Pet Supplements Market Size, Share & Industry Analysis, By Pet Type (Dogs, Cats, and Others), By Form (Tablets & Capsules, Chewable, and Liquid & Powder), By Function (Skin & Coat, Hip & Joint, Digestive Health, and Others), By Supplement Type (Glucosamine, Probiotics & Prebiotics, Multivitamins, Resveratrol and Others), By Distribution Channel (Online and Offline), and Regional Forecast, 2026–2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

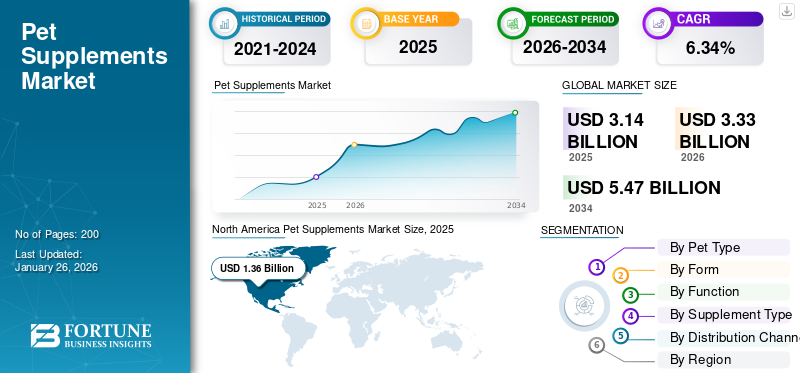

The global pet supplements market size was valued at USD 3.14 billion in 2025 and is projected to grow from USD 3.33 billion in 2026 to USD 5.47 billion by 2034, exhibiting a CAGR of 6.34% during the forecast period. North America dominated the pet supplements market with a market share of 43.37% in 2025.

Pet supplements are concentrated health-boosting ingredients, such as vitamins, minerals, fatty acids, or herbs, added to a pet's regular diet to support specific health needs, ranging from joint and skin health to digestion and overall well-being. Pet supplements are available in several types, including glucosamine, probiotics, prebiotics, multivitamins, and others, and can be found in forms of tablets, capsules, chewable, liquid, and powdered. Furthermore, these pet dietary supplements are made for skin & coat health, hips & joints, and others for cats, dogs, and other pets. The products are distributed through online and offline sources.

The pet population has displayed rapid growth in recent years, and rising pet humanization trends have significantly influenced the market. This has allowed it to showcase rapid growth in the forecast period.

Major players operating in the global market include Nestlé S.A., General Mills S.A., H&H Group, Mars Inc., and Virbac Corporation. Companies have been focusing on personalized nutrition, specialized products, and functional ingredients to cater to specific pet needs and preferences, mainly those related to individual pets' overall health conditions or breed-specific requirements.

Download Free sample to learn more about this report.

Pet Supplements Market Key Takeaways

- 2025 Market Size: USD 3.14 billion

- 2026 Market Size: USD 3.33 billion

- 2034 Forecast Market Size: USD 5.47 billion

- CAGR: 6.34% from 2026–2034

- North America dominated the pet supplements market with a 43.37% share in 2025.

- The dog segment is projected to account for the largest market share of 49.55% in 2026.

- The chewable form segment is projected to hold a 43.84% share in 2026.

North America

North America accounted for 43.37% of the global market in 2025, valued at USD 1.36 billion, and is projected to reach USD 1.44 billion in 2026.

Europe

Europe market was valued at USD 0.86 billion in 2025 and is estimated to reach USD 0.92 billion in 2026.

Asia Pacific

Asia Pacific held a 20.55% share of the global market in 2025, valued at USD 0.64 billion, and is projected to reach USD 0.69 billion in 2026.

U.S.

U.S. Market projected to reach USD 1.22 billion by 2026.

Japan

Japan Market projected to reach USD 0.17 billion by 2026.

Read More

MARKET DYNAMICS

Market Drivers

Growing Demand for Pet Supplements Amongst Millennial Pet Owners to Drive the Market Growth

The millennial age group drives the global pet supplement industry, as they hold a significant share of the global pet owner population. Millennial adults, particularly between their early 20s and late 30s, represent a rising portion of pet owners as they are more likely to pamper them as their own child. As per the American Pet Products Association, in 2023, millennials held a majority share in total pet ownership of around 33%. In addition, the number of multi-pet households has increased in recent years, with more than 75% of Generation Z and Millennial households owning more than one pet. The millennial and Generation Z demographics are tech-savvy and have higher educational levels and digital fluency. Thus, they are aware of supplements and pet health through online advertisements and product promotions, making them more inclined to purchase personalized and wellness-related product ranges, further fueling the global pet supplements market growth.

Increasing Pet Ownership Globally to Drive Market Growth

Dog and cat ownership has been rising steadily worldwide. The emerging economies such as the Asia Pacific and South America have the fastest pet adoption rate. Thus, an increasing pet population in these countries is fueling the pet supplement market. Factors such as the COVID-19 pandemic and demographic changes have driven more people to adopt pets. Another major driver for the industry growth is the rising disposable income of consumers. As end-user’s incomes rise, they are more likely to spend money on pet-related food, supplements, and services. According to the American Pet Products Association, U.S. consumers spent USD 152 billion on pets in 2024, out of which USD 65.8 billion was spent on pet food and treats. The developing regions have the fastest pet adoption rate. Thus, an increasing pet population in these countries is fueling the market growth.

Market Restraints

Stringent Regulations and Labelling Complexities to Impede Market Growth

Supplements and nutraceutical products for pets are highly regulated, especially in developed countries such as the U.S., Germany, and others. Pet supplement regulation varies significantly between nations, prompting businesses to navigate various regulatory environments and compliance regimes, particularly while internationally expanding. For instance, in the U.S., pet supplements and food are among the most highly regulated food products and are required to meet state and federal regulations. The U.S. Food and Drug Administration (FDA) has been regulating both finished pet food products (including treats and chews) and their ingredients. Moreover, inconsistent definitions such as what constitutes a “treat”, “functional food,” or “supplement” can lead to legal disputes and confusion. Moreover, the absence of universal labeling standards further leads to false claims, which in turn can erode consumer trust in pet supplements.

Market Opportunities

E-commerce Expansion to Provide Opportunity for Market Growth

The rise in direct-to-consumer (DTC) and e-commerce channels presents a significant opportunity for the market. The COVID-19 pandemic fueled the growth of e-commerce in all areas, including the pet industry. Social distancing practices, public health, urbanization, and decreasing household sizes have led to a shift in consumer behavior. Online shopping has been outperforming physical stores, with Chewy and Amazon channels being at the forefront. According to the American Veterinary Medical Association (AVMA), in the U.S., the percent of pet products purchased online tripled over the past five years, from 8% in 2015 to 30% in 2020. Subscription-based models are also emerging as a growth driver for the pet supplements industry. These models offer businesses a recurring and predictable revenue stream and foster financial stability and long-term growth. By offering unique pet health goals and aiding in specific dietary functions, these models enhance customer loyalty and engagement, creating a dedicated customer base.

Pet Supplements Market Trends

Rising Demand for Personalized Supplements to Shape the Industry

The global market has recorded a shift in individual mindsets from pet owners to pet parents, contributing to the rising pet humanization trend and making individuals more conscious of the ingredients used in pet supplements. The rapid growth in consciousness among individuals regarding their pet diet patterns, with the increasing awareness of diseases and factors that influence pet health, has augmented the demand for personalized supplements that deal with specific problems related to their pets. Thus, personalized supplement products such as anxiety, cognitive function development, immune support, eye health, and others have shown substantial growth in demand among pet parents/owners.

For instance, in March 2024, CV Sciences, Inc., a wellness company specializing in CBD extract, announced the launch of its new CBD chew line for pets called the +PlusCBD Pet line. This new pet supplement line is designed for dogs. It is a more personalized and organic product range with the new product launch catering to the growing demand for personalized and organic products among pet parents. The new product line includes Hip and Joint Health Chews and Calming Care Chews.

Download Free sample to learn more about this report.

Impact of Tariffs

Implementation of Tariff has disrupted Supply Chain, Hampering the Market Growth

The new reciprocal tariff imposed by the U.S. on several countries, including Canada, Mexico, and China, in April 2025, has significantly impacted the pet supplements sales. Tariffs can disrupt supply chains by making imported materials from certain countries more expensive. A shortage of raw materials in the U.S. may impact the production of key industry players. Thus, key players in the U.S market might need to restructure their supply chain to maintain sustainability in their business operations and accordingly frame their pricing strategy. As the trade environment continues to shift, pet food companies are closely monitoring further developments and planning to reframe their strategies to maintain stability in the supply chain and cost fluctuations. The uncertainties in the supply chain and pricing strategy may adversely affect the market growth for a couple of years. Non-government organizations and associations are stepping up to tackle the situation and have initiated collaborative strategies to maintain stability and sustainability in the business operation. In May 2025, the American Pet Products Association (APPA) initiated a joint effort by collaborating with seven other pet industry organizations including IndiePet, National Animal Supplement Council (NASC), Pet Advocacy Network (PAN), Pet Food Institute (PFI), Pet Industry Distributors Association (PIDA), and World Pet Association (WPA) to share strategies and align efforts to mitigate the impacts of tariffs on the pet industry. Such developments and assistance will help industry players to take effective strategic decisions to overcome the tariffs challenges.

SEGMENTATION ANALYSIS

By Pet Type

High Adoption Rates of Dogs Leads to Segment’s Highest Market Proportion

Based on pet type, the market is segmented into dogs, cats, and others.

The dog segment is projected to dominate the market with a share of 49.55% in 2026, with more individuals owning and interested in adopting dogs in the future. For instance, as per the American Pet Products Association, around 1.5 million dogs were adopted in 2024. Dogs mostly require frequent vaccinations, regular physical examinations, and rising preventive health care, fueling the need for pet care. Moreover, the rising awareness of hip and joint health among dog owners further contributes to segment growth.

Cats are the second most preferred pets globally, and the rising adoption of felines among Generation Z will further fuel the segment growth. As compared to dogs, cats are more independent and self-sustaining, which makes them an ideal choice as a pet for individuals with busy lifestyles and who reside in small apartments, leading to increased demand for cat-related products such as supplements.

By Form

Ease of Administration and Convenience Lead to the Chewable Form Segment’s Highest Market Share

Based on form, the market is segmented into tablets & capsules, chewable, and liquid & powder.

Chewable form segment is projected to dominate the market with a share of 43.84% in 2026, owing to the higher demand for chewable supplement products among dog owners. Several factors such as ease of use, taste preference, and perceived effectiveness influence supplement purchasing decisions based on the form in which they are available. However, the higher convenience provided by the chewable form has made it the most preferred form among individuals. These forms are often formulated with appealing flavors and are easier to administer, offering convenience to pets than traditional tablets or capsules.

Tablets & capsules are the second most preferred form type; holding the second largest global market share. Tablets and capsules are designed for specific types of disease, have a longer shelf life, and are more affordable; thus, they hold a significant share in the global market.

The liquid & powder segment is expected to have moderate growth during the forecast period. The powder form allows easy mixing with pet food, whereas, liquid form offers faster absorption and adjustable dosing.

By Function

Growing Prevalence of Joint Issues Leads to the Hip & Joint Segment’s Growing Market Proportion

Based on function, the market is segmented into skin & coat, hip & joint, digestive health, and others.

The hip & joint segment is projected to dominate the market with a share of 40.24% in 2026, owing to the higher prevalence of hip & joint problems among dogs. Furthermore, due to the higher number of aged pets, the demand for hip & joint supplements has grown significantly. Additionally, with increasing awareness of the health of pets among individuals, the sales of these supplements have shown rapid growth.

The digestive health holds a significant share in the global market, driven by the sensitive digestive health of pets, especially dogs. Furthermore, the rapidly growing awareness among pet owners and increasing pet humanization are expected to fuel the demand for digestive supplements in the global market. In addition, the digestive health of pets is monitored on a routine basis, which results in its steady consumption, further contributing toward the segment growth.

By Supplement Type

The Glucosamine Segment accounts for the Highest Market Share Due to Joint Health Issues and Increased Awareness

By supplement type, the market is classified into glucosamine, probiotics & prebiotics, multivitamins, resveratrol, and others.

Glucosamine, which holds a dominant market share of 37.24% in 2026, is known for protecting chondrocyte cells. It has the ability to help build cartilage and alleviate joint pain, making it a popular choice for pet owners seeking to improve their animals' mobility and overall well-being, fueling the demand for glucosamine supplements in the market.

Probiotics and prebiotics is the fastest-growing segment in the global market, owing to the higher demand for digestive function. Probiotics are supplements designed to maintain better digestive health.

Resveratrol is known to be a naturally occurring chemical found in some plants. Various studies have shown many positive benefits of resveratrol in pets such as dogs, cats, and horses, particularly in the areas of cardiovascular health, metabolic health, joint and bone health, and cognitive health.

The other segment, which includes supplements such as omega-3 fatty acids and several other nutrients, shows a rapid growth in demand, with a rising demand for anxiety-free supplements.

By Distribution Channel

Offline Segment accounts for the Highest Market Share Due to Wide Product Availability and Convenience

By distribution channel, the market is segmented into online and offline distribution channels.

The offline segment holds a dominant share of pet supplement sales globally. The higher pet supplements market share of the offline segment is owed to the availability of a wide range of products across retail stores such as supermarkets/hypermarkets and specialty stores, with a significant range of local and international brands. Furthermore, the offline distribution channel offers increased convenience in price comparison, fueling the segment’s growth.

The online distribution channel showcases the fastest CAGR during the forecast period, owing to the higher inclination of millennials toward online purchasing. Millennials account for the highest share of pet ownership across the globe. The restrictions and lockdown during the COVID-19 pandemic led to a surge in online pet product purchases, driving the sales. As online retailers and e-commerce grew, brick-and-mortar pet product specialists further expanded their product line over e-commerce platforms in order to meet the rising demand. For instance, in September 2021, PetSmart Inc., a privately held Canadian chain of pet superstores, launched The Pharmacy at PetSmart, an online portal for pet owners. The new website offers owners access to pet food, supplements, and other medications.

To know how our report can help streamline your business, Speak to Analyst

Pet Supplements Market Regional Outlook

Geographically, the global market report covers analysis across North America, Europe, Asia Pacific, South America, the Middle East & Africa.

North America

North America Pet Supplements Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 1.36 billion in 2025, representing 43.37% of the global market share, and is projected to reach USD 1.44 billion in 2026. The higher demand for pet supplements in the North American region is due to the growing awareness of the health and wellness of pets among pet owners in the U.S., Canada, and Mexico. The U.S. is the largest pet supplements market in the North American region, and its growth is primarily driven by the trend of pet humanization, where people in the country treat their pets as family members and are thus willing to spend more on premium and niche products.

According to the American Pet Products Association (APPA) National Pet Owners Survey, U.S. households reported ownership of approximately 68 million dogs, up from 65.1 million in the 2023-2024 survey. Additionally, increasing consumers’ health concerns drives the demand for natural, organic, and functional products. Therefore, companies are introducing new products in the organic and natural category. This will change the industry landscape in the upcoming years. The U.S. market is projected to reach USD 1.22 billion by 2026.

Europe

Europe has shown rapid growth in pet humanization, one of the significant factors fueling the demand for pet care products, and is a significant factor driving the market’s growth. According to the European Pet Food Industry Federation (FEDIAF), in 2021, 46% of European households, or 90 million houses, owned pets, compared to 88 million households in 2020. In addition, the region has shown increasing consumer awareness about sustainable and safe pet supplements. The U.K. is the dominant country in the European market, followed by Germany. Most European households are known to own one or more pets, indicating that pet ownership is very popular in Europe. According to the European Pet Food Industry Federation (FEDIAF), in 2023, 139 million households in Europe owned a pet. The rising number of pets in the region has further increased emphasis on animal healthcare and mobile pet grooming services. The UK market is projected to reach USD 0.2 billion by 2026, and the Germany market is projected to reach USD 0.19 billion by 2026. The Europe market was valued at USD 0.86 billion in 2025, capturing 27.48% of global revenue, and is estimated to reach USD 0.92 billion in 2026. The Europe market was valued at USD 0.86 billion in 2025, capturing 27.48% of global revenue, and is estimated to reach USD 0.92 billion in 2026.

Asia Pacific

Asia Pacific is expected to reflect the highest growth rate during the forecast period due to the increasing adoption of pets in China, India, Australia, Japan, and other countries. This growth is fueled by rising disposable income, growing demand for premium products, and expansion of online retail channels. Moreover, pet humanization is also fueling the demand for premiumization of healthcare, services, and food, with the Asian pet market showing staggering growth. In the past decade, lower birth rates and increasing loneliness levels across the population have given rise to a surge in pet demand. Animal companions have been bridging the gap between the need for belongingness and companionship across all age groups. Millennials often treat pets as a part of their family, while older generations find comfort in pet companionship to cope with the "empty nest" phenomenon. In 2025, Asia Pacific held 20.55% of the global market, reaching a valuation of USD 0.64 billion, and is projected to grow to USD 0.69 billion in 2026.

This trend is particularly noticeable in Japan, where millennials are a significant and the largest portion of pet owners. According to the Japan Pet Food Association (JPFA), in 2025, around 7.1 million pet dogs resided in Japan. While the pet adoption phenomenon was initially more common in Western countries, it has gained major traction in several Asian countries in the last few years, especially after the COVID-19 pandemic. The Japan market is projected to reach USD 0.17 billion by 2026, the China market is projected to reach USD 0.23 billion by 2026, and the India market is projected to reach USD 0.09 billion by 2026. In 2025, Asia Pacific held 20.55% of the global market, reaching a valuation of USD 0.64 billion, and is projected to grow to USD 0.69 billion in 2026.

South America

Emerging urbanization and shifting consumer lifestyles are vital factors influencing the adoption of pets in Latin American households. The market for pet supplements is exhibiting a notable shift in the region, with an increasing pet population, rising pet humanization trends, and growing urbanization across Brazil, Argentina, Chile, and Peru. Additionally, the emerging trend of pet parenting is likely to change the purchasing decisions of pet products. Thus, the demand for pet food and pet supplements is growing in the region. The positive shift in the supplements industry attracts regional and international players to enter the industry, which will drive market growth in the upcoming years. The Latin America region captured 7.20% of the global market in 2025, generating USD 0.23 billion in revenue, and is projected to reach USD 0.24 billion in 2026.

Middle East & Africa

The market in the Middle East & Africa is driven by the rising adoption of companion animals, strict regulation of pet food safety and packaging, and a higher focus on quality products. The growing middle class population in Africa also supports the growth of the Middle East & Africa region. The increasing popularity of premium products in developed Middle Eastern markets has remarkably contributed to the increased demand for functional and niche category products. The growing awareness regarding pet health has augmented the demand for premium pet supplements across different retail food channels. Moreover, e-commerce players such as Amazon are expanding their presence across the country. This will enhance the industry growth perspective in the upcoming years. For instance, in June 2025, Amazon South Africa expanded its product offerings by launching pet food & supplements, non-perishable groceries, and health supplements across the country. Middle East & Africa contributed approximately USD 0.04 billion to the global market in 2025, accounting for 1.41% share, and is expected to reach USD 0.05 billion in 2026. Middle East & Africa contributed approximately USD 0.04 billion to the global market in 2025, accounting for 1.41% share, and is expected to reach USD 0.05 billion in 2026.

Latin America

The Latin America region captured 7.20% of the global market in 2025, generating USD 0.23 billion in revenue, and is projected to reach USD 0.24 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Merger & Acquisition Strategies to Support Market Growth

The global market is consolidated and characterized by a dynamic and competitive landscape. This market is driven by increased pet ownership, preventive healthcare, and a growing focus on pet nutrition and wellness. Prominent companies engage in mergers and acquisitions to expand product portfolios and gain access to new markets, while partnerships with pet healthcare providers, veterinary doctors, and research institutions are growing in number. Major players operating in the global market include Nestlé S.A., General Mills S.A., H&H Group, Mars Inc., Virbac Corporation, and others.

- For instance, in April 2025, FoodScience, LLC, one of the leading providers of premium health and wellness solutions, acquired Natural Dog Company, a brand known for its high-quality dog care products. The acquisition expanded the company's presence in pet wellness and supplements and would address strong growth potential.

Key Players in the Pet Supplements Market

|

Rank |

Company Name |

|

1 |

Nestle SA |

|

2 |

Mars Inc. |

|

3 |

H&H Group |

|

4 |

Virbac Corporation |

|

5 |

General Mills Inc. |

List of Key Pet Supplements Companies Profiled:

- FoodScience LLC (U.S.)

- General Mills Inc. (U.S.)

- General Nutrition Centers, Inc. (U.S.)

- H&H Group (China)

- Mars, Incorporated (U.S.)

- Nestle S.A. (Switzerland)

- Nutramax Laboratories, Inc. (U.S.)

- PetLab Co. (U.K.)

- Virbac Corporation (France)

- Vitapower Limited (New Zealand)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: Fera Pets, the pet supplement brand, launched its first line of Soft Chews to support dog wellness from head to tail. The new Soft Chews offer the same high-quality support in a convenient and drool-worthy format. The new line includes Hip + Joint, Calming, Probiotic, Allergy + Immune, and Multivitamin supplements.

- May 2025: Zesty Paws, an award-winning pet supplement brand, launched Vet Strength Weight Management Bites for Dogs, a supplement containing ingredients to support fat metabolism, digestion, and a sense of fullness after eating.

- April 2025: FoodScience, LLC, one of the leading providers of premium health and wellness solutions, acquired Natural Dog Company, a brand known for its high-quality dog care products. The acquisition expanded the company’s presence in pet wellness and supplements and would address strong growth potential.

- March 2025: Nestle S.A. established a new pet food business in South Korea. The company’s Purina PetCare took over the company’s pet food business, marking a strategic shift in the South Korean market.

- March 2023: Mars Petcare entered the supplements category with the launch of a trio of new Pedigree multivitamins. The new range contains 100% natural chicken, at least eight vitamins, and is designed with active ingredients and available in soft chew format.

REPORT COVERAGE

The global pet supplements market report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, and distribution channels. Besides this, the market statistics report also provides insights into the global market analysis and highlights significant global market industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.34% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentations |

By Pet Type, Form, Function, Supplement Type, Distribution Channel, and Region |

|

Segmentation |

By Pet Type · Dog · Cat

|

|

By Form · Tablets & Capsules · Chewable · Liquid & Powder |

|

|

By Function · Skin & Coat · Hip & Joint · Digestive Health

|

|

|

By Supplement Type · Glucosamine · Probiotics & Prebiotics · Multivitamins · Resveratrol · Others |

|

|

By Distribution Channel · Online · Offline |

|

|

By Region · North America (By Pet Type, Form, Function, Supplement Type, Distribution Channel, and Country) • U.S. (By Supplement Type) • Canada (By Supplement Type) • Mexico (By Supplement Type) · Europe (By Pet Type, Form, Function, Supplement Type, Distribution Channel, and Country) • France (By Supplement Type) • Germany (By Supplement Type) • Italy (By Supplement Type) • Spain (By Supplement Type) • U.K. (By supplement Type) • Rest of Europe (By Supplement Type) · Asia Pacific (By Pet Type, Form, Function, Supplement Type, Distribution Channel, and Country) • Australia (By Supplement Type) • China (By Supplement Type) • India (By Supplement Type) • Japan (By Supplement Type) • Rest of Asia Pacific (By Supplement Type) · South America (By Pet Type, Form, Function, Supplement Type, Distribution Channel, and Country) • Argentina (By Supplement Type) • Brazil (By Supplement Type) • Rest of South America (By Supplement Type) · Middle East and Africa (By Pet Type, Form, Function, Supplement Type, Distribution Channel, and Country) • South Africa (By Supplement Type) • UAE (By Supplement Type) • Rest of the Middle East & Africa (By Supplement Type) |

Frequently Asked Questions

Fortune Business Insights says that the global Pet Supplements market value was USD 3.14 billion in 2025 and is anticipated to reach USD 5.47 billion by 2034.

At a CAGR of 6.34%, the global market will exhibit steady growth over the forecast period (2026-2034).

By type, the dog segment leads the market.

North America dominated the pet supplements market with a market share of 43.37% in 2025.

Mars Incorporated, Nestle S.A., Biostime Pharmaceuticals (Zesty Pas), iVet Professional Formulas, Farmina Pet Foods, and Nutramax Laboratories, Inc. are the major players in the market.

Increasing pet ownership globally is driving market growth.

Mars Incorporated, Nestle S.A., H&H Group, Virbac Corporation, and General Mills Inc. are the leading companies in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us