Potassium Carbonate Market Size, Share & Industry Analysis, By Form (Powder, Granules, and Others), By Application (Glass Manufacturing, Fertilizers & Agrochemicals, Food Additives & Food Processing, Soaps, Detergents & Cleaners, Pharmaceuticals, and Others), and Regional Forecast, 2026-2034

POTASSIUM CARBONATE MARKET SIZE and FUTURE OUTLOOK

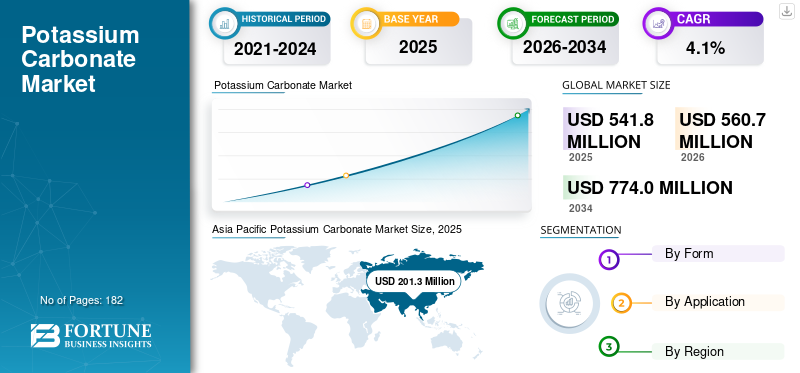

The global potassium carbonate market size was valued at USD 541.8 million in 2025. The market is projected to grow from USD 560.7 million in 2026 to USD 774.0 million by 2034 at a CAGR of 4.1% during the forecast period. Asia Pacific dominated the potassium carbonate market with a market share of 37.15% in 2025.

The Potassium Carbonate (PMMA) market refers to the global industry involved in the production, distribution, and consumption of potassium carbonate (K2CO3) across different forms and applications such as glass manufacturing, fertilizers and agrochemicals, food additives and food processing, soaps and detergents, pharmaceuticals, gas treatment, potassium silicate production, and other specialty industrial uses. The market is supported by a diversified application base, which is one of its key growth factors, as demand comes from multiple industries rather than depending on a single end-use sector. Growth is especially driven by its established role in glass manufacturing, where it is used as a specialty alkali and flux, as well as by rising demand for food-grade and high-purity potassium carbonate in regulated food-processing applications. Key players operating in the market include Armand Products Company, AGC Chemicals, Hawkins Inc, UNID Co. Ltd., and Vynova Group.

Download Free sample to learn more about this report.

Potassium Carbonate Market KEY TAKEAWAYS

- 2025 Market Size: USD 541.8 million

- 2026 Market Size: USD 560.7 million

- 2034 Forecast Market Size: USD 774.0 million

- CAGR: 4.1% from 2026–2034

- Asia Pacific dominated the potassium carbonate market with a 37.15% share in 2025.

- The powder segment is expected to account for the largest market share during the forecast period.

- The glass manufacturing segment is expected to hold the leading share of the global market.

Asia Pacific

Asia Pacific USD 201.3 million in 2025, driven by strong manufacturing and downstream industries.

North America

North America USD 116.6 million in 2025, supported by stable industrial demand and domestic production.

Europe

Europe Expected to witness significant growth due to its strong specialty chemicals and manufacturing base.

U.S.

U.S. USD 116.6 million in 2025, accounting for approximately 21.5% of global market revenue.

Japan

Japan Supported by strong demand from the specialty chemicals, electronics, and glass manufacturing industries.

Read More

POTASSIUM CARBONATE MARKET TRENDS

Shift Toward Application-Specific Purity, Food Compliance, and Lower-Carbon Chlor-Alkali Supply to be a Significant Market Trend

A visible trend in the global market is the move away from treating the product as a simple commodity alkali and toward application-specific grades aligned with end-use performance, purity, and compliance requirements. Producer documentation from Armand shows distinct grades such as extra fine, dense granular, glass grade, and food grade, while AGC Vinythai markets potassium carbonate 99% minimum and positions it for uses ranging from glass and ceramics to food processing applications. This suggests that suppliers are increasingly differentiating their portfolios by particle size, purity, and downstream suitability rather than competing only on bulk tonnage.

A second trend is the gradual integration of sustainability and process-efficiency positioning into chlor-alkali value chains that produce potassium carbonate from potassium hydroxide and carbon dioxide. USDA’s 2023 technical report notes that synthetic potassium carbonate is commonly produced through reaction of potassium hydroxide with carbon dioxide, and AGC Vinythai recently announced carbon-footprint certification for potassium carbonate at its MTP2 plant in Thailand. That does not make potassium carbonate a “green chemistry” market overnight, but it does show that suppliers are starting to compete on lower-emissions manufacturing credentials alongside quality and supply reliability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Broad Multi-Industry Use Base Supports Stable Structural Market Demand

One of the strongest drivers for potassium carbonate market growth is its broad application base across glass, fertilizers and agrochemicals, food processing, detergents, pharmaceuticals, gas treatment, and potassium silicates. Armand’s potassium carbonate handbook and SDS both list these uses explicitly, which is important as it shows demand is not tied to a single cyclical end market. That diversified use pattern helps support baseline consumption even when one downstream segment softens.

Glass manufacturing remains particularly important as potassium carbonate functions as a flux and specialty alkali input in glass and ceramic systems. At the same time, the product is approved for food use in regulated settings, with the U.S. eCFR listing potassium carbonate under 21 CFR 184.1619 as a direct food substance generally recognized as safe and Armand offering food-grade material that meets FCC and cGMP-linked specifications. That combination of industrial and food-linked demand makes the market more resilient.

MARKET RESTRAINTS

Availability of Substitute Alkalis Limits Wider Volume Expansion

A major restraint for the market is the availability of alternative alkaline chemicals in several downstream applications. In detergents, cleaners, industrial processing, and some chemical formulations, potassium carbonate competes with other alkalis such as sodium carbonate, potassium hydroxide, and caustic-based systems, depending on formulation requirements, cost position, and performance needs. This limits the market’s ability to expand freely across broader industrial applications, since buyers often evaluate potassium carbonate not as a compulsory raw material but as one option within a larger alkaline chemicals basket.

This restraint is important as many end users remain highly sensitive to input cost, process efficiency, and product formulation flexibility. If competing alkalis offer lower cost or easier availability, potassium carbonate can lose share in non-critical applications even when it remains technically suitable. As a result, the market’s growth is often stronger in specialized uses such as food processing, specialty glass, and selected pharmaceutical or gas-treatment applications, while broader industrial penetration may remain constrained by substitution risk.

MARKET OPPORTUNITIES

Food, Processed Beverage, and Higher-Purity Industrial Grades Create Premium Growth Space

One of the opportunities in the market is the expansion of higher-purity and food-compliant potassium carbonate grades. The U.S. FDA framework recognizes potassium carbonate for specified food use, USDA continues to review it within organic handling contexts, and Armand’s food-grade specifications reference FCC compliance and cGMP-related controls. This creates room for suppliers to defend better margins in food processing, beverage buffering, cocoa alkalization, and specialty formulated products compared with purely bulk industrial sales.

Another opportunity is the continued development of Southeast Asian manufacturing and regional chemical processing networks. AGC has been expanding and reorganizing its chlor-alkali operations in Southeast Asia, while AGC Vinythai’s annual reporting confirms potassium carbonate as part of its product portfolio. As food processing, specialty glass, detergents, and industrial manufacturing expand across Asia, suppliers with integrated chlor-alkali assets and regional logistics should be well placed to capture incremental demand.

MARKET CHALLENGES

Demand Diversity Helps, but Market Remains Vulnerable to End-Use Mix and Supply Concentration

A major challenge for potassium carbonate is that although it serves many applications, several of them are specialty or mid-scale uses rather than massive commodity outlets, which can limit volume acceleration. The market benefits from diversification, but that same fragmentation means growth often depends on steady expansion across multiple sectors rather than one dominant engine. Armand’s handbook shows a wide set of uses, but many of these are niche industrial applications rather than very large single-volume categories.

The market also faces concentration risk in supply. Armand states that it is one of the world’s largest producers, while AGC Chemicals says it has potassium carbonate production plants in Japan and Thailand. That kind of concentrated visible producer base can support quality and reliability, but it also means regional outages, plant disruptions, or chlor-alkali feedstock issues can affect availability more noticeably than in highly fragmented commodity markets.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions can affect the market by increasing uncertainty around feedstock, energy, and cross-border chemical trade flows. The OECD’s 2024 inventory says export restrictions on industrial raw materials are becoming more prevalent and more prohibitive, with negative spillovers across downstream supply chains. Potassium carbonate is not itself a marquee critical mineral, but it sits within globally linked chlor-alkali and industrial chemical systems that are still sensitive to trade friction, logistics disruption, and regional policy shifts.

This effect is especially relevant in Asia Pacific, where 2024 WITS data shows South Korea as the leading exporter of potassium carbonates, while India is a major importer and AGC/AGC Vinythai maintain production in Japan and Thailand. That means shifts in Asian trade routes, energy costs, or industrial policy can influence global availability and delivered pricing more than the market’s modest size might initially suggest.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly centered on process efficiency, purity control, application-specific grades, and lower-footprint production systems. On the product side, the market is clearly segmented into forms and applications tailored to food, glass, and industrial processing. On the manufacturing side, USDA’s technical description of the potassium hydroxide-plus-carbon dioxide route highlights the importance of reaction efficiency and quality control, while AGC Vinythai’s carbon-footprint certification points to rising interest in proving environmental performance at the plant level.

That makes potassium carbonate R&D less about radical chemistry innovation and more about better manufacturing, tighter specifications, and stronger compliance positioning. Food-grade purity, stable particle-size distribution, handling performance, and carbon-accounting visibility are likely to remain the main development themes, especially as customers seek both functional reliability and cleaner supply chains.

SEGMENTATION ANALYSIS

By Form

Powder Segment Dominates Due to its Broad Suitability Across Glass, Food, Detergent, and General Chemical Applications

Based on form, the market is segmented into powder, granules, and others.

Among these, powder segment is expected to hold the dominant potassium carbonate market share as it is the most versatile format for downstream formulation, blending, food processing, specialty glass, and chemical manufacturing. Armand’s product portfolio includes extra fine and food-grade formats, while AGC Vinythai also markets solid potassium carbonate, indicating strong commercial relevance for dry material forms in mainstream industrial use.

The granules segment also maintains an important position since dense granular material supports handling efficiency and controlled dissolution in industrial systems. The segment expected to register 3.7% CAGR during the forecast period.

The others segment, including liquid solution and flakes where applicable, remains smaller and more application-specific, typically serving customers with particular storage, dosing, or process-line requirements.

By Application

To know how our report can help streamline your business, Speak to Analyst

Glass Manufacturing Segment Leads Due to Potassium Carbonate’s Established Role as a Specialty Alkali and Flux

Based on application, the market is segmented into glass manufacturing, fertilizers & agrochemicals, food additives & food processing, soaps, detergents & cleaners, pharmaceuticals, and others.

Among these, glass manufacturing segment is expected to hold the leading share of the global market. This dominance is supported by the long-established use of potassium carbonate as a specialty alkali and flux in glass and ceramic systems, where it helps modify melting behavior and supports the production of specialty formulations. The segment benefits from continued demand for specialty glass products used in laboratory equipment, technical glass, display-related components, and selected industrial and decorative applications. Compared with many other applications, glass manufacturing offers a more structurally stable demand base as it consumes potassium carbonate as part of an established materials formulation rather than a highly limited specialty function.

The fertilizers & agrochemicals segment to register significant growth during the forecast period. Potassium carbonate is used in selected agricultural chemical systems and related formulations, giving it relevance in crop-input chemistry and allied processing chains. Its connection to broader potash chemistry also supports this segment’s role, as potassium-based materials remain important across the agricultural value chain. Although potassium carbonate is not as dominant as more mainstream potash fertilizers, its use in specialized formulations and intermediate processing applications provides a stable secondary demand stream. The segment also benefits from ongoing agricultural productivity requirements and the need for chemical inputs that support efficient cultivation and crop protection practices. The segment is set to grow at a CAGR of 4.4% during the forecast period.

The food additives & food processing segment is also expected to account for a notable share of the market. Potassium carbonate is recognized for food-related uses in buffering, acidity regulation, and processing functions, which gives it direct relevance in selected food and beverage applications. It is used in areas such as cocoa processing, pH control, and formulation support in processed food systems. This segment remains commercially attractive as food-grade applications typically require tighter quality and compliance standards, which can support better pricing compared with some bulk industrial uses.

The others segment includes gas treatment, potassium silicate production, rubber additives, catalysts, cement, and other specialty industrial uses. This category remains relevant as potassium carbonate serves a wide variety of technical functions across smaller downstream markets. In gas treatment, it is used in selected process systems, while in potassium silicate production it acts as a key input for downstream chemical manufacturing. Additional niche uses in rubber, catalysts, and cement further broaden the application base of the product.

POTASSIUM CARBONATE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Potassium Carbonate Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global potassium carbonate market. The region benefits from strong manufacturing depth, a broad downstream base in glass, food processing, detergents, and industrial chemicals, and visible producer presence in Japan, Thailand, Korea, and China-linked supply chains. AGC Chemicals states that it has potassium carbonate production plants in Japan and Thailand, AGC Vinythai confirms production and distribution from Thailand, and WITS data shows South Korea as the largest 2024 exporter of potassium carbonates.

China Potassium Carbonate Market

China’s market is one of the largest globally, with 2025 revenue at USD 73.4 million, representing roughly 13.5% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is likely to register steady growth, supported by established domestic manufacturing, diversified end-use demand, and relatively strong supply reliability. Armand operates a potassium carbonate production facility in Muscle Shoals, Alabama, describes itself as one of the world’s largest producers, and says it ships products across North America and globally.

U.S. Potassium Carbonate Market

In 2025, the U.S. represented a USD 116.6 million market, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 21.5% of global market sales.

Europe

Europe to register significant growth during the forecast period. The growth is driven by its mature specialty chemicals base, food and beverage processing, pharmaceutical production, and established intra-regional trade. The region’s importance comes not only from single-country output but also from the way specialty chemicals, formulated products, and cross-border distribution are integrated across European markets.

Germany Potassium Carbonate Market

The Germany market was valued at around USD 37.6 million in 2025, representing roughly 6.9% of global market revenues.

U.K. Potassium Carbonate Market

The U.K. market was valued at around USD 15.2 million in 2025, representing roughly 2.8% of global market revenues.

Latin America

Latin America is a smaller but relevant market, supported by food processing, detergents, industrial chemicals, and selected glass and agricultural applications. The region does not stand out as a major global production base in the same way as Asia Pacific or North America, so demand is more likely to depend on imports and distributor networks. That makes Latin America commercially meaningful, even if it is not one of the primary global supply centers.

Brazil Potassium Carbonate Market

Brazil market was valued at around USD 19.4 million in 2025, representing roughly 3.6% of global market revenues.

Middle East & Africa

The Middle East & Africa market remains comparatively smaller, but opportunities exist in food processing, industrial chemicals, detergents, and selected gas-treatment or specialty industrial applications. WITS import data shows scattered demand across Kuwait, Qatar, Morocco, Nigeria, and South Africa-linked regional trade channels, suggesting a fragmented market structure rather than one dominant country base. Growth here is likely to depend more on industrial expansion and import accessibility than on large-scale local production.

GCC Potassium Carbonate Market

The GCC market was valued at around USD 15.6 million in 2025, representing roughly 2.9% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Competing Through Upstream Chlor-Alkali Integration, Food/Pharma Certifications, and Application-Led Grade Positioning

The global potassium carbonate market is moderately concentrated around a mix of integrated chlor-alkali producers, specialty potassium-chemicals manufacturers, and high-purity/reagent-grade suppliers. Competition is shaped less by branding and more by backward integration into potassium hydroxide, manufacturing reliability, food and pharmaceutical compliance, regional logistics, and the ability to supply application-specific grades for glass, food processing, detergents, agrochemicals, pharmaceuticals, and specialty chemicals. Armand positions itself as one of the world’s largest potassium carbonate producers, AGC manufactures potassium carbonate from its own caustic potash and has production in Japan and Thailand, Vynova has built out its potassium derivatives platform in Europe, and INEOS KOH highlights integrated liquid potassium carbonate production at its chlor-alkali site in Ohio.

LIST OF KEY POTASSIUM CARBONATE COMPANIES PROFILED IN REPORT

- Armand Products Company (U.S.)

- AGC Chemicals (Japan)

- Hawkins Inc (U.S.)

- UNID Co. Ltd. (South Korea)

- Vynova Group (Belgium)

- INEOS KOH Inc. (U.S.)

- TOAGOSEI CO., LTD. (Japan)

- Takasugi Pharmaceutical Co.Ltd. (Japan)

- KANTO CHEMICAL CO., INC. (Japan)

- KISHIDA CHEMICAL Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Armand Products’ potassium carbonate product range was listed under updated Orthodox Union kosher certification, supporting its continued food and specialty-ingredient market positioning.

- May 2022: AGC announced capacity expansion of its chlor-alkali business in Thailand through AGC Vinythai, which is relevant for potassium carbonate as AGC’s potassium carbonate production is integrated with its caustic potash chain in Japan and Thailand.

- December 2021: INEOS Enterprises completed the acquisition of ASHTA Chemicals, now INEOS KOH, preserving and strengthening a North American potassium-based chemicals platform that includes liquid potassium carbonate made from upstream potassium hydroxide.

REPORT COVERAGE

The potassium carbonate market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, form, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Million), Volume (Kiloton) |

| Growth Rate | CAGR of 4.1% from 2026 to 2034 |

| Segmentation | By Form, By Application, By Region |

| By Form |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 541.8 million in 2025 and is projected to reach USD 774.0 million by 2034.

Recording a CAGR of 4.1%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The glass manufacturing segment is expected to lead market during the forecast period.

Asia Pacific held the highest market share in 2025.

Broad multi-industry use base supports stable structural demand drives market growth.

- 2021-2034

- 2025

- 2021-2024

- 182

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us