Hydraulic Equipment Market Size, Share & Industry Analysis, By Component (Pumps, Valves, Cylinders, Motors, Filters and Accumulators, Transmission, and Others), By Type (Mobile and Industrial), By End User (Construction, Aerospace, Material Handling, Agriculture, Mining, Automotive, Marine, Oil and Gas, and Others), and Regional Forecast, 2026 - 2034

Hydraulic Equipment Market Size and Future Outlook

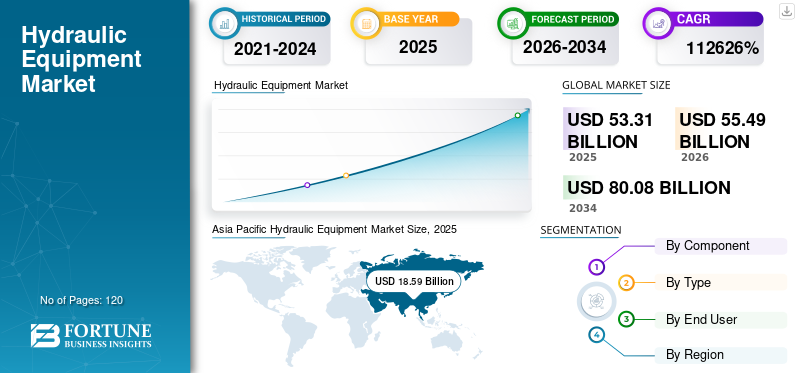

The global hydraulic equipment market size was valued at USD 53.31 billion in 2025. The market is projected to grow from USD 55.49 billion in 2026 to USD 80.08 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the hydraulic equipment market with a market share of 34.87% in 2025.

Hydraulic equipment is witnessing steady growth driven by sustained demand from construction, mining, agriculture, and industrial hydraulics, alongside ongoing upgrades of aging hydraulic systems across mature manufacturing facilities. The increasing focus on higher power density, precision control, and reliability in harsh operating environments continues to strengthen the role of hydraulic technology in applications where electric alternatives remain limited. At the same time, the integration of electro-hydraulic systems, smart pumps valves, and sensor-enabled components is enabling real time monitoring and improved asset visibility. In parallel, the rising adoption of condition monitoring, predictive maintenance, and fluid health analytics to deliver reduced downtime, lower lifecycle costs, and extended service intervals is accelerating replacement and retrofit demand across mobile equipment fleets and industrial hydraulic installations. The market growth is supported by ongoing research and development efforts by leading manufacturers.

- For instance, in February 2025, Bosch Rexroth expanded its CytroPac and smart hydraulic solutions portfolio by introducing digitally connected hydraulic power units with integrated sensors and condition monitoring capabilities, enabling real-time performance tracking and predictive maintenance for industrial and mobile hydraulic applications.

Bosch Rexroth, Parker Hannifin, Danfoss, Eaton, and HYDAC are among the key players holding a significant share of the market. Strong engineering expertise, comprehensive portfolios spanning pumps, valves, cylinders, motors, and hydraulic systems, sustained investments in energy-efficient designs and electro-hydraulic integration, and long-standing relationships with OEMs, distributors, and aftermarket customers underpin the competitive positioning of leading manufacturers globally across mobile applications.

Download Free sample to learn more about this report.

HYDRAULIC EQUIPMENT MARKET TRENDS

Rising Retrofit Demand for Legacy Hydraulic Systems across Mobile and Industrial Assets

Industrial plants and mobile equipment fleets are increasingly constrained by aging hydraulic power units, valve manifolds, and cylinder assemblies that were designed for fixed-duty cycles and limited diagnostics. A large share of installed hydraulic systems across construction, mining, metals, and process industries is operating beyond original design life, creating performance losses, higher leakage risk, and unplanned downtime. As full system replacement is often cost-prohibitive, end users are prioritizing targeted hydraulic retrofits, including cartridge valve upgrades, energy-efficient pump replacements, and sensor-integrated components that can be deployed without major system redesign. This shift is driving the demand for hydraulics solutions that support drop-in compatibility, extended service intervals, and incremental efficiency gains in brownfield environments.

- For example, in 2024, Bosch Rexroth expanded its hydraulic retrofit and service solutions portfolio, introducing upgrade kits and replacement components designed to improve efficiency and reliability of existing hydraulic systems without requiring full equipment replacement.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Infrastructure, Mining, and Heavy Industrial Projects to Increase Demand for High-Load Equipment

The expansion of infrastructure development, mining operations, and heavy industrial projects is a key factor driving hydraulic equipment market growth. Large-scale construction, metals processing, energy generation, and resource extraction activities increasingly rely on hydraulics for applications requiring high force density, durability, and reliable performance under extreme operating conditions. Rising equipment sizes, higher duty cycles, and stricter uptime requirements are increasing hydraulic content per machine, sustaining the demand for high-pressure pumps, heavy-duty cylinders, advanced valve systems, and integrated hydraulic power units. In parallel, replacement demand from aging equipment fleets and capacity expansion across emerging industrial regions is reinforcing steady equipment consumption across both mobile and stationary applications.

- For instance, in 2024, Caterpillar and its hydraulic system suppliers expanded hydraulic component sourcing to support increased production of large mining trucks and excavators, driven by rising global mining investment and demand for high-capacity earthmoving equipment.

MARKET RESTRAINTS

High Initial Capital Cost and System Integration Challenges to Limit Hydraulic Upgrades

Hydraulic equipment upgrades often require significant upfront investment due to the cost of high-pressure pumps, precision valves, custom manifolds, and heavy-duty cylinders, along with system redesign and commissioning requirements. In many industrial and mobile applications, integrating new hydraulic components into existing equipment platforms involves modifications to piping layouts, mounting structures, control interfaces, and safety systems, increasing total project cost and downtime risk. For small and mid-sized operators, particularly in cost-sensitive sectors such as regional construction, agriculture, and contract manufacturing, these capital and integration challenges can delay hydraulic system modernization.

MARKET OPPORTUNITIES

Rising Replacement and Retrofit Demand across Aging Equipment Fleets to Create New Growth Opportunities

The product demand is increasingly expanding beyond new machine production for replacement and retrofit projects across aging construction, mining, agricultural, and industrial equipment fleets. Many installed hydraulic systems operate under harsh conditions and face performance degradation, leakage losses, and rising maintenance costs over time, prompting end users to prioritize selective component replacement rather than full system overhaul. This trend is creating opportunities for manufacturers offering drop-in pumps, cartridge valves, standardized cylinders, and modular power units that can be integrated into existing machines with minimal redesign. The growing emphasis on extending equipment life, improving energy efficiency, and reducing unplanned downtime is supporting steady aftermarket and retrofit-driven growth across both mature and emerging markets.

- For instance, Domin’s hydraulic valve retrofit solutions are depicting industry attention in early 2026 for enabling the modernization of legacy hydraulic platforms with next-generation control precision and diagnostic capabilities. These solutions are helping operators enhance performance without extensive redesign or downtime.

MARKET CHALLENGES

Energy Efficiency Losses and Leakage Management to Limit Hydraulic System Optimization

Energy inefficiency remains a persistent challenge in the market due to inherent losses associated with fluid compression, throttling, heat generation, and leakage across system components. In many industrial and mobile applications, legacy hydraulic systems operate at partial load conditions for extended periods, leading to excessive energy consumption and thermal stress. Leakage from hoses, seals, and fittings further reduces system efficiency while increasing maintenance frequency and environmental risk. Addressing these inefficiencies often requires system redesign, component upgrades, or the adoption of variable-speed drives and load-sensing architectures, which can be complex and capital intensive. As energy costs rise and sustainability targets tighten, the difficulty of balancing hydraulic performance with efficiency improvement continues to challenge end users and equipment manufacturers.

Segmentation Analysis

By Component

High Load, Pressure, and Continuous-Duty Requirements to Drive Dominance of Hydraulic Pumps

Based on component, the market is segmented into pumps, valves, cylinders, motors, filters and accumulators, transmission, and others.

The pumps segment accounts for the largest share of the global market due to their critical role in generating flow and pressure across both mobile and industrial hydraulic systems, as well as their comparatively higher value per installation. Pump demand is particularly strong in construction equipment, mining machinery, agricultural equipment, and industrial presses, where rising machine size, higher operating pressures, and continuous-duty cycles significantly increase pump capacity requirements. The widespread use of variable displacement and load-sensing pumps to improve energy efficiency and system responsiveness further reinforces pump dominance, especially in high-horsepower and heavy-duty applications.

Hydraulic cylinders continue to witness substantial adoption and the segment is poised to expand at a CAGR of 5.0% over the forecast period, owing to their extensive use in load lifting, positioning, and force transmission across earthmoving equipment, material handling systems, mining operations, and industrial machinery. Increasing payload capacities, longer stroke lengths, and harsher operating environments are driving the demand for heavy-duty and application-specific cylinder designs. High wear rates in demanding operating conditions also support steady aftermarket demand for cylinder replacement and refurbishment.

- For instance, in 2024, Bosch Rexroth highlighted sustained demand growth for high-pressure hydraulic pumps and heavy-duty cylinders driven by infrastructure, mining, and mobile equipment applications, particularly in large-scale and continuous-operation environments.

The hydraulic valves segment is projected to witness strong growth due to increasing system complexity and rising demand for precise flow control, pressure regulation, and operational safety. The rising adoption of cartridge valves, proportional valves, and modular valve manifolds is enabling more compact system layouts, improved controllability, and simplified maintenance, supporting valve demand across both new equipment production and hydraulic system upgrades.

To know how our report can help streamline your business, Speak to Analyst

By Type

High Equipment Utilization to Drive the Dominance of the Mobile Hydraulics Segment

Based on type, the market is segmented into mobile and industrial.

The mobile segment accounts for the largest share of the global market due to the extensive use of hydraulic systems in construction equipment, agricultural machinery, mining vehicles, and material handling equipment. Mobile hydraulics rely heavily on pumps, valves, cylinders, and motors to deliver high force density, operational flexibility, and durability in dynamic and harsh outdoor environments. Increasing infrastructure development, mechanization of agriculture, and expansion of mining activities continue to drive strong demand for mobile hydraulic systems. Higher machine capacities, elevated operating pressures, and greater equipment complexity further increase hydraulic component value per unit, reinforcing the dominance of the mobile segment.

The industrial segment is projected to witness steady growth, registering a CAGR of approximately 4.4% over the forecast period. The expansion is driven by sustained demand from manufacturing facilities, process industries, metal processing, power generation, and material handling systems. Industrial hydraulics are widely used in presses, injection molding machines, machine tools, and heavy industrial equipment where precision, reliability, and continuous-duty performance are essential. The ongoing modernization of aging hydraulic installations, efficiency improvement initiatives, and replacement demand across brownfield industrial facilities are supporting stable growth in the industrial segment over the forecast period.

By End User

Extensive Equipment Deployment to Drive the Dominance of Construction Segment

Based on end user, the market is segmented into construction, aerospace, material handling, agriculture, mining, automotive, marine, oil and gas, and others.

The construction segment accounts for the largest hydraulic equipment market share due to the extensive deployment of hydraulic systems in excavators, loaders, bulldozers, cranes, and other heavy machinery. Construction equipment relies heavily on hydraulic pumps, cylinders, and valves to enable lifting, digging, positioning, and load-bearing operations under high-pressure and continuous-duty conditions. Rising infrastructure development, urbanization projects, and public capital expenditure across emerging and developed economies continue to support strong equipment demand in this segment. Larger equipment sizes and higher operating capacities further increase hydraulic component value per machine, reinforcing the construction segment’s dominance.

The aerospace segment is projected to witness the fastest growth, registering a CAGR of approximately 6.0% over the analysis period. The segment growth is driven by increasing aircraft production, fleet modernization, and demand for advanced flight control and landing gear systems. Hydraulic systems remain critical in aerospace applications for actuation, braking, thrust reversers, and control surface movement, where precision, reliability, and weight optimization are essential. Expanding commercial aircraft backlogs, defense modernization programs, and growing maintenance, repair, and overhaul (MRO) activities are supporting the accelerated equipment adoption within the aerospace industry.

Material handling, mining, agriculture, automotive, marine, and oil and gas industries continue to generate steady demand, supported by equipment replacement cycles, industrial expansion, and rising mechanization levels across global markets.

Hydraulic Equipment Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Hydraulic Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific remains the fastest-growing and dominant market, generating a revenue of USD 18.59 billion in 2025 globally. The market growth is driven by the high concentration of construction activity, manufacturing capacity, automotive production, and heavy industrial operations across China, Japan, South Korea, India, Taiwan, and ASEAN countries. The rapid expansion of infrastructure development, mining, automotive manufacturing, and industrial machinery production is driving the large-scale demand for hydraulic pumps, valves, cylinders, motors, and power units. In addition, government-led investments in infrastructure expansion, industrial self-sufficiency, and domestic equipment manufacturing continue to reinforce Asia Pacific’s leadership in global equipment consumption.

China Hydraulic Equipment Market

The China market is projected to remain dominant in the Asia Pacific region, with 2026 revenues estimated to reach around USD 8.21 billion, representing roughly 14.8% of global sales.

Japan Hydraulic Equipment Market

The Japan market is estimated to touch around USD 2.55 billion in 2026, accounting for roughly 4.6% of the global market.

India Hydraulic Equipment Market

The India market is estimated to reach a value of around USD 2.88 billion in 2026, accounting for roughly 5.2% of global revenues.

North America

The North America market accounted for a revenue of over USD 13.09 billion revenue in 2025, supported by strong demand from construction, mining, agriculture, and industrial manufacturing sectors. The region benefits from a large installed base of mobile and industrial equipment, high equipment utilization rates, and well-established aftermarket and service networks. Ongoing infrastructure investment, mining activity, and replacement demand from aging machinery fleets are sustaining hydraulic equipment consumption across the U.S., Canada, and Mexico. In addition, stricter safety, reliability, and performance standards, combined with continued modernization of legacy hydraulic systems in brownfield facilities, are supporting steady demand for pumps, valves, cylinders, and hydraulic power units across North America.

U.S. Hydraulic Equipment Market

The U.S. is likely to dominate the North American market with a revenue of about USD 11.39 billion in 2026, driven by its large installed base of construction machinery, industrial equipment, agricultural machinery, and material handling systems. Strong demand from infrastructure development, mining activity, automotive manufacturing, and industrial processing supports market leadership. The presence of major OEMs, extensive aftermarket and service networks, and advanced manufacturing capabilities further strengthen domestic demand. In addition, ongoing replacement of aging hydraulic systems in brownfield industrial facilities, along with stringent safety, reliability, and performance standards, continue to drive the adoption of high-pressure pumps, precision valves, heavy-duty cylinders, and integrated hydraulic systems across the U.S.

Europe

The European market is supported by strong demand from automotive manufacturing, industrial machinery, construction equipment, renewable energy projects, and process industries. The region’s emphasis on energy efficiency, emissions reduction, and compliance with stringent safety and environmental regulations is driving upgrades of hydraulic systems toward more efficient pumps, valves, and integrated solutions. Ongoing investments in industrial modernization, electrification of mobile equipment, and advanced manufacturing across countries such as Germany, France, Italy, and the Netherlands are further contributing to steady demand for both mobile and industrial equipment across Europe.

U.K. Hydraulic Equipment Market

The U.K. market is estimated to reach around USD 1.40 billion in 2026, representing roughly 2.5% of global revenues.

Germany Hydraulic Equipment Market

The Germany market is projected to reach approximately USD 3.29 billion in 2026, equivalent to around 5.9% of global product sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing industrialization and government-led initiatives aimed at diversifying economies beyond oil and gas. Rising investments in infrastructure development, power generation, water & wastewater treatment, mining, and heavy industrial projects are supporting steady product demand across the region. In addition, large-scale construction programs, energy transition projects, and ongoing modernization of industrial assets are creating new opportunities for hydraulic pumps, valves, cylinders, and power units, particularly across GCC countries and South Africa. In these countries, hydraulics remains critical for high-load and continuous-duty applications.

GCC Hydraulic Equipment Market

The GCC market is projected to reach around USD 2.10 billion in 2026, representing roughly 3.8% of the global market.

South America

The South America market is supported by rising investments in infrastructure development, mining activity, energy projects, and gradual modernization of industrial assets, particularly in countries such as Brazil and Argentina. While large-scale advanced manufacturing remains limited, steady demand from mining, oil & gas, agriculture, and construction equipment is sustaining equipment consumption across the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on Application Engineering and Innovation to Enhance Market Footing

The hydraulic equipment market is moderately consolidated, characterized by the presence of a limited number of global manufacturers offering broad portfolios spanning pumps, valves, cylinders, motors, filtration systems, and integrated hydraulic solutions. Key players such as Bosch Rexroth, Parker Hannifin, Danfoss, Eaton, and HYDAC are focusing on continuous product innovation and application engineering to strengthen their competitive positions. Product development efforts are increasingly centered on improving energy efficiency, power density, durability, and compatibility with diverse mobile and industrial operating environments.

Leading manufacturers are also enhancing their competitive advantage through expanded aftermarket and lifecycle service offerings, including refurbishment programs, replacement kits, condition monitoring services, and long-term maintenance support. Companies are entering strategic collaborations with OEMs, distributors, and end users to secure long-term supply positions across construction, mining, agriculture, industrial machinery, and energy sectors.

- For instance, in 2024, companies such as Bosch Rexroth and Danfoss highlighted increased strategic focus on energy-efficient hydraulic systems, modular component platforms, and expanded aftermarket services to support the modernization of installed equipment fleets and long-term customer retention.

LIST OF KEY HYDRAULIC EQUIPMENT COMPANIES PROFILED

- Parker Hannifin Corp. (U.S.)

- Eaton Corporation (Ireland)

- Bosch Rexroth (Germany)

- Danfoss (Denmark)

- HYDAC International GmbH (Germany)

- Bucher Industries (Switzerland)

- Moog Inc. (U.S.)

- KYB Corporation (Japan)

- Kawasaki Precision Machinery (Japan)

- HAWE Hydraulik (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Bosch Rexroth highlighted expanded investment in energy-efficient and compact hydraulic systems in its 2024 company disclosures, focusing on high-pressure pumps, integrated hydraulic power units, and modular valve platforms to support infrastructure, mining, and mobile equipment applications.

- March 2024: Danfoss Power Solutions announced continued capacity expansion and portfolio focus on mobile hydraulics, emphasizing pumps, motors, and electro-hydraulic solutions for construction, agriculture, and off-highway equipment as part of its 2024 strategic growth roadmap.

- February 2024: Parker Hannifin reinforced its focus on hydraulics and fluid power systems through ongoing investments in hydraulic component manufacturing and aftermarket services, targeting replacement demand and lifecycle support across industrial and mobile equipment markets, as outlined in its fiscal 2024 investor communications.

- January 2024: Bucher Hydraulics announced the continued expansion of its manufacturing capabilities and modular hydraulic system solutions to strengthen its position in mobile and industrial hydraulics, supporting OEM demand across Europe and North America.

- November 2023: Eaton reported increased demand for hydraulic components used in construction, material handling, and industrial machinery, highlighting continued product development around energy-efficient hydraulic systems and ruggedized components in its industrial segment updates.

REPORT COVERAGE

The global market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Type, End User, and Region |

| By Component |

|

| By Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 53.31 billion in 2025 and is projected to reach USD 80.08 billion by 2034.

In 2025, the North America market value stood at USD 13.09 billion.

The market is expected to exhibit a CAGR of 4.7% during the forecast period.

By end use industry, the construction segment dominates the market.

Expanding infrastructure investment, mining output growth, equipment mechanization, and rising replacement demand across aging mobile and industrial hydraulic systems are key factors driving the market.

Parker Hannifin, Eaton Corp., Bosch Rexroth, Danfoss, HYDAC, and Bucher Industries are the major players in the global market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us