Cell and Gene Therapy Market Size, Share & Industry Analysis, By Type (By Cell Therapy {By Therapy Type [CAR-T Cell Therapy, TCR-T Cell Therapy, Natural Killer Cells, &Others], By Product (Kymriah, Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, & Others], By Indication [Oncology & Others]}, and By Gene Therapy {By Vector Type [Viral Vectors & Non-Viral Vectors], By Product Type [Zolgensma, Luxturna, Roctavian, & Others], and By Indication [Genetic Diseases, Ophthalmology, Hematology, & Others]}), By End User (Hospitals & Clinics, Specialty Clinics, & Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

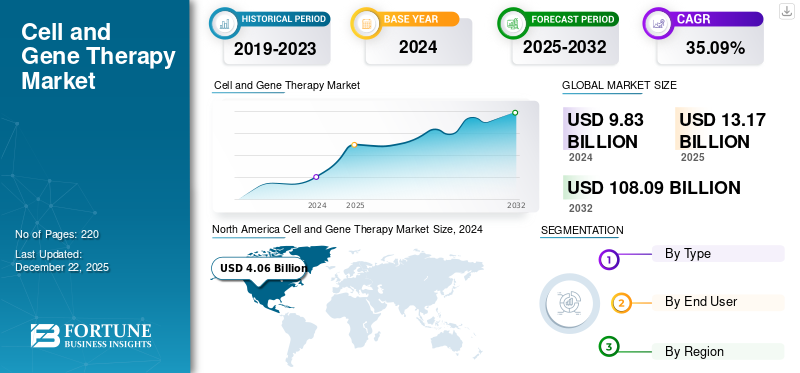

Cell and Gene Therapy Market Size and Future Outlook

The cell and gene therapy market size was valued at USD 12.21 billion in 2025. The market is projected to grow from USD 16.45 billion in 2026 to USD 143.55 billion by 2034, exhibiting a CAGR of 31.10% during the forecast period. North America dominated the cell and gene therapy market with a market share of 52.58% in 2025.

The market is moving into a more disciplined growth phase, supported by a rising base of approved products, continued regulatory progress, and a stronger focus on commercial execution. As more therapies move from clinical development to launch planning, demand is increasing not only for innovation in oncology and rare diseases, but also for the manufacturing, supply chain, and treatment-center capabilities needed to deliver these therapies at scale. This is expected to support market expansion as companies are now focusing more on access, affordability, and operational readiness, which are critical for converting scientific progress into sustainable revenue growth.

Key companies operating in the market are increasingly focusing on expanding their product offerings and commercializing them.

- For instance, in February 2026, Gilead Sciences, Inc. entered into a definitive agreement to acquire Arcellx, a biotechnology company focused on delivering a new class of innovative immunotherapies for patients with cancer and other incurable diseases. Kite, a Gilead company, and Arcellx have an existing collaboration to co-develop and co-commercialize Arcellx’s lead pipeline candidate, anitocabtagene autoleucel (anito-cel), a CAR T-cell therapy for patients with multiple myeloma.

Furthermore, leading players in the industry, such as Vertex Pharmaceuticals Incorporated, Novartis AG, Bristol-Myers Squibb Company, and Krystal Biotech, Inc., are focusing on research and development and strategic partnerships, expanding their offerings to strengthen their market positions.

Download Free sample to learn more about this report.

Cell and Gene Therapy Market Key Takeaways

- 2025 Market Size: USD 12.21 billion

- 2026 Market Size: USD 16.45 billion

- 2034 Forecast Market Size: USD 143.55 billion

- CAGR: 31.10% from 2026-2034

- North America dominated the cell and gene therapy market with a 52.58% share in 2025.

- The gene therapy segment is projected to grow at a CAGR of 21.97% during the forecast period.

- The specialty clinics segment is expected to grow at a CAGR of 32.79% during the forecast period.

North America

North America reached USD 6.42 billion in 2025 after recording USD 5.04 billion in 2024.

Europe

Europe is projected to reach USD 4.47 billion in 2026, growing at a CAGR of 28.43% during the forecast period.

Asia Pacific

Asia Pacific is estimated to reach USD 2.18 billion in 2026.

U.S.

The market is estimated at USD 7.95 billion in 2026, accounting for approximately 48.34% of the global market.

Japan

The market is estimated at USD 0.44 billion in 2026, representing approximately 2.65% of the global market.

Read More

CELL AND GENE THERAPY MARKET TRENDS

Shift Toward Allogeneic and Off-the-Shelf Therapies is a Prominent Market Trend

A prominent trend observed in the market is a shift toward allogeneic and off-the-shelf therapies. In autologous therapy, products are made from a patient’s own cells, which increases manufacturing complexity and creates supply constraints. These challenges are overcome by the shift toward allogenic therapies that can be manufactured in advance in larger standardized batches. This shift is crucial as off-the-shelf therapies can improve treatment availability, reduce turnaround time, support inventory-based distribution, and lower manufacturing burden over time. These benefits make the model more commercially attractive and better suited for broader market expansion.

Additionally, allogeneic platforms are encouraging significant investments in research and development for next-generation cell engineering and large-scale automated manufacturing, which further supports innovation across the market.

- In March 2026, Atara Biotherapeutics leveraged a novel allogeneic EBV T-cell platform to develop therapies for cancer and autoimmune diseases. This is a strong market signal as it shows continued commercial and regulatory commitment to off-the-shelf cell therapy

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Prevalence of Rare Diseases and Cancers to Boost Market Growth

Cell and gene therapies offer an innovative approach for the treatment of hereditary diseases and several types of cancer by targeting the root cause rather than symptom management. Thus, the increasing prevalence of rare diseases and oncology indications is acting as a major growth driver for the market. The rising prevalence of such hereditary diseases is driving demand for gene and cell therapies, which offer alternatives where traditional medicines fall short. Cell and gene therapies are designed to address conditions with high unmet clinical needs in cancer and rare diseases. A large number of rare genetic diseases, making these therapies suitable for gene therapy-based interventions aim to correct, replace, or regulate faulty genes underlying the disease. The combination of rising patient burden, insufficient standard-of-care options, and growing clinical confidence in targeted biological interventions is therefore driving the cell and gene therapy market growth.

- In February 2026, Cellares, the first Integrated Development and Manufacturing Organization (IDMO), in collaboration with the University of Wisconsin (UW) School of Medicine and Public Health, expanded its partnership to support the clinical production and regulatory advancement of the university’s CRISPR-edited GD2 CAR-T investigational therapy for pediatric and adult solid tumors.

MARKET RESTRAINTS

High Therapy Cost & Challenges in Reimbursement Policies to Hinder Market Growth

The market is facing a major growth restraint as these therapies carry very high upfront treatment costs and require complex manufacturing, specialized hospital infrastructure, and long-term patient monitoring. As a result, payers and health systems often apply strict reimbursement reviews before granting broad coverage. This creates delays in patient access and makes it harder for therapy developers to scale commercialization across countries. When reimbursement remains uncertain or takes longer to negotiate, hospitals may be cautious in adopting these therapies, and eligible patients may face access barriers. Therefore, high therapy costs and challenges in reimbursement policies are expected to hinder overall market growth.

- For instance, in October 2025, InspiroGene by McKesson announced its 2025 Cell and Gene Therapy Report, which highlighted that while payers recognize the promise of cell and gene therapies, they still view cost and durability as key challenges to reimbursement. This instance reflects a real market restraint as even when clinical value is recognized, reimbursement concerns can slow treatment adoption and limit the speed at which these therapies reach wider patient populations. Such reimbursement friction is likely to continue restraining market expansion, especially for ultra-high-cost therapies that require payer confidence in long-term outcomes.

MARKET OPPORTUNITIES

Rising Investment in Manufacturing Capacity to Offer Lucrative Market Opportunities

The market is expected to witness strong growth opportunities as companies continue to increase investment in manufacturing capacity, automation, and specialized production infrastructure. This is due to the dependence of the market on complex manufacturing processes, controlled supply chains, and timely product delivery, especially for personalized and high-value therapies. When companies expand production facilities and improve manufacturing efficiency, they can reduce capacity bottlenecks, support larger patient volumes, and improve commercial readiness. As a result, rising investment in manufacturing capacity is expected to create lucrative growth opportunities for the market by enabling faster scale-up, broader geographic reach, and better long-term supply reliability.

- For instance, in February 2026, Johnson & Johnson announced an investment of more than USD 1 billion in a next-generation cell therapy manufacturing facility in Pennsylvania. This development is important for the market as it shows that major biopharmaceutical companies are strengthening their manufacturing base to support future demand for advanced therapies. Such large-scale capacity investments are anticipated to open new growth opportunities for the overall market, as they can improve production scale, support commercialization, and increase the ability to serve more patients over time.

MARKET CHALLENGES

Difficulties in Scaling Autologous Therapies Pose a Significant Challenge for Market Growth

Difficulty in scaling autologous therapies is one of the key challenges faced by the market. Since each treatment is made from an individual patient’s own cells and must move through collection, manufacturing, testing, and reinfusion within a tightly managed timeline. These factors make the production model more complex, time-sensitive, and expensive than conventional biologics or off-the-shelf therapies. As a result, any capacity limitation, process variability, or delay in manufacturing can affect treatment availability and slow broader commercialization. Therefore, difficulties in scaling autologous therapies are expected to challenge market expansion, especially as developers try to serve larger patient populations across multiple regions.

- For example, in January 2026, Autolus Therapeutics announced that it would evaluate automated manufacturing of AUCATZYL (obe-cel) on the Cellares Cell Shuttle platform. The development highlights a challenge to the company’s move toward automation, reflecting the industry’s ongoing need to improve throughput, reliability, and commercial-scale manufacturing for autologous cell therapies. Such developments show that scaling autologous therapies remains a bottleneck for the market, and overcoming this challenge is critical for expanding patient access and supporting future growth.

Segmentation Analysis

By Type

Wide Adoption and Commercial Importance Leads to Cell Therapy Segmental Growth

Based on type, the market is categorized into cell therapy and gene therapy.

Among these, the cell therapy dominated the market. The segment has gained stronger commercial traction earlier than gene therapy, especially in oncology, where CAR-T and other cell-based approaches have already established treatment use in real-world clinical settings. This has created a direct revenue advantage for cell therapy, as more approved products, broader treatment experience, and stronger physician familiarity have supported higher adoption. Furthermore, cell therapies are benefiting from ongoing label expansions and regulatory confidence, which is helping companies reach more eligible patients across hematologic malignancies and other targeted indications. Due to the high commercial importance, key companies are increasingly investing in new product launches and their subsequent approvals.

- For instance, in December 2025, Bristol Myers Squibb announced that the U.S. FDA approved Breyanzi as the first and only CAR-T cell therapy for adults with relapsed or refractory marginal zone lymphoma. This development is important as it shows how cell therapy continues to expand into additional cancer indications, strengthening its commercial position within the overall market. Such approval-based expansion is anticipated to support the continued dominance of the cell therapy segment.

The gene therapy segment is expected to grow at a CAGR of 21.97% over the market forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Large Patient Volumes to Drive Demand for Hospitals & Clinics and Propel Segment Growth

Based on end user, the market is segmented into hospitals & clinics, specialty clinics, and others.

The hospitals & clinics segment is estimated to dominate the market over the forecast period. Most cell and gene therapies require highly specialized administration, multidisciplinary care teams, controlled infusion or transplantation settings, and close patient monitoring before and after treatment. These requirements make large hospitals and advanced clinics the most suitable settings for therapy delivery, especially for high-acuity treatments such as CAR-T and complex gene therapies. Additionally, these facilities are probable to have the infrastructure needed for patient workup, adverse-event management, coordination with manufacturers, and long-term follow-up. Therefore, the concentration of specialized capabilities within hospitals and clinics has made this segment leading end-user category in the market.

- For instance, in February 2025, Cellino collaborated with Mass General Brigham’s Gene and Cell Therapy Institute to launch the hospital-based autologous iPSC foundry in the U.S. The development highlighted how hospital care settings are becoming central not only to therapy administration but also to decentralized manufacturing and treatment integration. Such hospital-based infrastructure expansion is expected to strengthen further the dominance of hospitals and clinics in the market.

The specialty clinics segment is projected to grow at a CAGR of 32.79% over the study period.

Cell and Gene Therapy Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Cell and Gene Therapy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 5.04 billion and maintained its leading position in 2025 at USD 6.42 billion. The market is growing in North America due to the increasing prevalence of cancer and the rising demand for cell and gene therapies. Also, the region has a robust healthcare infrastructure along with high healthcare expenditure. These factors support continued demand for long-term pain medicines, including both generic and newer non-opioid therapies.

U.S. Cell and Gene Therapy Market

Given North America's substantial contribution, the U.S. market is estimated at around USD 7.95 billion in 2026, accounting for roughly 48.34% of the global market.

Europe

Europe is projected to grow at 28.43% over the coming years, the second-highest among all regions, and reach a valuation of USD 4.47 billion by 2026. The market is growing as the region has an aging population with multiple long-term health needs, increasing the burden of chronic diseases. These factors create sustained demand for cell and gene therapies as health systems manage a larger elderly population requiring ongoing symptom control.

U.K. Cell and Gene Therapy Market

The U.K. market is estimated at around USD 0.72 billion in 2026, representing roughly 4.40% of the global market.

Germany Cell and Gene Therapy Market

Germany's market is projected to reach approximately USD 1.09 billion in 2026, equivalent to around 6.64% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 2.18 billion in 2026 and secure the position of the third-largest region in the market. The market is growing in the Asia Pacific as the region is witnessing a rapidly aging population and a rising burden of non-communicable diseases and functional limitations associated with older age. These factors are expected to increase long-term demand for chronic pain treatment.

Japan Cell and Gene Therapy Market

The Japanese market for cell and gene therapies in 2026 is estimated at around USD 0.44 billion, accounting for approximately 2.65% of the global market.

China Cell and Gene Therapy Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.79 billion, representing approximately 4.78% of global sales.

India Cell and Gene Therapy Market

The Indian market in 2026 is estimated at around USD 00.18 billion, accounting for roughly 1.11% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.67 billion in 2026. The market is growing in Latin America as population aging and the increasing burden of non-communicable diseases are causing more disability and long-term illness, including pain-linked conditions. Similarly, countries such as Brazil continue to strengthen cancer surveillance and access to specialist treatment. In the Middle East & Africa, the GCC is set to reach USD 0.33 billion in 2026.

South Africa Cell and Gene Therapy Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 1.54 % of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Emphasis on Research and Development by Key Players to Propel Market Competition

The global market is highly consolidated, with companies such as Vertex Pharmaceuticals Incorporated, Novartis AG, Bristol-Myers Squibb Company, Krystal Biotech, Inc., Rocket Pharmaceuticals, F. Hoffmann-La Roche Ltd., and Gilead Sciences, Inc. holding significant global cell and gene therapy market share. Strategic partnerships, new product launches, pipeline development, and increased investments in the sector drive these companies' market share gain.

- For instance, in August 2025, Kite (Gilead) announced plans to acquire Interius to advance a platform intended to generate engineered immune cells inside the patient, potentially reducing ex vivo manufacturing burdens.

Other notable players in the global market include Bayer AG, CRISPR Therapeutics, and Adaptimmune. These companies are expected to prioritize technological advancements in gene therapies, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY CELL AND GENE THERAPY COMPANIES PROFILED

- Vertex Pharmaceuticals Incorporated (U.S.)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Krystal Biotech, Inc. (U.S.)

- Rocket Pharmaceuticals (U.S.)

- Hoffmann-La Roche Ltd. (Switzerland)

- Bayer AG (Germany)

- CRISPR Therapeutics (Switzerland)

- Gilead Sciences, Inc. (U.S.)

- Adaptimmune (U.K.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Lexeo Therapeutics, Inc. entered a research collaboration with Johnson & Johnson to investigate localized cardiac delivery of gene therapy. The collaboration aimed to advance the potential efficacy and safety profile of gene therapy for genetically mediated cardiovascular diseases.

- February 2026: Cellipont Bioservices and Soter Bio announced a strategic collaboration to support integrated U.S. cell therapy manufacturing.

- January 2026: Nona Biosciences collaborated with Link Cell Therapies. This collaboration leveraged Nona's proprietary human HCAb Harbour Mice platform and its innovative direct CAR-function-based HCAb library screening platform, NonaCarFx, to generate novel CAR-T cell therapy

- January 2026: ElpasBio Holdings with Fosun Kairos for the commercialization of ElpasBio's investigational allogeneic human adipose-derived mesenchymal stem cell (haMPC) therapy, lotazadromcel for the treatment of knee osteoarthritis (KOA) in Mainland China, Hong Kong SAR, and Macau SAR.

- September 2025: Scientific and Basilard BioTech established a technology partnership for the advancement and scaling of Celletto, a nanomechanical, non-viral gene delivery platform, with an emphasis on increasing efficiency, cost, and scalability for T-cell and induced pluripotent stem cell (iPSC) workflows.

REPORT COVERAGE

The report provides a comprehensive global cell and gene therapy market analysis and covers a detailed assessment of the industry across key therapy types, end users, and major regions. It analyzes market trends, growth drivers, restraints, challenges, and emerging opportunities influencing demand for cell and gene therapy across different treatment settings. The study also evaluates the impact of rising clinical development activity, regulatory approvals, manufacturing expansion, reimbursement dynamics, and increasing investment by biopharmaceutical companies on overall market growth. In addition, the report provides insights into the competitive landscape, including key company profiles, strategic developments, product approvals, partnerships, acquisitions, and capacity expansion initiatives shaping the market. along with segment-level outlook by type and end user providing a comprehensive understanding of the market’s long-term outlook.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 31.10% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, End User, and Region |

| By Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 12.21 billion in 2025 and is projected to reach USD 143.55 billion by 2034.

In 2025, North America’s market value stood at USD 6.42 billion.

The market is expected to grow at a CAGR of 31.10% over the forecast period of 2026-2034.

The cell therapy segment is expected to lead the market.

The rising prevalence of cancer and rare diseases is driving the market growth.

Vertex Pharmaceuticals Incorporated, Novartis AG, Bristol-Myers Squibb Company, Krystal Biotech, Inc., and Rocket Pharmaceuticals are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us