, AI-based coaching tools, sports data platforms, digital ticketing, streaming technologies, and fan engagement applications. Unlike traditional manual coaching methods, basic broadcasting systems, or conventional stadium operations, sports technology provides real-time visibility into player performance, audience behavior, operational efficiency, content delivery, and revenue opportunities across clubs, leagues, broadcasters, stadiums, and sports federations.

The rapid expansion of digital fan engagement, athlete performance tracking, connected stadiums, OTT streaming, AI-powered analytics, and mobile-first sports consumption is driving demand for sports technology solutions. Sports organizations are also increasingly investing in these platforms to improve match preparation, reduce injury risks, personalize fan experiences, optimize stadium operations, enhance live broadcasts, and create new revenue streams through digital content, sponsorships, advertising, and data-driven engagement.

- According to IBM’s 2025 global sports fan study, 90% of surveyed fans consume sports content beyond watching live events, highlighting the growing importance of interactive, personalized, and digital sports experiences.

Key players such as Apple, Inc., Garmin Ltd, Catapult, and Samsung Electronics are strengthening their sports technology capabilities through wearables, AI, machine learning, computer vision, cloud analytics, performance monitoring, real-time sports data, and digital fan engagement platforms. These companies focus on delivering solutions that support athlete monitoring, coaching intelligence, officiating accuracy, live match analytics, audience personalization, content automation, and smart venue management. For instance,

- Catapult works with more than 4,600 teams across 40+ sports and 100+ countries, demonstrating the growing adoption of performance analytics and athlete-monitoring solutions in professional sports.

Download Free sample to learn more about this report.

SPORTS TECHNOLOGY MARKET Key Takeaways

- 2025 Market Size: USD 32.36 billion

- 2026 Market Size: USD 39.34 billion

- 2034 Forecast Market Size: USD 200.83 billion

- CAGR: 22.6% from 2026–2034

- North America dominated the sports technology market with a market share of 36.86% in 2025.

- Sports organizations & leagues captured the highest market share and held 35.8% of the market share in 2025.

- Performance enhancement captured the largest market share and accounted for 23.1% of the market share in 2025.

North America

North America held the largest sports technology market share in 2025, supported by strong adoption across American football, baseball, basketball, golf, soccer, esports, and ice hockey.

Europe

Europe was valued at USD 9.73 billion in 2025 and is exhibiting a CAGR of 21.30% during the forecast period, supported by strong sports leagues and growing interest in niche sports.

Asia Pacific

Asia Pacific is expected to grow at the highest CAGR during the forecast period, driven by infrastructure development and increased investment in sports across India, China, Australia, and Japan.

U.S.

The U.S. market reached USD 8.40 billion in 2025, accounting for roughly 25.6% of sales, driven by major professional sports leagues and sports entertainment events.

Japan

The Japan market in 2025 was valued at around USD 1.59 billion, accounting for roughly 4.9% of global revenues.

Read More

IMPACT OF GENERATIVE AI

Generative AI Adoption Enhance Fan Engagement, Broadcasting, and Athlete Performance Analytics

Generative AI is expected to have a strong influence on the sports technology market growth as it improves fan engagement, sports broadcasting, content creation, athlete analytics, and venue operations. It enables clubs, leagues, broadcasters, and stadium operators to create personalized content, automated highlights, match summaries, player insights, fan updates, and real-time digital experiences. Sports organizations are also using generative AI to deliver customized match previews, post-match summaries, social media content, and interactive fan communication. For instance,

- ESPN worked with Accenture to use generative AI for personalized sports coverage and real-time content. At the same time, NBC Sports announced the use of Nippon TV’s AI solution for live event tracking, player recognition, auto-score graphics, and mobile-friendly vertical cropping.

Generative AI also supports athlete performance analysis by converting large volumes of wearable, GPS, and biometric data into actionable training insights. Overall, generative AI is creating opportunities to improve content speed, fan personalization, operational efficiency, and data-driven decision-making across the sports ecosystem.

SPORTS TECHNOLOGY MARKET TRENDS

Increasing Use of Wearables and Athlete Performance Tracking to Shape Market Growth

The growing use of wearables and athlete performance-tracking systems is emerging as a key trend in the market. Sports teams, leagues, academies, and training centers are increasingly adopting GPS trackers, smart clothing, heart-rate monitors, motion sensors, and biometric monitoring devices to collect real-time data on athlete movement, workload, fatigue, recovery, speed, acceleration, and injury risk.

These technologies help coaches, trainers, and medical teams gain a deeper understanding of player condition and performance during training sessions and competitive matches. For instance,

- In April 2026, UAE Team Emirates-XRG signed a two-year partnership with WHOOP, making WHOOP its official health and performance wearable. The collaboration will provide real-time athlete data such as strain, recovery, sleep, and heart rate to enhance performance insights and fan engagement during major cycling events.

- In February 2026, ŌURA was named the official wearable of Team USA and the LA28 Olympic and Paralympic Games. The partnership will equip athletes with Oura Rings to track sleep, recovery, and overall well-being, supporting performance and training.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth of Digital Broadcasting, Streaming, and Sports Media Monetization to Drive Market Growth

The growth of digital broadcasting, streaming, and sports media monetization is a major driver for the market. Fans are increasingly consuming sports content through OTT platforms, mobile apps, social media clips, live streaming services, and personalized digital channels. This shift is encouraging leagues, clubs, broadcasters, and rights holders to use digital platforms to reach wider audiences across regions, devices, and viewing formats. Technologies such as AI-generated highlights, real-time statistics, live data overlays, multilingual commentary, and interactive viewing tools are refining content delivery and fan engagement. For instance,

- A 2025 IBM survey found that 90% of sports fans engage with sports content beyond live matches, while 38% use another device to check live statistics and follow updates.

- According to IISM, IPL’s 2023 to 2027 broadcast rights are valued at around USD 5.80 billion, highlighting the rising monetization potential of digital sports content.

Market Restraints

Cybersecurity Risks in Connected Stadiums and Digital Sports Ecosystems May Limit Market Growth

Cybersecurity risks in connected stadiums and digital sports ecosystems may limit the growth of the market. Modern venues are increasingly using IoT sensors, digital ticketing, cashless payments, mobile apps, surveillance systems, Wi-Fi networks, and cloud-based venue management platforms. While these technologies improve fan experience and operational efficiency, they also increase exposure to cyberattacks and data breaches. A cyberattack can disrupt ticketing, entry gates, payment systems, broadcasting, scoreboards, and stadium security during live events. For instance,

- Cybersecurity company, Surfshark reported that cyberattacks on professional sports organizations surged by 112% over the past five years.

- In November 2025, the French Football Federation confirmed a cyberattack that exposed members’ personal data, while in August 2025, several Israeli sports websites were hit by a large-scale cyberattack.

Market Opportunities

Rising Demand for Digital Fan Engagement and Personalized Experiences to Create Growth Opportunities

The rising demand for digital fan engagement and personalized experiences is creating strong growth opportunities for the market. Sports organizations are increasingly moving beyond ticket sales and match-day attendance to build continuous relationships with fans before, during, and after live events. Clubs, leagues, broadcasters, and venue operators are investing in mobile apps, digital communities, loyalty programs, social media engagement, fantasy sports integration, and personalized content platforms. Stadiums are also adopting mobile ticketing, seat upgrades, food and beverage ordering, wayfinding, AR-based experiences, and cashless payments to improve fan convenience. For instance,

- In May 2026, Major League Baseball partnered with RISE Worldwide to expand fan engagement and digital content in India. Similarly, the Australian Football League expanded its partnership with Tradable Bits to strengthen fan data, real-time interactions, and personalized campaigns.

Segmentation Analysis

By End-user

Surge in Demand for Performance and Tactical Enhancement Propelled Adoption of Sports organizations & leagues

Based on end-user, the market is classified into sports organizations & leagues, broadcasters and media companies, sports clubs, and others (athletes, coaches & trainers, etc.).

Sports organizations & leagues captured the highest market share in 2025, as wearables and GPS tracking devices are increasingly used by leagues such as the National Football League (NFL), National Basketball Association (NBA), and English Premier League (EPL) to collect real-time athlete performance data. Moreover, systems such as Hudl, Catapult, and STATSports analyze player movements, tactics, and fitness by using wearable devices. The segment held 35.8% of the market share in 2025.

Broadcasters and media companies are anticipated to grow at the highest CAGR of 26.40% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Rising Demand for Performance Monitoring and Optimization Boosted Adoption of Wearable Technology

Based on technology, the market is divided into wearable technology, AI and ML, GPS and motion tracking, VR/AR, cloud & big data IoT, and others (computer vision, robotics & automation, etc.).

Wearable technology captured the largest market share of 31.8% in 2025, as professional athletes mainly use it to track speed, distance, heart rate, body temperature, and movement efficiency. These devices provide data-driven insights that help the coaching team to train athletes in a personalized way.

VR/AR segment is expected to grow at the highest CAGR of 26.00% during the forecast period.

By Application

Growing Adoption of AI and Data Analytics Boosted Popularity of Performance Enhancement Segment

Based on application, the market is categorized into performance enhancement, injury prevention & recovery, talent scouting & recruitment, fan experience & engagement, broadcast & media analytics, fitness & health monitoring, and game strategy & tactical analysis.

Performance enhancement captured the largest market share in 2025. Sports organizations and coaching teams are increasingly using AI-powered tools to analyze athlete performance and create personalized training recommendations. Video analytics platforms help coaches break down game footage, identify players’ weaknesses, and suggest improvements. The segment captured 23.1% of the market share in 2025.

The fan experience & engagement segment is expected to grow at the highest CAGR of 26.00% during the forecast period.

Sports Technology Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, Middle East & Africa, and Asia Pacific.

North America

North America Sports Technology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest sports technology market share in 2025. In the region, sports such as American football, baseball, basketball, and golf have dominated the market. However, emerging games such as soccer, esports, and ice hockey are also gaining popularity among people. Esports are becoming more well-known among youngsters, owing to investments of big brands in tournaments, sponsorships, and gaming events. As a result, North America is expected to become a hub for more niche sports. For instance,

- In April 2025, Utah Jazz and Utah Hockey Club owner Ryan Smith invested over USD 1 billion to launch tech startups operating within sports in partnership with private equity firm Accel. Through this investment, Ryan Smith plans to expand its investment team.

U.S. Sports Technology Market

Given North America’s strong contribution, the U.S. market reached USD 8.40 billion in 2025, accounting for roughly 25.6% of sales. In the U.S., people are very enthusiastic about sports. National Football League (NFL), National Hockey League (NHL), National Basketball Association (NBA), Major League Soccer (MLS), and Major League Baseball (MLB) are some of the major sports leagues in the country. The U.S. is a leader in sports entertainment, as it hosts major events such as the Super Bowl and the NBA finals to attract huge audiences. For instance,

- In July 2024, Catapult extended its strategic partnership with U.S. Volleyball. Through this partnership, the company provided its innovative athlete monitoring technology to the U.S. Volleyball national team for the 2024 Summer Olympics in Paris and helped them to enhance their performance.

Europe

Europe is the second largest market, valued at USD 9.73 billion in 2025, exhibiting a CAGR of 21.30% during the forecast period. In Europe, sports technology is growing at a prominent pace. Europe is home to many of the world’s most prestigious sports leagues, especially tennis, soccer, and rugby. The U.K., Spain, France, Italy, and Germany are home to some of the biggest soccer clubs with global fanbases. These sports clubs generate huge revenues through broadcasting rights and sponsorships. Moreover, Europe is experiencing a growing interest in niche sports such as motorsports, handball, and cycling. Thus, with growing fan bases, tournaments become more accessible in the region. For instance,

- In February 2025, Sportradar Group AG, a Switzerland-based company, engaged in a partnership with Major League Baseball (MLB). Through this partnership, the company aims to provide MLBs with complete statistical data and Audiovisual (AV) content and support future growth opportunities.

U.K. Sports Technology Market

The U.K. market in 2025 was valued at USD 1.40 billion, representing roughly 4.3% of global revenues.

Germany Sports Technology Market

Germany’s market reached approximately USD 1.75 billion in 2025, equivalent to around 5.4% of global sales.

Asia Pacific

The market in Asia Pacific is expected to grow at the highest CAGR during the forecast period. The region is witnessing a rapid shift in the sports sector, driven by infrastructure development and increased investment. India, China, Australia, and Japan are massively investing in sports, with an emphasis on cricket, soccer, and basketball. Additionally, Esports are thriving in South Korea and China, with growing sponsorships creating a million-dollar industry. These factors are expected to fuel market growth across the region. For instance,

- In August 2024, Catapult launched an innovative sideline video solution for football, owing to growing demand worldwide. Earlier in 2024, the National Collegiate Athletics Association (NCAA) Football Rules Committee officially permitted the usage of sideline video solutions for live review.

Japan Sports Technology Market

The Japan market in 2025 was valued at around USD 1.59 billion, accounting for roughly 4.9% of global revenues.

China Sports Technology Market

China’s market is projected to be one of the largest worldwide and its 2025 revenues reached USD 2.06 billion, representing roughly 6.3% of global sales.

India Sports Technology Market

The India market in 2025 was at USD 0.98 billion, accounting for roughly 3.0% of global market share.

Middle East & Africa

The Middle East & Africa is the fourth leading region, expected to showcase noteworthy growth with a valuation of USD 2.39 billion in 2025. Increasing focus on hosting international events to accelerate digital transformation in sports is fueling market growth. In 2022, Qatar hosted the FIFA World Cup, where the country invested heavily in smart stadiums. For instance,

- According to industry experts, the market value of sports tourism in the Middle East was approximately USD 600 billion in 2022. Moreover, the projected annual growth for the region’s sports industry by 2026 is 8.7%.

- In December 2024, over USD 65 billion was invested in sports development in GCC countries. This investment is expected to boost sports industry growth in the region.

GCC Sports Technology Market

The GCC market reached around USD 0.77 billion in 2025, representing roughly 2.4% of global revenues.

South America

The adoption of sports technology is growing significantly in South America, owing to the region’s passionate sports culture, particularly around football (soccer), and a rising interest in innovation to enhance athlete performance and fan engagement. Leading football clubs in Brazil, Argentina, and Colombia are significantly using GPS trackers and biometric wearables to optimize player performance. Furthermore, stadiums across the region are implementing AI, IoT, and 5G technology for security monitoring and enhancing the fan experience in the stadiums.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Companies Are Implementing Acquisition and Collaboration Strategies to Gain Strong Market Foothold

Industry participants are concentrating on expanding their global geographical presence by showcasing industry-specific services. Key industry participants are adopting initiatives such as acquisitions and partnerships to gain a competitive edge across the region. Moreover, companies are also introducing new solutions to expand their consumer base. Increased R&D spending for product innovations is enhancing market expansion. Therefore, leading players are executing their strategic approaches to maintain their competitive edge in the market.

LIST OF KEY SPORTS TECHNOLOGY COMPANIES PROFILED

- Apple Inc. (U.S.)

- Catapult (Australia)

- Garmin Ltd. (U.S.)

- Genius Sports Group (U.K.)

- Hawk-Eye Innovation Ltd. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- IBM Corporation (U.S.)

- Samsung Electronics (South Korea)

- Sportradar AG (Switzerland)

- Stats Perform (U.K.)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Stats Perform announced the launch of new AI-assisted video creation and distribution solution Opta Pulse, which allows to produce high-quality highlight of the game. It enables leagues, broadcasters and rights holders to generate synchronized short videos with AI-assisted detection and publish to enhance fan engagement.

- March 2026: Stats Perform partnered with VSiN to provide exclusive access to Opta Predictions’ player prop projection tools for VSiN Pro subscribers. The tools cover NBA, NFL, MLB, and NHL player projections, including metrics such as points, rebounds, assists, passing yards, rushing yards, receptions, and shots on goal.

- February 2026: Huawei introduced the newly developed watch GT Runner 2 in a product launch event in Madrid, Spain. The watch is equipped with a 3D floating antenna architecture and an intelligent positioning algorithm, enabling runners to share live locations and improve safety tracking.

- April 2025: La Liga leads in AI expertise worldwide, focusing on the Middle East and the U.S. The AI technology will help La Liga provide effective match analysis and automate real-time video content for digital platforms.

- March 2025: Catapult launched Vector 8, an athlete performance monitoring platform. This platform will enable teams and sports clubs to make accurate and real-time decisions through live experiences. This platform is expected to transform the future of the athlete monitoring experience.

- March 2025: Sportradar Group AG acquired IMG ARENA and its global sports betting rights portfolio. Through this acquisition, the company aims to enhance its content and product offering and provide its platform to various games, including tennis, soccer and basketball.

- January 2025: Catapult increased its R&D spending on wearable technology, owing to a rise in women's professional sports and wearable integration. These technologies include GPS devices and video analysis software, which are essential to evaluate the performance of athletes.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Key players in the market are increasingly investing in IoT, AI, machine learning, cloud platforms, and advanced analytics to improve smart stadium operations, fan engagement, athlete performance, and sports broadcasting. These investments are helping clubs, leagues, broadcasters, and technology vendors build data-driven platforms for real-time decision-making, personalized content delivery, scouting, training optimization, and venue management. For instance,

- In June 2025, Catapult acquired Perch to expand its Performance & Health vertical and strengthen its athlete-performance analytics capabilities.

- In October 2025, Catapult also completed the acquisition of IMPECT, a soccer scouting analytics company, to enhance tactical analysis and data-driven scouting solutions.

- Similarly, in October 2025, the NBA partnered with AWS, making AWS its Official Cloud and Cloud AI Partner to support advanced analytics, AI-powered statistics, broadcasting, and fan experiences.

These developments indicate rising investment activity and strategic collaborations across the sports technology ecosystem, creating lucrative opportunities for market growth.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, technology, end user, and leading applications. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology, Application, End-user, and Region |

| By Technology |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 32.36 billion in 2025 and is projected to reach USD 200.83 billion by 2034.

In 2025, the North America market value stood at USD 11.93 billion.

The market is expected to grow at a CAGR of 22.6% over the forecast period.

By end-user, sports organizations & leagues segment is expected to lead the market.

Growth of digital broadcasting, streaming, and sports media monetization to drive market growth.

Apple, Inc., Garmin Ltd., Catapult, and Samsung Electronics are the major players in the global market.

North America held the highest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us