Radome Market Size, Share & Industry Analysis, By Material (Glass Fiber, Plastics, and Composite Materials), By Application (Radar, Sonar, Communication Antenna, and Others), By Deployment Mode (Multi Band and Single Band), By Frequency (HF/UHF/VHF-Band, L-Band, S-Band, C-Band, K/Ku/Ka-Band, and X-Band), By Platform (Ground, Air, Naval, and Space Launch Vehicle), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

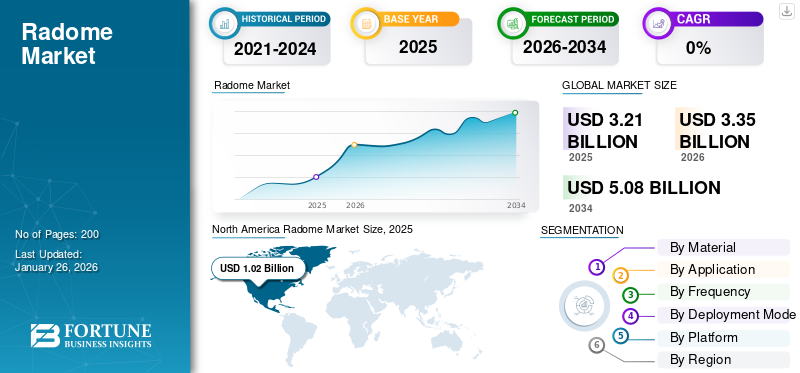

The global radome market size was valued at USD 3.21 billion in 2025. The market is projected to grow from USD 3.35 billion in 2026 to USD 5.08 billion by 2034, exhibiting a CAGR of 5.87% during the forecast period. North America dominated the radome market with a market share of 31.71% in 2025.

Radomes shield the antenna from environmental elements and hide the electronic equipment from sight. The purpose is to provide a weatherproof enclosure for a radar antenna. It is made of a material that allows radio waves to pass through. The market encompasses products which are designed to protect radar and communication antennas from environmental factors, is experiencing significant growth.

Download Free sample to learn more about this report.

This growth is driven by advancements in technology, increasing military spending, and the rising demand for enhanced communication systems. Moreover, the design of systems can vary based on the intended use, with different shapes, sizes, and construction materials being utilized. Common shapes include spherical, geodesic, and planar, while materials such as fiberglass, polytetrafluoroethylene (PTFE)-coated fabric, and other materials are commonly used in construction to protect from environmental damage, thus driving market growth.

The COVID-19 pandemic had a substantial impact on the market, disrupting supply chains and causing delays in production. Many manufacturing facilities faced temporary closures, and the rapid spread of COVID-19 resulted in a significant decline in demand, particularly in sectors reliant on timely deliveries and installations.

The market includes significant key players such as General Dynamics, Raytheon, Saint-Gobain, Northrop Grumman Corporation, and Cobham Limited. These companies hold a robust presence in radar and radome technologies and are concentrating on developing advanced radome designs, especially for missile defense and avionics applications.

The pandemic caused delays in obtaining necessary certifications for new products, which are critical for ensuring safety and compliance. For instance, certifications from regulatory bodies, such as the FAA, can take years, and any disruption in this process can lead to further delays in bringing new technologies to market.

Download Free sample to learn more about this report.

Radome Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.21 billion

- 2026 Market Size: USD 3.35 billion

- 2034 Forecast Market Size: USD 5.08 billion

- CAGR: 5.87% from 2026–2034

- North America dominated the radome market with a 31.71% share in 2025.

- The composite materials segment accounted for the largest market share of 47.30% in 2026.

- The radar segment is projected to capture the largest market share of 45.67% in 2026.

North America

North America generated USD 1.02 billion in 2025 and is projected to reach USD 1.06 billion by 2026.

Europe

Asia Pacific accounted for USD 0.87 billion in 2025 and is projected to reach USD 0.92 billion by 2026.

Europe

Europe contributed 19.57% of the global market in 2025, valued at USD 0.63 billion, and is projected to reach USD 0.66 billion by 2026.

U.S.

U.S. The market is projected to reach USD 0.9 billion by 2026.

Japan

Japan The market is projected to reach USD 0.1 billion by 2026.

Read More

Market Dynamics

Market Drivers

Growing Demand for Protecting the RADAR and Communication System is Driving Market Growth

The increasing use of the product across various platforms and applications is a key driver fueling the growth of the market. They are critical components that protect radar and communication systems from environmental conditions while ensuring optimal performance, thereby contributing to the global market share.

Growth momentum is mainly driven by rising adoption in traditional industries such as military and aerospace, alongside emerging applications in telecommunications and the commercial aviation sector. Increased military spending worldwide has played a significant role in the expansion of the market, as there is a growing need for protective radomes to enhance the performance and lifespan of radar systems.

The demand for commercial air travel after the pandemic has boosted product demand. The rise in air passenger numbers has led to an increased need for more aircraft equipped with radar systems that require radome body protection.

For instance, in August 2023, a successful flight test was conducted on an aircraft with the plate number RJ100, which was fitted with the combat aircraft nose system. This test, announced by QinetiQ, was carried out through QinetiQ’s Airborne Technology Demonstrator (ATD) in partnership with BAE Systems, showcasing advancements in airborne radar technology.

Rapid Expansion of 5G Networks Boosts Market Growth

Radomes play a crucial role in the expansion of 5G networks by addressing the unique challenges posed by the higher frequencies used in this technology. Here are the key functions and contributions in facilitating 5G deployment,

Protection and Signal Integrity: Radomes shield sensitive antenna systems from environmental factors, such as rain, snow, and debris, ensuring reliable operation under various weather conditions. This protection is vital for maintaining signal integrity, particularly for 5G antennas that operate at higher frequencies, which are more susceptible to attenuation from physical obstructions.

Accommodating Higher Frequencies: Manufacturers are optimizing designs to enhance performance based on specific antenna functionalities and frequency requirements. This customization helps address the unique challenges of 5G frequencies, ensuring effective support for advanced communication technologies.

Supporting Infrastructure Development: As telecommunications companies expand their 5G networks, they are crucial for housing antennas across various deployment platforms, including cell towers, vehicles, and aircraft. Their ability to protect antennas while ensuring optimal performance supports the rapid deployment of essential infrastructure needed for widespread 5G coverage.

Integration with Advanced Technologies: Radomes are increasingly being integrated with technologies, such as satellite communication (SATCOM) systems, enhancing their functionality and making them suitable for multi-band operations. This integration is vital for ensuring seamless communication across different frequency bands, including those used in 5G networks.

Market Restraints

Complicated Maintenance Efforts Can Hinder Market Growth

Radomes are constructed from materials that need to maintain specific physical characteristics to ensure optimal performance. Any changes in these characteristics can negatively impact the functionality of radar and antenna systems, making timely maintenance essential. The requirement for specialized technical expertise and proper tools for repairs complicates maintenance efforts and can deter manufacturers from efficiently managing their products.

Moreover, the high costs associated with maintaining the systems can be substantial, requiring skilled labor and advanced tools for effective operation. A lack of skilled manpower in the industry further exacerbates this issue, limiting the ability of companies to maintain and operate systems efficiently.

In the aviation industry, the situation is even more complex due to the rigorous safety regulations, which vary across different countries and regions. Compliance with these diverse regulations requires significant efforts and resources from manufacturers, as they must ensure that their radomes meet international safety standards set by organizations, such as the International Civil Aviation Organization (ICAO).

Market Opportunities

Technological Advancement to Create Lucrative Opportunities for the Market

Growth in Aerospace and Defense: Increasing aircraft production, rising military spending, and demand for advanced radar systems create sustained opportunities.

Telecommunications Expansion: The rollout of 5G and satellite communications infrastructure requires more radomes for antennas.

Material Advancements: Innovations in composite materials, nanotechnology, and metamaterials enable higher-performance radomes.

Emerging Applications: Radomes are finding new uses in autonomous vehicles, weather monitoring, and commercial drones.

Strategic Partnerships: Collaborations between radome manufacturers, technology providers, and end-users can drive innovation and market penetration.

Geographic Expansion: Emerging markets in Asia Pacific, the Middle East, and Latin America offer significant growth potential as these regions invest in infrastructure and defense capabilities.

Next-generation radomes are evolving rapidly through advancements in materials, design, and manufacturing processes to meet the increasing needs of telecommunications, aerospace, defense, and satellite applications.

Market Challenge

Shortage of Qualified Workers to Hinder Market Growth

The radome sector plays an essential role in safeguarding radar and communication systems across industries such as aerospace, defense, and telecommunications. However, it encounters several major obstacles that affect growth, profitability, and innovation.

Cutting-edge radomes, particularly those crafted from composite materials or incorporating advanced technologies, come with a substantial development and production cost. This elevated expenditure impacts profit margins and hinders widespread adoption, especially among smaller manufacturers or aerospace industries sensitive to costs. The sector is governed by stringent regulatory standards, particularly in the aviation and defense sectors, to guarantee safety and operational reliability. Adhering to a range of international, national, and bilateral regulations (such as those established by the ICAO and FAA) complicates the process, prolongs development timelines, and raises expenses.

The creation, engineering, and upkeep of radomes require significant expertise. A lack of qualified personnel hampers companies' ability to effectively develop and support these systems. As avionics and radar systems become increasingly complex, radomes must provide protection while minimizing signal interference, necessitating sophisticated engineering and meticulous design. Radomes need to endure extreme environmental conditions and operational challenges, such as temperature variations, rapid airflow, UV radiation, and severe weather. Addressing performance issues in these environments, such as weakened structural integrity or disrupted signal transmission, continues to pose a challenge.

Radome Market Trends

Developments in Composite Materials to Catalyze Market Growth

New composite materials are being developed to improve properties. These include Rayceram 8, Nitroxyceram, Aeronutronic Reaction-Bonded Silicon Nitride (RBSN), and Hot-Pressed Silicon Nitride (HPSN). Moreover, glass fiber composites are gaining popularity as cost-effective, lightweight, and moldable solutions that support a variety of design requirements. North America witnessed radome market growth from USD 0.94 Billion in 2023 to USD 1.01 Billion in 2024.

Hydrophobic coatings are being developed to protect antennas from water damage. This is expected to be a major driver for growth in the naval segment. In addition, radar technology is expected to continue to dominate the market, with sustained demand across military and commercial sectors.

Innovations, such as GaN power transistors, AESA antennas, and MIMO technology, are reshaping the radar technology, providing increased precision and adaptability. AESA antennas' modular design improves reliability, while radar components produced through 3D printing help decrease size and weight. Furthermore, the demand for shelters in the communication segment is expected to grow rapidly as demand for enhanced communication in harsh environments increases.

Segmentation Analysis

By Material

The composite materials segment led the Market Due to Their Lightweight Nature

Based on material, the market is divided into glass fiber, plastics, and composite materials.

The composite materials segment accounts for the largest market share 47.30% in 2026. Composite materials are increasingly favored in manufacturing due to their lightweight nature, high strength-to-weight ratio, and durability. They are used in high-performance applications where weight is a critical factor. They offer enhanced durability and resistance to environmental factors, further driving their adoption across various industries.

The glass fiber segment is projected to be the fastest-growing segment during the forecast period. The growth is driven by their wide usage in radome structures due to its excellent electromagnetic wave transparency, which minimizes interference with radar signals. Innovations in glass fiber technology enhance its appeal, making it suitable for various applications in defense, aerospace, and telecommunications.

By Application

Radar Segment Led the Market due to their Rising Usage Across Various Sectors

Based on the application, the market is distributed into radar, sonar, communication antenna, and others.

The radar segment is projected to capture the largest market share of 45.67% in 2026. The advancements and applications of radar technology across various sectors significantly influenced segment growth. Radars are critical components in numerous applications, including military defense, aerospace, telecommunications, and weather monitoring, propelling the growth of the segment.

The communication antenna segment is estimated to be the fastest-growing segment during the forecast period. The rollout of 5G networks and improvements in satellite communication infrastructure are creating new opportunities for communications antenna applications. These antennas are widely used in satellite communication systems where they ensure reliable signal transmission to protect antennas from weather-related damage.

By Deployment Mode

X-band Segment Led the Market Due to Its Increased Usage in Advanced Radar Systems

Based on deployment mode, the market is divided into multi band and single band.

The multi-band segment is likely to lead the global market in 2026 and is estimated to be the fastest-growing segment during the forecast period. Multi-band radomes are experiencing significant growth due to the increasing demand for advanced radar systems across various sectors, including defense, aerospace, and telecommunications. This growth is fueled by technological advancements, rising military spending, and the need for enhanced communication and sensing capabilities.

For instance, in November 2020, Meggitt PLC, a prominent global firm focused on high-performance components and subsystems for the aerospace, defense, and specific energy markets, secured a USD 4.8 million contract with BAE Systems. Under this contract, the company is providing advanced nose radome technology to support the efficient functioning of a cutting-edge multi-function array radar system on the Typhoon fighter jet.

The single band segment is projected to be the second fastest-growing segment throughout the forecast period, driven by improvements in radar technology, growth of telecommunication networks, and rising military expenditures, especially in the defense and aerospace sectors. The increasing need for advanced communication systems, the deployment of radomes in satellite communications, and imaging radar military applications are also contributing factors.

By Frequency

X-band Segment Led the Market Due to Its Increased Usage in Airborne Weather Radar Systems

Based on frequency, the market is divided into HF/UHF/VHF-Band, L-Band, S-Band, C-Band, K/Ku/Ka-Band, and X-Band.

The X-band segment is expected to dominate the market share of 23.94% in 2026, driven by its critical role in military, aerospace, telecommunications, and weather monitoring applications. X-band radars are commonly used in airborne weather radar systems and require specialized radomes for optimal performance. The L-Band segment is expected to hold a 20.02% share in 2024.

The K/Ku/Ka-Band segment is estimated to be the fastest-growing segment during the forecast period, driven by the expansion of high-throughput satellite communication networks and the increasing use of imaging radar systems. Moreover, its increasing use in satellite communication systems and imaging radar applications further boosts the segment’s growth.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Ground Segment Dominated the Market Due to Growing Number of Antenna Installations

Based on platform, the market is classified into ground, air, naval, and space launch vehicle.

The ground segment is expected to capture a significant market in 2026, with 39.58% due to its widespread use across various applications and the growing number of antenna installations for surveillance and communication purposes. Ongoing military modernization programs globally are driving the demand for advanced radar and communication systems, which in turn increases the need for specialized ones across various platforms.

The air segment is estimated to be the fastest-growing segment during the forecast period, attributed to the increasing demand for advanced radar systems in both military and civilian aviation.

RADOME MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Radome Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 1.02 billion in 2025, representing 31.71% of the global market landscape, and is expected to reach USD 1.06 billion in 2026, and is projected to experience significant growth over the forecast period. The U.S. is a hub for aerospace manufacturing, hosting several original equipment manufacturers (OEMs) and radome manufacturers. This industrial concentration fosters innovation and collaboration, driving the demand for high-performance components in both military and commercial aviation. These factors contribute to the significant growth in the global market. The U.S. market is projected to reach USD 0.9 billion by 2026.

Asia Pacific

Asia Pacific accounted for USD 0.87 billion in 2025, representing 27.05% of the global market share, and is projected to reach USD 0.92 billion in 2026. The Asia Pacific region is expected to grow at the fastest rate in the coming years. Countries such as China, India, South Korea, Australia, and Singapore are experiencing robust economic growth, which is fueling increased spending on infrastructure development, including telecommunications and defense systems. This economic momentum directly contributes to its demand. The Japan market is projected to reach USD 0.1 billion by 2026, the China market is projected to reach USD 0.27 billion by 2026, and the India market is projected to reach USD 0.21 billion by 2026.

Europe

Europe contributed 19.57% to the global market in 2025, with a valuation of USD 0.63 billion, and is projected to reach USD 0.66 billion in 2026. Europe is poised for significant growth, driven by advancements in technology, increasing defense budgets, and a strong emphasis on modernization within the aviation sector. The European aviation industry prioritizes safety upgrades and modernization, leading to increased demand for radomes that protect advanced radar systems used in commercial and military aircraft. They are essential for navigation, terrain avoidance, and weather detection. Countries, such as France, Germany, and U.K., are investing heavily in defense capabilities, which include upgrading radar systems that rely on high-quality. The UK market is projected to reach USD 0.13 billion by 2026, while the Germany market is projected to reach USD 0.08 billion by 2026.

Middle East & Africa

In 2025, Middle East & Africa held 14.06% of the global market, reaching a valuation of USD 0.47 billion, and is projected to grow to USD 0.48 billion in 2026. The Middle East & Africa region is experiencing steady growth in the market, driven by increasing investments in military modernization and the expansion of the aerospace industry. Countries in the region, such as Saudi Arabia, UAE, and Israel, are investing heavily in military modernization programs to enhance their defense capabilities.

Latin America

Latin America is expected to witness steady growth in the coming years, driven by increasing investments in aerospace and defense and the expansion of telecommunications infrastructure in the region.

- In 2025, the Rest of the World market stood at USD 0.23 billion, representing 7.07% of global demand, and is projected to grow to USD 0.23 billion in 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Players Focus on Distribution to Boost Their Product Portfolio

The market is characterized by the presence of several key players who are actively involved in the development, manufacturing, and distribution across various applications, including military, aerospace, telecommunications, and weather monitoring. Rising military and weather monitoring systems in North America and Europe will boost the product demand in the near future. Key players operating in the market include Raytheon Technologies, L3harris Technologies, Northrop Grumman Corporation, BAE Systems, Thales Group, Saint Gobain, General Dynamics, and Nordam Comtech Telecommunication.

List of Top Radome Companies Profiled

- Antesky Science Technology Inc. (China)

- BAE Systems (U.K.)

- FDS Italy Srl (Italy)

- General Dynamics Mission Systems, Inc. (U.S.)

- Infinite Technologies RCS, Inc. (U.S.)

- Northrop Grumman (U.S.)

- Pacific Radomes Inc. (U.S.)

- Meggitt Baltimore, Inc. (U.S.)

- The Boeing Company (U.S.)

- Cobham plc (U.K.)

- Lockheed Martin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENT

- July 2024 - Airbus prolonged a component services agreement with HAECO that encompasses the majority of its commercial aircraft fleet. HAECO's composite services division will be responsible for conducting radome repair work on A320, A330, A340, A350, and A380 aircraft as part of the agreement. The radome repair activities will be carried out at HAECO's composites facility located in Jinjiang, Mainland China.

- March 2023 - Carborundum Universal Limited (CUMI), an industry leader in material sciences within the private sector, entered into a Licensing Agreement with the Defence Research and Development Organisation (DRDO) to transfer technology for the production of ceramic radomes utilized in aerospace and missile systems. Ceramic radomes are considered a crucial, cutting-edge technology for ballistic and tactical missiles and high-performance aircraft.

- May 2022 - Radant Technologies Division of Communications & Power Industries (CPI) finalized the purchase of AdamWorks, LLC, a Centennial, Colorado-based design engineering and manufacturing company with expertise in composite structures for business and commercial aviation, manned and unmanned systems, and space and defense applications. The acquisition enhanced CPI's current radome business through the addition of new airborne product offerings.

- February 2021 - Comtech Telecommunications Corp. revealed that its Space & Component Technology Division from the Mission-Critical Technologies group received a subsequent order from a global infrastructure support firm for a 21.5m radome.

REPORT COVERAGE

The market report provides a thorough market analysis. It comprises all major aspects, such as R&D capabilities, supply chain analysis, competitive landscape, and segmentations by material, application, frequency, and platform. Moreover, the report offers insights into the global radome market trends, growth analysis, size, and highlights key industry developments. In addition to the factors mentioned above, the report focuses on several factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.87% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Application

|

|

|

By Deployment Mode

|

|

|

By Frequency

|

|

|

By Platform

|

|

|

By Region

|

Frequently Asked Questions

As per the study by Fortune Business Insights, the market stood at USD 3.21 billion in 2025.

The market is likely to grow at a CAGR of 5.87% over the forecast period.

By platform, the ground segment led the market.

North America was valued at USD 1.02 billion in 2025.

Expansion of 5G networks is a key factor driving market growth.

BAE System, Antesky Science Technology Inc., Northrop Grumman, and The Boeing Company are the top players in the market.

U.S. is the dominant country in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us