Naval Weapon Container Market Size, Share & Industry Analysis, By Weapon Type (Anti-Ship Missiles, Land-Attack Cruise Missiles, Surface-to-Air Missiles, & Others), By Platform Integration (Surface Combatants, OPVs, Auxiliary Vessels, & Others), By Range Class (Short Range (<50 km), Medium Range (50–200 km), Long Range (200–1,000 km), & Extended Range (>1,000 km)), By Container Size (10 ft ISO, 20 ft ISO, 40 ft Heavy Module, & Custom Reinforced), By Application (Sea Denial Operations, Power Projection & Land Attack, & Others), By End User, and Regional Forecast, 2026-2034

Naval Weapon Container Market Size and Future Outlook

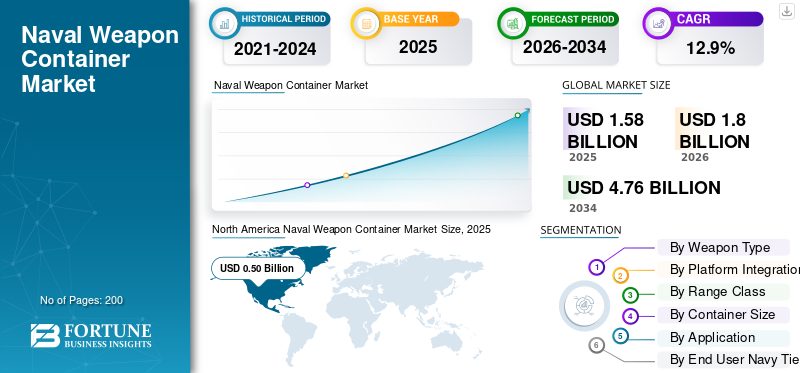

The global naval weapon container market size was valued at USD 1.58 billion in 2025. The market is projected to grow from USD 1.80 billion in 2026 to USD 4.76 billion by 2034, exhibiting a CAGR of 12.9% during the forecast period. North America dominated the naval weapon container market with a market share of 31.64% in 2025.

The market includes modular, containerized weapon systems designed for flexible deployment in military and coastal defense missions. These containerized weapons combine anti-ship missiles, automatic cannons, and combat systems into standardized modules for use on littoral combat ships and other platforms. The growing geopolitical tensions in North America, the Middle East, and Asia Pacific are prompting navies to improve defense capabilities with scalable maritime operations, better surveillance systems, and flexible defense systems. The rise of unmanned surface vessels is also increasing the demand for containerized weapon systems that can be quickly integrated into modern weapon designs.

Key players such as Lockheed Martin, MBDA, Kongsberg, RTX, Saab, Rafael, and companies from the U.S. and South Korea are developing containerized weapons and next-generation combat systems. They are improving anti-ship capabilities, updating automatic cannon modules, and enhancing defense systems to meet the evolving needs of maritime operations. In Asia Pacific, North America, and the Middle East, these advancements directly respond to geopolitical tensions while strengthening coastal defense and military readiness through modular containerized weapon systems.

Download Free sample to learn more about this report.

NAVAL WEAPON CONTAINER MARKET TRENDS

Modular Containerized Firepower to Accelerate Distributed Maritime Operation

A major trend in the global market is the shift toward modular, containerized weapon systems that support distributed maritime operations. Navies are moving away from fixed launch systems and using flexible containerized weapons that can be deployed on littoral combat ships, auxiliaries, and unmanned surface vessels. This strategy improves coastal defense and military readiness without requiring complete platform redesigns. As geopolitical tensions rise in North America, the Middle East, and Asia Pacific, modular combat systems are becoming crucial for improving defense capabilities. The ability to integrate anti-ship missiles, automatic cannon modules, surveillance systems, and layered defense into standardized containerized weapon systems allows navies to quickly scale maritime operations while keeping fleet flexibility.

- In April 2023, the U.S. Navy introduced the Mk 70 Payload Delivery System (PDS), a containerized launch system that can deploy Standard Missile-6 and Tomahawk missiles from a modular platform.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Geopolitical Tensions to Strengthen Demand for Rapidly Deployable Naval Firepower

The growing geopolitical tensions are driving the global naval weapon container market growth. Navies face pressure to quickly improve their defense capabilities without lengthy shipbuilding processes. Containerized weapon systems let military forces deploy anti-ship missiles, automatic cannon modules, and advanced defense systems on existing platforms such as littoral combat ships and support vessels. This flexibility improves coastal defense and enables scalable maritime operations, especially as unmanned surface vessel integration becomes more common. The ability to upgrade combat and surveillance systems with modular containerized weapons is increasingly important in high-risk maritime environments.

- In August 2022, the U.S. Navy confirmed its deployment of containerized missile systems, including the Mk 70 Payload Delivery System, in Europe as part of its distributed maritime operations strategy.

MARKET RESTRAINTS

Integration Complexity to Limit Rapid Adoption across Legacy Fleets

One major constraint in the global market is the technical difficulty of integrating containerized weapon systems into current combat systems. While these weapons provide flexibility, matching them with older weapon system structures, radar interfaces, surveillance systems, and fire-control networks can be expensive and time-consuming. Many older fleets used in coastal defense and military operations were not designed for modular combat systems, leading to structural and certification challenges. Integration with unmanned surface vessel platforms also requires secure data links and compatible defense systems, which adds another layer of complexity.

MARKET OPPORTUNITIES

Expansion of Unmanned Surface Vessel Programs to Create New Growth Avenues

A major opportunity in the global market comes from the rapid growth of unmanned surface vessel programs. As navies modernize maritime operations, they seek lightweight, modular containerized weapon systems. These systems can be used on unmanned platforms without needing to redesign hull structures. This boosts the demand for scalable anti-ship modules, compact automatic cannon systems, and defense systems that work well with combat and surveillance systems. Rising geopolitical tensions in North America, Asia Pacific, and the Middle East are speeding up investments in unmanned surface vessel fleets.

- In May 2024, the U.S. Navy announced its ongoing investment in its Large and Medium Unmanned Surface Vessel programs. This is part of its budget request and shows the integration of modular weapon system payloads to improve distributed maritime operations.

MARKET CHALLENGES

Export Controls and Regulatory Barriers to Limit Cross-Border Deployment

A major challenge in the global market is navigating export controls and defense trade rules. Containerized weapon systems that include anti-ship missiles, automatic cannon modules, and combat systems often fall under strict arms transfer laws. This makes sales difficult across North America, the Middle East, and Asia Pacific. Coastal defense upgrades are needed, but the licensing processes take a long time. For military buyers who want to quickly improve defense capabilities and readiness for maritime operations, regulatory approvals can slow down the deployment of containerized weapons and related surveillance and defense systems.

- In September 2023, the U.S. Department of State approved several Foreign Military Sales cases involving naval missile systems under the Arms Export Control Act. This was announced by the U.S. Defense Security Cooperation Agency.

Impact of Russia Ukraine War

Russia-Ukraine War to Accelerate Naval Modernization and Containerized Strike Concepts

The Russia-Ukraine war has drawn attention to the need for quick force adaptation, especially in coastal defense and distributed maritime operations. The conflict demonstrated the value of mobile anti-ship systems, layered defense setups, and strong surveillance networks in contested areas. As a result, navies in North America, the Middle East, and Asia Pacific are reevaluating their defense capabilities and investing in flexible containerized weapon systems. These systems can be deployed on littoral combat ships and support platforms. The war has also increased interest in using unmanned surface vessels and modular combat systems. Militaries seek weapon options that can be moved quickly during times of high geopolitical tension.

- In April 2022, Ukrainian authorities and international defense agencies widely reported Ukraine’s successful use of the Neptune anti-ship missile against the Russian cruiser Moskva. This event highlighted the effectiveness of mobile coastal defense and anti-ship capabilities in modern warfare.

Segmentation Analysis

By Weapon Type

Anti-Ship Missiles Led the Market with Mounting Need for Effective Anti-ship Strike Capabilities

In terms of weapon type, the market is categorized into anti-ship missiles, land-attack cruise missiles, surface-to-air missiles, loitering munitions, and others.

The anti-ship missiles segment dominated the market in 2025. Sea control and sea denial are important for modern maritime operations. As geopolitical tensions rise in North America, the Middle East, and Asia Pacific, navies are prioritizing effective anti-ship strike capabilities. This focus allows them to strengthen defense without expanding fleet size. Containerized weapon systems facilitate easier deployment of anti-ship missiles. These systems can be used on littoral combat ships, coastal defense units, and even unmanned surface vessels. Unlike other weapon types, anti-ship missiles deliver an immediate strategic effect. This makes anti-ship missiles the top choice for quick integration into combat systems and faster enhancement of maritime forces.

In January 2024, the U.S. Department of Defense announced a contract with Lockheed Martin for producing Long Range Anti-Ship Missiles (LRASM). This contract, revealed by the U.S. DoD, highlights ongoing investment in effective anti-ship missile systems as a key element in modernizing naval combat capabilities in response to evolving global security challenges.

The loitering munitions segment is expected to show the fastest growth at a CAGR of 20.0% over the forecast period.

By Platform Integration

Surface Combatants Segment Leads due to Significant Role in Coastal Defense Strategies

On the basis of platform integration, the market is classified into surface combatants, OPVs, auxiliary vessels, commercial conversions, and Unmanned Surface Vessels (USVs).

The surface combatants segment holds the largest market share. Major navies still rely on frigates, destroyers, and corvettes as the main platforms for high-value weapon systems. These vessels are designed for combat systems, surveillance systems, and layered defense systems, making them ideal for containerized weapon systems. While the use of unmanned surface vessels is increasing, surface combatants remain essential to military sea power and coastal defense strategy. This ensures that they continue to perform well in platform integration.

The Unmanned Surface Vessels (USVs) segment is expected to show the fastest growth at a CAGR of 22.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Range Class

Long-Range (200–1,000 km) Systems Dominate Due to Expanding Stand-Off Strike Doctrine

Based on range class, the market is segmented into short range (<50 km), medium range (50–200 km), long range (200–1,000 km), and extended range (>1,000 km).

The long range (200–1,000 km) segment holds the largest global naval weapon container market share. Navies are focusing more on stand-off strike capability. Modern maritime operations require the ability to neutralize threats far beyond coastal areas. This need is particularly urgent amid rising geopolitical tensions in North America, Europe, and Asia Pacific. Long-range anti-ship and land-attack weapon systems improve defense capabilities while minimizing the exposure of platforms. Containerized weapon systems make it easier to integrate long-range missiles into surface combatants and support distributed operations. This strategy enhances layered defense systems and deterrence.

The extended range (>1,000 km) segment is second fastest growing segment, expanding at a CAGR of 14.8% across the forecast period.

By Container Size

Standardization and Deployment Flexibility to Drive the Dominance of 20 ft ISO Containers Segment

Based on container size, the market is segmented into 10 ft ISO, 20 ft ISO, 40 ft heavy module, and custom reinforced.

The 20 ft ISO segment dominates the global market. It provides the best balance between payload capacity and platform compatibility. This standardized size allows containerized weapon systems to be used on surface combatants, auxiliary vessels, and coastal defense units without major structural changes. Navies in North America, Europe, and Asia Pacific choose 20 ft ISO modules for adding anti-ship missiles, automatic cannon systems, and other defense systems into their existing combat setups. Its familiarity in maritime operations also lowers integration risk and supports scalable defense capabilities.

The 40 ft heavy module segment is the fastest growing segment, surging at a CAGR of 16.4% during the forecast period.

By Application

Sea Denial Operations Lead the Market due to Significance of Controlling Strategic Maritime Chokepoints

Based on application, the market is segmented into sea denial operations, power projection & land attack, fleet air defense extension, unmanned & distributed maritime operations, and others.

The sea denial operations dominates the market as controlling access to important sea lanes is a major priority for military planners. Navies in North America, Europe, the Middle East, and Asia Pacific are investing into containerized weapon systems. These systems improve anti-ship capabilities and layered defense, which helps deter hostile naval movements. Containerized weapons enable quick deployment of coastal defense and ship-based strike assets without needing to fully expand fleets. As geopolitical tensions continue, sea denial plays a key role in maritime operations strategy, especially for countries aiming to improve their defense capabilities in contested waters.

The unmanned & distributed maritime operations segment is the fastest growing segment, surging at a CAGR of 17.3% over the forecast period.

By End User Navy Tier

Tier 1 Blue-Water Navies Segment Dominates the Market Due to Global Power Projection Mandates

Based on end user navy tier, the market is segmented into tier 1 blue-water navies, tier 2 regional powers, tier 3 coastal defense navies, and paramilitary / coast guard.

The tier 1 blue-water navies segment leads the global market as they operate in various areas and need flexible, high-quality combat systems. These navies emphasize long-range anti-ship capability, layered defense systems, and advanced surveillance systems to keep maritime operations ongoing. Containerized weapon systems provide the flexibility to improve defense capability without delaying fleet readiness. This includes integrating with unmanned surface vessel programs to support distributed maritime operations.

The tier 2 regional powers segment is expected to show the second-fastest growth at a CAGR of 11.7% across the forecast period.

Naval Weapon Container Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and Rest of the World (Africa and Latin America).

North America

North America Naval Weapon Container Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads the market mainly due to the extensive naval modernization efforts of the U.S. and its focus on distributed maritime operations. The region continues to invest heavily in combat systems, anti-ship missile capabilities, and layered defense systems to improve its defense abilities. Containerized weapon systems align well with the U.S. Navy's shift toward modular weapon deployment on surface combatants and new unmanned surface vessel platforms. Increased geopolitical tensions and ongoing military readiness needs further strengthen North America's position in scalable maritime operations and the integration of next-generation surveillance systems.

U.S. Naval Weapon Container Market

Based on North America market’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.46 billion in 2025, expanding at a CAGR of 11.1% over the forecast period.

Europe

The Europe market size reached the second largest share in 2025 and is projected to depict a CAGR of 14.2% during the forecast period. The regional market is experiencing steady growth as governments are boosting defense capabilities in response to rising geopolitical tensions. Countries such as the U.K., France, Germany, Italy, and Russia are updating surface combatants and enhancing combat systems with longer-range anti-ship and land-attack weapon systems. There is an increasing focus on modular containerized weapon systems that can improve maritime operations without major ship redesigns. NATO interoperability standards are also encouraging the use of flexible defense systems and better surveillance systems across European fleets.

U.K. Naval Weapon Container Market

The U.K. market reached approximately USD 0.07 billion in 2025, equivalent to around 16.18% of Europe industry revenues.

Germany Naval Weapon Container Market

The Germany market size touched around USD 0.06 billion in 2025, representing roughly 12.63% of Europe market revenues.

Asia Pacific

The Asia Pacific market size is the third largest in the global market and is anticipated to be the fastest growing region, surging at a CAGR of 15.1% during the forecast period. The market is expanding owing to naval expansion programs in China, India, Japan, South Korea, and Australia. The rising maritime tensions are increasing investment in anti-ship capabilities, integrating long-range weapon systems, and deploying unmanned surface vessels. Many navies in the region are enhancing coastal defense and expanding blue-water operations. Containerized weapon systems offer flexibility for distributed maritime operations and allow for quicker upgrades of combat systems on both large surface ships and smaller patrol vessels.

China Naval Weapon Container Market

The China market is projected to be one of the largest in the Asia Pacific. The 2025 revenues touched around USD 0.17 billion, representing roughly 40.52% of Asia Pacific sales.

India Naval Weapon Container Market

In 2025, the India market reached a value of around USD 0.07 billion, accounting for roughly 17.63% of Asia Pacific revenues.

Middle East

The Middle East market is anticipated to be the third fastest growing segment, growing at a CAGR of 12.6% during the forecast period. The market is shaped by the need for chokepoint security and coastal defense. Countries such as Saudi Arabia, Turkey, the UAE, and Israel are investing in anti-ship systems and layered defense systems to protect maritime operations in sensitive waters. Modular containerized weapons are attractive as they quickly boost defense capabilities and can be deployed on patrol vessels and surface combatants. The region is also slowly exploring the use of unmanned surface vessels to support distributed maritime operations.

Saudi Arabia Naval Weapon Container Market

The Saudi Arabia market is projected to be one of the second largest in the Middle East. The 2025 revenues in the country touched around USD 0.04 billion, representing roughly 24.96% of the Middle East sales.

United Arab Emirates Naval Weapon Container Market

The United Arab Emirates market reached a value of around USD 0.02 billion in 2025, accounting for roughly 16.28% of the Middle East revenues.

Rest of the World

The rest of the world (Africa and Latin America) region is comparatively smaller in share but is poised to grow at a CAGR of 2.7% over the forecast period. In Africa and Latin America, modernization is progressing slowly but steadily. Many navies are concentrating on offshore patrol vessels and coastal defense platforms. They are adding containerized weapon systems to improve maritime security and surveillance. While large-scale blue-water expansion is limited, regional forces are upgrading combat systems and anti-ship capabilities to enhance defense readiness. Gradually, using modular weapon system concepts is allowing more flexible maritime operations within fleets that have tight budgets.

Latin America Naval Weapon Container Market

The Latin America market reached a value of around USD 0.04 million in 2025, accounting for roughly 44.77% of rest of the world revenues.

Africa Naval Weapon Container Market

The Africa market size reached a value of around USD 0.05 billion in 2025 and is expected to reach USD 0.09 billion in 2034, representing roughly 55.23% of rest of the world sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Enhancing Anti-ship Capabilities to Secure a Strong Edge

The global naval weapon container market is influenced by major defense contractors and naval system integrators that combine missile expertise with modern combat systems. Companies such as Lockheed Martin, MBDA, RTX (Raytheon), Kongsberg, Saab, Naval Group, Rafael, and Roketsan, along with top shipbuilders in the U.S. and South Korea, are essential to market progress. These players are improving anti-ship capabilities, strengthening layered defense systems, and integrating containerized weapon systems into surface combatants and new unmanned surface vessel platforms. Their ability to link weapon system development with distributed maritime operations gives them a strong edge in competition.

The focus is shifting toward modularity, interoperability, and quick deployment. Leading firms are incorporating advanced surveillance systems and digital fire-control upgrades into scalable containerized weapons to enhance defense capabilities without completely redesigning the platform. As geopolitical tensions remain high in North America, Europe, Asia Pacific, and the Middle East, the demand for flexible coastal defense and blue-water combat systems continues to grow. Companies that can offer standardized, mission-adaptable containerized weapon systems while ensuring compatibility with evolving naval defense systems are positioning themselves as long-term market leaders.

LIST OF KEY NAVAL WEAPON CONTAINER COMPANIES PROFILED

- BAE Systems (U.K.)

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (Raytheon Technologies) (U.S.)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- Naval Group (France)

- Thales Group (France)

- MBDA (France)

- Saab AB (Sweden)

- Kongsberg Gruppen (Norway)

- Leonardo S.p.A. (Italy)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Roketsan A.Ş. (Turkey)

- Hanwha Aerospace (South Korea)

- Hyundai Heavy Industries (South Korea)

KEY INDUSTRY DEVELOPMENTS

- March 2024: The U.S. Department of Defense's FY2025 Budget Request stressed ongoing funding for Large and Medium Unmanned Surface Vessel (LUSV/MUSV) programs. The documents pointed out the need for modular payload and weapon system integration. This increased focus shows the demand for scalable containerized weapon systems.

- January 2024: The U.S. Department of Defense granted Lockheed Martin a contract modification for ongoing production of the Long Range Anti-Ship Missile (LRASM). This award supports the U.S. Navy and allied maritime strike abilities.

- December 2023: MBDA secured new contracts to produce Exocet anti-ship missiles for European naval customers. The Exocet remains a key maritime strike system used in various combat systems across NATO fleets.

- October 2023: The U.S. Navy continued contract activity for the Constellation-class (FFG-62) frigate program. The focus was on combat systems, missile integration, and modernizing the design.

- July 2023: Kongsberg Defence & Aerospace announced new production contracts for the Naval Strike Missile (NSM) to support U.S. Navy and allied deployments. The NSM is an important anti-ship weapon system that is widely used on surface vessels and coastal defense units.

- April 2023: The U.S. Navy publicly introduced the Mk 70 Payload Delivery System (PDS) at Sea-Air-Space 2023. The 20 ft containerized launch system showed it can deploy Standard Missile-6 and Tomahawk missiles. This event highlighted how well the weapon system integrates with distributed maritime operations concepts.

- June 2022: Saab received an order for the RBS15 anti-ship missile system to integrate with naval platforms. The system improves coastal defense and maritime operations for European customers.

REPORT COVERAGE

The global naval weapon container market analysis provides an in-depth study of the market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.9% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By Weapon Type

|

|

By Platform Integration

|

|

|

By Range Class

|

|

|

By Container Size

|

|

|

By Application

|

|

|

By End User Navy Tier

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.58 billion in 2025 and is projected to reach USD 4.76 billion by 2034.

In 2025, the North America market value stood at USD 0.50 billion.

The market is expected to exhibit a CAGR of 12.9% during the forecast period of 2026-2034.

The anti-ship missiles segment led the market by weapon type in 2025.

Rising geopolitical tensions strengthening the demand for rapidly deployable naval firepower is a key factor driving the global market.

Lockheed Martin, RTX (Raytheon), Northrop Grumman, General Dynamics, MBDA, Naval Group, Thales, Saab, Kongsberg, Leonardo, Rafael Advanced Defense Systems, Roketsan, Hanwha Aerospace, and Hyundai Heavy Industries, among others, are the top companies in the market.

North America dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us