Over-The-Horizon Radar Market Size, Share & Industry Analysis, By Sensing Mode (Skywave OTHR, Surface-Wave, Oceanographic HF Radar, and Others), By Application (Air Surveillance, Border and Coastal security, Homeland Defense, and Others), By Instrumented Range, By RF Band, By Waveform, By Deployment Format (Fixed Strategic Installation, Expeditionary Deployment, and Manned Site), By Procurement Model (New-Build Program, Mid-Life Upgrade, and Subsystem Retrofit), By End User (Air Force, Navy, Joint Force, Missile Defense Organization,and Others), and Regional Forecast 2026-2034

Over-The-Horizon Radar Market Size and Future Outlook

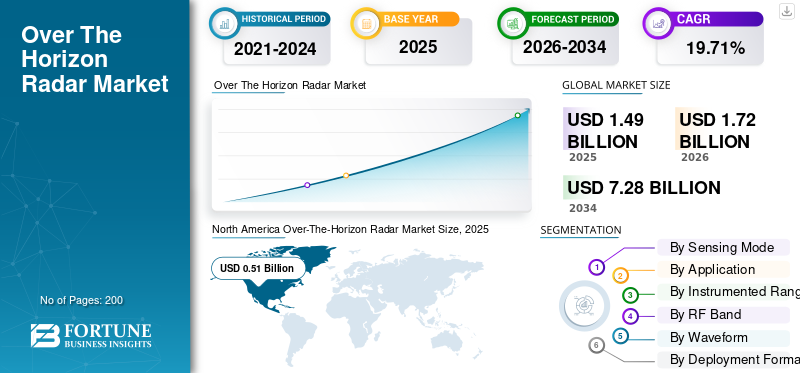

The global over-the-horizon radar market size was valued at USD 1.49 billion in 2025. The market is projected to grow from USD 1.72 billion in 2026 to USD 7.28 billion by 2034, exhibiting a CAGR of 19.71% during the forecast period. North America dominated the over the horizon radar market with a market share of 34.22% in 2025.

The Over-The-Horizon Radar (OTHR) market covers long-range surveillance systems that can detect aircraft, missiles, and maritime targets far beyond normal line-of-sight. This is done by using high-frequency waves refracted from the ionosphere or other extended-range sensing approaches. It is a defense-led, program-driven market built around early warning, border, coastal surveillance, maritime domain awareness and missile-threat detection rather than high-volume commercial demand. Australia’s JORN operates at roughly 1,000-3,000 km, while Canada and the U.S. are actively pushing new OTHR layers under NORAD modernization, which shows why this segment is gaining strategic weight.

The global market growth drivers include expanding defense budgets for rising cruise-missile and long-range strike threats. They also include the need to monitor Arctic and maritime approaches, and the push for earlier warning against low-altitude or hard-to-detect multi-mission targets. The market is also being driven by Department of Defense modernization budgets and by demand for wider-area sensing that complements satellites, conventional air-defense radars, and integrated command networks. In simple terms, the government wants more reaction time, more territory covered, and fewer blind spots.

The prominent players in the industry include Raytheon (RTX), BAE Systems, Lockheed Martin Australia, Leonardo, and Reutech Radar Systems. The major players are pushing next-generation OTHR with higher sensitivity and 2D-array designs. They are also expanding through U.S. Navy integration work on relocatable OTH radar systems, JORN upgrades, sustainment programs, supplier-partnership expansion, JORN Phase 6 systems integration, and wider multi-domain defense networking.

Download Free sample to learn more about this report.

Over-The-Horizon Radar Market Trends

Shift from Legacy HF Radars to Software-Defined, Upgradeable, and Model-Driven Systems is a Key Market Trend

The strongest trend is a move toward more flexible and software-led OTHR systems. Australia’s JORN modernization includes an open software architecture and a modern user interface, while Raytheon is marketing AI/ML decision aids, adaptive signal processing, and digital beamforming to improve operator support and detection performance. At the same time, NASA’s CCMC keeps updating ionospheric modeling tools such as PHaRLAP and IRI, which shows that software models and propagation prediction models are becoming central to radar performance planning, not just back-end research support.

For instance, in July 2025, Australia stated that the collaboration with Canada would support OTHR R&D, development, manufacturing and commissioning planning.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Early-Warning Demand Rises as Countries Seek Faster Response to Missile, Arctic, And Maritime Threats

OTHR demand is being driven by a basic military need as traditional line-of-sight radars do not monitor far enough ahead for modern low-altitude and long-range threats. Canada’s NORAD modernization work directly links OTHR to stronger warning against advanced cruise missiles and faster long-range detection of threats approaching North America. On the other hand, Raytheon Technologies is explicitly positioning next-generation OTHR for low-altitude cruise missile detection. In simple terms, this technology is evolving from a niche surveillance option into a strategic layer of homeland and continental defense, further resulting in the over-the-horizon radar market growth.

For instance, in July 2025, Canada announced the first transmit and receive sites for its Arctic OTHR program, with initial operational capability targeted for the end of 2029 and initial site work expected in winter 2026.

MARKET RESTRAINTS

Market is Constrained by High Costs, Large Land Needs, Long Deployment Times, and Siting Challenges

OTHR is not an easy short-range and long-range radar program to buy or install. Canada’s public A-OTHR material shows that the full system will ultimately need four antenna farms, while the remaining future sites together will require about 1,500 hectares. Further, it must meet strict conditions on latitude, parcel size, orientation, radio-frequency environment, terrain, power access, and surrounding land use. That sharply narrows the customer base, as many countries may want long-range warning but only a few can fund, site, and sustain such a system over many years.

MARKET OPPORTUNITIES

Exportable Sovereign OTHR and Arctic-Ready Variants are Expanding Growth Beyond Domestic Radar Replacement

The biggest commercial opportunity is not just selling a radar set, but exporting a full sovereign capability package. Canada chose a radar technology partnership with Australia, as it judged that route to be the best way to strengthen Northern domain awareness quickly, and the arrangement is designed to build Canadian expertise, domestic industrial capacity, and local jobs. That is important, as future OTHR deals are likely to reward suppliers that can transfer know-how, support local manufacturing, and prove interoperability with allied defense networks, not just ship hardware.

For instance, in April 2026, Continental Electronics Corp. received a not-to-exceed USD 234.52 million contract from the U.S. Air Force Life Cycle Management Center for the Homeland Defense Over-the-Horizon Radar transmit subsystem. Further, covering specialized transmitter capability for the U.S. OTHR program.

MARKET CHALLENGES

Limited Market Performance Due to Ionospheric Instability, Polar Effects, Clutter, and Heavy Processing Demands

The biggest technical challenge is that OTHR relies on the ionosphere, and the ionosphere does not behave the same way all the time. NOAA says changes in ionospheric density and structure can modify HF transmission paths and even block HF signals completely, while Canada’s NORAD R&D material states that polar regions can produce false or inaccurate radiolocation readings due to auroral effects. NASA also notes that ionospheric density changes with solar radiation, solar storms and time conditions. In simple business language, this means OTHR remains a performance-management problem as much as a hardware problem.

In March 2026, NASA’s CCMC refreshed PHaRLAP 4.7 for 2D and 3D HF ray tracing. Further, underlining that propagation modeling is still an active requirement for this market. However, NOAA also showed minor HF degradation conditions on April 3, 2026.

SEGMENTATION ANALYSIS

By Sensing Mode

Layered/Mixed Networks Segment Grow Fastest Due to Rising Customers Demand for Broader Coverage, Fewer Blind Spots, and Better Sensor Fusion

The global market by sensing mode is divided into skywave OTHR, surface-wave OTHR / HFSWR, oceanographic HF radar, and layered/mixed networks.

Layered / mixed networks is estimated to be the fastest-growing segment with a highest CAGR of 20.74% during the forecast period. This growth comes from the market shift toward combining skywave, surface-wave, coastal radar, and command-network inputs into one operating picture. Buyers increasingly prefer a multi-layer architecture as it improves resilience, target confirmation, and low-altitude detection support. The result is faster growth; as new programs are being designed as integrated networks rather than single-radar installations.

The skywave OTHR segment accounted for the largest market share of 36.60% in 2025 and is estimated to grow at a CAGR of 20.22% during the forecast period.

By Application

Strategic Early Warning Segment Grows Fastest Due to Rising Missile and Long-Range Threat Concerns, Driving Countries to Buy More Reaction Time

The global market by application is divided into strategic early warning, air surveillance, maritime domain awareness, border and coastal security, homeland defense, air and missile defense cueing, search and rescue support, disaster relief support, and others.

Strategic early warning is estimated to be the fastest-growing segment with a highest CAGR of 21.37% during the forecast period. The segment is accelerating as militaries want earlier detection of cruise or ballistic missiles, high-speed threats, and hostile approach patterns before they reach defended zones. OTHR is increasingly being linked to air-defense and homeland-defense networks, which raises its value in strategic warning roles. In simple terms, the market is growing fastest where the radar directly improves decision time for national command authorities.

The maritime domain segment accounted for the largest market share of 36.60% in 2025 and is estimated to grow at a CAGR of 20.22% during the forecast period.

By Instrumented Range

500–1,000 km Segment Grows Fastest as More Countries Increase Adoption for Regional Defense, Coastal Surveillance, and Chokepoint Monitoring

The global market by instrumented range is divided into 0-100 km, 100-200 km, 200-300 km, 300-500 km, 500-1,000 km, 1,000-3,000 km, and above 3,000 km.

500–1,000 km is estimated to be the fastest-growing segment with a highest CAGR of 21.51% during the forecast period of 2026-2034. This segment is expanding quickly as it supports regional missions without the full infrastructure burden of the longest-range systems. It is attractive for coastal states, island chains, and medium-scale defense programs that need wide-area surveillance but want faster implementation. That makes it the most scalable growth pocket in the range structure.

The 1,000-3,000 km segment accounted for the largest market share of 33.07% in 2025 and estimated to grow at a CAGR of 20.13% during the forecast period.

By RF Band

Seasonally Adaptive Frequency Plans Segment Grows Faster Due to Increasing Adoption for Smarter Planning Tools for Seasonal and Environmental Behavior

The global market by RF band is divided into single-band, multi-band, frequency-agile, site-optimized frequency plans, and seasonally adaptive frequency plans.

Seasonally adaptive frequency plans are estimated to be the fastest-growing segment with a highest CAGR of 20.53% during the forecast period. Their growth is driven by the increasing use of smarter planning tools that adjust frequencies based on seasonal and environmental behavior. This improves radar efficiency without requiring a full platform replacement, which makes adoption easier and commercially attractive. In effect, it is a high-value upgrade path for operators that want better performance from existing and new OTHR networks.

The multi-band segment accounted for the largest market share of 24.94% in 2025 and is estimated to grow at a CAGR of 19.66% during the forecast period.

By Waveform

Pulsed-Doppler HF Segment Leads Due to Better Target Discrimination and Clutter Rejection, Making It Most Commercially Useful Waveform

The global market by waveform is divided into pulsed HF, pulse-doppler HF, FMCW HF, pulsed-FMCW HF, and others.

Pulse-Doppler HF accounted for the largest market share of 26.47% in 2025 and is estimated to be the fastest-growing segment at a CAGR of 20.59% during the forecast period. It holds this position as it offers a stronger balance between detection, tracking, and movement discrimination, which is critical in both air and maritime surveillance. It also performs better in separating real targets from clutter, which improves operator confidence and system usefulness. In market terms, buyers are choosing the waveform that delivers clearer operational output, so this segment leads on both size and growth.

Pulsed HF is estimated to be the second-dominating segment, with a market share of 23.49% in 2025, and is estimated to grow at a CAGR of 20.41% during the forecast period.

By Deployment Format

Fixed Coastal Installation Segment Grows Fastest Due to Faster Expansion of Maritime Security Demand Compared to Inland Surveillance Missions

The global market by deployment format is divided into fixed strategic installation, fixed coastal installation, fixed arctic / remote installation, transportable HFSWR, expeditionary deployment, and manned site.

Fixed coastal installation is estimated to be the fastest-growing segment with a highest CAGR of 20.36% during the forecast period. Such growth is being driven by rising concern around coastal monitoring, shipping routes, offshore assets, and exclusive economic zones. Coastal installations are also easier to justify in budget terms as they directly support everyday security missions, not only wartime use. That makes them a faster-expanding deployment choice, especially for countries focused on maritime surveillance.

Fixed strategic installation segment accounted for the largest market share of 27.15% in 2025 and is estimated to grow at a CAGR of 20.18% during the forecast period.

By Procurement Model

New-Build Programs Lead Due to Increasing Establishment of First-Generation OTHR Capacity with Modern Architecture from Day One

The global market by procurement model is divided into new-build program, mid-life upgrade, life-extension / sustainment, and subsystem retrofit.

The new-build program accounted for the largest market share of 39.25% in 2025 and is estimated to be the fastest growing segment at a CAGR of 20.70% during the forecast period. The market is still being shaped more by fresh installations than by simple upgrades. Many buyers are entering OTHR through full greenfield programs so they can adopt newer processing, networking, and site design standards from the start. In commercial terms, new-build contracts are larger, more strategic, and more radar technology-rich, which is why this segment leads on both current size and future growth.

The life-extension/sustainment segment accounted for the second-largest market share of 24.19% in 2025 and is estimated to grow at a CAGR of 18.00% during the forecast period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Joint Force/Strategic Command Segment Leads Due to High Value of OTHR Data Feeds in Central Multi-Domain Decision Layers

The global market by end user is divided into air force, navy, joint force / strategic command, missile defense organization, coast guard, and border security.

Joint force / strategic command accounted for the largest market share of 26.11% in 2025 and is estimated to be the fastest-growing segment at a CAGR of 20.53% during the forecast period. It leads as OTHR is most valuable when it supports theatre-level awareness, cross-service coordination, and strategic warning rather than only one branch’s local mission. These command structures can justify larger budgets as the radar supports air, naval, missile-defense, and homeland-defense decisions at the same time. That broader mission value is the main reason this end-user group stays ahead in both revenue and growth.

The navy segment accounted for the second-largest market share of 19.71% in 2025 and is estimated to grow at a CAGR of 20.33% during the forecast period.

Over-The-Horizon Radar Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Over-The-Horizon Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest over-the-horizon radar market share in 2025, valued at USD 0.51 billion, and will also maintain the leading share in 2026, with USD 0.59 billion. Growth is fueled by high defense spending, modernization of surveillance systems, rising geopolitical tensions, and the need for advanced long-range early warning capabilities to detect emerging threats beyond traditional line-of-sight radar systems.

U.S. Over-The-Horizon Radar Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 0.40 billion in 2025 and is estimated to record a CAGR of 18.79% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 0.42 billion in 2025 and secured the position of the second-largest region in the market. The Asia Pacific market is experiencing rapid growth, driven by escalating regional geopolitical tensions, rising defense budgets, and the need for enhanced maritime/airspace surveillance. Key nations such as China, India, Japan, and South Korea are leading adoption, driven by the demand for long-range, early-warning detection.

China Over-The-Horizon Radar Market

The China market size in 2025 was valued at USD 0.10 billion and is estimated to grow at a rate of 21.05% during the forecast period.

India Over-The-Horizon Radar Market

The Indian market size in 2025 was valued at USD 0.06 billion and is estimated to grow at a rate of 23.41% during the forecast period.

Japan Over-The-Horizon Radar Market

The Japan market size in 2025 was valued at USD 0.05 billion and is estimated to grow at a rate of 22.62% during the forecast period.

Europe

Europe is projected to grow at the highest CAGR of 21.27% during the forecast period. In 2025, the market value stood at USD 0.40 billion. The European market is experiencing robust growth, driven by intensified regional security concerns, rising defense budgets, and modernization efforts. Key drivers include the need for early warning defense systems against long-range threats, border surveillance, and maritime security, with Germany, France, and the U.K. leading adoption.

U.K. Over-The-Horizon Radar Market

The U.K. market size in 2025 was valued at USD 0.07 billion and is estimated to grow at a rate of 19.78% during the forecast period.

Germany Over-The-Horizon Radar Market

The Germany market size in 2025 was valued at USD 0.06 billion and is estimated to grow at a rate of 18.33% during the forecast period.

Northern Europe Over-The-Horizon Radar Market

The Northern Europe market size in 2025 was valued at USD 0.08 billion and is estimated to grow at a rate of 24.08% during the forecast period.

Middle East & Africa and Latin America

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market was valued at USD 0.06 billion in 2025. The region’s growth is more focused on maritime surveillance, EEZ protection, illegal fishing control, and national sovereignty, rather than large-scale missile-defense early warning. In the Latin America region, Brazil represents the strongest demand driver. The Middle East & Africa market was valued at USD 0.10 billion in 2025. The region is anticipated to witness stronger growth in the market due to its direct need for long-range early warning, maritime surveillance, and integrated air/missile defense.

Gulf Countries Over-The-Horizon Radar Market

The Gulf Countries market size in 2025 was valued at USD 0.02 billion and is estimated to grow at a rate of 17.86% during the forecast period.

Brazil Over-The-Horizon Radar Market

The Brazil market size in 2025 was valued at USD 0.02 billion and is estimated to grow at a rate of 12.82% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Growth Is Driven by Upgrades, Partnerships, and Software Gains, Concentrating the Market Among a Few Proven Players

The OTHR market is not highly fragmented. It is led by a small number of companies with active programs, long-standing defense relationships, and experience in handling highly complex HF radar networks. BAE Systems Australia holds the strongest operational position, as it leads the JORN upgrade program, which remains the world’s best-known deployed OTHR system. Additionally, the Australia-Canada OTHR partnership has increased the export value of that ecosystem. Lockheed Martin Australia continues to play an important role through sustainment engineering, maintenance, facilities support, and enhancement work on Australian OTHR assets. On the other hand, Daronmont strengthens the competitive base through subsystem delivery and specialist HF radar integration.

LIST OF KEY OVER-THE-HORIZON RADAR COMPANIES PROFILED

- RTX Corporation (U.S.)

- BAE Systems Plc (U.K.)

- Maerospace Corporation (Canada)

- IACIT Soluções Tecnológicas S.A. (Brazil)

- Northern Radar Inc. (Canada)

- CODAR Ocean Sensors, Ltd. (Brazil)

- W R Systems, Ltd. (U.S.)

- Lencom Antennas Pty. Ltd. (Australia)

- Seaview Sensing Ltd (U.K.)

- SRI International (U.S.)

- Thales Group (Germany)

- Lockheed Martin Corporation (U.S.)

- Elta Systems (Israel)

- Terma A/S (Denmark)

- Rohde & Schwarz (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Raytheon received a USD 40.25 million cost-plus-fixed-fee contract for operations and maintenance support for the Relocatable Over-the-Horizon Radar (ROTHR) at the Forces Surveillance Support Center in Chesapeake, Virginia. With option years, the total potential value rises to about USD 212.12 million, making this one of the clearest recent OTHR sustainment awards.

- February 2026: MAEROSPACE Corporation received a contract from the Canadian Coast Guard for High-Frequency Surface Wave Radar data services, supporting maritime-domain surveillance through HFSWR-derived operational data

- April 2025: Brazil’s airspace-control authorities formally signed a contract with IACIT for the development and implementation of the OTH 0200 Skywave radar system. This is a real program award and one of the most important new sovereign OTHR contracts disclosed in Latin America.

- March 2025: Inuvialuit Frontec Services (ATCO Frontec + Inuvialuit Development Corporation), Government of Canada awarded a two-year USD 48.4 million contract to design, build, install, and operate a Polar OTHR system in the Northwest Territories. ATCO also said the contract commenced on March 28, 2025, with options for additional years.

- February 2025: Ventia announced it had been awarded a contract by BAE Systems Australia to deliver a new chiller plant system for the Jindalee Operational Radar Network (JORN) upgrade. It is not the full radar prime contract, but it is a direct industrial subcontract supporting a live OTHR modernization program.

REPORT COVERAGE

The global over-the-horizon radar market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key radar industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.71% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Sensing Mode

By Application

By Instrumented Range

By RF Band

By Waveform

By Deployment Format

By Procurement Model

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.49 billion in 2025 and is projected to reach USD 7.28 billion by 2034.

In 2025, the market value stood at USD 0.40 billion.

The market is expected to exhibit a CAGR of 19.71% during the forecast period.

The strategic early warning segment is expected to hold the highest CAGR over the forecast period.

Early-warning demand is rising as countries seek faster response to missile, arctic, and maritime threats.

Raytheon Technologies Corporation (RTX), BAE Systems, Lockheed Martin Australia, Leonardo, Reutech Radar Systems and so on are the top key players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us