Military Aerospace & Defense Lifecycle Management Market Size, Share & Industry Analysis, By Solution (Digital Engineering & PLM Backbone, Configuration, Airworthiness & Compliance Management, Sustainment & Maintenance Management Platforms, Supply Chain, & Others), By Platform (Fixed-Wing Aircraft, Rotorcraft, Space Systems, & Others), By Lifecycle Phase (Concept & Requirements, Engineering, Development & Test, Production, Assembly & Acceptance, & Others), By End User (Defense Ministries / Armed Services, Defense Primes / OEMs, Depots, & Others), and Regional Forecast, 2026-2034

Military Aerospace & Defense Lifecycle Management Market Size and Future Outlook

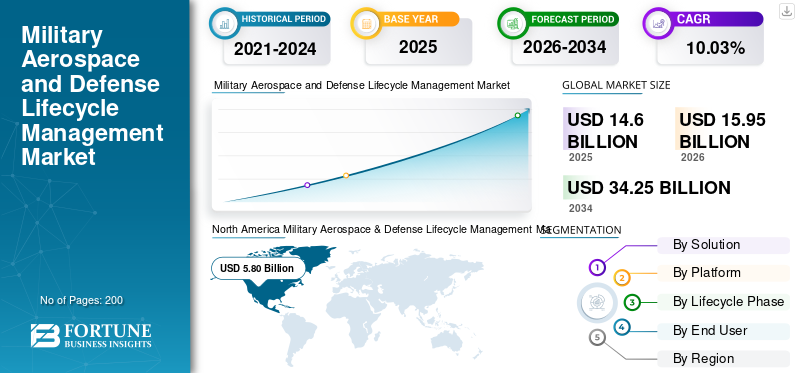

The global military aerospace & defense lifecycle management market size was valued at USD 14.60 billion in 2025. The market is projected to grow from USD 15.95 billion in 2026 to USD 34.25 billion by 2034, exhibiting a CAGR of 10.03% during the forecast period. North America dominated the military aerospace & defense lifecycle management market, with a market share of 39.72% in 2025.

Military aerospace and defense lifecycle management manages complex systems like aircraft, drones, satellites, and missiles from design, procurement, manufacturing, and maintenance through Product Lifecycle Management (PLM), Service Lifecycle Management (SLM), upgrades and disposal, maximizing readiness, cutting costs, and ensuring compliance. It includes data analytics, digital twins, AI-driven predictive maintenance, and integrated ERP for real-time insights across phases. These systems are used primarily in air forces for fighter jets, UAVs, and transport aircraft to handle obsolescence, regulatory standards, and aging fleets amid harsh operations. Key drivers for the market growth are rising platform complexity, budget pressures for return on investment, modernization needs, and AI/cloud for efficiency, and more.

Key players include Lockheed Martin, Boeing, PTC, and among others. They provide integrated sustainment services by offering comprehensive aircraft lifecycle solutions.

Download Free sample to learn more about this report.

MILITARY AEROSPACE & DEFENSE LIFECYCLE MANAGEMENT MARKET TRENDS

Integration of AI for Predictive Lifecycle Management is a Market Trend

Integration of AI for predictive lifecycle management emerges as a pivotal trend in military aerospace and defense because it shifts maintenance from reactive schedules to proactive strategies, anticipating failures through real-time sensor analysis. This addresses aging fleets and complex systems by enabling smarter decision making, optimizing asset performance, and ensuring mission readiness without human oversight limitations. Furthermore, AI's ability to process vast range of data streams fosters adaptive strategies, streamlining sustainment across design, operations, and upgrades amid evolving threats.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Modernization Programs Is Anticipated To Drive Market Growth

Rising modernization programs is driving the military aerospace and defense lifecycle management market growth by addressing aging fleets that require upgrades to maintain combat effectiveness against evolving threats. Budget reallocations prioritize modernization programs over new builds, fueled by geopolitical pressures demanding rapid adaptability in fighters, UAVs, and transports. These initiatives extend platform’s lifespans through retrofits, avionics enhancements, and sensor integrations, avoiding costly full replacements while integrating next-gen capabilities like networked warfare.

MARKET RESTRAINTS

Cybersecurity vulnerabilities to Pose Hindrance in Market Growth

Cybersecurity vulnerabilities restrain the implementation of lifecycle management by exposing interconnected systems to sophisticated state-sponsored attacks targeting sensors, avionics, and supply chains. As Internet of Things (IoT) and Artificial Intelligence (AI) integration expands data flows across fighters and UAVs. Adversaries exploit weak links for espionage or disruption, compromising mission-critical operations. Legacy or traditional infrastructure lacks modern defenses, amplifying risks from jamming, spoofing, and ransomware amid geopolitical cyber warfare.

MARKET OPPORTUNITIES

Emerging Lifecycle-as-a-Service Models Creates New Market Opportunities

Emerging Lifecycle-as-a-Service (LCaaS) models represent a key market opportunity in the market by shifting from traditional ownership to performance-based contracts focused on outcomes like availability and readiness. Providers handle end-to-end solutions from monitoring and upgrades to disposal freeing operators to prioritize missions while leveraging provider expertise in digital tools. This aligns with tightening budgets and complex assets, enabling scalable modernization without massive upfront capital, particularly for aging fleets needing continuous adaptation.

MARKET CHALLENGES

Regulatory Compliance Across Multinational Operations Present a Major Market Challenge

Regulatory compliance across multinational operations poses a significant market challenge in military aerospace and defense lifecycle management by imposing divergent standards like International Traffic in Arms Regulations (ITAR), Federal Acquisition Regulation (FAR), Cybersecurity Maturity Model Certification (CMMC), and European Union Aviation Safety Agency (EASA) that vary by region. Moreover, coordinating data sharing, audits, and certifications among global partners creates inconsistencies, delaying sustainment activities for aircraft and UAVs. Additionally, frequent regulatory updates demand constant vigilance and resource allocation, complicating supply chain traceability and export controls amid international collaborations.

Segmentation Analysis

By Solution

High Cost Effectiveness to Boost the Sustainment & Maintenance Management Segmental Growth

Based on the solution, the market is segmented into digital engineering & PLM backbone, configuration, airworthiness & compliance management, sustainment & maintenance management platforms, supply chain, Spares & obsolescence management, lifecycle analytics & digital twin, and others.

The sustainment & maintenance management platforms segment is anticipated to account for the largest market share. The segmental growth is owing to drastic reduction in overall maintenance costs done by sustainment platforms, which is crucial, considering defense organizations' relatively limited financial resources.

The lifecycle analytics & digital twin segment is anticipated to rise with a highest CAGR of 10.47% over the forecast period.

By Platform

Fixed-Wing Aircraft Segment Accounted For Largest Market Share Due To Requirement of Constant Upgrades

Based on platform, the market is segmented into fixed-wing aircraft, rotorcraft, Uncrewed Air Systems (UAS) / attritable systems, space systems (satellites, payloads, ground control), and others.

In 2025, the fixed-wing aircraft segment dominated the global market. The segmental growth is mainly due to constant upgrades required by these aircraft for their avionics, sensors, and weapons systems.

The Uncrewed Air Systems (UAS) / attritable systems segment is projected to grow at a CAGR of 10.63% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Lifecycle Phase

Operational Readiness for Aging Fleets is Leading to the Dominance of Operations & sustainment Segment

Based on the lifecycle phase, the market is segmented into concept & requirements, engineering, development & test, production, assembly & acceptance, fielding & deployment, operations & sustainment, upgrade / modernization & service life extension, and retirement, disposal & demilitarization.

The operations & sustainment segment is anticipated to witness a dominating market share over the forecast period. This is due to its focus on maintaining operational readiness through continuous maintenance, upgrades, and logistics support for aging fleets, ensuring mission-capable rates amid budget constraints favoring sustainment over new acquisitions.

The upgrade / modernization & service life extension segment is projected to grow at a CAGR of 10.58% over the forecast period.

By End User

Stringent Maintenance Requirement is Propelling The Lion’s Share Of Defense Ministries / Armed Services Segment

Based on end user, the market is segmented into defense ministries / armed services, defense primes / OEMs, depots, arsenals & government maintenance commands, suppliers, and others.

The defense ministries / armed services segment dominated the end user segment. The segmental dominance is due to their stringent maintenance requirements ensuring zero-tolerance for failures in high-stakes operations. These mandates drive demand for advanced sustainment solutions like predictive analytics and compliance tracking to maintain peak readiness across global deployments.

In addition, suppliers segment is projected to grow at a CAGR of 10.62% from 2026-2034.

Military Aerospace & Defense Lifecycle Management Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Military Aerospace & Defense Lifecycle Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant military aerospace & defense lifecycle management market share in 2024, valuing at USD 5.33 billion, and also maintained the leading share in 2025, with USD 5.80 billion. North America dominates due to substantial U.S. defense budgets being focused on F-35 sustainment and B-21 lifecycle integration. Investments target AI-driven predictive maintenance for fleet readiness.

U.S. Military Aerospace & Defense Lifecycle Management Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be valued approximated at around USD 3.82 billion in 2026, growing roughly with 6.46% CAGR. The growth in the U.S. is driven through DoD modernization prioritizing aging fleet upgrades like F-16s.

Europe

Europe is projected to record a steady growth rate during the forecast period with 9.74%, which is the second highest among all regions, and is expected to reach a valuation of USD 3.22 billion by 2026. Europe's market grows steadily through NATO driven interoperability requirements in multinational programs like the Future Combat Air System (FCAS), compelling standardized lifecycle approaches for shared platforms across member states.

U.K. Military Aerospace & Defense Lifecycle Management Market

The U.K. market in 2026 is estimated to be around USD 1.22 billion, increasing with roughly 10.20% CAGR during the study period. The U.K. advances its capabilities through the Tempest program under BAE Systems, establishing dedicated R&D hubs for end-to-end lifecycle management that incorporate digital threads for predictive analytics and export sustainment.

Germany Military Aerospace & Defense Lifecycle Management Market

Germany’s market is projected to reach approximately USD 0.79 billion in 2026. Germany focuses on Eurofighter Typhoon mid-life upgrades through partnerships with Airbus and MTU Aero Engines.

Asia Pacific

Asia Pacific region is estimated to reach USD 4.53 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. Asia Pacific experiences rapid expansion driven by escalating territorial tensions, prompting nations in the region to develop indigenous lifecycle capabilities for self-reliant sustainment of advanced platforms.

Japan Military Aerospace & Defense Lifecycle Management Market

The Japan market in 2026 is estimated at around USD 0.77 billion, with a growth rate roughly being 10.65% during the forecast period. Japan modernizes its F-15J fleet using Mitsubishi Heavy Industries' IoT-enabled platforms for predictive maintenance and upgrades, aligning with U.S. alliance requirements.

China Military Aerospace & Defense Lifecycle Management Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated to be around USD 1.77 billion. China aggressively invests in J-20 stealth fighter lifecycle management through Aviation Industry Corporation of China (AVIC), deploying state-backed digital PLM systems for stealth coatings and avionics sustainment.

India Military Aerospace & Defense Lifecycle Management Market

The India market in 2026 is estimated to be around USD 1.16 billion. India accelerates Tejas Mk2 lifecycle development via Hindustan Aeronautics Limited (HAL) and DRDO R&D centers, focusing on indigenous sustainment to reduce import dependency.

Rest of the World

The Rest of the World market includes Middle East & Africa and Latin America. Latin America advances through Brazilian Gripen E sustainment partnerships with Embraer, building regional MRO expertise. Middle East nations include Saudi Arabia and UAE upgrade F-15 platforms via Boeing hubs. The Middle East & Africa and Latin America market is set to reach a valuation of USD 1.13 billion and USD 0.73 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players are Competing Through Strategic Partnerships and Collaborations

The military aerospace and defense lifecycle management market remains moderately consolidated, with specialized players like Lockheed Martin, Boeing Defense, Northrop Grumman, and BAE Systems commanding shares through sustainment contracts and ITAR-compliant digital platforms.

Strategic partnerships drive expansion as Lockheed Martin teams with Palantir for F-35 ALIS/ODIN analytics, Boeing partners L3Harris for KC-46 digital twins alongside USAF, and Northrop Grumman collaborates IFS on B-21 PLM frameworks. These alliances strengthen supply chain resilience amid UAV sustainment demands, fighter modernization surges, and next-gen programs requiring predictive lifecycle capabilities.

LIST OF KEY MILITARY AEROSPACE & DEFENSE LIFECYCLE MANAGEMENT COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Boeing (U.S.)

- Northrop Grumman (U.S.)

- Raytheon Technologies Inc. (U.S.)

- General Dynamics (U.S.)

- BAE Systems PLC. (U.K.)

- Airbus (France)

- L3Harris Technologies Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS

- November 2025: A multi-year deal was announced by Honeywell and Abu Dhabi Aviation (ADA) to use Honeywell's Primus Epic integrated avionics system and other associated parts to expedite and simplify the Maintenance, Repair, and Overhaul (MRO) process for AW139 helicopters. This will boost productivity and decrease downtime by offering local repair logistics support to AW139 operators in the United Arab Emirates.

- September 2025: At the 2025 MRO Asia Pacific event in Singapore, Korean Air and Boeing announced a strategic collaboration agreement centered on innovative predictive maintenance analytics methodology and software.

- September 2024: Honeywell announced the completion of its all-cash acquisition of CAES Systems Holdings LLC (CAES) from Advent International, a private equity firm, for about USD 1.9 billion. In addition to improving Honeywell's defense technology solutions for land, sea, air, and space, the acquisition is anticipated to generate positive tailwinds for expansion throughout Honeywell's Aerospace Technologies division.

- December 2023: – Dassault Aviation has expanded its use of the 3DEXPERIENCE platform on a sovereign cloud to maximize the upkeep, overhaul, and repair of its fleet of Rafale aircraft for the French Ministry of Armed Forces, according to a statement from Dassault Systèmes.

- February 2023: Honeywell and BAE Systems Australia signed an agreement to provide aircraft parts and component repair services for 33 Hawk 127 aircraft at the 2023 Australian International Airshow (Avalon). The Royal Australian Air Force (RAAF) Hawk 127 fleet will use the five-year, non-exclusive contract. In order to fulfill the training objectives of the RAAF's military modernization program, it will assist with fleet maintenance, repair, and overhaul.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.03% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Solution, Platform, Lifecycle Phase, End User, and Region |

| By Solution |

|

| By Platform |

|

| By Lifecycle Phase |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 14.60 billion in 2025 and is projected to reach USD 34.25 billion by 2034.

In 2025, the market value for North America stood at USD 5.80 billion.

The market is expected to exhibit a CAGR of 10.03% during the forecast period.

By solution, the sustainment & maintenance management platforms segment is expected to dominate the market.

Rising modernization programs is anticipated to drive market growth.

Lockheed Martin, Boeing Defense, Northrop Grumman, and BAE Systems are few market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us