Membrane Bioreactor Market Size, Share & Industry Analysis, By Membrane Type (Hollow Fiber Membranes, Flat Sheet Membranes, and Multi-Tubular/Capillary Membranes), By System Configuration (Submerged MBR Systems and Side-Stream MBR Systems), By End-Use (Municipal Wastewater Treatment and Industrial Wastewater Treatment), and Regional Forecast, 2026-2034

Membrane Bioreactor Market Overview

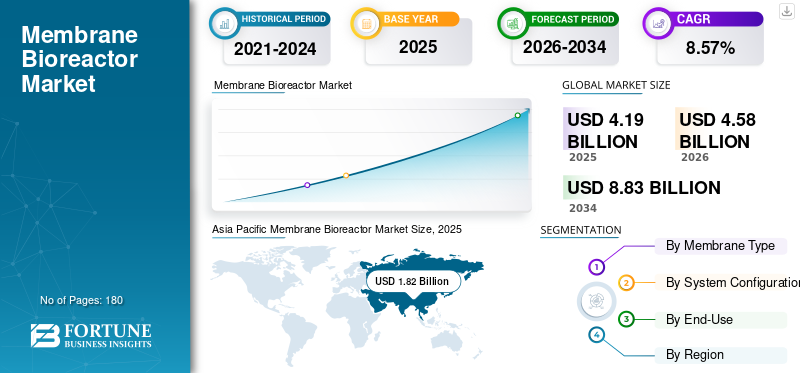

The global membrane bioreactor market size was valued at USD 4.19 billion in 2025. The market is projected to grow from USD 4.58 billion in 2026 to USD 8.83 billion by 2034, exhibiting a CAGR of 8.57% during the forecast period. Asia Pacific dominated the membrane bioreactor market with a market share of 43.43% in 2025. Moreover, the Asia Pacific market is experiencing rapid growth supported by rising investments in municipal and industrial wastewater treatment, decentralized plants, and advanced membrane technologies that enable high‑quality effluent reuse.

A Membrane Bioreactor (MBR) is an advanced wastewater treatment process that integrates biological degradation (using microorganisms to eat organic matter) with membrane filtration (using microfiltration or ultrafiltration membranes) to separate solid particles from liquid. It is a modern alternative to the Conventional Activated Sludge (CAS) process, replacing secondary clarifiers and tertiary filtration with a single membrane unit.

- In January 2026, Kuwait has awarded a Chinese state‑owned group, China State Construction Engineering Corporation, a roughly USD 3.3 billion contract to build, operate, and maintain its largest sewage treatment plant at North Kabd, with a capacity of up to 1 million cubic meters per day over a 10‑year period.

Veolia Water Technologies holds a leading position in the global MBR market, characterized by a massive installed base, a comprehensive portfolio of proprietary technologies, and a strong global presence in both municipal and industrial sectors with Xylem Inc., Kubota Corporation standing out as dominant global leaders due to their extensive installed bases, advanced membrane technologies, and long-standing industry presence.

Download Free sample to learn more about this report.

Membrane Bioreactor Market Key Takeaways

- 2025 Market Size: USD 4.19 billion

- 2026 Market Size: USD 4.58 billion

- 2034 Forecast Market Size: USD 8.83 billion

- CAGR: 8.57% from 2026–2034

- Asia Pacific dominated the membrane bioreactor market with a 43.43% share in 2025.

- Hollow fiber membranes led the market with a 64.91% share in 2025.

- Submerged MBR systems accounted for the largest share at 78.35% in 2025.

Asia Pacific

Asia Pacific led the market with USD 1.82 billion in 2025 and accounted for 43.43% of global revenue.

Europe

Europe was the second-largest regional market, valued at USD 1.07 billion in 2025.

North America

North America reached USD 0.76 billion in 2025, supported by infrastructure upgrades and water reuse initiatives.

U.S.

The market was valued at USD 0.66 billion in 2025, representing approximately 15.73% of global revenue.

Japan

The market reached USD 0.23 billion in 2025, accounting for around 5.56% of global revenue.

Read More

MEMBRANE BIOREACTOR MARKET TRENDS

Increasing Adoption of Water Reuse & Recycling is Shaping Market Trends

Increasing adoption of water reuse and recycling is a key driver shaping the MBR market, as industries and municipalities seek compact, high‑quality effluent solutions to meet tightening discharge norms and water‑stress challenges. These are increasingly deployed in municipal wastewater reuse for irrigation, industrial processes, and groundwater recharge, as well as in zero‑liquid‑discharge and decentralized systems. Governments and corporations are prioritizing circular‑water‑economy models, boosting investments in advanced MBR‑based reuse projects, which in turn expands the technology’s footprint in both developed and emerging markets.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Water Scarcity is a Primary Driver for Market Growth

Rising water scarcity is becoming a primary driver for the membrane bioreactor market growth, as regions with stressed freshwater resources seek advanced wastewater treatment and reuse solutions. Declining surface‑water availability and growing urban and industrial water demand are pushing municipalities and industries to adopt MBR systems that deliver high‑quality effluent suitable for reuse. Governments in water‑scarce areas, including the Middle East and parts of Asia, are increasingly investing in MBR‑based plants to close water‑loop gaps and support sustainable water‑management programs, thereby accelerating technology adoption and market expansion.

- In March 2026, in India, Government of Delhi has launched a time‑bound plan to overhaul its water and sewer infrastructure following a critical CAG report, aiming to end untreated sewage discharge, plug high water losses, and achieve 100 percent sewer connectivity and 1,500 MGD treatment capacity over the next two years.

MARKET RESTRAINTS

High Capital and Operational Costs to Restraint Market Growth

High capital and operational costs act as a key restraint on the market, particularly in developing economies and smaller utilities with limited budgets. Such systems entail substantial upfront expenditure on membranes, aeration, control systems, and steel/civil works, making them more expensive than conventional activated‑sludge plants. Ongoing operational burdens include membrane replacement, energy‑intensive aeration, chemical cleaning, and skilled maintenance, which raise the total cost of ownership and deter price‑sensitive buyers. As a result, end‑users often opt for lower‑cost alternatives unless regulatory pressure or water‑reuse needs justify the premium, thereby limiting broader MBR adoption despite its technical advantages.

MARKET OPPORTUNITIES

Integration of Industrial Zero Liquid Discharge Systems Expected to Create Lucrative Opportunities

Integration of MBRs into industrial Zero Liquid Discharge (ZLD) systems is expected to create lucrative opportunities in the MBR market. They serve as a robust pre-treatment step that removes organics and suspended solids, enabling downstream ZLD units such as reverse osmosis and evaporators to operate more efficiently and with lower fouling risk. Industries in textiles, power, petrochemicals, and food processing are increasingly adopting MBR‑based ZLD configurations to meet stringent effluent norms, minimize freshwater intake, and recover water for reuse. This alignment with ZLD mandates and circular‑water strategies is driving demand for advanced MBR systems, especially in water‑scarce regions, thereby opening high‑value growth avenues for membrane and technology providers.

MARKET CHALLENGES

Managing Membrane Fouling & Lifespan May Create Challenges for Market Growth

Managing membrane fouling and ensuring adequate membrane lifespan remains a significant challenge for the market. Membrane fouling reduces permeability, increases energy consumption, and raises operating costs due to frequent cleaning and downtime. Over time, repeated fouling and chemical cleaning shorten membrane life, leading to higher replacement frequency and capital outlay. These issues diminish the economic attractiveness of MBR systems, especially for cost‑sensitive projects and regions with inconsistent feed‑water quality. Moreover, lack of standardized fouling‑mitigation protocols and operator expertise can undermine long‑term performance, discouraging wider adoption. As a result, persistent fouling and lifespan concerns continue to constrain market growth despite the technology’s high‑quality effluent and compact footprint.

Segmentation Analysis

By Membrane Type

Hollow Fiber Membranes Dominated Due to High Packaging Density and Compact Design

Based on membrane type segmentation, the market is classified into hollow fiber membranes, flat sheet membranes, and multi-tubular/capillary membranes.

In 2025, hollow fiber membranes dominated the segment, capturing 64.91% of the membrane bioreactor market share. This growth is due to their high packing density, compact design, and lower energy requirements, making them well suited for large‑scale municipal and industrial wastewater treatment.

Multi‑tubular/capillary membrane systems have emerged as the fastest‑growing segment with a CAGR of 11.68% over the study period. Such growth is supported by their robustness, ease of cleaning, and suitability for high‑strength or challenging industrial effluents where reliability and operational flexibility are critical.

By System Configuration

Submerged MBR Systems Dominated Due to High Efficiency for Large-scale Wastewater Treatment

Based on system configuration segmentation, the market is classified into submerged MBR systems and side-stream MBR systems.

In 2025, submerged MBR systems dominated the segment with a market share of 78.35%. The growth is due to their compact footprint, lower energy consumption, and seamless integration with activated sludge processes, making them ideal for large‑scale municipal wastewater treatment.

Side‑stream MBR systems have emerged as the fastest‑growing segment with CAGR of 9.54%. It is driven by their flexibility in retrofitting existing plants, better fouling control, and suitability for high‑strength industrial effluents where precise operating conditions and easier maintenance are required.

By End-Use

To know how our report can help streamline your business, Speak to Analyst

Municipal Wastewater Treatment Segment Dominated Due to High Demand for Anaerobic Digestion and Biogas Recovery

Based on end-use segmentation, the market is bifurcated into municipal wastewater treatment and industrial wastewater treatment.

In 2025, municipal wastewater treatment dominated the segment with a market share of 66.51%. As large‑scale sewage plants generate consistent organic loads ideal for anaerobic digestion and biogas recovery.

Industrial wastewater treatment is the fastest‑growing segment with a CAGR of 9.86%. This growth is fueled by stricter effluent norms, rising biogas incentives, and growing adoption of on‑site digesters in food, beverage, pulp and paper, and chemical sectors.

Membrane Bioreactor Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Membrane Bioreactor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest share in 2025, valued at USD 1.82 billion, and in 2026 is estimated at USD 2.01 billion. Asia Pacific market is the largest and fastest‑growing market, driven by rapid urbanization, industrialization, tightening discharge norms, and acute water‑stress in China, India, and Southeast Asian nations. The market is expanding rapidly, supported by rising investments in municipal and industrial wastewater treatment, decentralized plants, and advanced membrane technologies that enable high‑quality effluent reuse.

China Membrane Bioreactor Market

The China market in 2025 was valued at around USD 0.70 billion, accounting for roughly 16.67% of the global market revenues. The country’s market is one of the world’s largest, driven by rapid urbanization, strict discharge norms, and acute water stress. Stricter wastewater discharge norms, rapid urbanization, water scarcity, rising demand for water reuse, and growth in municipal and industrial wastewater treatment plants are key drivers of China’s market.

India Membrane Bioreactor Market

India's market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 0.35 billion, representing approximately 8.31% of the global market.

Japan Membrane Bioreactor Market

The Japan market size in 2025 was valued at around USD 0.23 billion, accounting for approximately 5.56% of global revenues.

Europe

Europe emerged as second largest market with a valuation of USD 1.07 billion in 2025. Europe’s market is expanding steadily, supported by strict EU wastewater directives, water‑reclamation targets, and strong uptake in municipal and industrial treatment, with Germany leading regional adoption.

Germany Membrane Bioreactor Market

The German market in 2025 was valued at around USD 1.07 billion. It is projected to reach USD 1.17 billion by 2026, representing approximately 5.23% of the global industry revenues.

North America

The North America market reached USD 0.76 billion by 2025 and the market is growing strongly. The growth is driven by aging infrastructure upgrades, urban population growth, water scarcity, and strong water‑reuse initiatives drive North America’s market.

U.S. Membrane Bioreactor Market

With North America's strong contribution and the U.S. dominance in the region, the U.S. market was valued at around USD 0.66 billion in 2025, accounting for roughly 15.73% of the global market. The U.S. market is growing steadily, driven by stringent discharge regulations, aging infrastructure, and rising industrial treatment needs, nutrient‑removal mandates, PFAS concerns, and automation‑driven efficiency gains further push adoption in municipal and industrial sectors. Hollow‑fiber‑based submerged MBRs dominate, with strong adoption in water‑stressed regions such as the western and southern states.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.27 billion in 2026. The region’s market is growing rapidly, driven by urbanization, Growing industrialization, water scarcity, and demand for water reuse in sectors like food and beverage, textiles, and mining further boost adoption in the region.

Brazil Membrane Bioreactor Market

Brazil's market reached approximately USD 0.10 billion in 2025, accounting for a very minor share of the global market.

Middle East & Africa

The Middle East & Africa accounts for market share of 7.2% in 2025 and expected to witness significant growth in this market space during the forecast period. The Middle East and Africa market is set to reach a valuation of USD 0.32 billion in 2026. The market in this region is growing steadily, led by Expanding industries, stricter discharge regulations, and rising demand for water reuse and recycling in oil & gas, petrochemicals, and smart‑city projects further boost adoption.

GCC Membrane Bioreactor Market

The GCC market reached approximately USD 0.16 billion by 2025, accounting for around 3.83% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Collaborations Strengthen Competitive Positioning of Vendors

The global industry is considered consolidated, featuring a mix of major global players and numerous regional market players. Top-tier companies include Veolia Water Technologies, SUEZ Water Technologies & Solutions, Kubota Corporation, and Toray Industries, Inc., among others. For instance, in July 2025, Toray has announced a new high‑efficiency separation membrane module for biopharmaceutical manufacturing that significantly cuts production costs, boosts facility utilization, and improves process robustness by enabling higher‑throughput, more compact purification trains in single‑use and stainless‑steel facilities.

LIST OF KEY MEMBRANE BIOREACTOR COMPANIES PROFILED

- Veolia Water Technologies (France)

- SUEZ Water Technologies & Solutions (France)

- Kubota Corporation (Japan)

- Toray Industries, Inc. (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- Koch Separation Solutions (Japan)

- Evoqua Water Technologies (U.S.)

- Xylem Inc. (U.S.)

- Pentair plc (U.S.)

- Alfa Laval AB (Sweden)

- Hitachi Zosen Corporation (Japan)

- Huber SE (Germany)

- GE Water & Process Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: xAI announced development of world’s largest ceramic MBR in Memphis, treating 49.2 MLD of municipal wastewater for cooling its AI supercomputer. This, along with CERAFILTEC supplying advanced ceramic membranes to enable reliable, plastic‑free water reuse, and protect local aquifers.

- February 2026: United Utilities’ Enterprise has named DuPont as its single preferred supplier for MBR technology. Further, to be deployed at major wastewater treatment works in the North West, including the U.K.’s largest MBR at Wigan, supporting higher capacity and stricter water‑quality standards.

- August 2025: Watercare announced new 6.0 MLD wastewater plant in Raglan, New Zealand. It is where DuPont’s MemPulse MBR and OxyMem MABR are combined to deliver high‑quality effluent with low total nitrogen, enabling land‑based discharge and meeting strict environmental standards.

- May 2025: Osmoflo and CERAFILTEC have expanded their partnership into an exclusive agreement for Australia, New Zealand, and the Pacific. Further, enabling Osmoflo to integrate CERAFILTEC’s advanced ceramic membranes into water, wastewater, and desalination systems, including MBR upgrades and retrofits, to deliver more robust, sustainable, and PFAS‑free filtration solutions.

- March 2024: Toray India has announced plans to strengthen its presence in India’s advanced materials and engineered‑plastics market. Further, focusing on expanding production capacity, localizing high‑performance polymers, and reinforcing supply‑chain resilience for automotive, electronics, and industrial applications within India and the broader Asia Pacific region.

REPORT COVERAGE

The global membrane bioreactor market analysis provides an in-depth study of the market size & forecast by all the segments included in the report. It contains details on the market dynamics and industry trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market report also encompasses a detailed competitive landscape, including market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.57% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Membrane Type, System Configuration, End-Use, and Region |

| By Membrane Type |

|

| By System Configuration |

|

| By End-Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.19 billion in 2025 and is projected to reach USD 8.83 billion by 2034.

In 2025, Asia Pacifics market value stood at USD 1.82 billion.

The market is expected to exhibit a CAGR of 8.57% during the forecast period.

The municipal wastewater treatment sector led the end-use segment.

The rising water scarcity is driving the market.

Veolia Water Technologies, SUEZ Water Technologies & Solutions, Kubota Corporation, and Toray Industries, Inc. are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us