PVDF Membrane Market Size, Share & Industry Analysis, By Type (Flat Sheet, Hollow Fiber, Tubular, and Others), By Application (Biopharma & Pharma Filtration, Water & Wastewater Treatment, Food & Beverage Processing, Electronics & Semiconductor, and Others), and Regional Forecast, 2026-2034

PVDF Membrane Market Size and Future Outlook

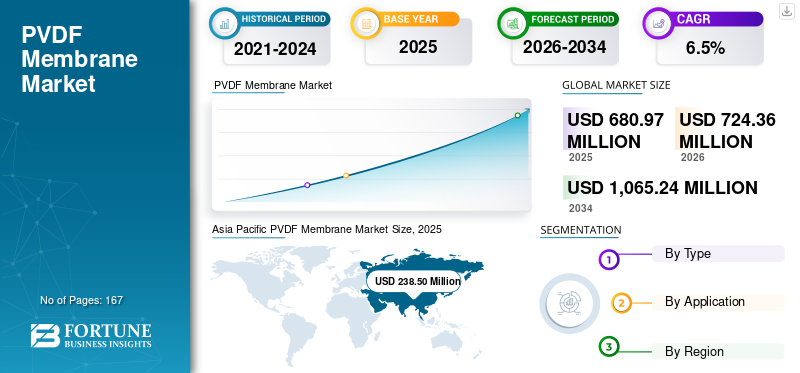

The global PVDF membrane market size was valued at USD 680.97 million in 2025. The market is projected to grow from USD 724.36 million in 2026 to USD 1,065.24 million by 2034, exhibiting a CAGR of 6.5% during the forecast period. Asia Pacific dominated the PVDF membrane market with a market share of 35.02% in 2025.

PVDF membranes are fluoropolymer-based filtration materials extensively utilized in separation and purification processes that demand high chemical resistance, thermal stability, oxidation tolerance, and mechanical durability. These membranes are frequently employed in ultrafiltrathion (UF), microfiltration (MF), membrane bioreactors (MBR), sterile liquid filtration, laboratory sample preparation, and specific industrial process filtration systems. These membranes are available in both hydrophilic and hydrophobic variants and are manufactured in hollow-fiber, flat-sheet, cartridge, and disc configurations to suit various end-use requirements. Their enhanced performance characteristics render them highly suitable for demanding applications in water and wastewater treatment, biopharmaceutical processing, laboratory filtration, food and beverage manufacturing, and specialized industrial separation systems.

A key demand driver for the market is the escalating global necessity for advanced water treatment and water reuse infrastructure. As industries and municipalities face increasing water scarcity, more stringent discharge standards, and growing demand for clean water quality, membrane-based systems are increasingly used for applications such as wastewater polishing, potable water production, and industrial water recycling. Concurrently, the expansion of biologics manufacturing, sterile filtration requirements, and contamination-sensitive laboratory procedures is underpinning demand for high-value products in the pharmaceutical and research sectors.

Furthermore, the market is bolstered by several leading entities, including Toray Industries, DuPont, Asahi Kasei, Veolia/SUEZ Water Technologies, Merck, Cytiva, Sartorius, and GVS, which continue to strengthen their positions through the advancement of membrane technologies, diversification of application portfolios, and the expansion of their infrastructure and life sciences filtration markets.

Download Free sample to learn more about this report.

PVDF Membrane Market Key Takeaways

- 2025 Market Size: USD 680.97 million

- 2026 Market Size: USD 724.36 million

- 2034 Forecast Market Size: USD 1,065.24 million

- CAGR: 6.5% from 2026-2034

- Asia Pacific dominated the PVDF membrane market with a 35.02% share in 2025.

- Biopharma & pharma filtration dominated in 2025 and will grow at a 6.5% CAGR.

- The hollow fiber segment is projected to grow at a CAGR of 7.9% during the forecast period.

Asia Pacific

Asia Pacific led the market with a valuation of USD 238.50 million in 2025.

North America

North America is expected to remain the second-largest market, driven by strong demand from biopharmaceutical and water treatment applications.

Europe

Europe is projected to reach USD 179.68 million in 2026, growing at a CAGR of 5.4% during the forecast period.

U.S.

The market is estimated to reach USD 178.97 million in 2026, accounting for around 24.7% of global sales.

Japan

The market is estimated to reach USD 54.83 million in 2026, representing approximately 7.6% of global revenues.

Read More

PVDF MEMBRANE MARKET TRENDS

Shift toward High-Durability Membranes for Reuse and Bioprocessing is a Key Market Trend

A key trend in the market is the growing shift from standard filtration media to application-specific membranes that offer durability, fouling resistance, process compatibility, and tailored performance for specific end uses. In water treatment, this trend is reflected in the increasing preference for PVDF-based ultrafiltration and membrane bioreactor systems designed for municipal reuse, industrial wastewater treatment, and high-solids environments. As treatment plants adopt more compact systems and aim for higher water recovery, demand is rising for membranes that can withstand aggressive cleaning, long operational cycles, and variable feed conditions.

This trend is also evident in life sciences and laboratory applications, where purchasers of membranes are increasingly favoring products that offer not only filtration efficiency but also low protein binding, broad chemical compatibility, and consistent performance. As the manufacturing of biologics, sterile liquid filtration, and analytical testing becomes increasingly dependent on quality, hydrophilic membranes are gaining broader significance within regulated and high-value workflows. Consequently, suppliers are focusing on premium membrane formats that ensure both process efficiency and enhanced value realization.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Water Reuse and High-Purity Filtration Requirements is Accelerating Product Adoption

PVDF membranes are increasingly significant in advanced water and wastewater treatment applications, where operators require filtration systems that can withstand chemical exposure, high fouling loads, and rigorous cleaning conditions. Their durability, chlorine tolerance, and mechanical robustness render them particularly suitable for ultrafiltration, microfiltration, and membrane bioreactor systems employed in municipal treatment, industrial effluent management, and water reuse facilities. As global water scarcity intensifies and demand for reliable treated water escalates, the use of these membrane systems continues to expand across both public and private-sector infrastructure.

The increasing demand for water reuse and circular water management is further intensifying. Municipalities and industrial facilities are increasingly investing in wastewater reclamation, polishing, and recycling initiatives to reduce reliance on freshwater sources and comply with environmental discharge standards. In these systems, such membranes are esteemed for their durability and operational resilience, rendering them a preferred material in advanced treatment configurations. This is particularly pertinent in regions experiencing water scarcity, industrial growth, and more stringent environmental regulations.

Simultaneously, high-purity applications, including biopharmaceutical processing, sterile liquid filtration, and laboratory sample preparation, are also driving market expansion. Hydrophilic membranes are widely used in these fields owing to their low protein binding, broad solvent compatibility, and reliable filtration performance. Consequently, the market advantages from both infrastructure-based volume demand and life sciences-based value demand.

MARKET RESTRAINTS

Cost Sensitivity, Fouling Management, and Qualification Requirements Can Limit Faster Market Penetration

Despite their performance advantages, PVDF membranes encounter limitations concerning cost competitiveness and system economics. In various applications, procurement decisions are guided not only by membrane performance but also by factors such as total lifecycle cost, module replacement frequency, energy consumption, and cleaning protocols. In price-sensitive water treatment and industrial process sectors, stakeholders may compare these membranes with alternative materials or competing separation technologies, consequently restricting the rate of substitution even when PVDF provides technical advantages.

Another significant limitation is the challenge posed by membrane fouling and process variability. Although PVDF performs well in demanding environments, its operational efficiency remains contingent on factors such as feed composition, pretreatment quality, cleaning protocols, and system design. In wastewater or process streams with high variability, fouling behavior can influence flux, maintenance frequency, and operational costs, potentially hindering broader adoption among cost-sensitive users.

Furthermore, regarding pharmaceutical and other regulated end-use applications, qualification and validation processes can be protracted. Once a membrane product secures approval within a validated production workflow, customers tend to exercise caution in altering suppliers or membrane grades. This cautious approach impedes product substitution and prolongs the time required to adopt new products, especially in applications where sterility, extractables, and documentation standards are of paramount importance.

MARKET OPPORTUNITIES

Reuse Infrastructure, Bioprocessing Growth, and Premium Membrane Design are Creating New Revenue Opportunities

A significant opportunity within the market resides in the expanding scope of municipal and industrial water reuse initiatives. As nations and industries endeavor to enhance water security, membrane-based treatment methodologies are increasingly adopted in tertiary treatment, wastewater recycling, and process-water recovery systems. PVDF membranes are strategically positioned to capitalize on this transition, given their established presence in ultrafiltration and membrane bioreactor configurations tailored for reuse-oriented infrastructure. This development ensures sustained long-term demand, stemming not only from new installations but also from ongoing replacement cycles.

Another significant opportunity is arising from the expansion of biopharmaceutical manufacturing and the increasing demand for sterile filtration. Compared with infrastructure applications, pharmaceutical and laboratory filtration generally offers higher profit margins and greater value per membrane unit. Hydrophilic membranes are increasingly used in biologics processing, sample clarification, sterile liquid filtration, and research workflows, where filtration consistency and chemical compatibility are critical. As the production of biologics expands and laboratory testing volumes worldwide grow, suppliers have an opportunity to enhance their presence in these high-end segments.

Suppliers are also fostering opportunities through advanced module engineering and digital process optimization. Innovations such as new hollow-fiber membrane designs, improved fouling resistance, and software-based membrane system modeling are helping end users enhance plant design, minimize uncertainty, and optimize operational costs. These advancements facilitate increased adoption in both water treatment and industrial process separation markets, especially in scenarios where performance-based selection supersedes traditional cost-based procurement

MARKET CHALLENGES

Balancing High Performance with Sustainability, Regulatory Scrutiny, and Long-Term Reliability Remains a Core Challenge

A significant challenge in the market is balancing the material’s notable technical advantages with growing concerns about sustainability and regulatory compliance. PVDF, as a fluoropolymer, continues to garner interest for its durability and chemical resistance; however, the broader discourse on fluorinated substances and chemical regulation is prompting increased caution among customers in certain markets. This situation imposes an additional responsibility on suppliers to deliver technical clarifications, lifecycle assessments, and compliance support, particularly in applications where procurement standards are becoming more rigorous.

Another challenge involves sustaining long-term membrane performance under actual operating conditions. In practice, end users assess membranes not solely based on initial filtration metrics but also consider cleanability, fouling response, mechanical integrity, and replacement intervals over time. Consequently, suppliers are required to provide not only membrane materials but also dependable module engineering, system integration, and after-sales application support. In numerous instances, the competitive advantage hinges equally on operational performance as on membrane chemistry itself.

Furthermore, the market remains technically demanding as performance expectations differ sharply across applications. Water reuse, industrial process separation, laboratory filtration, and sterile pharmaceutical workflows each require distinct performance profiles, making broad-based product standardization difficult. As a result, producers must continue investing in application engineering and product customization to remain competitive.

Segmentation Analysis

By Type

High Demand for Flat Sheet Membranes Contributed to Segmental Growth

Based on type, the market is segmented into flat sheet, hollow fiber, tubular, and others.

The flat sheet segment led the PVDF membrane market share in 2025, accounting for the largest proportion of global demand. This segment encompasses the membrane formats supplied as discs, sheets, and roll stock for laboratory filtration, process filtration, transfer applications, and device-level filtration assemblies. Its predominant position is underpinned by extensive applicability across the life sciences, analytical, pharmaceutical, and specialty industrial sectors, where these formats are favored for their ease of integration, product flexibility, and availability in multiple pore sizes and structures. Additionally, in terms of value, the segment benefits from increased participation in higher-priced applications, such as biopharmaceutical filtration, analytical testing, and specialty process filtration.

The hollow fiber segment accounted for the second-largest market share in 2025 and remains a pivotal area of structural growth. This segment encompasses the membranes used in water treatment and specific hollow-fiber configurations for process or bioprocess applications. The demand is robustly supported by municipal water treatment, industrial wastewater treatment, membrane bioreactors, and reuse systems, where PVDF hollow-fiber membranes are esteemed for their mechanical durability, oxidation resistance, and extended operational lifespan. Although the average price realization is lower than that of certain specialty flat-sheet formats, the segment benefits from a substantial installed base demand and recurrent replacement requirements in infrastructure-scale applications. Furthermore, this segment is forecast to grow at a CAGR of 7.9% over the designated study period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Stringent Selection Standards Drive Biopharma & Pharma Filtration Segment Dominance

In terms of application, the market is categorized into biopharma & pharma filtration, water & wastewater treatment, food & beverage processing, electronics & semiconductor, and others.

The biopharma & pharma filtration segment accounted for the largest share of the market in 2025. This segment encompasses sterile, clarifying, and process filtration of biological and pharmaceutical liquids, where hydrophilic membranes are widely used for their low protein-binding capacity, robust chemical compatibility, and dependable filtration performance. The segment benefits from higher pricing compared to infrastructure-driven applications, as membrane selection in pharmaceutical settings is heavily influenced by factors such as product consistency, validation requirements, and contamination control. Consequently, despite lower overall membrane area demand than in some utility-scale applications, this segment still significantly contributes to market value. Furthermore, this segment is forecast to grow at a CAGR of 6.5% over the designated study period.

The water & wastewater treatment segment accounted for a significant portion of the market and remains one of the most robust categories in terms of volume demand. This segment encompasses municipal and industrial water treatment, wastewater reuse, and desalination membrane demand. PVDF membranes are highly appropriate for these applications due to their durability, fouling resistance, and compatibility with ultrafiltration, microfiltration, and membrane bioreactor systems. The segment’s market share is reinforced by increasing global demand for water security, tightening wastewater discharge standards, and heightened interest in water reuse infrastructure, particularly in the Asia Pacific region, the Middle East, and the industrial treatment sector. Additionally, this segment is forecast to grow at a CAGR of 7.2% over the designated study period.

The electronics & semiconductor segment is expected to be the fastest-growing segment during the forecast period. This segment encompasses high-purity wet-chemical and electronic-process filtration, where the membranes are valued for their chemical resistance, purity, and compatibility with stringent process conditions. The expansion of semiconductor fabrication, electronics materials processing, and contamination-sensitive manufacturing environments is driving demand for such membranes within this category. Relative to broader industrial applications, this segment generally commands higher average prices owing to stringent purity standards and performance expectations. Furthermore, this segment is forecast to grow at a CAGR of 7.4% over the designated study period.

PVDF Membrane Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific PVDF Membrane Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the dominant share valued at USD 222.98 million, and continued to lead in 2025 with a valuation of USD 238.50 million. The region benefits from a high concentration of water treatment infrastructure development, substantial industrial wastewater treatment requirements, expanding manufacturing activities, and a robust presence of membrane production and technology suppliers. Furthermore, the growth of the pharmaceutical and laboratory sectors in major Asian economies continues to drive demand for premium products.

China PVDF Membrane Market

By 2026, the Chinese market is projected to reach USD 82.89 million. China is the principal demand hub in the Asia Pacific region, driven by its extensive industrial infrastructure, escalating investments in wastewater treatment, and rising demand for sophisticated water reuse systems. This demand is further bolstered by the pharmaceutical sector, electronics manufacturing processes, and upgrades to municipal treatment facilities. The magnitude of industrial and infrastructural deployment renders China a significant contributor to both regional volume and value demand.

To know how our report can help streamline your business, Speak to Analyst

Japan PVDF Membrane Market

The Japan market size in 2026 is estimated to be around USD 54.83 million, accounting for roughly 7.6% of the global revenues.

India PVDF Membrane Market

The Indian market value in 2026 is estimated at around USD 26.87 million, accounting for roughly 3.7% of global revenues.

North America

The market in North America is anticipated to retain its position as the second-largest globally, driven by robust demand within the biopharmaceutical filtration, laboratory consumables, industrial water treatment, and advanced municipal treatment sectors. The region has a well-established high-value filtration ecosystem and continues to benefit from investments aimed at enhancing process reliability, water reuse, and premium separation technologies. Projections indicate that by 2026, the U.S. market will reach USD 178.97 million.

U.S. PVDF Membrane Market

The U.S. is the largest market in North America, driven by its leading role in biopharmaceutical manufacturing, laboratory filtration requirements, industrial treatment systems, and the widespread adoption of high-performance membranes across essential end-use sectors. Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 178.97 million in 2026, accounting for roughly 24.7% of global sales.

Europe

Europe is expected to experience substantial PVDF membrane market growth in the coming years. During the forecast period, the European region is projected to grow at 5.4% and reach USD 179.68 million in 2026. A robust combination of industrial water treatment, wastewater compliance requirements, pharmaceutical manufacturing, and a growing focus on sustainable water management supports the region's growth. Increased investments in reuse, improvements in discharge quality, and contamination-sensitive laboratory filtration further strengthen the demand.

U.K. PVDF Membrane Market

The U.K. market in 2026 is estimated at around USD 33.77 million, accounting for roughly 4.7% of global revenues.

Germany PVDF Membrane Market

Germany’s market in 2026 is estimated at around USD 45.99 million, accounting for roughly 6.3% of global revenues.

Latin America and the Middle East & Africa

Over the forecast period, Latin America and the Middle East & Africa regions are anticipated to experience moderate growth within this market. These regions constitute comparatively smaller markets; however, they are gaining momentum due to increasing demands for industrial water treatment, wastewater recycling, and targeted municipal treatment infrastructure. The Middle East, in particular, benefits from water scarcity-driven filtration requirements, while Latin America is progressively expanding its membrane-based reuse and industrial treatment infrastructure. The Latin America market is projected to reach USD 39.13 million by 2026.

GCC PVDF Membrane Market

The GCC market in 2026 is estimated at USD 23.64 million, accounting for approximately 3.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Performance, Installed Base, and Application Engineering Support Drive Competitive Differentiation

The market demonstrates moderate concentration, with global water treatment enterprises, life science filtration suppliers, and specialty membrane manufacturers competing within various end-use sectors. Competitive advantage is established through membrane durability, fouling mitigation, process compatibility, validation support, and the capacity to deliver dependable performance in challenging applications. In the water treatment sector, suppliers compete fiercely on lifecycle economics, module design, and plant-level operational efficiency. Conversely, in life science applications, competition primarily revolves around sterile filtration performance, regulatory assurance, documentation standards, and demand for recurring consumables.

Large incumbents benefit from broad portfolios that span water infrastructure, industrial separation, and laboratory or pharmaceutical filtration. Their ability to support customers through application engineering, system optimization, replacement supply, and performance troubleshooting strengthens long-term customer retention. Toray Industries, DuPont, Asahi Kasei, Veolia/SUEZ Water Technologies, Merck, Cytiva, Sartorius, and GVS are some of the key players in the market.

LIST OF KEY PVDF MEMBRANE COMPANIES PROFILED

- Toray Industries, Inc. (Japan)

- DuPont (U.S.)

- Asahi Kasei Corporation (Japan)

- Veolia (France)

- Merck KGaA (Germany)

- Cytiva (U.S.)

- Sartorius AG (Germany)

- GVS S.p.A. (Italy)

- Koch Separation Solutions (U.S.)

- Pall Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: DuPont launched WAVE PRO for ultrafiltration modeling, expanding the use of digital process design tools for membrane system optimization across drinking water, wastewater, and industrial utility water applications.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.5% from 2026-2034 |

| Unit | Value (USD Million), Volume (Million Meter Square) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 680.97 million in 2025 and is projected to reach USD 1,065.24 million by 2034.

Recording a CAGR of 6.5%, the market is slated to exhibit steady growth during the forecast period.

The biopharma & pharma filtration application segment led in 2025.

Asia Pacific held the highest market share in 2025.

The rising water reuse and high-purity filtration requirements are accelerating the adoption.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us