Motor Lamination Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Propulsion (ICE and Electric), By Motor Application (Propulsion, Auxiliary Systems, Energy Recovery, and Start-Stop), By Manufacturing Process (Stamping, Laser Cutting, and Etching), By Material (Silicon Steel, Cobalt Alloys, and Others), By Motor Type (Permanent Magnet Synchronous Motors (PMSM), Induction Motors, Brushless DC Motors (BLDC), and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

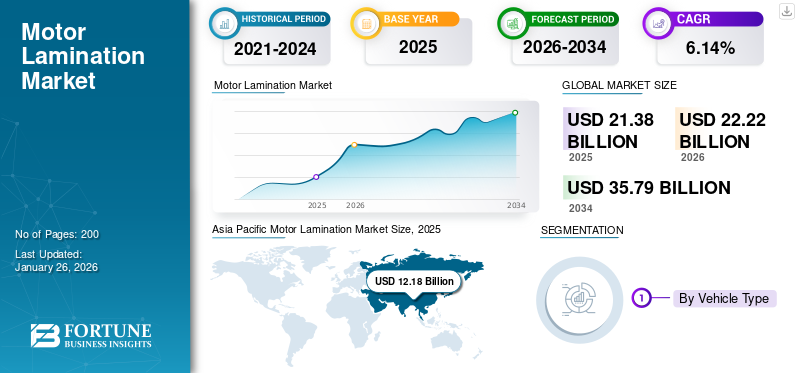

Motor Lamination Market Size and Future Outlook

The global motor lamination market size was valued at USD 21.38 billion in 2025. The market is projected to grow from USD 22.22 billion in 2026 to USD 35.79 billion by 2034, exhibiting a CAGR of 6.14% during the forecast period. Asia Pacific dominated the global market with a share of 56.99% in 2025.

Motor lamination refers to thin layers of steel or iron stacked together to form the core of an electric motor. These laminated sheets reduce energy loss by minimizing eddy currents, improving motor efficiency. In automotive applications, this helps motors operate smoothly, with reduced heat generation and energy consumption. Laminated cores are crucial in Electric Vehicles (EVs) and hybrid systems, enhancing overall performance and longevity.

The market is growing due to the elevating demand for Electric Vehicles (EVs) and hybrid vehicles, which require efficient motor components. However, high manufacturing costs associated with advanced lamination techniques pose a restraint. On the other hand, the continuous advancements in motor design and materials, such as high-grade steel and innovative manufacturing processes, are expected to drive market growth over the forecasted period.

Download Free sample to learn more about this report.

Motor Lamination Market KEY TAKEAWAYS

- 2025 Market Size: USD 21.38 billion

- 2026 Market Size: USD 22.22 billion

- 2034 Forecast Market Size: USD 35.79 billion

- CAGR: 6.14% from 2026–2034

- Asia Pacific dominated the motor lamination market with a 56.99% share in 2025.

- The SUVs segment is expected to account for the largest market share of 47.37% in 2026.

- The ICE segment is projected to dominate the market with a 77.41% share in 2026.

Asia Pacific

Asia Pacific reached USD 12.72 billion in 2026, driven by rapid EV adoption and automotive manufacturing.

North America

North America is projected to reach USD 3.95 billion in 2026, supported by advanced motor technologies.

Europe

Europe held an 18.43% market share in 2025, driven by growing electric vehicle production.

U.S.

The U.S. market is projected to reach USD 3.36 billion in 2026, fueled by expanding EV manufacturing.

Japan

Japan is projected to reach USD 0.70 billion in 2026, supported by investments in electric mobility.

Read More

Market Dynamics

Market Drivers

Growth of Electric Vehicle Industry Drives Market Demand

EVs rely heavily on electric motors, where laminations play a critical role in reducing energy losses, improving motor performance, and enhancing overall vehicle efficiency. As the adoption of EVs rises globally, automakers focus on improving motor technology to meet performance, range, and energy efficiency standards. Laminations help achieve these goals by minimizing eddy current losses, reducing heat generation, and optimizing energy use, all of which are crucial for the long-term success of EVs in the automotive sector. Thus, growth of electric vehicles plays a crucial role in generating the demand for the market over the forecasted period.

The International Energy Agency stated that, in 2023, nearly 14 million electric cars were sold globally. This marked a 35% increase from 2022, and the total number of electric cars on the roads reached 40 million. Weekly registrations exceeded 250,000, surpassing the total annual registrations of 2013. Electric cars represented 18% of global car sales, up from 14% in 2022 and just 2% in 2018, with battery electric cars making up 70% of the stock.

Market Restraints

Supply Chain Constraints to Hinder Market Growth

The motor lamination market is constrained by its dependency on specific raw materials, such as silicon steel, cobalt, and other alloys, which are essential for manufacturing efficient laminations. Fluctuations in the accessibility and prices of these materials significantly impact production costs and supply chain stability. Any disturbances in the supply of these raw materials due to geopolitical factors, natural disasters, or trade restrictions lead to delays and increased production costs, limiting the market growth. This dependency makes manufacturers vulnerable to external factors that disrupt market expansion.

In February 2025, The Center for Strategic & International Studies projects that steel prices in the U.S. are expected to increase by 8.2%, while aluminum prices are expected to witness a surge of 5.7%. This surge will directly affect industries such as automotive manufacturing, construction, and industrial tools, all of which heavily depend on these metals, which restrains market growth over the considered time frame.

Market Opportunities

Emerging Markets Provide Growth Opportunities

Emerging markets, particularly in regions such as the Asia Pacific, South America, and Africa, present significant growth opportunities. Rapid industrialization, rising urbanization, and increasing disposable incomes are driving higher vehicle production and demand. As countries in these regions adopt stricter emissions and fuel efficiency standards, automakers are increasingly investing in electric and hybrid vehicles, which require efficient motor systems. This shift boosts the demand for advanced motor laminations to enhance performance and energy efficiency. Moreover, the expansion of electric vehicle infrastructure and consumer acceptance of EVs in these markets further accelerate the need for high-quality motor components. Major players are investing in developing countries and establishing plants, fueling demand in the motor lamination market during the forecast period. In August 2024, EuroGroup Laminations, an Italian manufacturer of electric motor components, acquired a 40% stake in India's Kumar Precision Stampings.

Market Challenge

High Initial Cost and Technical Complexity Challenges Market Expansion

Manufacturing laminations for motors requires specialized materials, such as high-quality silicon steel, and complex processes that drive up expenses. Additionally, the need for advanced technology and precision in production further increases costs. These high costs make laminations less affordable, especially for smaller manufacturers and price-sensitive markets. As a result, automakers seek more cost-effective alternatives or delay in adopting advanced motor technologies, slowing the expansion of the market. This challenges the market demand.

Motor Lamination Market Trends

Focus on Lightweight Materials to Act a Market Trend

Lightweight motor laminations reduce the overall weight of electric motors, improving energy efficiency and extending battery life, which is essential for the performance of EVs. Manufacturers are progressively using innovative materials, such as high-strength, thinner steel, or alternative alloys, to create laminations that offer the same or better efficiency while reducing weight. This trend aligns with the broader automotive industry's goal of dropping vehicle weight to improve fuel economy and performance, particularly in the growing electric and hybrid vehicle segments.

In June 2024, Feintool System launched the glulock MD process, which improves rotor and stator production by using adhesive bonding to replace mechanical joints, which can cause energy loss. This method reduces material cost, energy use, and increases motor efficiency. It allows thinner sheets to be used, creating stronger stacks. Additionally, glulock MD supports integrated cooling solutions for electric motors, enhancing performance and compactness. Feintool’s advancements are pushing the boundaries of e-mobility, achieving up to a 10% efficiency increase and reducing iron losses by 30%, improving electric motor range.

Download Free sample to learn more about this report.

Impact of COVID-19

During the COVID-19 pandemic, initial lockdowns and disruptions in global supply chains led to delays in production and a temporary halt in automotive manufacturing, reducing the demand for motor laminations. Additionally, raw material and labor shortages affected manufacturing capabilities. However, as recovery began, there was a shift toward Electric Vehicles (EVs), which drove increasing demand for energy-efficient motor components. Despite challenges, the pandemic also accelerated the adoption of green technologies, creating long-term growth opportunities for laminations for motors in EVs and hybrid vehicles.

Segmentation Analysis

By Vehicle Type

Growing Popularity of SUVs Drives Segment's Growth

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs, and HCVs.

The SUVs segment is expected to account for 47.37% of the market in 2026, and is attributed to develop with the fastest-growing CAGR during the forecasted period. The growing popularity of SUVs, driven by consumer preference for larger, safer, and more versatile vehicles, has resulted in increased production of this segment. As SUVs become a dominant vehicle type, automakers require high-efficiency motor systems to meet performance expectations. This demand for powerful and efficient motors directly drives the need for laminations, which help improve motor performance and energy efficiency, especially in larger vehicles.

The International Energy Agency reports that SUVs made up 48% of global car sales in 2023, setting a record and reinforcing the dominant automotive trend of the early 21st century- the growing preference for larger and heavier vehicles.

LCVs segment held the second largest market share in 2024. The increasing demand for LCVs across industries, such as logistics and delivery, drives the need for efficient and durable motor systems. LCVs are essential for goods transportation and require powerful motors. As LCV production rises, there is a parallel demand for laminations to improve motor performance and energy efficiency, ensuring LCVs meet operational requirements and reduce fuel consumption. This drives the segmental growth over the forecasted period.

By Propulsion

Increased Focus on Hybrid Vehicles Drives the Growth of ICE Segment

The market by propulsion is segregated into categories, including ICE and electric.

The ICE segment is expected to dominate the market with a share of 77.41% in 2026. The rise of hybrid vehicles, which combine internal combustion engines with electric motors, is boosting the demand for laminations in the ICE segment. Hybrid vehicles rely on both ICE and electric motors, requiring efficient laminations to reduce energy loss and improve performance. As hybrid technology becomes more widespread, the demand for high-performance motor laminations continues to grow within the ICE vehicle segment.

The electric segment is attributed to grow at a CAGR of 7.20% over the forecasted period of 2026-2034. Governments worldwide are endorsing the adoption of electric vehicles through various incentives, tax breaks, and stricter emissions regulations. These policies encourage automakers to accelerate EV production, which, in turn, increases the demand for electric motors and motor laminations. Laminations of motors help EV manufacturers meet energy efficiency standards and performance expectations, driving growth in the electric vehicle segment of the market.

According to the European Automobile Manufacturers’ Association (ACEA), France offers various tax benefits and incentives to boost the adoption of electric and alternative fuel vehicles. These include exemptions on vehicles using electric, hybrid, CNG, LPG, and E85, ranging from 50% to full exemption. Electric vehicle types such as BEVs, FCEVs, and plug-in hybrid electric vehicles with over 50 km range are exempt from malus taxes. Vehicles emitting less than 60g CO2/km, except diesel, are exempt from TVS taxes. The government offers bonuses for new BEVs and FCEVs under EUR 47,000 (USD 49220.33) and 2.4 tonnes, with up to EUR 7,000 (USD 7330.69) for low-income households.

By Motor Application

Rising Demand for EVs and Increased In-car Electronic Features Drives Auxiliary Systems Market Growth

The market is categorized based on motor application into propulsion, auxiliary systems, energy recovery, and start-stop.

The auxiliary systems segment is anticipated to hold a dominant market share of 51.13% in 2026. The rise of hybrid and electric models has significantly driven the demand for efficient motors in automotive applications. Auxiliary systems, including air conditioning, power steering, and braking, rely on electric motors, making laminations crucial for optimal performance. As EV adoption grows, more auxiliary motors are required, thus fueling the demand for the market to support these systems' efficiency and longevity.

The energy recovery segment is attributed to propel at the fastest-growing CAGR over the forecasted period of 2026-2034. Regenerative braking systems, especially in electric and hybrid vehicles, are designed to capture and store energy that would otherwise be lost during braking. Efficient motors with high-performance laminations are vital for this process as they minimize energy loss and improve the overall recovery efficiency. With more automakers integrating regenerative braking, the demand for advanced laminations in energy recovery applications continues to grow, contributing to better energy management in vehicles.

In June 2023, ZF, as a preferred supplier and development partner, collaborated with British electric vehicle manufacturer Tevva to develop the regenerative braking system for its 7.5t battery-electric truck. This involved ZF working closely with Tevva engineers to integrate its Electronic Brake System (EBS) into Tevva's zero-emission electric trucks.

The propulsion segment is likely to grow with a considerable CAGR of 4.90% during the forecast period (2026-2034).

To know how our report can help streamline your business, Speak to Analyst

By Manufacturing Process

Versatility in Design Augments Stamping Segment Adoption

Based on the manufacturing process, the market is divided into stamping, laser cutting, and etching.

The stamping segment is expected to attain 54.59% of the market share in 2026. Stamping allows manufacturers to create a wide range of lamination shapes and sizes to fit various automotive applications. This versatility is essential for producing specialized components that cater to specific motor designs, from small auxiliary systems to large traction motors. The ability to customize the lamination shape and size with high precision makes stamping a preferred method for motor lamination production in the automotive industry.

The laser cutting segment is attributed to developing at the fastest-growing CAGR of 6.20% during the forecasted period of 2025-2032. Laser cutting offers superior precision and accuracy in shaping laminations, which is crucial for optimal motor performance. This process allows for intricate, fine cuts with minimal deviation, ensuring that laminations are produced to exact specifications. This precision reduces defects and increases motor efficiency, making laser cutting the preferred method for manufacturing motor laminations used in high-performance automotive motors.

By Material

Increasing EV Adoption Fuels the Silicon Steel Demand

Based on the material, the market is divided into silicon steel, cobalt alloys, and others.

Silicon steel held the largest motor lamination market share and is attributed to developing at the fastest-growing CAGR during the forecasted period of 2025-2032. Silicon steel is known for its excellent magnetic properties, which are crucial in reducing energy losses in automotive motors. The material’s high permeability enables efficient energy transfer, making it ideal for laminations. As electric vehicle adoption grows, the demand for high-performance materials such as silicon steel rises to optimize motor efficiency and improve vehicle range, directly driving its use in the market. The segment is foreseen to capture 60.09% of the market share in 2025.

The others segment held the second-largest market share in 2024. Other materials driving the market include aluminum alloys for lightweight and corrosion resistance, soft magnetic composites for reduced energy loss in high-frequency operations, nickel alloys for high-temperature resistance, copper for improved conductivity and reduced energy losses in electric vehicles, and iron powder for lightweight, energy-efficient sintered laminations. These materials enhance motor performance, efficiency, durability, and overall vehicle functionality in the growing automotive industry. This segment is forecasted to document a CAGR of 5.50% during the forecast period (2025-2032).

By Motor Type

Wide Application in EVs Fuels the Permanent Magnet Synchronous Motors (PMSM) Segment Growth

The market is segmented by motor type into Permanent Magnet Synchronous Motors (PMSM), induction motors, BrushLess DC motors (BLDC), and others.

The Permanent Magnet Synchronous Motors (PMSM) segment dominated the market in 2024 and is attributed to developing at the fastest-growing CAGR during the forecasted period of 2025-2032. They are widely favored for their high efficiency and performance in Electric Vehicles (EVs), providing a better power-to-weight ratio. Their ability to deliver consistent torque and improved energy efficiency makes them a popular choice, driving growth in the market. Automakers are adopting PMSMs to enhance vehicle range and reduce energy consumption, which fuels their demand. This segment is set to acquire 48.82% of the market share in 2025.

In October 2024, MAHLE and Valeo expanded their magnet-free electric motor portfolio for higher-segment vehicles. The two companies revealed that they had collaborated to develop a magnet-free electric axle system, offering peak power ranging from 220 kW to 350 kW. The company introduced the iBEE system (inner Brushless Electrical Excitation), a groundbreaking technology designed to enhance the performance and efficiency of magnet-free electric motors.

The induction motor segment held the second-largest market share in 2024. Induction motors are known for their cost-effective manufacturing, especially in comparison to other motor types such as PMSMs. Their simple design and reliance on induction rather than permanent magnets make them more affordable to produce. This cost advantage encourages the widespread adoption of induction motors in various automotive applications, contributing to the motor lamination market growth.

The BrushLess DC motors (BLDC) segment is likely to grow with a significant CAGR of 5.30% during the forecast period (2025-2032).

Motor Lamination Market Regional Outlook

By region, the market is studied across North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Motor Lamination Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 56.99% of the global market in 2025, generating USD 12.18 billion in revenue, and is projected to reach USD 12.72 billion in 2026. The Asia Pacific region dominates the market and is also attributed to propelling the fastest-growing CAGR during the forecasted period of 2026-2034. Consumer attention to electric vehicles is swiftly growing in the Asia Pacific region, driven by increasing environmental awareness and the desire for cost-effective, low-maintenance vehicles. This demand is particularly strong in China, which is the largest EV market globally. As automakers respond to consumer preferences for sustainable vehicles, they require efficient electric motors, which, in turn, drive the demand for laminations. The rising adoption of EVs and hybrids in the region significantly contributes to the expanding motor lamination market. China is poised to acquire USD 4.69 billion in 2026.

The International Energy Agency stated that, in 2023, China represented almost 60% of all new electric car registrations globally. The proportion of electric vehicles in total car sales in China surpassed 35% in 2023, up from 29% in 2022, successfully meeting the country's 2025 national target of a 20% market share for New Energy Vehicles (NEVs) ahead of schedule.

India is estimated to be worth USD 0.72 billion in 2026, while Japan is predicted to be valued at USD 0.7 billion in the same year.

North America

North America contributed approximately USD 3.82 billion to the global market in 2025, accounting for 17.88% share, and is expected to reach USD 3.95 billion in 2026. Continuous innovation in motor technology, including the development of advanced laminations, is driving growth in the North American motor lamination market. These advancements focus on improving motor efficiency, reducing energy losses, and enhancing overall vehicle performance. Innovations such as use of high-grade steel and improved lamination design, which reduce eddy current losses and heat generation, are becoming essential in the production of electric motors. As automakers strive for higher-performing, more energy-efficient electric vehicles, the demand for cutting-edge laminations increases, contributing to market expansion. The U.S. market continues to expand, projected to reach a market value of USD 3.36 billion in 2026.

Europe

In 2025, the Europe market stood at USD 3.94 billion, representing 18.43% of global demand, and is projected to grow to USD 4.08 billion in 2026. The region held the second-largest market in 2024. Many European automakers, including giants such as Volkswagen, BMW, and Daimler, are increasingly focusing on electric vehicle development as part of their long-term strategies. The U.K. market continues to grow, estimated to reach a value of USD 0.62 billion in 2026. This transition toward electrification requires significant investments in electric motor technologies, particularly in motor components such as laminations that enhance motor efficiency. As Europe becomes a hub for electric vehicle production, the demand for motor laminations rises, driven by the need for cost-effective, high-performance motors that meet both the performance and sustainability goals of automakers.

In December 2024, BMW expanded its electric motor production to Austria, marking a key step in its transition to electric mobility. The Steyr facility aims to produce up to 600,000 electric motors annually by 2028. This move supports the company's shift to electric vehicles, with the sixth generation of motors now produced outside Germany. While the majority of BMW’s electric motors have been made in Dingolfing, Bavaria, this new production expansion signals a strategic effort to strengthen its electric vehicle portfolio and global market presence. Germany is poised to hold USD 0.8 billion in 2026, while France is expected to stand at USD 0.49 billion in 2025.

Rest of the World

In 2025, Rest of the World represented USD 1.43 billion, accounting for 6.70% of the worldwide market, and is projected to grow to USD 1.46 billion in 2026. The automotive industry in the Rest of the World region is undergoing significant modernization, with several countries investing in electric vehicle manufacturing and adopting advanced automotive technologies. As automakers modernize their production lines and shift toward more sustainable technologies, there is a rising demand for electric motors that are efficient and cost-effective. This shift encourages the use of advanced laminations, which improve motor efficiency and power density. As a result, the demand for laminations grows, helping the RoW automotive market stay competitive globally.

Competitive Landscape

Key Market Players

Companies Investing in R&D Fuels Compeitive Edge In the Market

The global motor lamination market is vastly competitive, with key players focusing on advancements in technology, cost efficiency, and strategic partnerships. Leading companies, including ArcelorMittal, Baosteel, JFE Steel, and POSCO, dominate the market by providing high-quality steel laminations essential for electric motors used in electric and hybrid vehicles. These players invest heavily in R&D to enhance lamination designs, improve motor efficiency, and reduce energy losses. Additionally, the market features regional players who focus on localized production to meet the specific needs of their respective automotive industries. As electric vehicle demand rises, competition intensifies around the supply of laminations, driving innovation in materials, manufacturing techniques, and cost-effective solutions to meet the growing demand for high-performance electric motors.

List of Key Companies Profiled In The Report

- ArcelorMittal (Luxembourg)

- POSCO (South Korea)

- JFE Steel Corporation (Japan)

- Baosteel Group (China)

- Nippon Steel Corporation (Japan)

- Thyssenkrupp Steel Europe AG (Germany)

- Tata Steel Ltd. (India)

- Thomson Lamination Co. Inc. (U.S.)

- Laser Technologies (U.S.)

- Precision Micro (U.K.)

- Tempel (U.S.)

- Lammotor (China)

- EuroGroup Lamination (Italy)

- Lake Air Companies Lamination Specialties Incorporated (U.S.)

- LCS Company (U.S.)

- Partzsch Elektromotoren E.K. (Germany)

- Pitti Laminations Ltd. (India)

- Polaris Laser Laminations LLC (U.S.)

Key Industry Developments

- January 2025: thyssenkrupp Steel announced the completion of key investments at its Bochum location, including the annealing and isolating line. This modern, energy-efficient facility produces electrical sheets as thin as 0.2 mm with consistent mechanical and magnetic properties, ideal for high-efficiency motors, especially for electric vehicles. The upstream rolling mill has been completed, and a new electrical steel inspection and finishing line, scheduled for 2026, will tailor the sheets to customer specifications.

- December 2024: Worthington Steel planned to acquire a 52% controlling stake in Italy-based Sitem Group through its subsidiary, Tempel Steel Company. With 50 years of experience, Sitem is a major European producer of laminations for electric motors for automotive and industrial uses. The deal, set to close in early 2025, includes acquiring shares, contributing Worthington's Nagold facility, and subscribing to reserved share capital increases. This acquisition strengthens Worthington's presence in Europe's growing EV market.

- July 2024: FIUKA expanded into the Electric Vehicle (EV) market by investing in cutting-edge technology. The company commissioned a Nidec Minster EV-350 high-speed press to stamp ultra-thin electrical laminations for EV motors. This press, known for its precision and high production speeds, enables FIUKA to meet growing EV demands.

- April 2024: Nippon Steel filed a patent for a non-oriented electrical steel sheet with a specialized chemical composition and a tensile strength of 550 MPa or more. The sheet's distinctive properties, verified through Auger electron spectroscopy, are designed to ensure superior performance in electrical applications.

- February 2024: ArcelorMittal initiated the construction of an advanced non-grain-oriented electrical steel (NOES) manufacturing facility in Alabama. The wholly owned facility will have the capacity to produce up to 150,000 metric tons of NOES annually, depending on the product mix. This facility will support a range of applications, including automotive and mobility, renewable energy production, and various industrial and commercial uses such as electric motors, generators, and specialized applications.

- August 2023: Vitesco Technologies, a global leader in advanced drive technologies and electrification solutions for sustainable mobility, entered into a strategic partnership with Baosteel, a prominent Chinese steel conglomerate. Together, the companies will collaborate on developing new materials using high-grade, non-oriented silicon steel. Their goal is to drive forward sustainable mobility, advance e-mobility technologies, and establish a model of shared value within the industry.

- April 2023: POSCO Group strengthened its position in the global eco-friendly vehicle market by excelling in cathode/anode materials and traction motor core businesses. POSCO MOBILITY SOLUTION invested significantly in enhancing traction motor core quality. It uses POSCO’s Hyper NO non-oriented electrical steel sheets and a proprietary lamination method to produce high-performance motor cores. The EM-Free lamination technology ensures efficiency by bonding steel plates, stacking them, and applying hardening and cooling processes for superior quality and performance.

- October 2021: Beckers introduced Beckry Core Core Plate Varnish (CPV) to support the e-mobility industry by improving electric motor efficiency and aiding the transition to a low-carbon society. This waterborne CPV enables thinner coatings for laminated cores, which is essential for compact, high-performance electric motors. It reduces power losses, enhances magnetic properties, and offers excellent stamping performance without damaging tools or generating dust. Available globally, Beckry Core is produced in Sweden and supported by Beckers’ local experts.

Investment Analysis and Opportunities

Rising Vehicle Demand and Technological Advancements Fuels Investments in the Market

The market offers significant investment opportunities, mainly driven by the rising demand for Electric Vehicles (EVs) and stringent emissions regulations. Investors are focusing on companies that innovate in motor efficiency and material technologies, such as advanced steel laminations that reduce energy loss and improve performance. As the shift toward electrification accelerates, opportunities lie in expanding production capabilities for laminations and establishing partnerships with EV manufacturers. Furthermore, growing demand in emerging markets such as China, India, and Latin America presents untapped potential. Investment in sustainable practices, such as recycling and eco-friendly materials, is also gaining traction. As EV adoption and automotive electrification continue to grow, the market presents robust prospects for long-term investments in both developed and developing regions.

Report Coverage

The global motor lamination market report analyzes the market in-depth. It highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, vehicle type, propulsion, motor application, manufacturing process, material, and motor type. Besides this, the market research report provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.14% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

By Propulsion

By Motor Application

By Manufacturing Process

By Material

By Motor Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market size was USD 22.22 billion in 2025 and is anticipated to record a valuation of USD 35.79 billion by 2034.

The CAGR of the global motor lamination market size is 6.14% over the forecasted period.

In 2026, the silicon steel segment led the market, holding the largest share.

The rising demand for electric vehicles is expected to propel the market growth.

Among the company profiles, ArcelorMittal, Baosteel, JFE Steel, and POSCO are the key players in the global market.

Asia Pacific dominated the global market with a share of 56.99% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us