Railway Testing Market Size, Share & Industry Analysis, By Testing Type (Static Testing, Dynamic Testing, Non-Destructive Testing (NDT), Functional Testing, and Performance & Safety Testing), By Service Type (In-house Testing and Third-party Testing & Certification Services), By System Type (Rolling Stock, Track & Civil Infrastructure, Signaling & Communication Systems, Electrification Systems, & Integrated System Testing), By End Use (OEMs, Railway Operators, and Maintenance & Service Providers), By Application (High-speed Rail, Metro & Light Rail, & Others), and Regional Forecast, 2026-2034

Railway Testing Market Size and Future Outlook

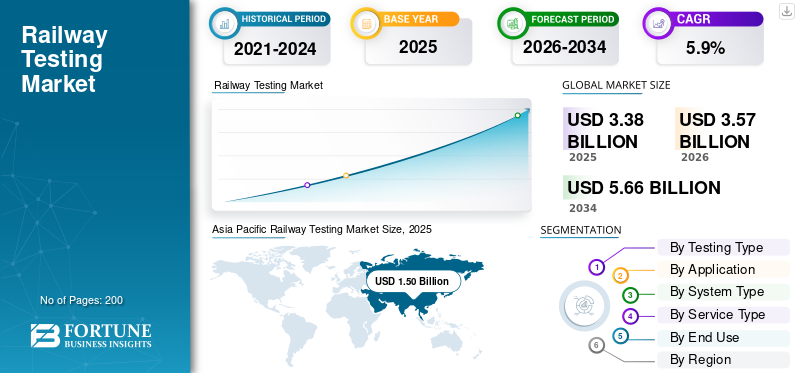

The global railway testing market size was valued at USD 3.38 billion in 2025. The market is projected to grow from USD 3.57 billion in 2026 to USD 5.66 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. Asia Pacific dominated the railway testing market with a market share of 44.37% in 2025.

Railway testing refers to the systematic evaluation of rolling stock, infrastructure, signaling, and electrification systems to ensure safety, performance, compliance, and reliability before deployment, operation, or maintenance within railway networks. Market growth is driven by increasing rail infrastructure investments, rising demand for safety and compliance, expansion of high-speed rail networks, technological advancements, and stringent government regulations ensuring efficient and reliable railway operations.

Major players in the market include TÜV SÜD, SGS SA, Bureau Veritas, Intertek Group plc, Ricardo plc, and Alstom, competing through advanced testing capabilities, digital simulation, regulatory expertise, and integrated system validation solutions.

Download Free sample to learn more about this report.

Railway Testing Market Key Takeaways

- 2025 Market Size: USD 3.38 billion

- 2026 Market Size: USD 3.57 billion

- 2034 Forecast Market Size: USD 5.66 billion

- CAGR: 5.9% from 2026–2034

- Asia Pacific dominated the railway testing market with a 44.37% share in 2025.

- The high-speed rail segment is projected to grow at a CAGR of 7.3% during the forecast period.

- The integrated system testing segment is anticipated to expand at a CAGR of 7.2% over the study period.

Asia Pacific

Asia Pacific led the global market in 2025, supported by rapid high-speed rail expansion, infrastructure modernization, and increasing government investments in railway development.

Europe

Europe held the second-largest market share, driven by stringent rail safety regulations, modernization of aging rail infrastructure, and cross-border interoperability requirements.

North America

North America represents the third-largest market, supported by strong freight rail networks, infrastructure upgrade programs, and rising adoption of predictive maintenance technologies.

U.S.

The U.S. railway testing market is estimated at around USD 0.51 billion in 2026, driven by infrastructure investments, freight rail dominance, and increasing safety compliance requirements.

Japan

Japan’s market is projected to reach approximately USD 0.22 billion in 2026, supported by advanced rail technologies and strict railway safety standards.

Read More

RAILWAY TESTING MARKET TRENDS

Adoption of Digital Twins and Simulation-Based Testing to Transform Validation Processes

The market is witnessing a strong shift toward digital twin technology and simulation-based validation. These tools enable real-time replication of railway systems, allowing engineers to test performance, detect faults, and optimize operations without physical trials. Market trends such as these reduces testing time, lowers costs, and enhances predictive maintenance capabilities. Increasing integration of AI and data analytics further strengthens testing accuracy. As rail networks become more complex, digital testing solutions are emerging as a critical component of modern railway validation frameworks.

- In July 2025, DB InfraGO developed a digital twin for autonomous rail operations, enabling AI training through simulated scenarios using NVIDIA Omniverse, ray-tracing GPUs, and sensor-based modeling, achieving up to 20x faster testing efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Investments in Rail Infrastructure and High-Speed Networks to Accelerate Market Growth

Global investments in rail infrastructure, particularly high-speed rail and metro projects, are significantly driving the railway testing market growth. Governments and private stakeholders are prioritizing efficient, safe, and sustainable transportation systems, leading to increased deployment of advanced testing solutions. The expansion of cross border rail networks and urban transit systems further necessitates rigorous validation processes. Additionally, funding initiatives and public-private partnerships are boosting project execution, thereby creating sustained demand for comprehensive testing, inspection, and certification services across the railway ecosystem.

- In March 2026, the California Transportation Commission allocated USD 848 million for rail and transit projects, including USD 100 million for a 5-mile BART tunnel between San Jose and Santa Clara, supported by federal IIJA and Senate Bill 1 funding.

MARKET RESTRAINTS

High Capital Requirements and Complex Testing Procedures to Limit Market Expansion

The market faces challenges due to high capital investments required for advanced testing equipment, electrification testing equipment, and infrastructure. Establishing testing facilities, acquiring specialized tools, and maintaining skilled personnel contribute to significant operational costs. Moreover, complex and time-consuming testing procedures can delay project timelines, impacting overall efficiency. Smaller players often struggle to compete due to limited financial and technical capabilities. These factors collectively act as barriers to entry and expansion, particularly in developing regions where budget constraints and resource limitations are more prominent.

MARKET OPPORTUNITIES

Emergence of Smart Rail Systems and Automation to Create New Growth Opportunities

The growing adoption of smart rail systems and automation technologies presents significant opportunities for the market. Integration of IoT, AI, and advanced communication systems in rail operations requires specialized testing to ensure seamless performance and cybersecurity. Automated train control, predictive maintenance systems, measurement systems and intelligent signaling solutions are expanding the scope of testing services. As rail operators increasingly focus on digital transformation, the demand for innovative testing methodologies and real-time monitoring systems solutions is expected to rise, opening new avenues for market players.

- In December 2025, Siemens Mobility launched the RemODtrAIn project, developing 5G-enabled remote-controlled trains with AI-based obstacle detection, tested on ICE 4 and Desiro Classic, integrating modular safety architecture and virtual radar-based validation systems.

MARKET CHALLENGES

Regulatory Variability and Standardization Challenges to Impact Global Testing Consistency

One of the key challenges in the market is the variation in regulatory standards across different countries and regions. Diverse compliance requirements make it difficult for companies to implement uniform testing procedures globally. This lack of standardization increases operational complexity and may lead to delays in project approvals. Additionally, adapting to evolving rail safety norms and certification processes requires continuous updates in testing methodologies. These factors create challenges for service providers aiming to maintain consistency and efficiency in international railway projects.

Segmentation Analysis

By Testing Type

Increasing Need for Real-Time Validation and On-Track Assessment to Propel Dynamic Testing Segmental Dominance

Based on testing type, the market is segmented into static testing, dynamic testing, non-destructive testing (NDT), functional testing, and performance & safety testing.

The dynamic testing segment dominates the market due to its critical role in evaluating real-world railway performance under operational conditions. It ensures system reliability, safety, and compliance by assessing rolling stock, signaling, and infrastructure in motion. The growing deployment of high speed rail and metro systems increases the need for continuous on-track validation. Additionally, integration of advanced monitoring technologies and real-time diagnostics further strengthens the importance of dynamic testing across modern railway networks.

- In August 2025, Maryland’s Purple Line initiated expanded dynamic testing of light rail vehicles across a 1.5-mile section, evaluating acceleration, braking, and operational performance under real conditions, with controlled traffic management and certified operator-led validation.

The performance & safety testing segment is the second-largest, projected to grow at a CAGR of 6.0% over the forecast period. Increasing emphasis on passenger safety, regulatory compliance, and certification standards is driving demand for rigorous validation of braking, crashworthiness, and operational safety testing systems.

To know how our report can help streamline your business, Speak to Analyst

By Application

Extensive Network Utilization and Continuous Modernization to Propel Conventional Passenger Rail Segmental Dominance

Based on application, the market is segmented into high-speed rail, metro & light rail, freight rail, and conventional passenger rail.

The conventional passenger rail segment dominates the market due to its widespread global presence and continuous operational demand. These networks require regular testing of rolling stock, signaling systems, and infrastructure to ensure safety and reliability. Aging rail assets, increasing passenger volumes, and ongoing modernization programs drive consistent testing requirements. Additionally, government investments in upgrading existing rail corridors further sustain demand for comprehensive testing services across conventional passenger rail systems.

The high-speed rail segment is projected to grow at a CAGR of 7.3% over the forecast period. Increasing investments in high-speed corridors and cross-border connectivity are driving advanced testing needs for speed, safety, and system integration.

By System Type

Extensive Infrastructure Development and Maintenance Requirements to Propel Track & Civil Infrastructure Segmental Dominance

Based on system type, the market is segmented into rolling stock, track & civil infrastructure, signaling & communication systems, electrification systems, and integrated system testing.

The track & civil infrastructure segment dominates the market due to its foundational role in railway operations and continuous maintenance requirements. Rail tracks, bridges, tunnels, and related civil structures require frequent inspection and testing to ensure structural integrity and safety. Increasing investments in rail network expansion, rehabilitation of aging infrastructure, and urban transit development further drive demand for comprehensive testing services in this segment.

- In February 2026, MxV Rail advanced its FAST facility, enabling accelerated testing of track geometry and mechanical components under 18,000-ton trains, simulating over 140 million gross tons annually on a 2.8-mile loop with controlled alignment and load conditions.

The integrated system testing segment is projected to grow at a CAGR of 7.2% over the forecast period. Rising system complexity and the need for seamless interoperability between subsystems are driving demand for end-to-end validation solutions.

By Service Type

Established Internal Capabilities and Cost Control to Propel In-house Testing Segmental Dominance

Based on service type, the market is segmented into in-house testing and third-party testing & certification services.

The in-house testing segment dominates the market as major railway operators and OEMs prefer internal capabilities to maintain control over testing processes, timelines, and costs. In-house facilities enable continuous monitoring, faster validation, and better integration with development cycles. Large-scale rail projects and advanced manufacturing setups further support internal testing infrastructure, ensuring compliance with safety standards while reducing dependency on external service providers.

- In November 2025, the MTA opened a railcar acceptance and testing facility in New York, enabling integrated inspection, commissioning, and CBTC-compatible validation of over 1,500 new subway cars with direct network connectivity.

The third-party testing & certification services is the fastest growing segment, projected to grow at a CAGR of 6.5% over the forecast period. Increasing regulatory complexity and the need for independent validation are driving demand for specialized certification bodies and external expertise.

By End Use

Extensive Operational Responsibility and Continuous Asset Monitoring to Propel Railway Operators' Segmental Dominance

Based on end use, the market is segmented into OEMs, railway operators, and maintenance & service providers.

The railway operators segment dominates the market due to their direct responsibility for ensuring safe, reliable, and efficient rail operations. Operators require continuous testing of rolling stock, infrastructure, and signaling systems to maintain service quality and comply with regulatory standards. Increasing passenger volumes, network expansions, and modernization initiatives further drive ongoing testing needs, making operators the primary contributors to overall testing demand across railway networks globally.

- In March 2026, Trenitalia initiated homologation of Frecciarossa high-speed trains for Italy, Germany routes, involving cross-border certification, interoperability testing, and adaptation to multi-system signaling and power standards ahead of planned 2027 operations.

The OEMs segment is projected to grow at a CAGR of 6.6% over the forecast period. Rising production of advanced rail systems and integration of new technologies are increasing the need for comprehensive testing during design and manufacturing stages.

Railway Testing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Railway Testing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is also the fastest-growing region due to large-scale investments in railway infrastructure, particularly in China, India, and Southeast Asia. Governments are prioritizing high-speed rail, metro expansion, and cross-border connectivity, significantly increasing testing requirements. Rapid urbanization and population growth further drive demand for efficient public transport systems. Additionally, strong policy support and funding initiatives accelerate project execution, boosting demand for advanced testing, inspection, and certification services across the region.

- In March 2025, Singapore’s LTA inaugurated the 50-hectare SRTC, featuring 2.8-km high-speed and performance tracks and a 3-km endurance loop, enabling multi-system testing with third-rail and overhead power for comprehensive railway validation.

China Railway Testing Market

The China market is estimated at around USD 0.75 billion in 2026, accounting for roughly 21.0% of global revenues. Growth is driven by extensive high-speed rail expansion, government funding, and continuous infrastructure modernization projects.

Japan Railway Testing Market

The Japan market is estimated at around USD 0.22 billion in 2026, accounting for roughly 6.3% of global revenues. Advanced rail technologies and stringent safety standards support steady demand for sophisticated testing solutions.

India Railway Testing Market

The India market is estimated at around USD 0.27 billion in 2026, accounting for roughly 7.6% of global revenues. Rapid rail expansion, metro development, and modernization initiatives are accelerating demand for comprehensive testing services.

Europe

Europe holds the second-largest railway testing market share and is projected to grow at a CAGR of 5.5% over the forecast period. The region’s well-established rail network and stringent safety regulations drive continuous demand for testing services. Ongoing modernization of aging infrastructure and adoption of digital signaling systems further contribute to growth. Cross-border rail interoperability standards and sustainability goals also encourage advanced testing solutions, ensuring compliance and efficiency across diverse railway systems within the region.

- In March 2026, PKP initiated autonomous train testing using ATO-based systems, integrating digital twin simulations, onboard sensors, and visual recognition algorithms, with real-world trials on WKD Line 48 using GoA2-enabled EN97 trains.

Germany Railway Testing Market

The Germany market is estimated at around USD 0.24 billion in 2026, accounting for roughly 6.8% of global revenues. Strong regulatory frameworks and infrastructure upgrades are driving consistent demand for testing and certification services.

U.K. Railway Testing Market

The U.K. market is estimated at around USD 0.18 billion in 2026, accounting for roughly 5.1% of global revenues. Ongoing rail modernization and digital signaling adoption support increased testing requirements across networks.

North America

North America represents the third-largest market, driven by significant investments in rail infrastructure upgrades and the strong presence of freight rail networks. The region emphasizes safety compliance, asset reliability, and performance optimization, leading to steady demand for testing services. Increasing adoption of advanced technologies such as automated inspection and predictive maintenance further supports market growth. Government funding programs and private sector participation also play a crucial role in enhancing testing capabilities.

- In December 2024, CPKC tested a hydrogen-powered locomotive on heavy-haul coal routes, integrating fuel cells, onboard power management, and regenerative braking batteries to replace diesel engines, enabling low-emission operations in mountainous terrains.

U.S. Railway Testing Market

The U.S. market is estimated at around USD 0.51 billion in 2026, accounting for roughly 14.3% of global revenues. Infrastructure investments, freight rail dominance, and safety compliance needs drive sustained testing demand.

Rest of the World

The rest of the world region is witnessing gradual growth driven by emerging rail projects in Latin America, and the Middle East & Africa. Governments are investing in metro systems, freight corridors, and regional connectivity to support economic development. Although infrastructure is still developing, increasing focus on safety standards and international partnerships is boosting demand for testing services. Rising urbanization and foreign investments are expected to further accelerate market expansion in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Digital Integration, Regulatory Expertise, and Global Certification Networks Define Competitive Intensity

The market is moderately consolidated, with a mix of global certification bodies and specialized engineering firms competing across regions. Key players such as TÜV SÜD, SGS SA, Bureau Veritas, Intertek Group plc, Ricardo plc, and Alstom compete through advanced testing capabilities, digital simulation platforms, and regulatory expertise. Companies are focusing on integrated system validation, automation in testing processes, and expansion of global service networks. Strategic collaborations, technology investments, and regional partnerships help enhance capabilities and ensure compliance with evolving railway safety standards globally.

- In February 2026, TÜV SÜD acquired Finland-based PTI provider Suomen Katsastusasemat, expanding inspection services across 11 stations and leveraging AI-driven digital processes to enhance testing, certification capabilities, and regional market presence.

LIST OF KEY RAILWAY TESTING COMPANIES PROFILED IN REPORT

- TÜV SÜD (Germany)

- SGS SA (Switzerland)

- Bureau Veritas (France)

- Intertek Group plc (U.K.)

- Ricardo plc (U.K.)

- Alstom SA (France)

- Siemens Mobility (Germany)

- Hitachi Rail Ltd. (Japan)

- Wabtec Corporation (U.S.)

- Knorr-Bremse AG (Germany)

- DB Systemtechnik GmbH (Germany)

- Mott MacDonald (U.K.)

- RINA S.p.A. (Italy)

- Applus+ (Spain)

- SYSTRA (France)

KEY INDUSTRY DEVELOPMENTS

- March 2026:K. tested a Quantum Inertial Navigation System (RQINS) on a mainline train, using ultra-sensitive sensors to track motion and position without GPS, enabling resilient real-time navigation in tunnels and dense urban environments.

- March 2026: TÜV SÜD published an assessment guide for alternative rail propulsion systems, outlining holistic safety evaluation frameworks covering hydrogen and battery drives, including hazard analysis, risk assessment, and system-level validation for regulatory compliance.

- February 2026: TÜV SÜD issued ISO 14067:2018 verification for Yokogawa’s electronic devices, validating lifecycle carbon footprint calculations from raw materials to production, supporting digital product passport compliance, and enhancing sustainability transparency through certified emissions reporting.

- November 2025: TÜV SÜD supported approval of Talgo 230 (ICE-L) high-speed trains, performing NoBo, DeBo, and AsBo roles, ensuring TSI compliance, risk assessment under CSM RA, and certification for multi-country European rail operations.

- November 2025: Europe launched the Arctic Test Arena, a 473 km rail testing platform enabling extreme-climate validation using advanced sensors for structural monitoring and operations at temperatures as low as –30°C, enhancing resilience and performance.

- November 2025: Intertek acquired U.S.-based Professional Testing Laboratory (PTL), expanding its ATIC portfolio with advanced flooring material testing capabilities, leveraging a 30,000 sq. ft. lab to enhance quality assurance and regulatory compliance services.

- July 2025: TÜV SÜD conducted derailment tests for digital automatic couplers in Görlitz, applying 550 kN horizontal forces in S-curve conditions to evaluate safety, interoperability, and real-time performance monitoring across multi-vendor systems.

REPORT COVERAGE

The global railway testing market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.9% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Testing Type, By Application, By System Type, By Service Type, By End Use, and By Region |

| By Testing Type |

|

| By Application |

|

| By System Type |

|

| By Service Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.38 billion in 2025 and is projected to reach USD 5.66 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.50 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period of 2026-2034.

The conventional passenger rail segment leads the market in terms of application.

Rising investments in rail infrastructure and high-speed networks are expected to accelerate market growth.

Major players in the market include TÜV SÜD, SGS SA, Bureau Veritas, Intertek Group plc, Ricardo plc, and Alstom.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us