Port Security Systems Market Size, Share & Industry Analysis, By Solution (Hardware, Software, and Services), By Deployment Model (On-premise, Cloud / SaaS, Hybrid, and Edge / Edge-AI Deployment), By Deployment Mode (Fixed, Mobile / Vehicle-Mounted, and Portable / Rapid-Deployment), By Security Area (Waterside / Maritime Domain, Landside Perimeter, and Others), By System (Video Surveillance and VMS, AI Video Analytics, and Others), By Technology (Video Surveillance, Radar Systems, Perimeter Intrusion Detection, and Others), By Port Type, By End User, and Regional Forecast 2026-2034

Port Security Systems Market Size and Future Outlook

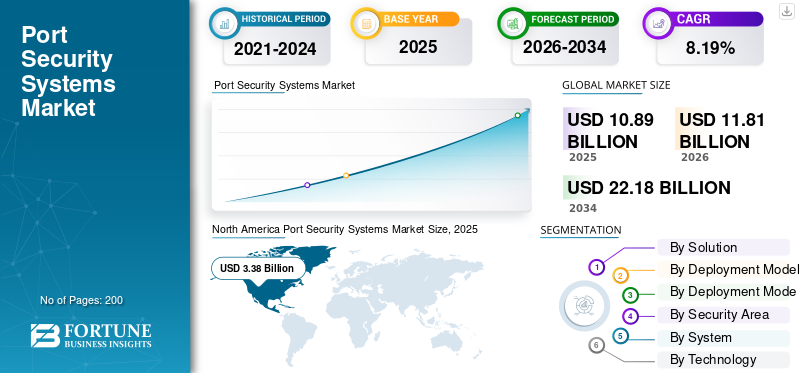

The global port security systems market size was valued at USD 10.89 billion in 2025. The market is projected to grow from USD 11.81 billion in 2026 to USD 22.18 billion by 2034, exhibiting a CAGR of 8.19% during the forecast period. North America dominated the port security systems market with a market share of 31.04% in 2025.

The market covers integrated security technologies used to protect seaports, terminals, cargo zones, passenger areas, situational awareness and waterside perimeters. It includes video surveillance, access control, perimeter intrusion detection, radar/AIS tracking, command-and-control software, cybersecurity, screening, and emergency communication systems. The demand for advanced port security is driven by ISPS Code compliance, rising maritime trade volumes, port automation, terrorism/smuggling risks, cyber threats, and the need to monitor people, cargo, vessels, and restricted zones in real time.

Major players include Honeywell, Siemens, Bosch Security and Safety Systems, Johnson Controls, and Thales Group, among others. These companies are pushing growth through integrated security platforms, combining access control, video surveillance, intrusion detection, radar/coastal surveillance, analytics, and cyber-resilient software into one operational view.

The strategies of key players are shifting from selling standalone cameras or gates to delivering modular, scalable, AI-enabled, and compliance-ready security ecosystems for ports. The focus is on upgrades of legacy port infrastructure, sensor fusion, open integration with third-party systems, cloud/remote real time monitoring, and long-term service partnerships with port authorities and terminal operators.

Download Free sample to learn more about this report.

Port Security Systems Market Trends

AI-Enabled Sensor Fusion, Hybrid Video Systems, and Integrated Command Centers Emerge as Significant Market Trends

The clear technology trend is the move from separate cameras, radars, gates, and alarms toward one shared operational picture. Thales’ CoastShield, published on November 4, 2024, reflects this direction. It combines AI, radar, electro-optical sensors, AIS, video management, drones, satellites, and control-center integration to detect abnormal maritime behavior and track threats from shore to open sea.

Siemens is taking a similar software-led approach in physical security. Its Siveillance Video platform highlights intelligent analytics, centralized control, hybrid cloud integration, real-time metadata search, vehicle analytics, and integration with access control and intrusion systems.

For instance, in April 2026, HENSOLDT UK secured two contracts with SRT Marine System Solutions to supply 50 coastal surveillance radars for integrated national coastal surveillance systems, with deliveries scheduled for 2026.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Compliance, Funding, and Real-Time Maritime Visibility to Push Ports toward Integrated Security Platforms

The main factor driving port security systems market growth is that ports are no longer securing only gates, fences, and cargo yards. They need a full operating picture across land, waterside, vessels, cargo, personnel, and digital systems. The IMO’s ISPS Code remains the baseline compliance driver as it requires port facility security assessments, security plans, designated security officers, and proportionate protective measures for ships and ports engaged in international trade. This directly supports the demand for access control, surveillance cameras, perimeter intrusion systems, screening, VTS/radar, emergency communication, and command-and-control software.

In the U.S., FEMA’s FY2025 Port Security Grant Program allocated USD 90 million to protect critical port infrastructure from terrorism, while the Coast Guard’s MTS cyber rule adds a cyber-compliance layer by requiring cybersecurity plans, cybersecurity officers, and cyber risk measures for regulated maritime entities.

For instance, in April 2026, MARAD announced USD 774 million for 37 U.S. port projects and the official release specifically mentioned upgraded screening technology to reinforce national security.

MARKET RESTRAINTS

High Integration Cost, Grant Uncertainty, and Legacy OT/IT Systems to Slow Security Modernization

The biggest restraint is the difficulty of upgrading complex, mixed-age port environments without disrupting operations. Many ports run older CCTV, gates, badge systems, terminal operating systems, cranes, VTS, access networks, and OT equipment from different vendors. Integrating these into one command platform is expensive and requires downtime planning, cybersecurity hardening, staff training, and often public procurement approvals.

Smaller ports also face budget pressure as advanced radar, AI video analytics, cybersecurity monitoring, and PSIM platforms require both purchase cost and long term maintenance, software licensing, and specialist operators.

For instance, in September 2025, GAO reported that the Port Security Grant Program awarded USD 690 million across 82 U.S. port areas over seven years, including surveillance cameras and cybersecurity projects. However, it also found that FEMA’s grant announcements did not fully explain scoring criteria and other award factors.

MARKET OPPORTUNITIES

Cyber Compliance, Port Modernization Grants, and Security-Sector Consolidation to Create New Upgrade Cycles

The strongest opportunity is in cyber-physical port security, where traditional physical security is being bundled with IT/OT protection. IMO’s revised Maritime Cyber Risk Management Guidelines dated April 4, 2025 highlight risks from digitalization, integration, automation, and network-based systems, while ENISA identifies port authorities, terminal operators, shipping companies, and related maritime entities as part of the EU maritime ecosystem covered under NIS2-driven cyber resilience expectations. This opens the demand for OT network segmentation, secure remote access, cyber drills, cybersecurity assessments, identity management, secure video networks, and managed security services for ports.

For instance, in June 2024, the acquisition of Carrier’s Global Access Solutions business added LenelS2, Onity, and Supra, strengthening enterprise access control, mobile credentials, cloud-based security, and recurring software revenue.

MARKET CHALLENGES

Cyber Risk, Supply-Chain Exposure, and Skills Gaps to Become as Serious as Physical Threats

The key challenge is that port security now spans physical security, cybersecurity, logistics data, industrial control systems, and third-party vendor access. GAO stated that the U.S. Maritime Transportation System handles more than USD 5.4 trillion in goods and services annually and faces significant cybersecurity risks from nation-state and criminal actors.

The same report found that Coast Guard oversight was limited by incomplete access to cybersecurity inspection information and cyber workforce gaps, which shows the scale of the operational challenge for ports adopting connected security systems.

SEGMENTATION ANALYSIS

By Solution

Software Segment to Grow at the Fastest Pace as Ports Shift from Standalone Systems to Integrated, AI-Led Security Platforms

By solution, the global market is classified into hardware, software, and services.

The software segment is estimated to be the fastest growing segment with the highest CAGR of 9.92% during the forecast period of 2026-2034. The growth is driven by ports moving from isolated CCTV, access control, and radar systems toward integrated command platforms, AI video analytics, cybersecurity dashboards, vessel tracking, and incident-management software. The segment growth is also supported by cloud deployment, predictive alerts, digital twin-style port monitoring, and centralized control rooms that help operators make faster decisions.

The hardware segment dominated the global port security systems market share, holding 57.61% in 2025. In addition, the segment is estimated to grow at a CAGR of 7.16% during the forecast period.

By Deployment Model

Edge / Edge-AI Deployment Segment to Surge at the Fastest Rate due to the Benefit of Reduced Latency

The global market, by deployment model, is classified into on-premise, cloud / SaaS, hybrid, and edge / edge-AI deployment.

The edge / edge-AI deployment segment is estimated to be the fastest growing with the highest CAGR of 10.37% during the forecast period of 2026-2034. This growth is driven by the need to process video, radar, access-control, and perimeter alerts closer to the source instead of sending everything to a central server. Edge AI reduces latency, lowers bandwidth pressure, and allows faster detection of intrusion, suspicious movement, unattended objects, drones, and unauthorized access. This is especially useful for large ports with wide perimeters and multiple terminals.

The on-premise segment dominated the global market share, accounting for 45.54% in 2025. In addition, the segment is estimated to grow at a CAGR of 7.36% during the forecast period.

By Deployment Mode

Mobile / Vehicle-Mounted Segment to Expand as Ports Need Flexible Security Coverage across Large Operating Areas

The global market, by deployment mode, is classified into fixed, mobile / vehicle-mounted, and portable / rapid-deployment.

The mobile / vehicle-mounted segment is estimated to be the fastest growing with the highest CAGR of 9.84% during the forecast period of 2026-2034. Ports are dynamic environments where risks shift between cargo yards, vessel security, passenger zones, fuel areas, and perimeter roads. Mobile command units, patrol vehicles with cameras, portable radar, and vehicle-mounted detection systems help operators respond quickly without waiting for permanent infrastructure. This makes mobile systems attractive for large, expanding, and multi-terminal ports.

The fixed segment dominated the global market with a share of 67.32% in 2025. In addition, the segment is estimated to grow at a CAGR of 7.50% during the forecast period.

By Security Area

Airspace / Counter-UAS Zone Segment Grows at the Fastest Rate as Drones Become a New Security Risk around Ports

The global market, by security area, is classified into waterside / maritime domain, landside perimeter, gate, road, and rail access points, cargo terminal area, passenger / public interface, critical infrastructure and utilities, administrative / command areas, cyber / OT network domain, and airspace / counter-UAS zone.

The airspace / counter-UAS zone segment is estimated to be the fastest growing with the highest CAGR of 11.73% during the forecast period of 2026-2034. Ports are increasingly exposed to drone-based surveillance, smuggling, disruption, and potential attack risks, especially near fuel terminals, naval-adjacent facilities, cruise terminals, and critical infrastructure. This is creating the demand for drone detection radar, RF sensors, electro-optical tracking, jamming-ready systems where permitted, and counter-UAS command integration. The segment is smaller but growing quickly as many ports are still at an early stage of airspace security adoption.

The cargo terminal area segment dominated the global market with highest share of 22.93% in 2025. In addition, the segment is estimated to grow at a CAGR of 9.60% during the forecast period.

By System

Counter-UAS / Drone Detection and Mitigation to Grow at the Fastest Rate as Ports Start Closing the Airspace Security Gap

By system, the global market is classified into video surveillance and VMS, AI video analytics, maritime domain awareness / VTS / AIS / radar integration, perimeter intrusion detection, access control and credentialing, biometric identity systems, cargo, baggage, and visitor screening, CBRNE detection systems, counter-UAS / drone detection and mitigation, cybersecurity / OT security systems, and PSIM / command-and-control / incident management.

The counter-UAS / drone detection and mitigation segment is estimated to be the fastest growing segment, expanding at the highest CAGR of 12.45% during the forecast period of 2026-2034. The segment growth is accelerating as drones create a relatively new threat layer for ports, while many existing security systems were designed mainly for land and waterside risks. Ports are adding RF detection, radar, EO/IR tracking, acoustic sensors, and integrated alert platforms to identify drones before they enter restricted airspace. Growth is the strongest where ports handle energy cargo, military-linked operations, cruise passengers, or critical national infrastructure.

The cargo, baggage, and visitor screening segment dominated the global market with a share of 18.28% in 2025. In addition, the segment is estimated to grow at a CAGR of 9.69% during the forecast period.

By Technology

Cybersecurity Segment to Expand at the Fastest Rate with Surging Port Dependence on Connected Systems

By technology, the global market is classified into video surveillance, radar systems, AIS / vessel tracking, electro-optical / IR systems, perimeter intrusion detection, access control, cybersecurity, and others.

The cybersecurity segment is estimated to be the fastest growing segment with the highest CAGR of 11.92% during the forecast period of 2026-2034. Modern ports depend on connected systems such as terminal operating systems, cranes, access control, surveillance networks, vessel tracking, cargo data, OT systems, and remote monitoring platforms. As these systems become more connected, cyber risk becomes a direct operational risk. This is why, the investment is rising in network monitoring, OT security, identity access management, secure communications, threat detection, and cyber-resilient command platforms.

The others segment dominated the global market with a share of 26.99% in 2025. In addition, the segment is estimated to grow at a CAGR of 7.39% during the forecast period.

By Port Type

LNG, LPG, Hydrogen, and Energy-Transition Ports Segment to Grow as Energy Cargo Raises Safety and National-Security Requirements

On the basis of port type, the global market is classified into smart / automated container ports, LNG, LPG, hydrogen, and energy-transition ports, cruise and ferry passenger ports, strategic/naval dual-use commercial ports, Ro-Ro and vehicle-handling ports, liquid bulk / oil / chemical ports, general cargo / multipurpose ports, and others.

The LNG, LPG, hydrogen, and energy-transition ports segment is estimated to be the fastest growing segment with the highest CAGR of 10.00% during the forecast period of 2026-2034. These ports need tighter security as energy cargo is high-value, hazardous, and strategically important. As hydrogen, LNG, and clean-energy infrastructure expand, operators require advanced perimeter systems, fire and gas monitoring, access control, maritime surveillance, cyber protection, and emergency-response integration. Security spending rises as any disruption at these ports can affect energy supply chains and public safety.

The smart / automated container ports segment dominated the global market with a share of 27.43% in 2025. In addition, the segment is estimated to grow at a CAGR of 9.78% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Energy Operator Segment to Expand with the Growth of LNG and Energy-transition Terminals

The global market by end user is classified into port authority, terminal operator, customs / border agency, coast guard / maritime police, navy / defense authority, logistics operator, cruise / ferry operator, energy operator, and others.

The energy operator segment is estimated to be the fastest growing segment with the highest CAGR of 10.47% during the forecast period of 2026-2034. Energy-linked port facilities face higher safety, environmental, and national-security risks compared with general cargo operations. This creates demand for stronger perimeter security, access control, waterside surveillance, cyber-OT protection, emergency communication, and integrated command systems. The segment growth is also supported by the expansion of LNG, hydrogen, offshore energy, and energy-transition terminals, where security is treated as a core operating requirement rather than a support function.

The port authority segment dominated the global market with a share of 22.95% in 2025. In addition, the segment is estimated to grow at a CAGR of 6.60% during the forecast period.

Port Security Systems Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Port Security Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant the global market share with a value of USD 3.38 billion in 2025 and is estimated to maintain the leading share in 2026, with USD 3.63 billion. The North America market is experiencing significant growth, driven by rising maritime trade, AI/IoT integration, and enhanced cybersecurity needs. It is projected to grow significantly, driven by threats such as smuggling, terrorism, and infrastructure upgrades, with key investments in surveillance, drones, and biometric technologies.

U.S. Port Security Systems Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 2.86 billion in 2025 and is estimated to depict a CAGR of 7.03% during the forecast period.

Europe

The Europe market is projected to grow at the second-fastest rate with a CAGR of 8.48% during the forecast period. In 2025, the market value stood at USD 2.79 billion. The regional market growth is driven by the need to protect EU trade, rising cybersecurity threats, and the need to combat smuggling. Key growth factors include adopting AI and IoT for surveillance, strict EU regulations (e.g., EMSA), and heightened geopolitical risks.

U.K. Port Security Systems Market

The U.K. market was valued at USD 0.46 billion in 2025 and is estimated to grow at a rate of 6.33% during the forecast period.

Nordic Countries Port Security Systems Market

In 2025, the Nordic Countries market was valued at USD 0.66 billion and is estimated to grow at a rate of 9.57% during the forecast period.

Rest of Europe Port Security Systems Market

The Rest of Europe market was valued at USD 0.38 billion in 2025 and is estimated to grow at a rate of 8.09% during the forecast period.

Asia Pacific

The Asia Pacific region is projected to depict the fastest growth with the highest CAGR of 9.67% over the analysis period. The regional market was valued at USD 3.36 billion in 2025. The growth is driven by rising maritime trade, infrastructure expansion, and digital transformation. The regional market is expanding with counter threats such as smuggling, piracy, and terrorism while improving operational efficiency. Moreover, massive investment in developing new ports and modernizing existing infrastructure across emerging nations is creating high demand for security technology.

China Port Security Systems Market

The China market was valued at USD 1.24 billion in 2025 and is estimated to grow at a rate of 7.74% during the forecast period.

India Port Security Systems Market

In 2025, the India market was valued at USD 0.44 billion and is estimated to grow at a rate of 12.59% during the forecast period.

Southeast Asia Port Security Systems Market

The Southeast Asia market was valued at USD 0.82 billion in 2025 and is estimated to grow at a rate of 11.43% during the forecast period.

Rest of the World

In the rest of the world, the Latin America and Middle East & Africa regional markets are expected to witness moderate growth during the forecast period. The Latin America market was valued at USD 0.48 billion in 2025. The Middle East & Africa market was valued at USD 0.86 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Industry Participants Invest in Edge Analytics and AI-enabled Monitoring Solutions to Outpace their Competitors

The competitive landscape is shifting from standalone hardware sales toward integrated security ecosystems that combine video surveillance, access control, intrusion detection, maritime radar, AIS/VTS, cybersecurity, and command-center software. Major OEMs are investing in AI-enabled monitoring, edge analytics, cloud/hybrid deployment, and open integration as port operators want one operational picture instead of separate systems for gates, waterside areas, terminals, and control rooms.

Industry competition is also being reshaped by mergers and agreements, portfolio restructuring, and larger surveillance contracts. Honeywell’s acquisition of Carrier’s Global Access Solutions strengthened its access-control, mobile credential, and security software portfolio, while Bosch’s sale of its security and communications product business to Triton shows that large players are refining portfolios around integration, services, and scalable platforms rather than only hardware manufacturing.

LIST OF KEY PORT SECURITY SYSTEMS COMPANIES PROFILED

- Honeywell International Inc. (U.S.)

- Thales Group (France)

- Bosch Security Systems / Robert Bosch GmbH (Germany)

- Siemens AG (Germany)

- Teledyne FLIR, LLC (U.S.)

- Tyco / Johnson Controls International plc (U.S.)

- Tidalis / Saab AB (Sweden)

- Leidos Holdings, Inc. (U.S.)

- Rapiscan Systems / OSI Systems, Inc. (U.S.)

- Smiths Detection Group Ltd. (U.K.)

- Indra Sistemas S.A. (Spain)

- Axis Communications AB (Sweden)

- Genetec Inc. (Canada)

- Leonardo S.p.A. (Italy)

- Kongsberg Gruppen ASA (Norway)

KEY INDUSTRY DEVELOPMENTS

- September 2025: OSI Systems’ S2 Global received a five-year CBP contract for the Non-Intrusive Inspection Common Integration Platform, with a potential value of about USD 54 million.

- September 2025: Planate Management Group received a CBP OASIS+ task order to support non-intrusive inspection infrastructure at the U.S. ports of entry.

- September 2025: SRT Marine Systems received formal award notification from a new sovereign customer for a maritime surveillance system expected to be worth about USD 200 million.

- July 2025: Terma signed an agreement with Denmark’s DALO to deliver 32 coastal surveillance radars and an AI-supported radar data integration platform.

- May 2025: SRT Marine Systems commenced the USD 167 million Indonesian National Maritime Security System project with Bakamla after financing and contract conditions were finalized.

REPORT COVERAGE

The global port security systems market analysis includes a comprehensive study of the market size and forecast by all the market segments included in the report. It contains details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions as well as key marine industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.19% from 2026-2034 |

| Unit | USD Billion |

|

Segmentation |

By Solution

By Deployment Model

By Deployment Mode

By Security Area

By System

By Technology

By Port Type

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 10.89 billion in 2025 and is projected to reach USD 22.18 billion by 2034.

In 2025, the Europe market value stood at USD 2.79 billion.

The market is expected to exhibit a CAGR of 8.19% during the forecast period.

By end user, the energy operator segment is expected to hold the highest CAGR over the forecast period.

Compliance, funding, and real-time maritime visibility are key factors driving the market.

Honeywell, Siemens, Bosch Security and Safety Systems, Johnson Controls, and Thales Group are the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us