Precision Oncology Market Size, Share & Industry Analysis, By Type (Diagnostics {Companion Diagnostics, Comprehensive Genomic Profiling, Liquid Biopsy Assays, Single Biomarker Tests, and Others} and Therapeutics {Targeted Therapies, Biomarker-Guided Immunotherapies, and Others}), By Cancer Type (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Melanoma, Hematologic Malignancies, and Others), By End User (Hospitals & Cancer Centres, Diagnostic Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, and Others), and Regional Forecast, 2026-2034

Precision Oncology Market Size and Future Outlook

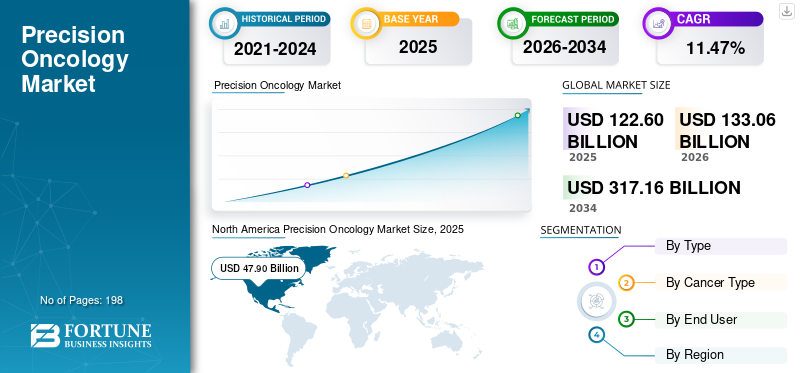

The global precision oncology market size was valued at USD 122.60 billion in 2025. The market is projected to grow from USD 133.06 billion in 2026 to USD 317.16 billion by 2034, exhibiting a CAGR of 11.47% during the forecast period. North America dominated the precision oncology market with a market share of 39.07% in 2025.

Precision oncology includes cancer diagnostics and therapies guided by biomarkers that align patients with more tailored treatment options based on tumor genetics, protein expression, and other significant molecular traits. The market is growing due to the escalating global cancer burden, the rising application of companion diagnostics and next-generation sequencing for treatment decisions, and the increasing accessibility of targeted therapies and biomarker-driven immunotherapies for key cancer types, including lung, breast, colorectal, prostate, melanoma, and blood cancers. The market is also gaining from wider use of comprehensive genomic profiling, liquid biopsy, and decisions directed by molecular tumor boards, as healthcare systems aim to enhance treatment accuracy, clinical results, and resource efficiency in cancer care.

Major participants in the global market include F. Hoffmann-La Roche Ltd, Guardant Health, Inc., TEMPUS, Caris Life Sciences, Illumina Inc., and others. These companies are focusing on companion diagnostics, comprehensive genomic profiling, liquid biopsy platforms, targeted oncology drugs, and biomarker-guided immunotherapies to strengthen their position in precision cancer care.

Download Free sample to learn more about this report.

Precision Oncology Market Key Takeaways

- 2025 Market Size: USD 122.60 billion

- 2026 Market Size: USD 133.06 billion

- 2034 Forecast Market Size: USD 317.16 billion

- CAGR: 11.47% from 2026–2034

- North America dominated the precision oncology market with a 39.07% share in 2025.

- The diagnostics segment is anticipated to grow at a CAGR of 13.95% during the forecast period.

- The hematologic malignancies segment is projected to expand at a CAGR of 12.15% during the forecast period.

North America

North America led the global market with a valuation of USD 47.90 billion in 2025.

Europe

Europe is expected to grow at a CAGR of 9.82% during the forecast period.

Asia Pacific

Asia Pacific is projected to reach a market value of USD 35.30 billion by 2026.

U.S.

The market is projected to reach approximately USD 47.56 billion by 2026.

Japan

The market is estimated at around USD 7.24 billion in 2026, accounting for roughly 5.4% of global revenue.

Read More

PRECISION ONCOLOGY MARKET TRENDS

Increasing Use of Genomics and Biomarker-Based Diagnostics is a Significant Market Trend

The rising adoption of genomics and biomarker-driven diagnostics is a key trend in the market. Precision oncology is progressively shifting from single-marker assessments to more extensive genomic and biomarker profiling since clinicians require comprehensive molecular data to align patients with targeted treatments, biomarker-driven immunotherapies, and pertinent clinical studies. Companion diagnostics continue to play a crucial role in treatment selection, as the FDA classifies them as tests that deliver information vital for the safe and effective administration of specific drugs or biologics. Simultaneously, increased utilization of next-generation sequencing, liquid biopsy, and multi-omic profiling is aiding providers in quicker identification of actionable changes in a more non-invasive manner, thereby promoting wider clinical adoption. This trend is bolstering the demand in the market for complete genomic profiling platforms, biomarker-testing services, and cohesive diagnostic workflows throughout hospitals, cancer centers, and specialized laboratories. Additionally, it is prompting companies to broaden distributed testing approaches, allowing greater patient access to precision-oncology diagnostics outside of just a limited number of specialized centers. These factors are supporting the overall global precision oncology market growth.

- For instance, in March 2026, Illumina and Labcorp’s expanded collaboration aims to broaden access to precision oncology testing through next-generation sequencing, including new distributed test offerings and efforts to improve cancer biomarker testing access across the healthcare ecosystem.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Targeted Therapies and Immunotherapy is Driving Market Growth

Increasing use of targeted treatments and immunotherapy is a major factor driving the market. With the classification of more cancers based on actionable mutations, receptor expression, and immune biomarkers, the selection of treatments is progressively shifting toward therapies customized for an individual’s specific tumor biology. This expands the commercial application of targeted therapies for conditions such as EGFR-mutated lung cancer, HER2-positive cancers, BRCA-driven tumors, and blood cancers, while also enhancing the significance of biomarker-guided immunotherapy in solid tumors and hematologic malignancies. The trend is enhancing the need for companion diagnostics, molecular profiling, and biomarker testing, as these tools are crucial for identifying suitable patients and boosting treatment response. It is likewise boosting market value, as these therapies generally involve greater per-patient treatment expenses than traditional chemotherapy and continue to play a crucial role in long-term oncology treatment strategies. With the ongoing expansion of clinical guidelines and approvals, an increasing number of patients are being directed toward precision-oncology care models, directly fostering the global market growth.

- For instance, in February 2026, Johnson & Johnson announced the U.S. FDA approval for RYBREVANT FASPRO, positioning it as the only EGFR-targeted therapy that can be administered once a month for EGFR-positive non-small cell lung cancer.

MARKET RESTRAINTS

Rising High Cost and Reimbursement Uncertainty to Limit Market Growth

The significant expense and uncertainty regarding reimbursement are key market limitations in precision oncology. Precision-oncology treatment frequently necessitates costly genomic tests, companion diagnostics, liquid biopsies, and expensive targeted therapies, elevating the overall financial strain on providers, payers, and patients. This presents a greater challenge when reimbursement is postponed, inadequate, or inconsistent, as clinicians might be reluctant to request advanced tests if coverage is uncertain. The issue is particularly significant in less mature markets, where funding for biomarker testing and precision therapies is still not consistent. ASCO’s 2025 worldwide view on precision oncology emphasizes economic, administrative, and health-policy obstacles as key factors preventing the advantages of precision oncology from being available to broader patient groups. Consequently, even when clinically significant biomarkers and treatments exist, real market uptake may lag behind expectations due to misalignment in affordability and payment options. This directly limits demand for both precision diagnostics and therapies guided by biomarkers, hindering broader market growth.

MARKET OPPORTUNITIES

Expansion of Precision Medicine Initiatives Globally to Offer Market Growth Opportunities

Expansion of precision medicine initiatives globally is a strong market opportunity in precision oncology. As governments, health systems, research networks, and industry groups invest more in genomics infrastructure, cancer data platforms, and biomarker-guided care pathways, the market is gaining a broader foundation for long-term growth. These initiatives improve access to molecular testing, strengthen integration of genomic data into routine oncology practice, and help identify more patients who are eligible for targeted therapies and biomarker-guided immunotherapies. They also support multi-country research collaboration, evidence generation, and standardization of precision-oncology workflows, which can accelerate adoption across both mature and emerging markets. As a result, companies active in diagnostics, liquid biopsy, CGP, and precision therapeutics gain new opportunities to expand geographically and clinically. This trend is especially important in regions where precision oncology is still underpenetrated, because national and cross-border initiatives can reduce infrastructure and access gaps. All these factors would drive the market growth in the coming years.

- For instance, in February 2026, the PreciseOnco research consortium award was announced by Philips, where the consortium received a USD 17.4 million Innovative Health Initiative grant to advance precision cancer treatment through large-scale collaboration in imaging, pathology, genomics, and AI-enabled clinical decision support.

MARKET CHALLENGES

Clinical and Operational Complexity Pose a Prominent Challenge to Market Growth

Clinical and operational intricacy pose a significant challenge in the precision oncology market. Precision-oncology processes are more challenging than traditional oncology routes due to their reliance on prompt biopsy collection, sufficient tissue quality, appropriate test selection, lab coordination, molecular interpretation, and alignment of findings with treatment choices. In various practical scenarios, delays may happen at numerous stages, such as specimen gathering, sample transportation, testing response time, and report analysis. The challenge intensifies as testing shifts from single-marker assays to extensive genomic profiling, since a higher number of biomarkers, greater data outputs, and more intricate treatment pathways place additional demands on pathology labs and oncology teams. Restricted tissue availability, particularly in small or difficult-to-reach tumors, complicates thorough testing and may necessitate repeated sampling or different procedures. Consequently, clinical and operational intricacies may hinder adoption, postpone treatment start times, and raise implementation expenses for providers. In general, while precision oncology provides distinct clinical benefits, the challenges of workflow burden and execution complexity are significant obstacles to better market growth.

Precision Oncology Market Segmentation Analysis

By Type

Therapeutics Segment Dominated the Market Due to Expanding Biomarker-Driven Treatment Use

In terms of type, the market is bifurcated into diagnostics and therapeutics. The diagnostics is further segmented into companion diagnostics, comprehensive genomic profiling, liquid biopsy assays, single biomarker tests, and others. The therapeutics segment is divided into targeted therapies, biomarker-guided immunotherapies, and others.

The therapeutics segment held the largest global precision oncology market share in 2025. This is due to precision-oncology medications producing much greater revenue per patient compared to diagnostic tests and continuing to be the primary source of commercial value in the market. Their supremacy is further bolstered by the increasing application of targeted therapies and biomarker-driven immunotherapies in major cancer categories such as lung, breast, and blood cancers. With the increasing identification of patients via genomic and biomarker testing, the pool of patients qualified for high-value precision treatments is growing, thereby enhancing therapeutic sales even more. Furthermore, ongoing treatment cycles, high pricing, and expanded indications in biomarker-defined cancers persist in reinforcing the segment’s dominant position.

- For instance, in June 2025, Roche announced that the European Commission approved Itovebi (inavolisib) in combination with palbociclib and fulvestrant for patients with PIK3CA-mutated, ER-positive, HER2-negative advanced breast cancer.

The diagnostics segment is anticipated to rise with a CAGR of 13.95% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Cancer Type

Lung Cancer Dominated the Market Due to Strong Biomarker-Driven Treatment Use

Based on cancer type, the market is classified into breast cancer, lung cancer, colorectal cancer, prostate cancer, melanoma, hematologic malignancies, and others.

The lung cancer segment captured the largest revenue share in the global market in 2025. This is because lung cancer has one of the most advanced precision-treatment pathways, with routine use of biomarker testing for mutations such as EGFR, ALK, ROS1, BRAF, MET, RET, KRAS, and others before treatment selection. The segment also benefits from a large global patient pool and the wide availability of targeted therapies and biomarker-guided immunotherapies across different lines of treatment. In addition, lung cancer patients often require repeated molecular testing during disease progression, which further increases the use of companion diagnostics, genomic profiling, and liquid biopsy assays. As more biomarker-defined therapies enter the market, the commercial value of lung cancer remains higher than most other cancer segments, which continues to support its leading position in precision oncology. Furthermore, the segment is set to hold 25.7% share in 2026.

- For instance, in February 2026, Johnson & Johnson announced that the U.S. FDA approved RYBREVANT FASPRO as the only EGFR-targeted therapy that can be administered once a month for certain patients with EGFR-positive non-small cell lung cancer.

The hematologic malignancies segment is anticipated to rise with a CAGR of 12.15% over the forecast period.

By End User

Hospitals & Cancer Centres Dominated the Market Due to their Central Role in Precision Cancer Diagnosis and Treatment Delivery

Based on end user, the market is segmented into hospitals & cancer centres, diagnostic laboratories, academic & research institutes, pharmaceutical & biotechnology companies, and others.

The hospitals & cancer centres segment dominated the market share in 2025. This is due to the fact that these settings oversee the entire patient journey, encompassing biopsy collection, biomarker testing choices, treatment selection, drug delivery, and follow-up care. They also manage a significant portion of high-value targeted treatments and biomarker-guided immunotherapies, resulting in the largest revenue contribution in the market. Moreover, multidisciplinary tumor boards, oncology experts, and combined pathology and imaging assistance are increasingly accessible in hospitals and cancer centers, facilitating the broader application of precision oncology treatment. Their leadership is additionally bolstered by the increasing number of cancer centers implementing genomic testing initiatives and organized molecular-guided treatment processes. Furthermore, the segment is set to hold 53.2% share in 2026.

- For instance, in November 2024, LGM Pharma announced the expansion of its analytical testing services with endotoxin and rapid sterility testing capabilities, stating that these services are essential for pharmaceutical companies developing sterile and injectable products.

In addition, diagnostic laboratories are projected to witness 13.00% growth rate during the forecast period.

Precision Oncology Market Regional Outlook

By region, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Precision Oncology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market attained USD 44.64 billion in 2024 and led the global market. In 2025, the regional market maintained its leading position, with USD 47.90 billion. The regional growth is mainly driven by the region’s strong biomarker-testing ecosystem, high adoption of companion diagnostics, broad access to targeted therapies and biomarker-guided immunotherapies, and early incorporation of molecular testing into routine oncology care.

U.S. Precision Oncology Market

The U.S. market led the North American region and is projected to be approximately USD 47.56 billion by 2026, representing about 35.7% of the global revenue.

Europe

The European market size is expected to grow at a 9.82% CAGR during the forecast period. European growth is supported by expanding precision-oncology guidelines, increasing use of actionable genomic profiling, and wider integration of biomarker testing into treatment pathways.

U.K. Precision Oncology Market

The U.K. market in 2026 is estimated at around USD 7.10 billion, representing roughly 5.3% of global revenues.

Germany Precision Oncology Market

Germany's market size is projected to reach approximately USD 7.39 billion in 2026, equivalent to around 6.0% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 35.30 billion by 2026. The regional growth is driven by the region’s large cancer burden, rising healthcare investment, expanding NGS capacity, and improving awareness of biomarker-led treatment selection.

Japan Precision Oncology Market

The Japanese market in 2026 is estimated at around USD 7.24 billion, accounting for roughly 5.4% of global revenues.

China Precision Oncology Market

China’s market is projected to reach revenues of around USD 9.39 billion in 2026, representing roughly 7.1% of global sales.

India Precision Oncology Market

The Indian market in 2026 is estimated at around USD 3.81 billion, accounting for roughly 2.9% of global revenues.

Latin America and the Middle East & Africa

The growth in the Latin America and Middle East & Africa regions is anticipated to be slower over the forecast period. The growth of the market is driven by increasing recognition of the clinical value of precision oncology, efforts to improve biomarker testing access, and broader calls for implementation across health systems. The Latin America market in 2026 is estimated at around USD 6.02 billion.

In the Middle East and Africa region, the GCC market is projected to reach approximately USD 2.77 billion by 2026, representing about 2.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on Integrated Diagnostics, Biomarker Partnerships, and Precision Therapy Expansion to Strengthen Market Position

The global precision oncology market is moderately concentrated, with major companies such as F. Hoffmann-La Roche Ltd, Guardant Health, Inc., TEMPUS, Caris Life Sciences, and Illumina Inc. accounting for a significant share of the market. These firms are focusing on companion diagnostics, comprehensive genomic profiling, liquid biopsy, targeted therapies, and biomarker-guided immunotherapies to strengthen their competitive position.

- For instance, in January 2026, Guardant Health announced a multi-year strategic collaboration with Merck to develop companion diagnostics and support the commercialization of new cancer therapies using the Guardant Infinity Smart platform.

Other significant participants include QIAGEN, AstraZeneca, Novartis AG, Bristol Myers Squibb Company, and Others. These companies are expected to prioritize new product innovation, portfolio expansion, and stronger support for regulated quality control environments to improve their competitive positions over the forecast period.

LIST OF KEY PRECISION ONCOLOGY COMPANIES PROFILED

- Hoffmann-La Roche Ltd (Switzerland)

- Guardant Health, Inc. (U.S.)

- TEMPUS (U.S.)

- Caris Life Sciences. (U.S.)

- Illumina Inc. (U.S.)

- QIAGEN (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- AstraZeneca (U.S.)

- Novartis AG (Switzerland)

- Myriad Genetics, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Tempus announced a strategic collaboration with Daiichi Sankyo to advance AI-driven biomarker discovery and clinical differentiation across an ADC oncology program.

- January 2026: Illumina announced that CMS reimbursement was granted for its FDA-approved TruSight Oncology Comprehensive test, which expands access to comprehensive genomic profiling and supports wider use of precision-oncology testing in clinical practice.

- November 2025: Novartis opened a new radioligand therapy manufacturing facility in California as part of its U.S. expansion plan, aimed at meeting future demand and strengthening supply reliability for precision radioligand oncology therapies.

- June 2025: QIAGEN announced two strategic partnerships to expand its minimal residual disease (MRD) testing portfolio in oncology, including work on blood-based MRD tests for solid tumors and kit development for lymphoma assays to support pharma co-development and companion diagnostics.

- January 2025: Foundation Medicine announced that the U.S. FDA has approved FoundationOne CDx as a companion diagnostic for OJEMDA (tovorafenib) in relapsed or refractory BRAF-altered pediatric low-grade glioma, marking a new pediatric precision-oncology CDx indication.

REPORT COVERAGE

The global precision oncology market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.47% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Cancer Type, End User, and Region |

| By Type |

|

| By Cancer Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 122.60 billion in 2025 and is projected to reach USD 317.16 billion by 2034.

In 2025, the market value stood at USD 47.90 billion.

The market is expected to exhibit a CAGR of 11.47% during the forecast period.

By type, the therapeutics segment is expected to lead the market.

Growing demand for targeted therapies and immunotherapies, along with increasing prevalence of cancer, are primarily driving market expansion.

F. Hoffmann-La Roche Ltd, Guardant Health, Inc., TEMPUS, Caris Life Sciences, and Illumina Inc. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us