Low Emission Vehicle Technology Market Size, Share & Industry Analysis, By Technology Type (Electric Vehicle Technologies, Hybrid Vehicle Technologies, Fuel Cell Technologies, Advanced ICE Technologies, and Emission Control Technologies), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Fuel Type (Electric, Hybrid, Hydrogen, ICE-based fuels, and Others), By Application (Powertrain Systems, Exhaust & Emission Systems, Energy Storage & Management, and Vehicle Lightweighting), and Regional Forecasts, 2026-2034

Low Emission Vehicle Technology Market Size & Future Outlook

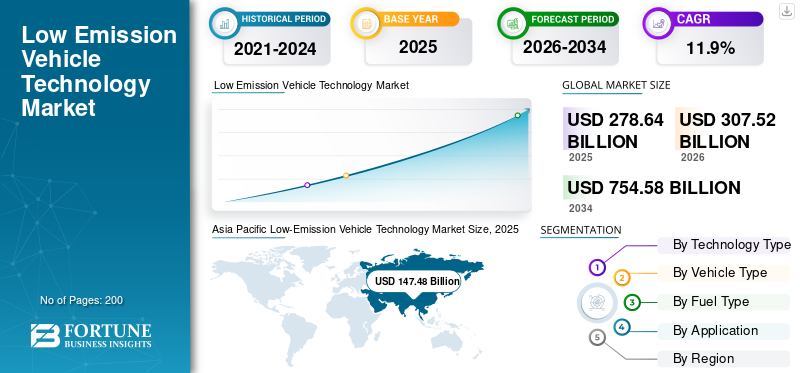

The global low-emission vehicle technology market size was valued at USD 278.64 billion in 2025. The market is projected to grow from USD 307.52 billion in 2026 to USD 754.58 billion by 2034, exhibiting a CAGR of 11.9% during the forecast period. Asia Pacific dominated the low emission vehicle technology market with a market share of 52.93% in 2025.

The global market represents the value of technologies used to reduce vehicle emissions, improve fuel efficiency, and support cleaner mobility. It includes components and systems installed in Electric Vehicles (EVs), Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicle (HEV), fuel-cell vehicles, and cleaner internal combustion engines.

The market is expected to evolve strongly during the forecast period as governments tighten emission standards, automakers shift product portfolios, and consumers demand cleaner vehicles. Rising concerns over greenhouse gas emissions are pushing automakers to invest in electrified powertrains, cleaner fuels, and advanced emission technologies. The expansion of charging infrastructure is also improving adoption, especially in urban and fleet applications.

The industry has several applications across passenger cars, light commercial vehicles, heavy trucks, buses, and fleet vehicles. Each market segment is influenced differently. Passenger cars lead in adoption due to high production volumes, while commercial vehicles are gaining attention as fleet operators are under pressure for reducing greenhouse gas output.

The emission vehicle industry will also benefit from local battery production, better supply localization, and stronger technology partnerships. Key players such as BYD, Geely, and Tesla are investing in batteries, fuel cells, powertrain systems, and software-driven energy management to improve market share and support future emission vehicle market size expansion.

Download Free sample to learn more about this report.

LOW-EMISSION VEHICLE TECHNOLOGY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 278.64 billion

- 2026 Market Size: USD 307.52 billion

- 2034 Forecast Market Size: USD 754.58 billion

- CAGR: 11.9% from 2026–2034

- Asia Pacific dominated the low-emission vehicle technology market with a 52.93% share in 2025.

- The electric vehicle technologies segment held the largest market share in 2025.

- The passenger vehicles segment dominated the global market in 2025.

Asia Pacific

Asia Pacific the market reached USD 147.48 billion in 2025, driven by strong EV production, battery manufacturing, and government-backed emission policies.

Europe

Europe the market is projected to reach USD 65.86 billion in 2026, supported by stringent CO₂ regulations and increasing adoption of BEVs and hybrid vehicles.

North America

North America the market is expected to reach USD 56.91 billion in 2026, fueled by EV investments, battery localization, and expanding charging infrastructure.

U.S.

The market was valued at USD 39.38 billion in 2025, supported by strong commercial EV demand, domestic battery production, and fleet electrification.

Japan

The country continues to strengthen the market through its leadership in hybrid technologies and ongoing investments in next-generation low-emission vehicle technologies.

Read More

LOW-EMISSION VEHICLE TECHNOLOGY MARKET TRENDS

Ultra-Fast Charging and Advanced Batteries Reshape EV Technology

A major trend is the shift toward faster charging, higher energy density, and safer battery systems. Automakers and suppliers are improving battery technology to reduce charging time, extend range, and improve user confidence. This supports the wider adoption of battery electric vehicles, improves charging infrastructure utilization, and strengthens the value of energy storage and powertrain systems across each market segment.

- In April 2025, CATL unveiled Naxtra sodium-ion, Freevoy dual-power, and second-generation Shenxing superfast-charging batteries for new energy mobility.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Tightening Emission Standards Accelerate Low-Emission Vehicle Technology Adoption

Stricter emission standards are a major driver for the low-emission vehicle technology market growth. Governments are pushing automakers to reduce tailpipe emissions, improve fuel efficiency, and shift toward electric vehicles and hybrid systems. This directly increases demand for batteries, motors, power electronics, after-treatment systems, and cleaner internal combustion engines, helping expand the emission vehicle market size during the forecast period.

- In May 2025, IEA reported electric car sales exceeded 17 million in 2024, reaching over 20% of global car sales.

MARKET RESTRAINTS

High Battery and Critical Mineral Costs Limit Faster Adoption

High raw material exposure remains a restraint for the emission vehicle industry, especially in battery electric vehicles and plug-in hybrid electric platforms. Battery metals, rare earths, and power electronics components are concentrated in limited regions, creating cost and availability risks. These pressures can delay affordability, reduce margins, and slow adoption in price-sensitive countries despite strong demand for reducing greenhouse gas emissions.

- In May 2025, IEA warned that sustained battery-metal supply shocks could raise global battery pack prices by 40-50%.

MARKET OPPORTUNITIES

Localized Battery Manufacturing Creates New Growth Potential

Battery localization is a major opportunity as it reduces import dependence, improves cost control, and strengthens the low-emission vehicle supply chain. Governments and companies are investing in domestic battery plants, cathode materials, recycling, and pack assembly. This supports battery technology growth, improves regional competitiveness, and helps automakers scale electric vehicles, hybrid electric vehicles, and commercial low-emission platforms.

- In December 2024, the U.S. DOE announced a USD 9.63 billion loan to BlueOval SK for three EV battery plants in Tennessee and Kentucky.

MARKET CHALLENGES

Charging Infrastructure Gaps Slow Mass-Market EV Penetration

Insufficient and uneven charging infrastructure remains a major challenge, especially outside China and major European cities. Many buyers still worry about charging access, charging speed, and reliability. This slows adoption of electric vehicles, especially among apartment residents, rural users, and fleet operators. Without faster infrastructure expansion, the global low emission vehicle market may grow unevenly across regions.

- For instance, in October 2024, India allocated INR 20 billion (~ USD 0.24 billion) under PM E-DRIVE to expand public EV chargers across cities and transport corridors.

Low Emission Vehicle Technology Market Segmentation Analysis

By Technology Type

Electric Vehicle Technologies Dominate Due to High Embedded Component Value

On the basis of technology type, the market is segmented into electric vehicle technologies, hybrid vehicle technologies, fuel cell technologies, advanced ice technologies, and emission control technologies.

Electric vehicle technologies dominate as BEVs contain high-value systems such as battery packs, motors, inverters, BMS, thermal systems, and software controls. These components create much higher technology value per vehicle than traditional internal combustion engines. The rising electric vehicles adoption, stronger emission standards, and declining battery costs further support this segment’s leadership in market share.

- In March 2025, BYD’s Super e-Platform introduced 1 MW charging, silicon carbide chips, and 580 kW single-motor output.

The fuel cell technologies segment is expected to grow at a CAGR of 22.8% over the forecast period.

By Vehicle Type

Passenger Vehicles Lead Due to Scale and Faster Electrification

On the basis of vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, and heavy commercial vehicles.

Passenger vehicles dominate as they represent the largest production base and the fastest adoption area for battery electric vehicles, hybrid electric vehicles, and plug-in hybrid electric models. Automakers prioritize passenger cars for technology launches, battery cost reduction, and software upgrades. High consumer demand and policy incentives help this vehicle type maintain the largest value market share.

- For instance, in January 2025, Volkswagen announced expansion of its ID family production in Europe, targeting higher passenger EV volumes through scalable MEB platform manufacturing.

The light commercial vehicles segment is expected to grow at a CAGR of 14.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Fuel Type

Electric Segment Dominates as BEVs Carry the Highest Technology Value

On the basis of fuel type, the market is segmented into electric, hybrid, hydrogen, ICE-based fuels, and others.

The electric segment dominates the low-emission vehicle technology market share as BEVs require expensive technology systems, including batteries, motors, power electronics, thermal management, and charging interfaces. Although hybrids remain important, battery electric vehicles have higher content value per vehicle. Stronger policy support, falling battery costs, and expanding charging infrastructure are increasing the segment’s contribution to the emission vehicle market size.

- In February 2025, Hyundai Motor introduced its next-generation E-GMP platform upgrades, enabling improved energy efficiency, faster charging, and longer range for electric vehicle models.

The hydrogen segment is expected to grow at a CAGR of 23.6% over the forecast period.

By Application

Powertrain Systems Dominate as Electrification Begins at the Drivetrain

On the basis of application, the market is segmented into powertrain systems, exhaust & emission systems, energy storage & management, and vehicle lightweighting.

Powertrain systems dominate as every low-emission pathway requires drivetrain upgrades. BEVs need motors and inverters, hybrids need dual propulsion systems, and cleaner internal combustion engines need efficiency components. This makes powertrain the largest application area across electric vehicles, hybrids, hydrogen vehicles, and advanced ICE platforms. It also directly supports fuel efficiency and lower emissions.

- In February 2025, Toyota developed its third-generation fuel-cell system for commercial applications, improving durability and hydrogen powertrain adoption.

The energy storage & management segment is expected to grow at a CAGR of 16.9% over the forecast period.

Low-Emission Vehicle Technology Market Regional Outlook

By region, the global market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Low-Emission Vehicle Technology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valuing at USD 147.48 billion, and also maintained the leading share in 2024, with USD 132.43 billion. The region dominates the global market as China leads global EV production, Japan remains strong in hybrids, South Korea supports batteries and hydrogen, and India is expanding affordable electrification. The region has the largest vehicle production base and a strong low-emission technology supply chain. Growing electric vehicles sales, battery manufacturing, and government-backed emission standards strengthen Asia Pacific’s value contribution across the forecast period.

- For instance, in April 2025, CATL launched sodium-ion and superfast-charging batteries, reinforcing China’s role in global battery technology leadership.

China Low-Emission Vehicle Technology Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 92.75 billion, representing roughly 33.3% of the global market.

India Low-Emission Vehicle Technology Market

India market in 2025 was valued at around USD 16.18 billion, accounting for roughly 5.8% of global revenues.

Europe

Europe is estimated to reach USD 65.86 billion in 2026 and secure the position of the second-largest region in the market. Europe will grow steadily due to strict CO₂ rules, strong premium vehicle demand, and high adoption of BEVs and hybrids. EU policy requires a 100% emission reduction target for new cars and vans from 2035, encouraging automakers to scale emission technologies, battery electric vehicles, hybrid electric vehicles, and PHEVs across the region.

Germany Low-Emission Vehicle Technology Market

The Germany market in 2025 was valued at around USD 18.67 billion, accounting for roughly 6.7% of global revenues.

U.K. Low-Emission Vehicle Technology Market

The U.K. market in 2025 was valued at around USD 10.11 billion, accounting for roughly 3.2% of global revenues.

North America

North America is projected to record a growth rate of 10.4% in the coming years, and reach a valuation of USD 56.91 billion by 2026. The region is expected to grow through U.S. led EV investment, battery localization, pickup electrification, and fleet decarbonization. The U.S. market remains the regional anchor due to high vehicle value, strong commercial fleet demand, and government-backed battery production. The growth is supported by domestic manufacturing incentives and expanding charging infrastructure.

U.S. Low-Emission Vehicle Technology Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was approximated at around USD 39.38 billion in 2025, representing roughly 18.7% of the global market.

Latin America

The Latin America region is expected to grow more gradually, led by Brazil’s ethanol, flex-fuel hybrid, and biofuel-linked low-emission strategy. The region’s market depends less on BEVs and more on cleaner internal combustion engines, hybrids, and fuel-flexible platforms. Argentina is adding support for vehicle production, while the rest of Latin America remains in the early-stage.

Middle East & Africa

The Middle East & Africa region is expected to grow from a smaller base, supported by the UAE’s clean-mobility policies and South Africa’s EV roadmap. UAE leads in charging infrastructure, while South Africa focuses on protecting automotive manufacturing competitiveness. Adoption remains gradual as affordability, power reliability, and policy execution still vary widely across the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Automakers and Suppliers Compete Through Electrification Depth and Powertrain Efficiency

The competitive landscape of the global low-emission vehicle technology market is shaped by automakers, Tier-1 suppliers, battery companies, fuel-cell developers, and power electronics manufacturers. Competition is no longer limited to vehicle launches. Companies are competing through deeper control of the supply chain, advanced battery technology, powertrain efficiency, software-defined energy management, and regional production localization.

Major manufacturers are developing dedicated EV platforms, hybrid powertrains, fuel-cell systems, and cleaner internal combustion engines to serve different regional demand patterns. Companies with strong battery sourcing, semiconductor access, and electric drivetrain expertise are gaining a clear advantage as low-emission vehicles require higher technology content per vehicle.

Partnerships are also becoming important. Automakers are working with battery suppliers, charging companies, and energy firms to reduce cost, improve range, and address consumer concerns around charging infrastructure. Meanwhile, suppliers such as Bosch, Denso, Continental, BorgWarner, ZF, and Valeo are focusing on e-axles, thermal systems, inverters, emission control systems, and hybrid modules.

The competitive environment is fragmented but increasingly technology-led. Chinese players are advancing rapidly in battery electric vehicles, while Japanese and European companies remain strong in hybrid and powertrain systems. North American players are focusing on battery localization, commercial fleet electrification, and software-enabled platforms. Over the forecast period, companies that combine cost control, localized production, and scalable emission technologies are expected to strengthen their market share.

LIST OF KEY LOW-EMISSION VEHICLE TECHNOLOGY COMPANIES PROFILED

- BYD Company Ltd. (China)

- Tesla, Inc. (U.S.)

- Toyota Motor Corporation (Japan)

- Volkswagen Group (Germany)

- Hyundai Motor Company (South Korea)

- Kia Corporation (South Korea)

- General Motors Company (U.S.)

- Ford Motor Company (U.S.)

- Stellantis N.V. (Netherlands)

- Mercedes-Benz Group AG (Germany)

- BMW Group (Germany)

- Renault Group (France)

- Nissan Motor Co., Ltd. (Japan)

- Honda Motor Co., Ltd. (Japan)

- Geely Auto Group (China)

KEY INDUSTRY DEVELOPMENTS

- October 2025: The U.K. government partnered with Toyota and industry stakeholders to launch a USD 40 million electric vehicle R&D initiative, backed by USD 20 million in public funding. The program focuses on advancing next-generation low-emission powertrain systems, battery efficiency, and manufacturing processes to accelerate innovation and strengthen the domestic EV technology ecosystem.

- September 2025: Mercedes-Benz successfully completed a 1,205 km real-world drive using an EQS prototype equipped with a lithium-metal solid-state battery. The test demonstrated significantly improved energy density, extended driving range, and reduced charging frequency, highlighting the potential of solid-state batteries to transform electric vehicle performance and support next-generation low-emission mobility solutions.

- August 2025: Nissan partnered with LiCAP Technologies to develop dry-electrode production process technology for all-solid-state batteries, supporting future cost-efficient EV battery manufacturing.

- July 2025: Panasonic Energy began mass production at its Kansas automotive lithium-ion battery factory, targeting annual capacity of 32 GWh for North American EV production.

- June 2025: Kia revealed full specifications of the EV4 electric sedan, offering ultra-rapid charging capability and up to 630 km WLTP-estimated range.

- June 2025: Nissan launched the third-generation LEAF, using learnings from nearly 700,000 LEAF sales and offering improved range, charging speed, and EV usability.

- April 2025: Stellantis and Factorial Energy validated automotive-sized solid-state battery cells with 375 Wh/kg energy density and 15–90% charging in 18 minutes.

REPORT COVERAGE

The global low-emission vehicle technology market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology Type, Vehicle Type, Fuel Type, Application, and Region |

| By Technology Type |

|

| By Vehicle Type |

|

| By Fuel Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 278.64 billion in 2025 and is projected to reach USD 754.58 billion by 2034.

In 2025, the market value stood at USD 147.48 billion.

The market is expected to exhibit a CAGR of 11.9% during the forecast period.

Passenger vehicles segment led the market by vehicle type.

Tightening emission standards is driving the global market.

BYD Company Ltd., Tesla, Inc., Volkswagen Group, and Geely Auto Group are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us