Polyethylene Foams Market Size, Share & Industry Analysis, By Foam Type (Non-crosslinked (EPE) and Crosslinked (XLPE/IXPE)), By End-use Industry (Protective Packaging, Construction & Insulation, Automotive & Transport, Sports & Recreational and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

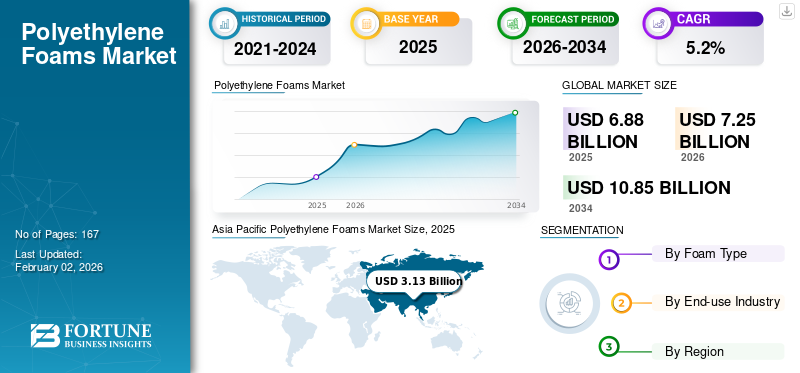

The global polyethylene foams market size was valued at USD 6.88 billion in 2025. The market is projected to grow from USD 7.25 billion in 2026 to USD 10.85 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period. Asia Pacific dominated the global polyethylene foams market with a market share of 45.5% in 2025.

Polyethylene (PE) foams are lightweight, closed-cell foamed materials primarily produced from LDPE/LLDPE. They can be manufactured as non-crosslinked Expanded Polyethylene (EPE) for cost-effective cushioning or as cross-linked polyethylene (XLPE/IXPE) for enhanced strength, thermal stability and improved compression set. These materials are typically supplied in the form of sheets, rolls, planks, profiles and fabricated components, and are used in protective packaging, insulation and industrial applications.

A significant market driver is the rising demand for protective packaging and lightweight, durable insulation solutions, supported by the growth of e-commerce, expanding shipments of electronics and appliances and the broader initiative to minimize shipping damage while enhancing energy efficiency in buildings and HVAC systems.

Furthermore, the market is dominated by several major players, including Sealed Air, Pregis LLC, Palziv, NMC PRODUCTS (M) SDN. BHD., and Zotefoams plc, which are at the forefront. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

POLYETHYLENE FOAMS MARKET Key Takeaways

- 2025 Market Size: USD 6.88 Billion

- 2026 Market Size: USD 7.25 Billion

- 2034 Forecast Market Size: USD 10.85 Billion

- CAGR: 5.2% from 2026–2034

- Asia Pacific dominated the global polyethylene foams market with a market share of 45.5% in 2025.

- The construction & insulation segment is anticipated to account for a 25.6% market share by 2025.

- The protective packaging segment is projected to grow at a CAGR of 6.3% throughout the study period.

Asia Pacific

Asia Pacific remained the largest regional market, reaching USD 3.13 billion in 2025, supported by strong manufacturing activity, electronics production, and export-oriented supply chains.

Europe

Europe is projected to reach USD 1.80 billion in 2026, driven by growing demand for engineered foam solutions in construction, transportation, and energy-efficient building applications.

North America

North America is expected to attain USD 1.09 billion in 2026, supported by robust logistics operations, industrial packaging demand, and construction-related insulation applications.

U.S.

The U.S. polyethylene foams market is estimated to reach USD 0.95 billion in 2026, benefiting from strong demand for protective packaging, industrial distribution, and high-performance foam products.

Japan

Japan continues to support regional market growth through its advanced manufacturing sector, increasing use of lightweight materials, and demand for high-quality packaging and insulation solutions.

Read More

POLYETHYLENE FOAMS MARKET TRENDS

Premiumization toward Engineered Foams and Application-Specific Solutions is an Emerging Market Trend

A notable trend involves a shift from generic cushioning materials to more engineered foam solutions that meet specific performance objectives, including compression set, thermal resistance, surface protection, cleanliness and dimensional stability. This shift fosters growth in crosslinked polyethylene foams and advanced laminates, as consumers increasingly prioritize predictable and validated performance over merely increasing material quantity. The trend also encompasses increased integration with converting and design services, as suppliers are engaging with clients to optimize packaging designs, minimize material consumption through more efficient geometry, and standardize components across product lines.

This approach benefits producers and converters who possess robust technical support, rapid prototyping capabilities and the capacity to deliver uniform parts at scale. Ultimately, sustainability-linked innovation is increasingly integrated into product differentiation strategies rather than an independent initiative. A greater emphasis on recyclable structures, formats that support take-back programs, recycled-content options where practicable and comprehensive documentation that assists customers in satisfying internal policies and regulatory mandates, predominantly in jurisdictions with stringent packaging regulations and high brand prominence.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Protective Packaging and Damage Reduction Needs Is Accelerating the Product Adoption

Polyethylene foams are extensively utilized for cushioning, blocking and surface protection due to their low density, reliable shock absorption and moisture resistance. As distribution networks become more intricate and shipping distances increase, manufacturers and logistics providers are increasingly prioritizing damage prevention, scuffing and product returns, mainly for high-value, fragile, or cosmetically sensitive items such as electronics, appliances, medical devices and premium consumer goods.

- UNCTAD estimates business e-commerce sales were around USD 25 trillion in 2021 and rose to almost USD 27 trillion in 2022.

An additional driving factor is the expansion of standardized, high-throughput packaging lines where uniform material properties are essential. The reliable compressive characteristics and widespread availability of PE foam in various formats, such as rolls, planks, and profiles, render it a practical option for international packaging standards that require consistent replication across manufacturing facilities and regions.

MARKET RESTRAINTS

Sustainability Scrutiny and Regulatory Pressure on Packaging Materials Limit Wider Adoption

A significant constraint is the heightened scrutiny regarding the end-of-life outcomes of packaging materials, particularly low-density plastics that pose challenges in collection and economically viable recycling. Although polyethylene (PE) is technically recyclable, foam formats are often disadvantaged due to collection inefficiencies, contamination risks and the need for additional densification processes prior to reprocessing. These factors can impact brand decisions, retailer packaging standards and procurement evaluation criteria.

Regulation and extended producer responsibility schemes have the potential to influence economic dynamics by increasing compliance costs, introducing reporting requirements, or incentivizing redesigns aimed at reuse or use of alternative materials. Consequently, certain end users may decrease foam utilization, modify packaging systems, or favor materials that is considered as more amenable to large-scale recycling.

MARKET OPPORTUNITIES

Circular PE Foam Systems and Higher Recycled-Content Adoption to Provide New Market Opportunities

A significant opportunity exists to enhance the compatibility of PE foam with circular economy principles by advancing collection, densification and recycling pathways, predominantly within B2B and industrial packaging industry, where take-back logistics are more straightforward. Implementing closed-loop programs for returnable transit packaging, protective interleaving, and reusable dunnage can facilitate the capture of foam in cleaner streams, thereby enabling more consistent recycling processes and supporting both economic and sustainability objectives.

Beyond packaging, there exist opportunities in higher-value applications where PE foam’s performance advantages are more challenging to substitute, such as technical insulation, sealing, vibration damping and engineered cushioning. These segments typically prioritize durability, moisture resistance, and stable mechanical properties, thereby creating opportunities for specialty grades, enhanced formulations and premium products.

MARKET CHALLENGES

Cost Volatility, Margins and Operational Complexity Constrain the Broader Use of Product

A fundamental challenge persists as the economics of PE foam are highly susceptible to fluctuations in resin and energy prices. Concurrently, numerous high-volume applications, particularly those involving commodity protective packaging, are subject to competitive pricing pressures. This dynamic can lead to margin compression and necessitate frequent price adjustments, thereby complicating capacity planning and the structuring of long-term contracts. Furthermore, producers encounter the ongoing challenge of balancing the production of low-cost commodity goods with the imperative to invest in differentiated products that offer higher profit margins.

Furthermore, supply chains for foam products can be voluminous and require significant logistical resources due to their low density, which heightens sensitivity to freight variations. Even amidst robust demand, factors such as transportation expenses, warehouse space limitations, and regional availability can pose constraints, necessitating companies to localize production and optimize conversion operations.

Download Free sample to learn more about this report.

Segmentation Analysis

By Foam Type

High Demand for Non-crosslinked Contributed to Segmental Growth

Based on Foam Type, the market is segmented into Non-crosslinked (EPE), Crosslinked (XLPE/IXPE), and Others.

The Non-crosslinked (EPE) segment dominated the Polyethylene Foams market share in 2025 as it provides dependable shock absorption, lightweight characteristics, and facile convertibility into pads, wraps, and inserts. The predominant advantage lies in its excellent compatibility with high-throughput packaging operations as manufacturers and converters can procure it broadly, process it expeditiously (including cutting, laminating, and die-cutting), and standardize protective performance across numerous SKUs, all while maintaining low unit costs.

The crosslinked segment is expected to grow at the highest CAGR during the forecast period. Crosslinked polyethylene foam is regarded as a higher-performance material characterized by superior compression set, enhanced thermal stability, and more consistent mechanical behavior over time. This renders it particularly suitable for demanding environments such as HVAC insulation, automotive interiors, and durable goods, where longevity is a critical factor.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Protective Packaging Segment to grow with the Fastest CAGR during the Forecast Period

In terms of End-use Industry, the market is categorized into protective packaging, construction & insulation, automotive & transport, sports & recreational, and others.

The protective packaging segment is expected to grow with the fastest CAGR. Protective packaging represents a primary application of polyethylene foam throughout the electronics, industrial, furniture and e-commerce sectors. The primary objective is to reduce distribution expenses by offering uniform, appropriately sized protection and thereby minimizing breakage and reverse logistics costs. This approach yields a favorable cost-benefit analysis compared to the higher costs associated with product loss or customer dissatisfaction. Furthermore, it is projected that this segment will grow at a compound annual growth rate of 6.3% throughout the specified study period.

The construction & insulation segment is expected to experience significant growth during the forecast period. Consistent demand for quicker, cleaner installation processes and enhanced comfort and performance within buildings is driving the segment growth. Contractors and OEM systems prefer materials that mitigate noise transmission, accommodate movement and support energy efficiency objectives, all while minimizing additional weight and complexity. Furthermore, the construction & insulation segment is anticipated to account for a 25.6% market share by 2025.

The automotive & transport segment is also experiencing moderate growth during the projected period. The key drivers include continuous effort to reduce vehicle weight and enhance interior comfort. Original Equipment Manufacturers (OEMs) and Tier suppliers strive to procure materials that ensure consistent NVH (Noise, Vibration, Harshness) and sealing performance, while maintaining low weight and simplifying part designs, particularly as vehicle configurations become increasingly intricate.

Polyethylene Foams Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East and Africa.

Asia Pacific

Asia Pacific Polyethylene Foams Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held a dominant share in 2024, valued at USD 2.90 Billion, and also took the leading share in 2025 with USD 3.13 billion of share. Asia Pacific is the largest and fastest-growing demand center for polyethylene foams, supported by the scale of manufacturing, electronics assembly, and export-oriented supply chains that rely heavily on protective packaging and cushioning. The key driving factors are expanding production of consumer electronics and appliances, rapid growth of intra-Asia and export logistics, and rising domestic consumption, which together drive high-volume EPE usage. At the same time, increasing adoption of higher-performance applications in automotive, infrastructure and premium consumer products is supporting faster growth for crosslinked PE foams in certain markets. In 2026, the China market is estimated to reach USD 1.83 billion.

China is the largest PE foam demand center in Asia Pacific, driven mainly by its huge manufacturing base and export-oriented supply chains that require high-volume protective packaging and surface protection for electronics, appliances and industrial goods. Domestic e-commerce and retail distribution also sustain steady consumption of cost-effective EPE in cushioning formats.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is expected to experience notable polyethylene foams market growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 4.0% and reach the valuation of USD 1.80 billion in 2026. Europe is characterized by a robust demand for technical, engineered foam solutions, particularly within construction-related applications such as underlayment, joint fillers and insulation adjuncts, as well as automotive and transport components, where performance and compliance standards are often stringent. The primary driving forces include the region’s emphasis on energy efficiency in buildings, high-value manufacturing practices, and ongoing demand for lightweight, durable materials. Additionally, sustainability considerations significantly influence product design and supplier selection, thereby accelerating interest in recyclable constructions, take-back-compatible formats and higher-value cross-linked foam applications. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 0.23 billion, Germany to record USD 0.36 billion, and France to record USD 0.25 billion in 2026.

North America

The market in North America is estimated to reach USD 1.09 billion in 2026 and secure a position of the third-largest region in the market. A substantial and mature market drives North America’s demand for polyethylene foam for protective packaging and industrial distribution, where PE foams are extensively specified for cushioning, surface protection and reusable transit packaging across electronics, appliances and industrial components. The primary driving forces include the region’s high logistics activity and a strong preference for consistent, standardized packaging performance, alongside a significant construction industry and HVAC sector that sustains steady demand for insulation-related foam applications, gasketing and underlayment products. With crosslinked grades increasingly capturing market share in higher-specification uses, this demand is expected to grow. In 2026, the U.S. market is estimated to reach USD 0.95 billion.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2026 is expected to reach a valuation of USD 0.06 billion. The demand in Latin America is primarily driven by protective packaging and broader industrial applications, with growth closely tied to manufacturing activities, consumer goods distribution, and ongoing modernization of packaging standards. In the Middle East & Africa, the GCC is set to reach a value of USD 0.17 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Innovation and Recyclability Are Essential Aspects for Growth of Companies Operating in Market

The global polyethylene foams market exhibits a moderate level of fragmentation, with leading manufacturers holding the majority of the market's total revenue. Industry participants concentrate on product innovation, lightweight solutions, recyclability and customized foam manufacturing. Regional competitors engage in competition through cost advantages and localized supply capabilities. The prominent market leaders include Sealed Air, Pregis LLC, Palziv, NMC PRODUCTS (M) SDN. BHD., and Zotefoams plc.

LIST OF KEY POLYETHYLENE FOAMS COMPANIES PROFILED

- Sealed Air (U.S.)

- Pregis LLC (U.S.)

- Palziv (Israel)

- NMC PRODUCTS (M) SDN. BHD. (Malaysia)

- Zotefoams plc. (U.K.)

- TORAY INDUSTRIES, INC. (Japan)

- FURUKAWA ELECTRIC CO., LTD. (Japan)

- JSP (Japan)

- Sekisui Alveo (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Sekisui Alveo launched a new recyclable thermoforming grade. The new product, Alveocel LLT LV, is positioned as a directly extruded, 100% mechanically recyclable polyethylene foam suitable for thermoforming. It serves as an alternative to highly crosslinked polyethylene foams.

- June 2025: Pregis, a worldwide leader in protective, mailing, bagging, and flexible packaging solutions, has announced the expansion of its IntelliPack high-performance foam-in-place line into North America. This expansion introduces the new Pregis IntelliPack Inspyre Film, a packaging solution designed with a focus on social impact. Foam-in-place packaging is specially engineered to safeguard fragile and heavy items during shipping.

- October 2024: Sekisui Alveo, a European producer renowned for premium polyolefin foams, has launched an innovative product with exceptional shock absorption. The Alveolen NSA is a polyethylene-based thermoplastic foam, ideal for challenging applications such as orthopaedics, sports protective gear, vibration damping, children's seats, and packaging.

- February 2024: Pregis introduced an advancement in foam technology utilizing certified circular polyethylene resins. In partnership with ExxonMobil, a pioneer in advanced recycling, Pregis now offers protective foam packaging that helps customers achieve their plastics circularity objectives.

REPORT COVERAGE

The global Polyethylene Foams market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The Polyethylene Foams market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.2% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Foam Type, End-use Industry, and Region |

|

By Foam Type |

· Non-crosslinked (EPE) · Crosslinked (XLPE/IXPE) |

|

By End-use Industry |

· Protective Packaging · Construction & Insulation · Automotive & Transport · Sports & Recreational · Others |

|

By Geography |

· North America (By Foam Type, End-use Industry, and Country) o U.S. (By End-use Industry) o Canada (By End-use Industry) · Europe (By Foam Type, End-use Industry, and Country/Sub-region) o Germany (By End-use Industry) o U.K. (By End-use Industry) o France (By End-use Industry) o Italy (By End-use Industry) o Rest of Europe (By End-use Industry) · Asia Pacific (By Foam Type, End-use Industry, and Country/Sub-region) o China (By End-use Industry) o Japan (By End-use Industry) o India (By End-use Industry) o South Korea (By End-use Industry) o Rest of Asia Pacific (By End-use Industry) · Latin America (By Foam Type, End-use Industry, and Country/Sub-region) o Brazil (By End-use Industry) o Mexico (By End-use Industry) o Rest of Latin America (By End-use Industry) · Middle East & Africa (By Foam Type, End-use Industry, and Country/Sub-region) o GCC (By End-use Industry) o South Africa (By End-use Industry) o Rest of the Middle East & Africa (By End-use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 6.88 Million in 2025 and is projected to reach USD 10.85 Million by 2034.

Recording a CAGR of 5.2%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The Protective Packaging End-use Industry segment led in 2025.

Asia Pacific held the highest market share in 2025.

Increasing demand for lightweight materials is accelerating the adoption of Polyethylene Foams

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us