Quantum Warfare Market Size, Share & Industry Analysis, By Capability Type (Post‑Quantum Cryptography & Crypto‑Agility, Quantum Sensing & Quantum‑Enhanced ISR, Quantum Timing & PNT Resilience, Quantum Communications, & Others), By Systems (Hardware, Software, Systems Integration & Test, and Services), By Platform (Land, Airborne, Naval, Space, & C4ISR Infrastructure), By Application (Secure Communications & Data Protection, ISR / Detection/Tracking, & Others), By End User (Defense Armed Forces, R&D Organization And Intelligence Agencies, & Others), and Regional Forecast, 2026-2034

Quantum Warfare Market Size and Future Outlook

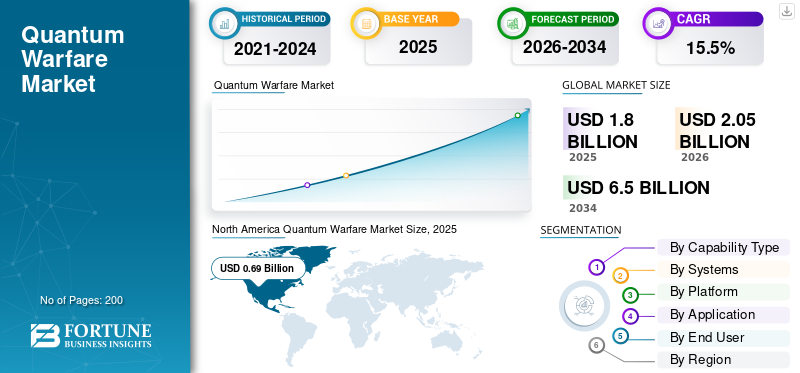

The global quantum warfare market size was valued at USD 1.80 billion in 2025. The market is projected to grow from USD 2.05 billion in 2026 to USD 6.50 billion by 2034, exhibiting a CAGR of 15.5% during the forecast period. North America dominated the quantum warfare market, with a market share of 38.33% in 2025.

The global market for quantum warfare focuses on defending national security by updating defense systems with quantum tools. It includes post quantum cryptography and quantum-resistant encryption for secure communications, as well as quantum sensors. Quantum sensors range from radar antennas and clock magnetometers to various quantum component upgrades that enhance detection and timing. As countries develop quantum capabilities like quantum networks and quantum simulators, the market is growing through its applications in the military. The U.S. leads in early adoption, North America remains a key market, and the Asia Pacific market is also rapidly expanding, contributing to overall growth of the market.

Key players including IBM, Google (Alphabet), Lockheed Martin, Northrop Grumman, RTX Corporation, BAE Systems, and Honeywell (Quantinuum) are advancing in this market, from research to practical use by rolling out post quantum cryptography, integrating sensing payloads, and enhancing platforms. In the U.S. and North America, major defense and cybersecurity companies are implementing upgrades in post-quantum cryptography, quantum resistant encryption, and secure communications across defense systems. In the Asia Pacific region, teams continue to develop quantum sensing and timing, utilizing quantum simulator testing and early quantum network pilots to accelerate field deployment. This progress is why the Asia Pacific market is the fastest and continues to boost the overall size of the market globally.

Download Free sample to learn more about this report.

Quantum Warfare Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.80 billion

- 2026 Market Size: USD 2.05 billion

- 2034 Forecast Market Size: USD 6.50 billion

- CAGR: 15.5% from 2026–2034

- North America dominated the quantum warfare market with a 38.33% share in 2025.

- Quantum Sensing & Quantum-Enhanced ISR was the leading application segment in 2025.

- Hardware accounted for the largest market share among component segments in 2025.

North America

North America led the market due to strong defense investments, quantum-risk compliance initiatives, and early deployment programs.

North America

Europe held the second-largest market position in 2025, supported by secure communications modernization and quantum-ready defense strategies.

Asia Pacific

Asia Pacific was the third-largest market in 2025 and is projected to be the fastest-growing region with a CAGR of 19.2%.

U.S.

U.S. The market was valued at approximately USD 0.63 billion in 2025, driven by defense modernization and quantum technology adoption.

Japan

Japan Government-led investments in quantum sensing, security, networking, and computing are supporting market growth.

Read More

QUANTUM WARFARE MARKET TRENDS

Government-Mandated Post-Quantum Cryptography rollout For Modernizing Secure Defense Communications

In the field of quantum warfare, the most immediate and scalable trend is that of Post Quantum Cryptography (PQC) which is moving from research and development planning stage to actual rollout. Defense and national security networks are adopting crypto-agility. Procurement specifications now reference PQC readiness. System owners face pressure to list and replace crypto which is vulnerable to quantum threats. It’s less waiting time for a perfect quantum computer and more about reducing harvest-now, decrypt-later risks, while ensuring that secure communications can be upgraded across platforms and C4ISR infrastructure.

In August 2024, NIST finalized and released its first three post quantum cryptography standards (FIPS 203, 204, 205). These standards are ready for immediate use, which speeds up procurement, compliance, and migration timelines across government and defense supply chains.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Mandated Migration to PQC is Propelling the Quantum Readiness, Driving the Market Growth

Governments no longer see quantum risk as a future research issue. They view it as a national security compliance problem that needs to be addressed in today's secure communications and mission networks. Once PQC and crypto-agility are required in inventories, timelines, and procurement expectations, budgets are being freed up for software upgrades, integration, validation, and replacing quantum-vulnerable crypto in defense systems. This policy pressure is what turning “interest” into funded programs.

In November 2022, the White House Office of Management and Budget issued Memorandum M-23-02. It has instructed U.S. federal agencies to start a structured transition, which includes inventories and planning, to quantum-resistant cryptography, following National Security Memorandum-10.

MARKET RESTRAINTS

Legacy Crypto Built Into Platforms Makes PQC Migration Slow, Costly, And Difficult To Verify

A key problem in the quantum warfare market growth is quantum-vulnerable cryptography being embedded in radios, SATCOM terminals, avionics, mission computers, ground C2, and even vendor middleware. This means migration isn’t just about changing an algorithm. It includes asset discovery, mapping dependencies, updating software and firmware, testing for interoperability, and re-certifying. This often happens across long-life defense platforms where changes are strictly controlled. In practice, the most challenging part is finding where the crypto exists and proving that the upgraded system still functions reliably and securely.

MARKET OPPORTUNITIES

Improvement of C4ISR and Mission Networks to Create Growth Opportunity in Market

Quantum warfare involves more than high-tech equipment, it focuses on strengthening allied networks against quantum threats. This opens up a solid path for vendors for crypto-agility toolkits, PQC migration services, validation labs, and integration packages for improving C4ISR and mission networks across various domains. In simpler terms, the opportunity is beneficial for consistent rollouts across multiple sites and programs, instead of single demos. The opportunity comes from across multiple programs instead of one-off demos, making it easier for suppliers to scale up and move confidently from pilot projects to full deployment.

MARKET CHALLENGES

Complexity Associated with PQC Migration to Hamper Market Development

The biggest challenge in the quantum warfare market growth is moving to quantum-safe security. This affects everything at once: devices, mission networks, certificates, and embedded crypto in long-life platforms. PQC migration is unmatched in scale. The hard part isn’t choosing an algorithm; it’s coordinating the phase-out of legacy crypto, updating products, proving interoperability, and gaining assurance and validation across various defense infrastructures without disrupting operations.

In November 2024, NIST published the Initial Public Draft of NIST IR 8547 (Transition to Post-Quantum Cryptography Standards). This document acknowledges the transition as unmatched in scale. It highlights the complexity of migrating many systems and describes it as a joint effort across products, services, and validation ecosystems.

Impact of Russia Ukraine War

Need For Quantum-Ready Modernization And Resilience Upgrades Boosted The Market Growth During The War

Ukraine has shown, repeatedly that modern forces can lose communication links, targeting, and navigation when jamming and spoofing are common. This puts pressure on the battlefield for pushing budgets for quantum warfare toward practical solutions: secure communications, more resilient timing/PNT, and improved sensing that keep ISR and strike operations running even when the spectrum is hostile. The impact goes beyond Ukraine.

The risks of GNSS disruption are now viewed as a NATO-level hybrid threat. This reinforces the need for quantum-ready modernization, which includes crypto-agility and PQC for lasting data protection, alternative timing sources, and next-generation sensor methods that reduce dependence on fragile signals. In short, the war has sped up timelines, buyers are funding resilience upgrades more quickly because they have witnessed the results of inaction.

In October 2023, NATO's Joint Air Power Competence Centre (JAPCC) published Electronic Warfare in Ukraine. The report highlighted out how the realities of electronic warfare in this conflict propelled the need for capability development to survive and operate effectively in highly contested environments.

In September 2025, after reports of GPS interference affecting a flight carrying the President of the European Commission, NATO publicly stated it was working to combat suspected Russian GPS jamming. This highlighted GNSS disruption as an ongoing hybrid threat with serious real-world consequences.

Segmentation Analysis

By Capability Type

Quantum Sensing & Quantum-Enhanced ISR are at the Forefront Due to their High Demand on the Account of Their Quick Deployment

In terms of by capability type, the market is categorized into Post Quantum Cryptography (PQC) & crypto‑agility, quantum sensing & quantum‑enhanced ISR, quantum timing & PNT resilience, quantum communications, quantum computing for defense workloads, and counter‑quantum & protection measures.

Quantum sensing & quantum‑enhanced ISR segment dominated the market in 2025. Quantum sensing is valuable as it provides a realistic answer for warfighters unlike longer-term quantum computing, quantum sensing can be deployed more quickly. This includes magnetic navigation, upgrades to inertial and timing systems, and ISR improvements that work with existing platforms. As a result, there is a steady demand for quantum sensors that improve detection, geolocation, and reliability in real missions, not just in laboratories.

In July 2025, Honeywell was selected by the U.S. DoD’s Defense Innovation Unit (DIU) for the Transition of Quantum Sensing (TQS) program. This program aims to accelerate the use of quantum sensors for immediate alternative PNT and ISR needs, including contracts for MagNav and inertial sensing.

Post Quantum Cryptography (PQC) & crypto‑agility segment in market expected to show fastest CAGR of 21.2% over the forecast period.

By Systems

Hardware Leads The Market due To Their Need In Fieldable Sensors And Timing Hardware

On the basis of systems, the market is classified into hardware, software, systems integration & test, and services.

Hardware segment held the largest global quantum warfare market share in 2025 as most quantum-warfare capabilities are still being built into the physical stack. This includes quantum sensors, clocks, photonics, and rugged modules that can handle vibration, EMI, and tough operating conditions. Even if the end goal is software-defined resilience, reliable hardware is still necessary to sense, time, and secure signals. As a result, budgets prioritize prototyping, qualification, and platform integration of hardware even before software and service layers can be developed.

Services is expected to show fastest market growth at a CAGR of 17.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Due To Network-Wide Modernization and Compliance-Driven PQC Rollout, C4ISR Infrastructure Dominates The Market

Based on platform, the market is segmented into land, airborne, naval, space, and C4ISR infrastructure.

C4ISR infrastructure segment held the largest market share in 2025 as C4ISR infrastructure upgrades related to quantum warfare takes place first, where militaries face the highest risk. These areas include mission networks, data links, gateways, identity and certificate infrastructures, and enterprise crypto. As a result, budgets focuses on updating C4ISR, improving crypto agility, and securing network design either before or alongside specific platform upgrades. This leadership is also supported by government policies. As governments and alliances encourage the use of post-quantum cryptography and quantum-resilient networking, C4ISR becomes the main layer for implementation.

Space segment is the fastest growing in market with a CAGR of 18.8% during the forecast period.

By Application

Secure Communications And Data Protection Is The Most Crucial Application Due To Necessary PQC Migration And Harvest-Now, Decrypt-Later Risk

Based on by application, the market is segmented into secure communications & data protection, ISR / detection / tracking, navigation & synchronization in GNSS‑denied environments, counter‑quantum, and others.

Secure communications & data protection segment accounted for the largest share of market in 2025. This application stands out because as it provides the fastest way to funded action from "quantum threat". Defense and national security networks cannot be under the assumption that quantum resistant encryption will stay secure forever. Nowadays, adversaries can take encrypted traffic now and try to decrypt it later. This urgency pushes spending toward post quantum cryptography, crypto-agility, certificate modernization, and quantum-resistant upgrades throughout mission networks and C4ISR backbones.

Secure communications & data protection segment is also expected to show fastest CAGR of 19.2% during the forecast period.

By End User

Due To Mission-First R&D Funding And Urgency Of Classified Threats, R&D Organizations And Intelligence Agencies Lead The Market

Based on by end user, the market is segmented into defense armed forces, R&D organization and intelligence agencies, national labs / defense R&D organizations, and prime contractors & integrators.

R&D organization and intelligence agencies segment dominated the market in 2025 as they are known to a identify the threat landscape and detect problems sooner. They can finance high-risk prototypes and act quickly when something appears crucial. In quantum warfare, R&D teams are linked to providing suitable intelligence which drives the early spending on quantum computing research, quantum sensing experiments, and transitions to “quantum-safe” security. After which, they share what works with armed forces and integrators for further development.

In February 2024, ODNI’s IARPA, the R&D arm of the U.S. Intelligence Community, launched a new quantum computing program. The aim is to advance the field beyond major technical challenges. This shows that intelligence-led R&D is actively funding and shaping the development of quantum capabilities.

Defense armed forces segment is expected to show fastest CAGR with a 17.8% across the forecast period.

Quantum Warfare Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and Rest of the World (Africa and Latin America).

North America

North America Quantum Warfare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region leads the market as U.S. has created actual compliance deadlines and contract opportunities revolving around quantum risk. When federal policy asks agencies and the defense supply chain to keep track of and update cryptography, it subsequently generates an immediate demand for C4ISR infrastructure, software upgrades, integration, testing, and validation. At the same time, the DoD is working to move quantum sensing from the labs to real-world demonstrations. This effort allows the region to secure significant number of early deployments and funded prototypes.

U.S. Quantum Warfare Market

Based on North America’s market size, strong contribution, and the U.S.’s dominance within the region, the U.S. market can be having been approximated to be valued at around USD 0.63 billion in 2025, growing at a CAGR of 12.9%.

Europe

Europe market size has secured the second largest position in 2025 and is also estimated to hold the same position during the forecast period. The region is projected to grow at a CAGR of 14.3% with a recoded valuation of USD 0.49 billion in 2025. Europe is making progress in the market by focusing on network resilience and secure connectivity. Its main goal is to improve government and defense communications, update C4ISR systems, and establish quantum-ready standards among allies. Two important aspects are NATO’s emphasis on quantum strategy, which includes PQC and quantum-secure communications, and the EU’s effort to ensure secure government connectivity through multi-orbit SATCOM. These strategies lower dependency risks and improves operational continuity.

U.K. Quantum Warfare Market

U.K. market approximately reached USD 0.08 billion in 2025, equivalent to around 16.24% of Europe market revenues.

Germany Quantum Warfare Market

The Germany market size has been recorded around USD 0.09 billion, representing roughly 17.70% of Europe market revenues, in 2025.

Asia Pacific

Asia Pacific market size is third largest in global market and is anticipated to be the fastest growing region during the forecast period, with a CAGR of 19.2%. The region is growing quickly as major countries in the region are investing in their national quantum ecosystems. These investments are translating into improvements in defense-related sensing, timing, and security. India’s National Quantum Mission demonstrates strong government backing for the long term. Japan has a government-led approach for quantum innovation that focuses on sensing, security, networking, and computing. Australia is linking its quantum initiatives to defense goals while also promoting wider industry growth. Overall, the region is moving from pilot projects to organized programs, making it one of the fastest regions to adopt quantum technology in defense.

China Quantum Warfare Market

China’s market is projected to be one of the largest in the Asia Pacific region, with 2025 revenues around USD 0.19 billion, representing roughly 44.78% of Asia Pacific market sales.

India Quantum Warfare Market

The India market in 2025 recorded around USD 0.06 billion, accounting for roughly 13.23% of Asia Pacific market revenues.

Middle East

Middle East market size is anticipated to be the second fastest growing region during the forecast period, growing at a CAGR of 18.1%. The Middle East emphasizes deployment and protection. The region's most notable advancements are in cryptography and data protection. Governments seek quantum-safe security for important state networks and have particular sensing and timing needs related to high-end purchasing and national security. The UAE's transition to post-quantum cryptography libraries shows a practical approach to implementation instead of merely highlighting research.

Saudi Arabia Quantum Warfare Market

Saudi Arabia market is projected to be one of the largest in Middle East, with 2025 revenues around USD 0.03 billion, representing roughly 33.78% of Middle East market sales.

Rest of the World

Rest of World (Africa and Latin America), has comparatively smaller share, growing at a CAGR of 15.6%. In Africa and Latin America, spending on quantum warfare tends to be less intense and more targeted. The key areas of interest are quantum-safe communications, preparation for post-quantum cryptography, modernization of intelligence, surveillance, and reconnaissance systems, and enhancements in resilience that fit into existing defense and security systems. The strategy is to adopt proven technology and secure the network layer instead of starting large domestic quantum hardware programs. Consequently, services, integration, and crypto migration often lead the initial efforts rather than advanced quantum computing projects.

Africa Quantum Warfare Market

Africa market size was around USD 0.03 billion in 2025, and is expected to reach USD 0.11 billion in 2034, representing roughly 39.56% of Rest of the world market sales.

Latin America Quantum Warfare Market

The Latin America market was around USD 0.05 billion, accounting for roughly 60.44% of rest of the world market revenues, in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Competition Is Defined By Deployable Now Stacks, PQC-Secure Networks, And Field-Ready Quantum Sensing

The quantum warfare market is in the race to provide operational resilience. The competitive landscape is splitting into two distinct paths: Post-Quantum Cryptography (PQC) and crypto-agility market players are strengthening C4ISR infrastructure and secure communications and quantum sensing companies are pushing for alternative PNT/ISR in jammed environments. Standards and mandates including NIST PQC standards, U.S. government migration direction, and NATO’s focus on quantum strategy, are translating quantum readiness into funded programs. This shift is rewarding for who can deliver certified products and integrate them into complex defense networks.

On the supply side, players who stand out are those who can offer a complete comprehensive solution, including hardware modules, software controls, and integration and testing, and lifecycle support. In sensing, U.S. DoD transition efforts; DIU’s quantum sensing initiative, are leading to real demonstrations and platform insertion, favoring robust sensor and timing suppliers. In crypto, companies that modify their products to meet the finalized NIST PQC standards and support crypto-agility rollouts across government and defense are gaining market share. Additionally, alliance-level modernization priorities, such as NATO, are increasing the demand beyond a single country.

LIST OF KEY QUANTUM WARFARE COMPANIES PROFILED

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- BAE Systems plc. (U.K.)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Airbus Defence and Space (Europe)

- Saab AB (Sweden)

- Rheinmetall AG (Germany)

- Honeywell International Inc. (U.S.)

- Quantinuum (U.S.)

- IonQ, Inc. (U.S.)

- Rigetti Computing, Inc. (U.S.)

- D-Wave Quantum Inc. (Canada)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Google LLC (U.S.)

- Amazon Web Services (AWS) (U.S.)

- Cloudflare, Inc. (U.S.)

- ID Quantique (Switzerland)

- Toshiba (Japan)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Thales launched a post-quantum encryptor for secure communications. The MISTRAL post-quantum encryptor was announced at European Cyber Week, marking it as a deployable solution for sensitive government communications.

- July 2025: DIU selected Honeywell for the Transition of Quantum Sensing (TQS) award. This contract aims to meet near-term alternative PNT and ISR needs, showcasing a real investment in deploying quantum sensing capabilities.

- August 2024: NIST finalized its first PQC standards, providing a baseline for procurement. NIST released its first three post-quantum cryptography standards (FIPS 203/204/205). This established concrete requirements for government and defense procurements. 2024. DARPA identified rugged quantum sensing as a priority for defense transitions. The Robust Quantum Sensors (RoQS) program is focused on moving quantum sensors from controlled lab environments to actual DoD platformswhere vibration and EMI can affect performance.

- February 2024: IARPA launched a new quantum computing program to accelerate intelligence-led R&D. ODNI and IARPA announced this new initiative, focusing on advancing quantum computing and positioning intelligence agencies as a key early-funding source for developing quantum capabilities.

- January 2024: NATO unveiled its Quantum Technologies Strategy as a demand signal for the alliance. NATO published a summary of its strategy, stressing the importance of post-quantum cryptography today and looking into quantum key distribution for secure communications in the future. This approach aimed to promote interoperability and prioritize quantum-ready networks among members.

- November 2022: The U.S. federal PQC migration mandate triggered funding for programs. The White House OMB issued M-23-02, directing agencies to begin structured migration to post-quantum cryptography, including inventory, planning, and reporting. This move immediately increased demand for defense and government C4ISR modernization.

- September 2022: CNSA 2.0 was released, setting quantum-resistant requirements for National Security Systems. NSA published the Commercial National Security Algorithm Suite 2.0 (CNSA 2.0) guidance to help NSS owners and vendors shift to quantum-resistant algorithms. This has pushed defense supply chains to update products and plans.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Capability Type

|

|

By Systems

|

|

|

By Platform

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.80 billion in 2025 and is projected to reach USD 6.50 billion by 2034.

In 2025, the market value stood at USD 0.69 billion.

The market is expected to exhibit a CAGR of 15.5% during the forecast period.

By systems, hardware segment led the market.

Mandated migration to post quantum cryptography is driving the market growth. It is transforming quantum readiness into a funded modernization program.

RTX (Raytheon), Lockheed Martin, Northrop Grumman, L3Harris Technologies, BAE Systems, Thales, Honeywell, Q-CTRL, IBM, Microsoft, and AWS, D-Wave, IonQ, Quantinuum, and Rigetti, among others, are the top companies in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us