Power Generation Equipment Market Size, Share & Industry Analysis, By Equipment Type (Turbines, (Steam Turbines, Gas Turbines, Hydro Turbines, and Wind Turbines), Generators, Boilers, Transformers, and Balance of Plant (BOP) Equipment), By Power Source (Thermal Power, Renewable Power, and Nuclear Power), By Application (Utility Power Generation, Industrial Power Generation, and Distributed Power Generation), and Regional Forecast, 2026 – 2034

Power Generation Equipment Market Size and Future Outlook

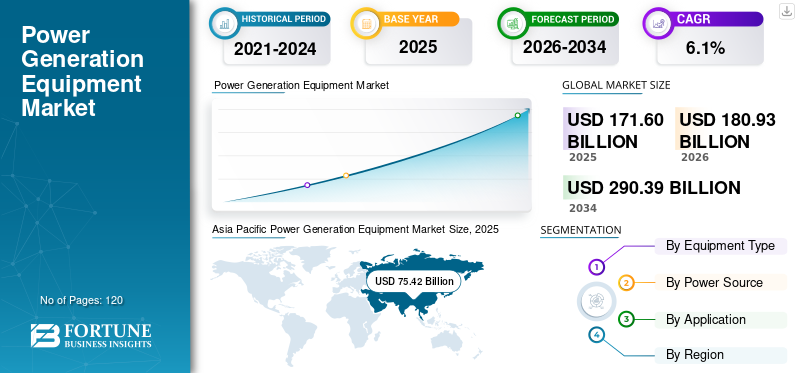

The global power generation equipment market size was valued at USD 171.60 billion in 2025. The market is projected to grow from USD 180.93 billion in 2026 to USD 290.39 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period. Asia Pacific dominated the power generation equipment market with a market share of 44.13% in 2025.

Power generation equipment comprises critical industrial machinery used to convert various energy sources, including fossil fuels, nuclear, and renewables, into electricity through mechanical and thermal processes. The market is witnessing steady growth, driven by rising demand for electricity, increasing investments in energy infrastructure, and the ongoing transition toward cleaner and more efficient power generation technologies across key regions, including the Asia Pacific and North America. These systems are widely deployed across large-scale utility power plants, industrial captive facilities, and distributed generation setups to ensure a reliable and efficient electricity supply for residential, commercial, and industrial applications. They play a vital role in improving generation efficiency, optimizing fuel utilization, and supporting compliance with stringent environmental and emission regulations. Current market trends indicate increasing adoption of high-efficiency gas turbines, renewable-integrated generation systems such as solar and wind, and advanced boiler technologies, enabling enhanced performance and reduced carbon footprint. The adoption of combined heat and power (CHP) systems is also gaining traction, particularly in industrial applications, to improve overall energy efficiency. Power producers are increasingly focusing on lowering operational costs, strengthening energy security, improving plant efficiency, and aligning with decarbonization targets. Additionally, advancements in digital monitoring and real-time performance optimization are enhancing operational reliability, while evolving supply chains are influencing equipment availability and deployment timelines. From a regional analysis perspective, growth is supported by capacity additions in emerging economies and replacement demand in mature markets, while the competitive landscape of key players continues to influence technology adoption and market expansion across various segments.

- For instance, in March 2026, Siemens Energy AG announced the deployment of its advanced hydrogen-ready gas turbine systems for a large-scale combined cycle power plant project in Europe. The project is aimed at improving efficiency and enabling future low-carbon fuel integration in utility-scale power generation facilities.

General Electric (GE Vernova), Siemens Energy AG, Mitsubishi Heavy Industries, Ltd., Wärtsilä Corporation, and Doosan Enerbility Co., Ltd. are among the key players holding a significant share in the market. Their competitive positioning is strengthened by strong expertise in turbine and power system technologies, the ability to deliver high-efficiency and application-specific generation solutions, extensive global manufacturing and service networks, and continuous innovation in low-emission and flexible power generation systems to meet evolving energy demand and sustainability requirements.

Download Free sample to learn more about this report.

Power Generation Equipment Market Key Takeaways

- 2025 Market Size: USD 171.60 billion

- 2026 Market Size: USD 180.93 billion

- 2034 Forecast Market Size: USD 290.39 billion

- CAGR: 6.1% (2026–2034)

- Asia Pacific dominated the market with a 44.13% share in 2025.

- The turbines segment held the largest market share.

- The utility power generation segment accounted for the largest share of the global market.

Asia Pacific

Asia Pacific generated USD 75.72 billion in 2025, maintaining its leading market position.

North America

North America accounted for USD 34.66 billion in 2025.

Europe

Europe is projected to witness steady growth, driven by decarbonization initiatives, renewable energy integration.

U.S.

U.S. market is projected to reach USD 28.54 billion by 2026.

Japan

Japan market is projected to reach USD 7.16 billion by 2026.

Read More

POWER GENERATION EQUIPMENT MARKET TRENDS

Growing Need for Operational Flexibility is Amplifying Product Demand

Demand for power generation equipment is increasingly being influenced by the growing need for operational flexibility and the ability to adapt to dynamic power demand patterns across modern energy systems. With the rising penetration of intermittent renewable energy sources such as wind and solar, power producers are focusing on deploying equipment capable of rapid ramp-up, load balancing, and efficient operation under variable load conditions. This shift is driving the adoption of advanced gas turbines, flexible steam systems, and hybrid generation configurations that can respond quickly to fluctuations in grid demand while maintaining efficiency. Unlike traditional base-load-centric systems, there is a growing emphasis on equipment that can operate efficiently across partial loads and frequent start-stop cycles without significant performance degradation. Additionally, utilities are prioritizing systems that support grid stability, frequency regulation, and seamless integration with renewable energy sources. Instead of purely maximizing output capacity, the focus is shifting toward enhancing operational responsiveness, reliability, and system flexibility, enabling power generation assets to function as dynamic components within increasingly complex and decentralized energy networks.

- For instance, in April 2026, Mitsubishi Heavy Industries, Ltd. introduced enhancements to its next-generation gas turbine systems designed for improved load-following capability and rapid start-up performance. These enhancement supports grid stability and renewable energy integration in modern power generation applications.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Electricity to Drive Market Growth

The market is witnessing steady growth as global energy systems increasingly focus on meeting rising electricity demand while transitioning toward more efficient and lower-emission generation technologies. Rapid urbanization, industrial expansion, and electrification across sectors such as manufacturing, data centers, and transportation are driving the need for a reliable and continuous power supply. The increasing complexity of power generation requirements, including base-load generation, peak load management, and renewable integration, is encouraging the deployment of advanced equipment capable of operating efficiently across varying load conditions. Power generation equipment equipped with high-efficiency turbines, advanced combustion systems, and optimized thermal processes enables operators to enhance fuel utilization while maintaining consistent output, particularly in combined cycle and hybrid generation configurations. The growing emphasis on reducing operational costs and improving plant performance is accelerating the adoption of systems that offer higher efficiency and flexibility. As investments in energy infrastructure continue to rise, particularly in emerging economies, there is increasing demand for equipment that can support both large-scale utility projects and decentralized power systems. Equipment manufacturers are responding by enhancing turbine efficiency, improving heat recovery systems, and integrating digital monitoring capabilities, enabling operators to achieve higher reliability and operational efficiency across diverse power generation applications.

- For instance, in April 2025, GE Vernova announced the successful deployment of its HA-class gas turbine at a combined cycle power plant project. The deployment achieved high-efficiency performance and supported flexible grid operations for renewable energy integration.

MARKET RESTRAINTS

High Capital Investment to Limit Market Expansion

The power generation equipment market growth is constrained by the high capital investment required for installation and integration within power generation facilities, which can be a significant barrier, particularly for developing economies and smaller power producers. Large-scale power projects involve substantial upfront costs associated with turbines, boilers, generators, and auxiliary systems, along with engineering, procurement, and construction activities, increasing overall project complexity and financial burden. While these systems offer long-term efficiency gains and operational benefits, the return on investment is highly dependent on plant utilization rates, regulatory stability, and long-term power demand, making investment decisions more sensitive to market uncertainties. In many regions, delays in project approvals, financing challenges, and regulatory hurdles further extend project timelines, limiting the pace of new equipment deployment. Additionally, the operation and maintenance of advanced power generation systems require a skilled workforce and technical expertise, which may not be readily available across all markets. This can lead to concerns regarding operational reliability and lifecycle costs, particularly in regions with limited technical infrastructure, thereby impacting the adoption of advanced power generation technologies.

MARKET OPPORTUNITIES

Accelerating Transition Toward Low-Emission Power Generation Systems to Create Several Growth Opportunities

An emerging opportunity in the market is the accelerating transition toward low-emission power generation systems and the increasing integration of renewable energy across global energy networks. While electricity demand continues to rise, a significant portion of new investments is being directed toward cleaner and more flexible generation technologies aimed at reducing carbon intensity and improving overall system efficiency. Power generation equipment, particularly high-efficiency gas turbines and renewable-compatible systems, serves as a critical bridge between conventional thermal generation and fully renewable-based power systems, enabling grid stability without compromising operational reliability. These systems are particularly valuable in regions with high renewable penetration, where flexible generation capacity is required to balance intermittent energy supply. Additionally, the growing focus on decarbonization and lifecycle cost optimization is encouraging utilities and independent power producers to invest in advanced equipment that offers long-term efficiency gains and lower emissions. The ability of modern power generation equipment to operate efficiently under variable load conditions and support hybrid power configurations further strengthens its adoption across both utility-scale and distributed power generation applications.

- For instance, in June 2025, Mitsubishi Power announced the deployment of its hydrogen-ready gas turbine technology for a large-scale power project. This deployment is aimed at enabling low-carbon fuel adoption and supporting the transition toward cleaner energy systems in utility-scale generation.

MARKET CHALLENGES

Capital Intensity and Project Execution Complexity Continue to Impact Adoption

A key challenge in the market is the high capital intensity and complexity associated with large-scale power generation projects, particularly in emerging and financially constrained markets. While advanced equipment offers significant benefits in terms of efficiency, flexibility, and emission reduction, the substantial upfront investment required for procurement, installation, and integration can limit adoption among smaller utilities and independent power producers. The benefits of high-efficiency systems are most evident in large, continuously operating power plants, but may be less pronounced in regions with fluctuating demand or underutilized capacity. Additionally, uncertainties related to regulatory policies, fuel price volatility, and long-term power demand can impact investment decisions, making it difficult for stakeholders to accurately assess project viability. Operational challenges, including extended project timelines, supply chain constraints, and the need for specialized technical expertise, further increase project risk and complexity. This combination of financial and operational uncertainties continues to influence procurement strategies and slows the adoption of advanced power generation equipment across global markets.

Segmentation Analysis

By Equipment Type

Turbines Segment Led due to Its Ability to Operate Across Diverse Power Sources

By equipment type, the market is segmented into turbines, generators, boilers, transformers, and Balance of Plant (BOP) equipment.

The turbines segment held the largest market share as they represent the primary energy conversion component in power generation systems across utility-scale power plants, industrial captive facilities, and renewable energy installations. These systems are responsible for converting thermal, mechanical, or kinetic energy into rotational energy, making them fundamental to electricity generation across thermal, hydro, wind, and gas-based power plants. Additionally, the increasing deployment of high-efficiency gas turbines and renewable-based turbines, such as wind and hydro turbines, is further strengthening their dominance in the market. The ability of turbine systems to operate across diverse power sources and support both base-load and flexible generation requirements enhances their widespread adoption across global energy infrastructure. Their critical role in improving plant efficiency, optimizing fuel utilization, and supporting energy transition initiatives continues to reinforce their leading position in the market.

- For instance, in March 2025, GE Vernova announced that its HA gas turbine technology had achieved over 3 million operating hours globally, highlighting its deployment across multiple high-efficiency combined cycle power plants to support reliable and flexible power generation.

Transformers are the fastest-growing segment and are projected to expand at a CAGR of 6.6% during the forecast period. The growth of this segment is driven by the increasing need for efficient power transmission from generation facilities to grid networks, particularly with the rising integration of renewable energy sources. As power generation becomes more decentralized and geographically dispersed, transformers play a critical role in stepping up voltage levels for long-distance transmission and ensuring stable power delivery.

To know how our report can help streamline your business, Speak to Analyst

By Power Source

Thermal Power Segment Led due to their Ability to Provide Consistent and Reliable Output

By power source, the market is segmented into thermal power, renewable power, and nuclear power.

Thermal power held the largest market share as it continues to represent the most widely deployed source of electricity generation across utility-scale power plants, industrial facilities, and captive power generation systems. This segment includes coal, natural gas, and oil-based power generation, which remain critical for ensuring base-load power supply and grid stability across both developed and emerging economies. Thermal power systems are extensively utilized due to their ability to provide consistent and reliable output, particularly in regions with high energy demand and limited renewable infrastructure.

Renewable power is the fastest-growing segment and is projected to expand at a CAGR of 7.5% during the forecast period. The growth of this segment is driven by increasing global investments in clean energy sources such as wind, solar, and hydropower, supported by government policies and decarbonization targets. As countries aim to reduce dependence on fossil fuels, there is a growing shift toward renewable energy infrastructure, driving demand for equipment such as wind turbines, hydro turbines, and associated power generation systems.

By Application

Utility Power Generation Segment Led Due to Extensive Deployment across Large-Scale Power Plants

By application, the market is segmented into utility power generation, industrial power generation, and distributed power generation.

Utility power generation held the largest power generation equipment market share, driven by its extensive deployment across large-scale power plants supplying electricity to national and regional grids. This segment includes coal, gas, nuclear, and renewable-based utility-scale generation facilities, which form the backbone of electricity supply across both developed and emerging economies. The product is widely utilized in these installations to support continuous base-load generation, high-capacity output, and grid stability, where efficiency, reliability, and long operational life are critical. The increasing demand for electricity, coupled with ongoing investments in grid expansion and large-scale renewable integration, is further driving the adoption of advanced equipment in utility applications.

Distributed power generation is the fastest-growing segment and is projected to expand at a CAGR of 7.2% during the forecast period. The growth of this segment is driven by the increasing shift toward decentralized energy systems, including captive power plants, microgrids, and on-site generation solutions across commercial and industrial End-Users. As energy reliability and resilience become critical, particularly in regions with grid instability or rising energy demand, there is growing adoption of distributed generation systems that can operate independently or alongside the main grid. Power generation equipment in this segment is typically designed for flexibility, modular deployment, and efficient operation under variable load conditions.

Power Generation Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Power Generation Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market accounted for over USD 34.66 billion in revenue in 2025, supported by strong demand for reliable electricity supply, ongoing grid modernization, and replacement of aging power generation infrastructure across the U.S., Canada, and Mexico. Regional demand is closely linked to increasing investments in natural gas-based power plants, renewable energy integration, and grid stability solutions, along with a growing focus on improving generation efficiency and reducing emissions. Utilities and independent power producers are increasingly deploying advanced power generation equipment to optimize performance in high-load and flexible generation operations, particularly in combined cycle power plants, renewable-integrated systems, and distributed energy installations.

U.S. Power Generation Equipment Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 28.54 billion by 2026, driven by its large installed power generation capacity, aging infrastructure, and continuous investments in energy transition and grid modernization projects. Unlike many regions, U.S.-based utilities place strong emphasis on improving generation efficiency, operational flexibility, and reducing lifecycle costs.

Europe

The European market is driven by a strong focus on decarbonization, renewable energy integration, and advanced power generation technologies across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for the product is closely linked to the region’s stringent environmental regulations and long-term carbon neutrality targets. Utilities and energy providers are prioritizing systems that offer higher efficiency, lower emissions, and compatibility with low-carbon fuels such as hydrogen. The increasing adoption of renewable energy sources, combined with the need for flexible backup generation, is encouraging the deployment of advanced turbines, generators, and grid-support equipment.

U.K. Power Generation Equipment Market

The U.K. market is estimated to reach around USD 4.32 billion by 2026, representing roughly 2.4% of global sales.

Germany Power Generation Equipment Market

Germany’s market is projected to reach approximately USD 6.10 billion by 2026, equivalent to around 3.4% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing market, generating revenue of USD 75.72 billion in 2025 globally. The region continues to dominate the market, driven by rapid industrialization, rising electricity demand, and large-scale investments in power generation infrastructure across key economies such as China, India, Japan, and Southeast Asian countries. The region’s growth is primarily supported by increasing government investments in energy capacity expansion, including thermal power plants, renewable energy projects, and grid modernization initiatives.

China Power Generation Equipment Market

China’s market is projected to remain the dominant one in the Asia Pacific region, with 2026 revenue estimates at around USD 37.67 billion, representing roughly 20.8% of global sales.

Japan Power Generation Equipment Market

The Japanese market in 2026 is estimated to reach around USD 7.16 billion, accounting for roughly 4.0% of the global sales.

India Power Generation Equipment Market

The Indian market by 2026 is estimated to reach around USD 14.97 billion, accounting for roughly 8.3% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in power generation infrastructure, electrification programs, and energy diversification initiatives across GCC countries, South Africa, Israel, and North Africa. Demand for the product is closely linked to the region’s focus on ensuring reliable electricity supply, improving energy efficiency, and supporting long-term economic development. Governments are prioritizing large-scale power projects, including gas-based power plants, renewable energy installations, and grid expansion initiatives, which require advanced and high-capacity generation equipment.

GCC Power Generation Equipment Market

The GCC market is projected to reach around USD 7.41 billion in 2026, representing roughly 4.1% of the global sales.

South America

The South American market is driven by increasing infrastructure development, improving road connectivity, and the gradual adoption of advanced construction equipment across key economies such as Brazil, Argentina, and Chile. Demand for the product is supported by expanding construction activities, urban development, and strong mining operations across the region. Contractors are increasingly adopting products to improve fuel efficiency and optimize performance in high-duty cycle end-users, such as excavation and material handling. The need to reduce operating costs and enhance equipment productivity is further supporting the adoption of hybrid technologies across infrastructure and mining projects.

Brazil Power Generation Equipment Market

The Brazilian market is projected to reach around USD 6.84 billion by 2026, representing roughly 3.8% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Technological Capabilities to Deliver High-Performance Power Generation Systems

The market is moderately consolidated, with competitive positioning driven by technological capabilities, operational efficiency, and the ability to deliver high-performance power generation systems across diverse End-Users such as utility-scale power plants, industrial facilities, and distributed energy systems. Leading players such as General Electric (GE Vernova), Siemens Energy AG, Mitsubishi Heavy Industries, Ltd., Wärtsilä Corporation, and Doosan Enerbility Co., Ltd. maintain strong market positions by offering advanced power generation equipment designed to improve efficiency, reduce emissions, and enhance operational flexibility across varying load conditions.

Competitive differentiation is increasingly shaped by the ability to develop high-efficiency systems equipped with advanced turbine technologies, optimized combustion systems, and digital performance monitoring solutions. As power producers focus on reducing operational costs, improving plant efficiency, and meeting decarbonization targets, market players are investing in flexible generation technologies such as hydrogen-ready gas turbines, combined cycle systems, and renewable-integrated solutions that deliver reliable performance across evolving energy systems.

- For instance, in October 2024, Siemens Energy announced advancements in its SGT-800 gas turbine platform, focusing on improving operational flexibility and supporting low-emission power generation applications, as part of its strategy to address evolving energy transition requirements.

LIST OF KEY POWER GENERATION EQUIPMENT COMPANIES PROFILED

- General Electric (GE Vernova) (U.S.)

- Siemens Energy AG (Germany)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Wärtsilä Corporation (Finland)

- Doosan Enerbility Co., Ltd. (South Korea)

- Ansaldo Energia S.p.A. (Italy)

- Harbin Electric Corporation (China)

- Dongfang Electric Corporation (China)

- Bharat Heavy Electricals Limited (BHEL) (India)

- Shanghai Electric Group Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Siemens Energy AG announced a USD 1 billion investment to expand manufacturing capacity for gas turbines and grid equipment in the U.S., aiming to address rising electricity demand and strengthen local production capabilities.

- January 2026: GE Vernova reported a significant increase in backlog to approximately USD 150 billion, driven by strong demand for power generation and electrification equipment, reflecting accelerating global investments in energy infrastructure.

- November 2025: Wärtsilä Corporation secured a contract to supply flexible engine-based power plant solutions in Latin America to support renewable energy integration and grid balancing.

- October 2025: GE Vernova reported gas power equipment backlog growth to over 60 GW, supported by strong global demand for high-efficiency turbines and power generation systems across utility-scale projects.

- September 2025: Doosan Enerbility Co., Ltd. signed an agreement to supply steam turbines and generators for a thermal power plant project in Asia, strengthening its EPC and equipment supply capabilities.

REPORT COVERAGE

The global power generation equipment market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Equipment Type, Power Source, Application, and Region |

| By Equipment Type |

|

| By Power Source |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 171.60 billion in 2025 and is projected to reach USD 290.39 billion by 2034.

In 2025, the Asia Pacific’s market value stood at USD 75.72 billion.

The market is expected to exhibit a CAGR of 6.1% during the forecast period (2026-2034).

By application, the utility power generation segment led the market.

Rising electricity demand is the key factor driving market growth.

General Electric, Siemens Energy AG, Mitsubishi Heavy Industries, Ltd., Wärtsilä Corporation, Doosan Enerbility Co., Ltd. are the top players in the market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us