PU Films Market Size, Share & Industry Analysis, By Form (Monolayer PU Films, Multilayer PU Films, PU Laminates, and Others), By Application (Surface Protection Films, Technical Membrane Films, Medical & Hygiene Films, and Others), By End-Use Industry (Automotive & Transportation, Medical & Healthcare, Textiles, Outdoor & Footwear, Electronics & Consumer, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

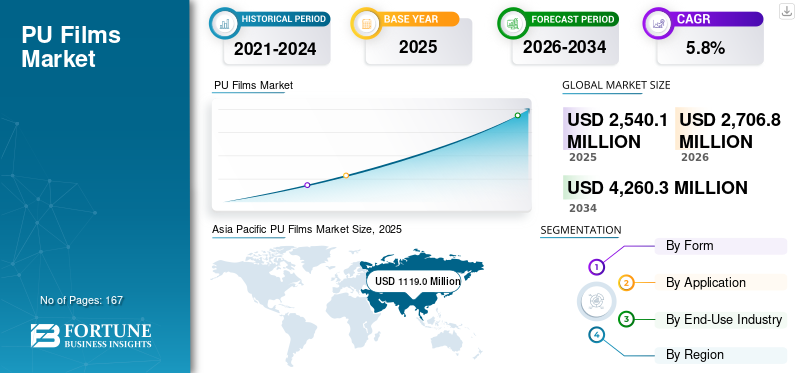

The global PU Films market size was valued at USD 2,540.1 million in 2025. The market is projected to grow from USD 2,706.8 million in 2026 to USD 4,260.3 million by 2034, exhibiting a CAGR of 5.8% during the forecast period. Asia Pacific dominated the global PU Films market with a market share of 44.1% in 2025.

Polyurethane films are engineered performance materials designed to deliver flexibility, durability and barrier protection across a wide range of industrial and consumer applications. Their ability to provide abrasion resistance, elasticity, transparency and chemical stability makes them essential in transportation and automotive industry, medical and hygiene products, electronics and surface protection applications where traditional PVC or PE films no longer meet modern performance expectations. As manufacturers push for lighter components, improved comfort and longer product lifecycles, PU films offer the processing versatility and material reliability required for next-generation product designs.

The market is shaped by leading specialty material producers with strong capabilities in TPU chemistry, film extrusion and multilayer laminate technologies. Key players include Covestro, BASF, Lubrizol, SWM International and Avery Dennison. Their portfolios span medical and hygiene films, breathable membranes, paint protection films and high-clarity surface protection solutions that support evolving performance and regulatory requirements across multiple industries. Close collaboration with OEMs and continued investment in solvent-free processing, recyclable TPU grades and advanced protective films reinforce their influence as they gain wider adoption in high-value applications.

Download Free sample to learn more about this report.

PU FILMS MARKET TRENDS

Rising Adoption of Solvent-Free and Low-VOC TPU Film Technologies is an Emerging Market Trend

Producers are accelerating the shift toward solvent-free extrusion, water-based adhesive systems and recyclable TPU film solutions. These advances reduce emissions, enhance workplace safety and align with global sustainability commitments. In textiles and electronics, TPU films are increasingly selected for their clarity, durability, and compatibility with low-VOC manufacturing processes, reflecting broader environmental and performance priorities across end-use industries.

- PU membranes are widely used in breathable waterproof garments that undergo testing under ISO 11092 for thermal and moisture-vapor resistance, highlighting the material’s established role in performance apparel systems.

MARKET DYNAMICS

MARKET DRIVERS

Growing Need for Lightweight and High-Performance Materials Strengthens PU Film Adoption

Industries such as automotive, medical, electronics, and technical textiles are steadily increasing the use as they deliver flexibility, durability and barrier protection that outperform conventional PVC and PE films. Their ability to combine softness with mechanical strength makes them essential for next-generation designs that demand comfort, efficiency and long service life. As OEMs push for lighter components and more advanced functionality, PU films continue to displace traditional films in premium and performance-critical applications.

- The European Commission’s CO2 reduction targets for new passenger vehicles encourage automakers to reduce vehicle mass, which upsurges the use of lightweight polymer materials, including PU films, in interior and protective components.

MARKET RESTRAINTS

Higher Material Costs and Processing Complexity Limit Wider Adoption

They often require more specialized chemistries and stricter processing controls than commodity plastics, which increases production costs and limits their suitability in price-sensitive industries. Applications that prioritize low cost over performance still rely on simpler polymer films that are easier to manufacture at scale. For processors without advanced extrusion capabilities, the operational demand of PU film production can further slow adoption.

- Polyurethane extrusion processes follow tighter temperature and curing control guidelines referenced in ASTM and ISO processing standards, contributing to higher production complexity as compared to basic thermoplastic films.

MARKET OPPORTUNITIES

Expansion of Skin-Contact, Breathable and Medical Applications Drives New Market Growth

PU films are gaining momentum in medical dressings, surgical drapes, wearable health devices, and technical apparel due to their breathability, elasticity and skin-friendly characteristics. Their ability to provide moisture vapor transmission while preventing fluid ingress makes them well suited for long-wear applications. As healthcare and wearable technology evolve toward flexible materials that improve patient comfort and performance, PU films are positioned to capture a larger share of these high-value segments.

- FDA guidance for moisture-vapor-permeable polymer films identifies polyurethane membranes as suitable materials for advanced wound-care dressings, reinforcing their relevance in medical and skin-contact applications.

MARKET CHALLENGES

Limited Recycling Pathways Constrain Progress Toward Material Circularity Hampers Market Growth

Despite strong functional advantages, market faces structural challenges in recycling due to their chemistry and multilayer construction. The lack of widely adopted recovery systems restricts end-of-life options, which can be a barrier for industries moving toward circular material strategies. As sustainability expectations rise, manufacturers must address the recyclability gap to maintain long-term competitiveness.

- EU REACH regulations continue to increase scrutiny on polymer waste and emissions, prompting industries to prioritize materials with clearer recycling and end-of-life pathways, an area where PU films remain limited.

Download Free sample to learn more about this report.

Segmentation Analysis

By Form

PU Laminates Lead Market as Manufacturers Prioritize Durability, Flexibility and Multi-Functional Performance

Based on form, the market is segmented into monolayer PU films, multilayer PU films, PU laminates and others.

To know how our report can help streamline your business, Speak to Analyst

The PU laminates segment accounted for a significant PU Films market share in 2025. PU laminates segment holds the largest share as they combine the structural benefits of multilayer designs with the softness, clarity and elasticity of polyurethane. This allows converters to achieve enhanced tear resistance, abrasion protection and barrier performance across automotive interiors, technical apparel, medical devices and industrial protection systems. Their ability to integrate breathable or reinforced layers makes PU laminates the preferred choice for performance-driven applications where monolayer films cannot meet durability or functional requirements.

- Automotive OEM specifications in the EU and the U.S. increasingly require abrasion-resistant laminates for seating and interior trims to ensure long-term durability and compliance with material performance standards.

Multilayer PU films is the fastest-growing segment with a CAGR of 7.0% in the market due to their ability to combine multiple functional layers, such as barrier protection, elasticity, abrasion resistance, and breathability, within a single structure. This enables superior performance customization for high-value applications in automotive interiors, medical devices, protective apparel, and advanced packaging. Growing demand for lightweight, durable, and high-performance materials is accelerating adoption over conventional monolayer films. Additionally, multilayer architectures support down gauging and material efficiency, aligning with OEM cost-reduction and sustainability objectives. Rapid innovation in lamination and co-extrusion technologies further reinforces their growth momentum.

By Application

Surface Protection Films Dominate Due to Rising Demand for High-Clarity and Durable Protective Solutions

In terms of application, the market is categorized into surface protection films, technical membrane films, medical & hygiene films and others.

The surface protection films segment accounted for the largest share in 2025. This segment growth is due to its superior scratch resistance, elasticity and optical clarity compared with conventional protective materials. These properties support their use in automotive paint protection, consumer electronics, display panels and industrial components that require high-quality surface retention. As manufacturers emphasize premium finishes and longer product lifecycles, PU-based protection films continue to gain preference across high-value sectors.

- Many leading automotive manufacturers specify polyurethane-based paint protection films to maintain exterior finish quality, reflecting their strong resistance to UV exposure and environmental stress.

The technical membrane films segment is expected to grow at a CAGR of 5.6% over the forecast period.

By End-Use Industry

Automotive and Transportation Lead as OEMs Shift Toward Lightweight and Low-Emission Materials

In terms of end-use industry, the market is categorized into automotive & transportation, medical & healthcare, textiles, outdoor & footwear, electronics & consumer, and others.

The automotive & transportation segment accounted for the largest share in 2025. Automotive and transportation represent the largest end-use segment because PU films align with OEM priorities of reducing vehicle mass, improving interior durability and adopting materials compatible with low-emission manufacturing. Their flexibility, abrasion resistance and aesthetic performance make them suitable for seating, trims, instrument panels and protective layers. The growing shift to solvent-free TPU films further supports OEM sustainability goals without compromising performance.

- EU vehicle CO2 reduction requirements encourage increased use of lightweight polymer-based materials, supporting ongoing replacement of heavier or higher-VOC films with polyurethane solutions.

The Textiles, Outdoor & Footwear segment is expected to grow at a CAGR of 6.4% over the forecast period. This growth is driven by steady demand for breathable, waterproof and lightweight materials. PU films are widely used in performance apparel, sportswear, outdoor gear, and footwear uppers due to their flexibility, abrasion resistance and comfort properties.

PU Films Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific PU Films Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valuing at USD 1,119.0 million, and is expected maintained the leading share in 2026, with USD 1,206.8 million. The region’s leadership is driven by its strong manufacturing base, extensive polymer-processing capabilities and growing adoption of PU films across automotive, medical, technical textiles and consumer industries. Rising investment in high-performance materials, expansion of breathable membrane production and scaling of TPU film technologies reinforce the region’s dominant position.

China PU Films Market

Based on Asia Pacific’s strong contribution and China’s manufacturing strength, the China market is recorded USD 633.9 million in 2025, accounting for roughly 25 % of global revenues.

India PU Films Market

The Japan market in 2025 secured USD 134.4 million. Increasing demand is supported by growth in medical films, footwear laminates, automotive interiors and protective apparel.

North America

North America remains a significant regional market and reached USD 581.4 million in 2025. Strong adoption of PU films in medical and hygiene applications, automotive interiors, electronics and protective surface films contributes to regional demand. The U.S. dominates the market due to its advanced healthcare infrastructure and a mature automotive sector that increasingly favors lightweight and low-VOC materials.

U.S. PU Films Market

The U.S. market in 2025 is approximated at USD 516.0 million, representing around 20% of global revenues.

Europe

Europe is projected to record a growth rate of 4.5% in the coming years and reached a valuation of USD 633.1 million by 2025. The region benefits from strong technical textile clusters, stringent environmental regulations and increasing substitution of PVC films with TPU and PU materials. Growing emphasis on clean processing, solvent-free films and recyclable TPU grades continues to support demand across automotive interiors, performance apparel and medical applications.

Germany PU Films Market

Germany market reached USD 191.9 million in 2025, equivalent to around 7.6% of global revenues. Its leadership is supported by advanced automotive and engineering industries that rely heavily on high-performance polymer films.

U.K. PU Films Market

The U.K. market in 2025 recorded USD 84.9 million, accounting for roughly 3.3% of global revenues. This growth is supported by expanding demand for breathable membranes, medical drape films and protective laminates.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth during the forecast period. The Latin America market reached a valuation of USD 110.0 million in 2025, supported by expanding footwear, textiles and protective film consumption. In the Middle East & Africa, demand is driven by industrial films, automotive aftermarket uses and increasing adoption of breathable membranes in regional healthcare systems. The Middle East & Africa market reached USD 96.6 million in 2025.

Saudi Arabia PU Films Market

The Saudi Arabia market reached around USD 29.1 million in 2025, accounting for roughly 1.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Material Innovation and Application Expertise Define Competitive Positioning

The market is shaped by companies that combine advanced polyurethane chemistry with strong film processing capabilities. Competition focuses on delivering films that achieve durability, elasticity, breathability and optical performance across automotive, medical, technical textile and industrial protection applications. As manufacturers prioritize cleaner processes, better sustainability profiles and longer product lifecycles, suppliers with integrated R&D and technical service support maintain a stronger market position.

Major players include Covestro, BASF, Lubrizol, SWM International and Avery Dennison. These players offer broad TPU film portfolios that span breathable membranes, medical-grade films, surface protection films and multilayer laminates. Their competitive strength comes from polymer expertise, global manufacturing networks and close alignment with OEM requirements in high-value sectors. Other participants such as American Polyfilm, Permali, Coveris and DingZing contribute specialized capabilities in adhesive films, medical films and advanced automotive PPF materials.

Across the landscape, companies are increasing their competitiveness by advancing solvent-free production technologies, developing recyclable TPU grades and enhancing film performance in demanding environments. Innovation activity is centered on stretchable electronics films, next-generation PPF materials and high-strength TPU layers used in technical apparel and commercial protection systems. Firms that combine material engineering depth with application-driven development continue to lead as PU films play a larger role in performance-oriented and design-intensive markets.

LIST OF KEY PU FILMS COMPANIES PROFILED

- Covestro AG (Germany)

- BASF (Germany)

- Lubrizol (U.S.)

- SWM International Corp. (U.S.)

- 3M (U.S.)

- AMERICAN POLYFILM, INC. (U.S.)

- AVERY DENNISON CORPORATION. (U.S.)

- Permali Gloucester Ltd. (U.K.)

- Coveris (U.S.)

- DingZing Advanced Materials Inc. (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: BASF introduced new TPU film solutions designed for advanced apparel and protective applications, focusing on durability, elasticity and improved processing performance. The launch strengthens BASF’s presence in high-performance PU film segments.

- December 2025: BASF expanded its TPU portfolio to support specialty industrial film applications, offering materials with enhanced chemical resistance and mechanical stability for technical PU film uses.

- October 2025: Avery Dennison launched the Neo Matte Black polyurethane paint protection film, an 8.5-mil self-healing matte film engineered for high-end automotive surface protection and long-term stain resistance.

- September 2025: Lubrizol strengthened its localization strategy in China to support medical-grade TPU films used in wound dressings, drapes and wearable medical devices. The initiative enhances regional supply capability for healthcare-related film applications.

- April 2024: Lubrizol introduced the Estane TPU Empowerment Ecosystem for the market, offering verification, technical support and quality assurance for manufacturers using Estane TPU in premium PU-based PPF films.

REPORT COVERAGE

The global PU Films market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The PU Films market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.8% from 2026-2034 |

|

Unit |

Value (USD Million) Volume (Kiloton) |

|

Segmentation |

By Form, Application, End-Use Industry, and Region |

|

By Form |

· Monolayer PU Films · Multilayer PU Films · PU Laminates · Others |

|

By Application |

· Surface Protection Films · Technical Membrane Films · Medical & Hygiene Films · Others |

|

By End-Use Industry |

· Automotive & Transportation · Medical & Healthcare · Textiles, Outdoor & Footwear · Electronics & Consumer · Offshore & Marine Structures · Others |

|

By Geography |

· North America (By Form, By Application, End-Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Form, By Application, End-Use Industry, and Country/Sub-region) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Form, By Application, End-Use Industry, and Country/Sub-region) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Form, By Application, End-Use Industry, and Country/Sub-region) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America (By End-Use Industry) · Middle East & Africa (By Form, By Application, End-Use Industry, and Country/Sub-region) o Saudi Arabia (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of the Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2,540.1 Million in 2025 and is projected to reach USD 4,260.3 Million by 2034.

Recording a CAGR of 5.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The automotive & transportation end-use industry segment led in 2025.

Asia Pacific held the highest market share in 2025.

5) What is the key factor driving the market growth?

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us