Military Electro-Optical and Infrared Systems Market Size, Share & Industry Analysis, By Platform (Land, Airborne, Naval and Dismounted), By System Type (Turrets/Gimbals, Targeting pods, Weapon/Vehicle sights, Surveillance directors and Driver vision/DVE), By Spectral Band (EO (visible/LLTV), SWIR, MWIR, LWIR and Multi‑spectral), By Application (ISR/Surveillance, Target acquisition, Navigation/DVE, Counter‑UAS and Others), By End User (Army/Land forces, Air force, Navy/Coast guard and SOF), and Regional Forecast, 2026-2034

Military Electro-Optical and Infrared Systems Market Size and Future Outlook

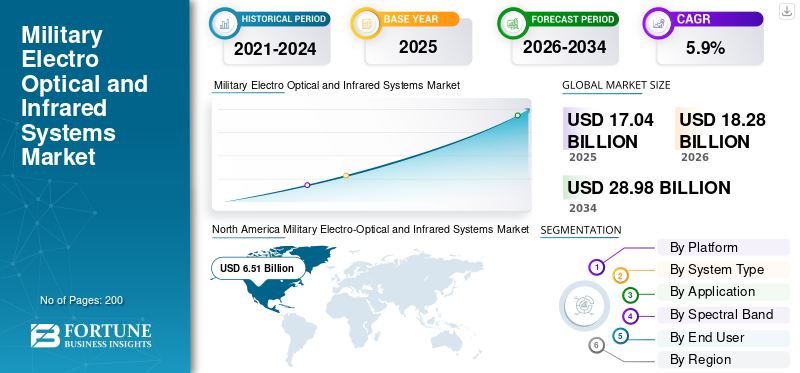

The military electro-optical and infrared systems market size was valued at USD 17.04 billion in 2025. The market is projected to grow from USD 18.28 billion in 2026 to USD 28.98 billion by 2034, exhibiting a CAGR of 5.9%% during the forecast period. North America dominated the military electro optical and infrared systems market with a market share of 38.20% in 2025.

The global market includes defense sensors that help forces detect, identify, and track targets in daylight, low light and darkness. This applies to land vehicles, aircraft, Unmanned Aerial Systems (UAS), ships and dismounted troops. The market features turrets, gimbals, targeting pods, sights, surveillance directors and driver-vision systems. The demand for these systems is growing as modern operations rely on sensors leading to improved capabilities for night fighting, longer-range Intelligence, Surveillance And Reconnaissance (ISR), faster target acquisition, and better counter-UAS and border or maritime surveillance.

Key players include Teledyne FLIR, L3Harris, RTX, Northrop Grumman, Collins, Safran, Thales, Leonardo, HENSOLDT Rheinmetall, Elbit, Rafael, IAI, and ASELSAN. They are driving growth by developing smaller and lighter multi-spectral payloads, upgrading older fleets and using sensor fusion and AI-enabled detection. This speeds up the find, fix, and track process in crowded, drone-heavy environments.

Download Free sample to learn more about this report.

MILITARY ELECTRO-OPTICAL AND INFRARED SYSTEMS MARKET TRENDS

Multi-Spectral Sensor Fusion and AI are Changing Battlefield Sensing and Speeding Up Market Growth

The shift from single-sensor feeds to intelligent, multi-sensor fusion is the most significant market trend. Militaries globally now prefer integrated views combining daylight, thermal, and ranging data to shorten the kill chain and significantly reduce operator workload. Imaging technology is shifting toward better EO IR systems designed for ISR, counter-UAS, and quick target handoff. This shift is especially driving adoption of UAVs and how companies deploy sensors for quick deployment.

In January 2025, Teledyne FLIR (Teledyne FLIR Defense) announced a five-year IDIQ contract worth up to USD 74.2 million. This contract is for delivering updated imaging surveillance systems for the U.S. Coast Guard. It shows that militaries are investing in sensor modernization and lifecycle upgrades instead of treating EO/IR as a one-time purchase.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Substantial Investment in Research & Development and Demand for UAVs Are Fueling Market Growth

Increased defense budgets and the rapid growth of drone fleets are fueling high demand for EO/IR payloads. As militaries prioritize persistent, real-time ISR, the need for advanced sensing capabilities on aircraft, vehicles, and stationary sites has become important for accelerated target acquisition, fueling the market growth.

In March 2024, the U.S. Department of Defense released its FY2025 Military Intelligence Program budget request of USD 28.2 billion. This shows the ongoing importance of ISR funding, which directly supports the purchase and maintenance of ISR tools such as EO/IR systems.

MARKET RESTRAINTS

Export Controls and Licensing Issues Slow Down Deployment and Cross-Border Growth

Export controls, end-use checks and licensing can delay or restrict the delivery of advanced infrared EO IR systems and sensitive imaging technology. For many programs related to ISR and other military uses, this compliance issue poses a significant barrier. This challenge is particularly relevant for integrators and market players seeking to expand advanced EO IR systems among allies and partners.

In February 2024, the U.S. Commerce Department’s Bureau of Industry and Security (BIS) released a final rule updating license requirements for certain cameras, systems, and related components under the Export Administration Regulations. It indicates that this category remains tightly controlled and focused on compliance.

MARKET OPPORTUNITIES

Shift from Passive Surveillance to Intelligent, Edge-Processed Autonomy Creates a Major Opportunity

The lucrative market opportunity is combining AI-driven, on-sensor processing with multi-spectral EO/IR payloads for UAVs and autonomous ground vehicles. With streaming high-definition video for human analysis, the next generation of EO/IR systems is also moving toward edge computing. Artificial intelligence detects, track, and classify threats, camouflaged targets, or obstacles in real time, even in GPS-denied or heavily jammed environments. This creates an opportunity to move beyond passive imaging to intelligent, actionable data.

MARKET CHALLENGES

Fragile Sensor Supply Chains and Long Lead Times are Challenging Market

A major issue in the electro-optical infrared systems field is requirement for specialized components, such as detectors, coolers, precision optics, and high-reliability electronics. These components often have few qualified suppliers and take a long time to manufacture. When demand rises, especially for ISR and counter-UAS, programs can experience delays, cost increases, and integration problems, even when funding is available. This situation hampers the military electro-optical and infrared systems market growth.

In January 2025, the U.S. Department of Defense’s Defense Business Board released its cleared report on “Supply Chain Illumination in the Department of Defense.” The report pointed out ongoing visibility gaps and weaknesses in defense supply chains.

Impact of Russia Ukraine War

Russia-Ukraine War is Driving the Demand for Electro-Optical Infrared Systems by Making ISR and Counter-UAS Fund Priorities

ISR efforts along with counter-UAS performance influence survival. Different factors are emphasizing improved EO/IR systems and infrared EO/IR systems for ongoing observation, target confirmation and drone identification. This change occurs as the adoption of unmanned aerial vehicles (UAVs) grows and defense budgets shift toward sensor-heavy military uses.

In April 2025, SIPRI reported that global military spending reached USD 2,718 billion in 2024, an increase of 9.4% in real terms. The report highlighted that Europe's spending rises were largely driven by the ongoing Russia-Ukraine war. This highlights increased procurement of ISR tools such as EO/IR.

Segmentation Analysis

By Platform

Due to Ongoing Demand for ISR And Use of UAVs Airborne Platform Leads Market

In terms of by platform, the market is categorized into land, airborne, naval, and dismounted.

Airborne platforms dominate the market as they give EO/IR a force-wide advantage. They provide a higher vantage point, wider coverage and quicker target confirmation for ISR missions. As fleets add more upgrades to crewed aircraft and UAV payloads, the need for stabilized turrets and targeting pods grows. Airborne EO/IR offers the best see-first effect for every system deployed.

In November 2025, Lockheed Martin announced the Sniper Evolved targeting pod upgrade. This upgrade acts as a connected airborne sensor that supports long-range targeting and ISR while also serving as an important node for sharing data. This demonstrates how airborne EO/IR capability is being improved and expanded.

Naval segment expected to show fastest growth at a CAGR of 6.6% over the forecast period.

By System Type

Turrets/Gimbals Dominates Due to Need for ISR Across Multiple Platforms and Fast UAV Integration

On the basis system type, the market is classified into turrets/gimbals, targeting pods, weapon/vehicle sights, surveillance directors, and driver vision/DVE.

Turrets/gimbals has highest market share as they are the plug-and-play foundation of modern electro-optical infrared systems. Each system includes a stabilized sensor ball that can be easily mounted on vehicles, aircraft, UAVs, ships and fixed sites with fewer redesign challenges. For ISR and typical military uses, buyers prefer turreted EO/IR sensor payloads. These systems combine stabilization, various sensor options (day, thermal, laser) and quick integration into mission systems. This setup allows programs to improve capabilities without having to rebuild the entire platform.

Turrets/Gimbals is expected to show fastest market growth at a CAGR of 6.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Spectral Band

LWIR Segment Leads as it Performs Well in all Weather and Can See Through Smoke

Based on spectral band, the market is segmented into EO (visible/LLTV), SWIR, MWIR, LWIR, and Multi‑spectral.

LWIR is preferred for its ability to provide reliable thermal images in challenging real-world situations, such as at night, in haze, dust, light fog and battlefield smoke, without needing an active emitter. For electro-optical infrared systems used in military applications such as ISR vehicle crew sighting, and force protection, the ability to function effectively in tough conditions keeps the demand for infrared EO IR systems focused on LWIR, even with the rise of multi-spectral payloads.

In October 2024, HENSOLDT introduced new optronic systems for Leopard 2A8 and PUMA. They showcased their ATTICA LWIR (long-wave infrared) and MWIR digital thermal imaging devices, which aim to improve reconnaissance performance in difficult weather and visibility conditions.

SWIR segment is expected to show fastest market growth at a CAGR of 7.8% across the forecast period.

By Application

Due to increasing demand for surveillance capabilities, ISR and surveillance are leading the EO/IR systems market.

Based on application, the market is segmented into, ISR/surveillance, target acquisition, navigation/DVE, counter‑UAS, and others.

the ISR/surveillance segment held the largest military electro-optical and infrared systems market. This is due to the daily eyes-on needed for modern military tasks, such as monitoring borders and maritime areas, strike support and counter-UAS operations. As defense budgets keep prioritizing ongoing sensing and the use of UAV rises, military forces are buying more advanced EO/IR systems that feature stabilized turrets and modern imaging technology. Thus, ISR and surveillance are the main use cases for most players in the market.

In January 2025, Teledyne FLIR announced a five-year IDIQ contract worth up to USD 74.2 million to provide modernized imaging surveillance systems (ESS-M) for the U.S. Coast Guard. This contract aids in ongoing surveillance missions across its helicopter fleets.

Counter‑UAS is fastest growing segment in market at a CAGR of 9.3% across the forecast period.

By End User

Army and Land Forces Lead Due to Ongoing Modernization of Ground Combat Units

Based on end user, the market is segmented into army/land forces, air force, navy/coast guard, and SOF.

Army and land forces segment leads as EO/IR is part of daily ground operations. This includes thermal weapon sights for soldiers, driver vision for vehicles and stabilized sensors on armored platforms for a see-first advantage. As night operations become more challenging and fleets and soldier systems receive constant upgrades, land forces continue to purchase EO/IR in larger quantities and more frequently than other end users.

In August 2024, Leonardo DRS announced a USD 117 million production order for the U.S. Army under the Family of Weapon Sights Individual (FWS-I) contract to keep delivering next-generation thermal weapon sights. This shows the ongoing large-scale procurement of EO/IR by land forces.

SOF segment is expected to show fastest market growth at a CAGR of 6.3% across the forecast period.

Military Electro-Optical and Infrared Systems Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East and Rest of the World (Africa, and Latin America).

North America

North America Military Electro-Optical and Infrared Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads the regional market due to large defense budgets and fast implementation of ISR and UAV technologies. The U.S., along with Canada to a lesser extent, views EO/IR as a key tool for ISR, as well as for daily military needs. This includes protecting ships, monitoring borders, and upgrading vehicles and aircraft. The area's quick program development, ongoing modernization purchases, and increasing use of UAV create strong demand for EO/IR systems and high-quality imaging technology.

U.S. Military Electro-Optical and Infrared Systems Market

Based on North America’s strong contribution the U.S. market reached USD 5.96 billion in 2025, increasing at a CAGR of 4.8%.

Europe

Europe market was the second largest in 2025 and estimated to have a CAGR of 6.4% over the forecast period. Europe is actively upgrading electro optical infrared systems for land vehicles, naval platforms and airborne ISR. This push is driven by the security situation between Russia and Ukraine, increased border surveillance needs and a noticeable shift toward modern EO-IR systems that combine day and thermal imaging and connect more quickly to networks. Russia is also a significant buyer and producer in the region, maintaining high levels of EO/IR activity even as Western Europe grows its procurement and research and development efforts.

U.K. Military Electro-Optical and Infrared Systems Market

U.K. market is projected to reach approximately USD 0.75 billion in 2026, equivalent to around 14.41% of industry revenues.

Germany Military Electro-Optical and Infrared Systems Market

The Germany market was at USD 0.65 billion, representing roughly 13.40% of revenues, in 2025.

Asia Pacific

Asia Pacific market is third largest and is anticipated to be the fastest growing segment during the forecast period, growing at a CAGR of 7.0%. Asia Pacific’s market growth is fueled by a need to watch wider and respond faster. There are more UAV fleets, increased maritime surveillance, and additional night-fighting upgrades for armored and mechanized forces. Countries are focusing on practical, deployable imaging technology such as driver night sights, surveillance payloads and thermal imagers. This technology directly improves readiness for ISR, border security and operations in contested environments.

China Military Electro-Optical and Infrared Systems Market

China’s market is projected to be one of the largest in Asia Pacific and 2025 revenues reached USD 1.41 billion, representing roughly 38.74% of sales.

India Military Electro-Optical and Infrared Systems Market

The India’s market in 2025 was at USD 0.58 billion, accounting for roughly 15.82% of Asia Pacific revenues.

Middle East

Middle East market is anticipated to be the second fastest growing segment during the forecast period growing at a CAGR of 5.8%. The demand for EO/IR in the Middle East stems from the need for continuous ISR coverage, drone threats and force protection. Buyers are still investing in turrets, gimbals and multi-sensor payloads for both airborne and ground applications. Another trend is the effort to build local capacity for assembly, integration and product development instead of depending on imports. Countries are trying to secure their supply chains and maintenance.

- In February 2025, the UAE's EDGE showcased a new suite of electro-optical/infrared systems at IDEX 2025. This event highlighted ongoing product development and a regional emphasis on EO/IR detection and tracking solutions.

Saudi Arabia Military Electro-Optical and Infrared Systems Market

Saudi Arabia market is projected to be one of the largest in Middle East and 2025 revenues was at USD 0.52 billion, representing roughly 34.18% of sales.

Rest of the World

Rest of World (Africa and Latin America), has comparatively smaller share but is growing at a CAGR of 3.9%. In Latin America and Africa, EO/IR purchases relate directly to real-world missions such as coastal monitoring, border surveillance and fleet modernization. Programs prefer durable EO/IR sights and directors that work day and night and are easy to maintain. Growth is steady rather than fast, but procurement stays consistent where maritime and border pressures are high.

- In June 2021, Safran announced that Brazil selected its PASEO XLR optronic (electro-optical) sight for the Tamandare-class frigates. This demonstrates how naval modernization programs encourage the use of EO/IR in Latin America.

Africa Military Electro-Optical and Infrared Systems Market

Africa’s market size was at USD 0.19 billion in 2025, and is expected to reach USD 0.33 billion in 2034, representing roughly 35.34% of sales.

Latin America Military Electro-Optical and Infrared Systems Market

The Latin America market was at USD 0.35 Billion, accounting for roughly 64.66% of revenues, in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Racing to Scale EO/IR Systems for ISR and UAV-Driven Military Applications

The market is led by a mix of sensor specialists and prime integrators that can deliver advanced EO/IR systems with strong imaging technology and smooth integration into platforms. The main demand comes from ISR and the growing demand for advanced surveillance capabilities. The rise of UAVs is pushing customers toward lighter and networked EO/IR payloads. In North America, this trend is supported by large defense budgets, which ensure consistent EO/IR upgrades and new purchases throughout the forecast period.

Key market players include Lockheed Martin Corporation, Teledyne FLIR, L3Harris, RTX, and Northrop Grumman, as well as European leaders such as Safran, Thales, Leonardo, and HENSOLDT. Strong suppliers from Israel and Turkey, such as Elbit Systems, Rafael, and ASELSAN, also play a significant role. These key players are advancing the market through significant investments in research and development. They focus on better stabilization, longer detection ranges, and multi-sensor fusion so that each EO/IR sensor works as part of a larger ISR system. Their recent initiatives, including new targeting pods, updated surveillance suites and sensor upgrades for vehicles and ships, demonstrate how electro optical and infrared capabilities are becoming essential rather than optional.

LIST OF KEY MILITARY ELECTRO-OPTICAL AND INFRARED SYSTEMS COMPANIES PROFILED

- BAE Systems (U.K.)

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (U.S.)

- Northrop Grumman (U.S.)

- L3Harris Technologies (U.S.)

- Teledyne FLIR (U.S.)

- Collins Aerospace (U.S.)

- General Atomics Aeronautical Systems (U.S.)

- Safran Electronics & Defense (France)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- HENSOLDT (Germany)

- Rheinmetall AG (Germany)

- Saab AB (Sweden)

- Ultra / Chess Dynamics (U.K.)

- Elbit Systems (Israel)

- Rafael Advanced Defense Systems (Israel)

- Israel Aerospace Industries (IAI / ELTA) (Israel)

- ASELSAN (Turkey)

- Hanwha Systems (South Korea)

- Mitsubishi Electric (Japan)

- Bharat Electronics Limited (BEL) (India)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Teledyne FLIR Defense announced it received a U.S. Army contract worth up to USD 32 million. The contract involves delivering and integrating advanced EO/IR systems for the Stryker Infantry Carrier Vehicle (ICV) Recon Kit. This addition will offer long-range detection and thermal imaging situational awareness. It underscores the strong demand for turret and gimbal systems in vehicle-mounted stabilized payloads.

- January 2026: Teledyne FLIR Defense announced a U.S. Army contract worth up to USD 32 million to deliver and integrate advanced EO/IR systems for the Stryker ICV Recon Kit, which supports Foreign Military Sales to Bulgaria.

- November 2025: Lockheed Martin showcased its Sniper Evolved direction, positioning the targeting pod as a more connected system that can act as a network node while supporting long-range targeting and ISR. This reflects the market’s shift from sensor as a box to sensor as a connected combat system, driving demand for upgrades.

- January 2025: Elbit Systems announced an approximately USD 60 million contract to supply a NATO European customer with its ReDrone Counter-UAS solution. Elbit pointed out that the package includes an EO day/night payload along with radar, SIGINT, and EW elements. This shows EO/IR being bought as part of integrated counter-drone systems.

- January 2025: Teledyne FLIR Defense announced a five-year IDIQ worth up to USD 74.2 million to modernize U.S. Coast Guard imaging surveillance systems. This is a clear sign that even mature fleets are funding EO/IR upgrades and maintenance to keep ISR performance updated throughout their lifecycle.

- August 2024: Leonardo DRS received a USD 117 million U.S. Army production order under the Family of Weapon Sights, Individual (FWS-I) IDIQ. This order supports ongoing production of thermal weapon sights. It shows how land forces buy EO/IR at scale as a regular readiness item, not just a one-time upgrade. In October 2024, HENSOLDT introduced three new digital optronic systems for the Leopard 2A8 and PUMA vehicles. The company presented these as upgrades that improve reconnaissance and targeting accuracy in harsh conditions. This reinforces the digital refresh cycle that keeps vehicle EO/IR budgets active.

- June 2022: The U.S. Navy awarded L3Harris a USD 205 million contract to provide a new passive EO/IR capability (SPEIR/SPATIAL) to improve fleet protection and navigation. This shows North America’s significant investment in EO/IR on a large scale.

REPORT COVERAGE

The global military electro-optical and infrared systems market analysis provide an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.9% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By System Type

|

|

|

By Spectral Band

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 18.28 billion in 2026 and is projected to reach USD 28.98 billion by 2034.

In 2025, the North America market value stood at USD 6.51 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period of 2026-2034.

The Airborne led the market, by platform.

Rising defense budgets for ISR and the use of unmanned aerial vehicles (UAVs) are fueling market growth.

Martin Corporation, RTX (Raytheon), Northrop Grumman, L3Harris Technologies, Teledyne FLIR, and Collins Aerospace, Safran Electronics & Defense, Thales, Leonardo, HENSOLDT, Elbit Systems and Rafael Advanced Defense Systems, are the top companies in the market.

North America dominated the market in 2024

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us