Rapid Test Kits Market Size, Share & Industry Analysis, By Technology (Lateral Flow Immunoassay, Agglutination-based Rapid Tests, Rapid Molecular Tests, Rapid Biochemical, and Others), By Sample Type (Blood, Nasopharyngeal, Urine, Saliva, and Others), By Application (Infectious Disease Testing, Pregnancy & Fertility Testing, Cardiac Marker Testing, Diabetes & Metabolic Testing, Toxicology Testing, and Others), By End-user (Hospitals & Clinics, Diagnostic Laboratories, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Rapid Test Kits Market Size and Future Outlook

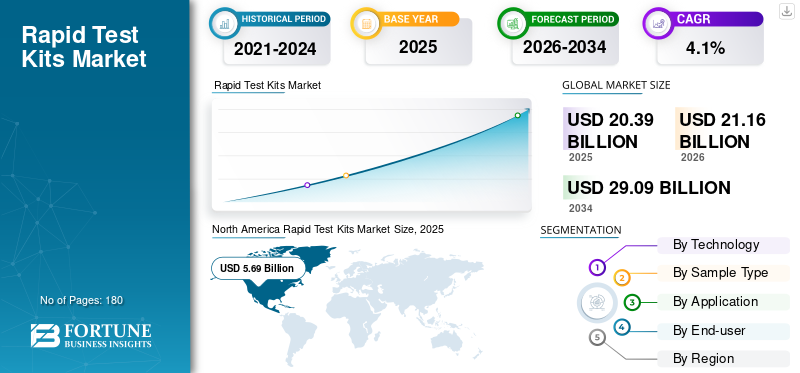

The global rapid test kits market size was valued at USD 20.39 billion in 2025. The market is projected to grow from USD 21.16 billion in 2026 to USD 29.09 billion by 2034, exhibiting a CAGR of 4.1% during the forecast period. North America dominated the rapid test kits market with a market share of 27.91% in 2025.

The global rapid test kits market comprises diagnostic kits that deliver quick results for disease screening, monitoring, and routine health assessment without requiring complex laboratory infrastructure. These kits are widely used for infectious disease testing, pregnancy and fertility testing, cardiac marker detection, diabetes and metabolic monitoring, toxicology screening, and other point-of-care applications. The market is growing as healthcare systems shift toward faster diagnosis, early intervention, decentralized testing, and home-based health monitoring. Demand has also increased due to the wider acceptance of self-testing after the COVID-19 pandemic, rising chronic disease prevalence, and the need for affordable diagnostics in both developed and emerging markets. Rapid biochemical products, glucose strips, urine-based tests, and lateral flow assays continue to see strong adoption as they are easy to use, cost-effective, and suitable for high-volume testing. Expansion of retail pharmacies, digital health platforms, and public screening programs is further supporting market growth.

Abbott Laboratories, F. Hoffmann-La Roche Ltd., LifeScan, Inc., Ascensia Diabetes Care Holdings AG, and Siemens Healthineers held the largest market share, driven by increased investments and strategic initiatives, including new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

RAPID TEST KITS MARKET TRENDS

Multiplex, Digital, and Consumer-friendly Rapid Testing is Reshaping Product Development

The market is moving toward rapid test kits that are easier to use, more informative, and better connected to healthcare decision-making. One of the most visible trends is the development of multiplex rapid tests, especially for respiratory infections, which can help distinguish between conditions with similar symptoms. This trend is also emerging in toxicology, fertility, cardiac, and infectious disease panels.

Another important trend is the integration of digital tools, such as smartphone-based reading, QR-enabled instructions, cloud reporting, and app-based result tracking. These features help reduce user error, improve recordkeeping, and support telehealth workflows. In homecare settings, packaging and usability have become more important, as consumers expect simple sample collection, quick interpretation, and reliable guidance on next steps. At the same time, hospitals and clinics are adopting rapid tests that fit into triage and workflow protocols, especially where quick decisions are needed. Companies are also focusing on compact formats, better stability, room-temperature storage, and longer shelf life to support distribution in emerging markets. Overall, the market is evolving from basic single-use strips and cassettes toward more convenient, connected, and condition-specific testing solutions.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Quick, Accessible, and Decentralized Diagnostics is Accelerating Market Expansion

The rapid test kits market growth is being driven by the growing need for diagnostic solutions that provide timely results at the point of care, in homes, pharmacies, clinics, and community health settings. Traditional laboratory testing remains essential, but it often involves sample transportation, longer turnaround times, skilled personnel, and higher infrastructure costs. Rapid test kits address these gaps by allowing patients and healthcare providers to make quicker decisions, particularly in infectious disease management, diabetes monitoring, pregnancy confirmation, toxicology screening, and emergency care. The increasing burden of chronic diseases is also strengthening demand for routine and repeat testing, especially glucose strips, ketone strips, urinalysis strips, and other metabolic testing products.

Patients have become more comfortable with self-testing after widespread use of COVID-19 antigen tests, creating a lasting behavioral shift toward at-home diagnostic. Hospitals and clinics are also using rapid kits to reduce diagnostic delays, support triage, and improve workflow efficiency. In emerging markets, rapid kits are valuable as they offer affordable testing where access to centralized laboratories is limited. These combined factors are making rapid test kits an important part of modern diagnostic delivery.

MARKET RESTRAINTS

Accuracy Concerns and Regulatory Scrutiny Can Limit Wider Adoption

Despite strong demand, the market faces constraints due to concerns about test accuracy, quality variation, and regulatory oversight. Rapid test kits are often designed for ease of use and speed, but this can sometimes involve trade-offs in sensitivity, specificity, or performance compared with advanced laboratory-based diagnostics. False positives or false negatives can create clinical risk, especially in infectious disease testing, cardiac marker testing, and toxicology screening, where results may influence urgent treatment decisions. Performance may also vary depending on sample collection technique, storage conditions, timing of testing, and user interpretation. This is particularly relevant for home-use tests, where consumers may not always follow instructions correctly. Regulatory agencies have therefore become more cautious in reviewing rapid diagnostic claims, especially after the large influx of COVID-19 tests during the pandemic.

Manufacturers must invest in validation studies, quality control, labeling improvements, and post-market surveillance, which can raise development costs and delay commercialization. Price competition from low-cost manufacturers further adds pressure, as buyers may demand affordability while regulators and healthcare providers expect reliable performance. These factors can limit adoption in higher-risk clinical applications and make procurement decisions more selective.

MARKET OPPORTUNITIES

Home Testing, Chronic Disease Monitoring, and Emerging Markets Offer Strong Growth Potential

A major opportunity for the market lies in the continued expansion of home-based and near-patient testing. Consumers are increasingly willing to manage routine health needs outside traditional healthcare facilities, particularly for pregnancy testing, fertility tracking, glucose monitoring, ketone testing, urinalysis, and selected infectious disease tests. This shift creates opportunities for companies to develop more user-friendly kits with clearer instructions, digital result interpretation, app connectivity, and subscription-based replenishment models.

Chronic disease monitoring represents another attractive opportunity, as diabetes, kidney disease, cardiovascular risk, and metabolic disorders require frequent testing over long periods. In emerging markets, rapid kits can help bridge diagnostic access gaps by enabling screening in rural clinics, pharmacies, mobile health units, and public health programs. Governments and NGOs are also expected to continue using rapid tests for infectious diseases, maternal health, and community-level screening. Manufacturers that can offer affordable, accurate, and scalable products will be well-positioned in these regions. There is also room for growth in multiplex testing, where a single kit can detect multiple conditions or markers, improving convenience and value. Together, these opportunities can expand the market beyond episodic infectious disease testing into broader preventive and routine healthcare use.

MARKET CHALLENGES

Pricing Pressure, Fragmented Competition, and Post-pandemic Demand Normalization Create Uncertainty

The market faces several challenges that can affect revenue growth and profitability. One of the biggest challenges is pricing pressure, especially in high-volume categories such as glucose strips, pregnancy tests, infectious disease kits, and urine-based rapid tests. Many products are relatively mature and have several competing suppliers, which limits manufacturers’ ability to raise prices. Public tenders, centralized procurement, and reimbursement controls further compress margins, particularly in Europe, Asia Pacific, Latin America, and parts of the Middle East & Africa. The market is also highly fragmented, with multinational companies competing against regional and low-cost manufacturers. This makes differentiation difficult unless companies can demonstrate better accuracy, usability, regulatory approvals, or brand trust.

Another challenge is post-pandemic normalization. COVID-19 created a temporary surge in demand for rapid testing, but many countries have since reduced routine testing volumes, causing volatility in revenue for companies that benefited from pandemic-related sales. At the same time, demand is shifting toward broader respiratory testing, chronic disease monitoring, and home diagnostics, requiring companies to adjust portfolios. Supply chain reliability, quality assurance, and regulatory compliance remain additional challenges, especially for companies operating across multiple regions with different approval standards.

Segmentation Analysis

By Technology

Rapid Biochemical Segment Leads Market as Routine Metabolic Monitoring Drives Repeat Demand

Based on technology, the market is segmented into lateral flow immunoassay, agglutination-based rapid tests, rapid molecular tests, rapid biochemical, and others.

Rapid biochemical tests hold the highest rapid test kits market share as they are widely used across large, recurring testing categories, such as glucose monitoring, ketone testing, urinalysis, kidney function screening, and other metabolic assessments. The inclusion of glucose strips, ketone strips, and urine reagent strips under the broad rapid test kits scope significantly strengthens this segment.

The rapid molecular tests segment is projected to grow at a CAGR of 7.0% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Sample Type

Urine Leads Due to Its Convenience, Non-Invasive Collection, and Wide Application Base

By sample type, the market is classified into blood, nasopharyngeal, urine, saliva, and others.

Urine holds the highest share as it is easy to collect, non-invasive, and suitable for several high-volume rapid testing applications. Pregnancy and fertility tests, toxicology panels, urinalysis strips, glucose/protein screening, ketone testing, and kidney-related assessments commonly rely on urine samples. This makes urine-based testing highly relevant across homecare, hospitals, clinics, workplaces, and diagnostic laboratories. Moreover, the segment is projected to hold a 41.4% share in 2026.

The saliva segment is estimated to grow at a CAGR of 7.9% during the forecast period.

By Application

Diabetes and Metabolic Testing Dominates Due to Chronic Disease Burden and Repeat Testing Needs

By application, the market is classified into infectious disease testing, pregnancy & fertility testing, cardiac marker testing, diabetes & metabolic testing, toxicology testing, and others.

Diabetes and metabolic testing holds the highest share as they involve frequent, recurring use rather than one-time testing. Within the broader market, this segment includes glucose strips, ketone strips, urinalysis/metabolic strips, rapid HbA1c kits, lipid testing, and other rapid biochemical tests. Diabetes patients often require regular monitoring, while hospitals and clinics use rapid metabolic testing to support diagnosis, treatment decisions, and ongoing care. Rising diabetes prevalence, growing awareness of metabolic health, and the shift toward home-based monitoring continue to support demand. Moreover, the segment is projected to hold a 42.9% share in 2026.

The toxicology testing segment is estimated to grow at a CAGR of 6.0% during the forecast period.

By End-user

Hospitals & Clinics Lead as Rapid Testing Supports Immediate Clinical Decisions

On the basis of end-user, the market is hospitals & clinics, diagnostic laboratories, homecare settings, and others.

Hospitals & clinics holds the highest share as rapid test kits are widely used for triage, diagnosis, monitoring, and treatment decisions across multiple departments. Emergency care units, outpatient clinics, maternity departments, infectious disease units, cardiology settings, and diabetes clinics all use rapid tests to shorten waiting times and support faster patient management. Furthermore, the segment is set to hold 37.5% share in 2026.

The homecare settings segment is projected to grow at a CAGR of 4.4% during the forecast period.

Rapid Test Kits Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Rapid Test Kits Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 5.54 billion, and reached USD 5.69 billion in 2025. North America’s growth is supported by strong adoption of point-of-care and home-based testing, high healthcare spending, and broad use of rapid test kits across diabetes monitoring, respiratory infections, toxicology, fertility testing, and cardiac care. The U.S. remains the key revenue contributor due to higher average selling prices, established reimbursement pathways for selected diagnostics, and a large patient base requiring frequent metabolic testing.

U.S. Rapid Test Kits Market

In 2026, the U.S. market is expected to represent USD 5.24 billion, capturing 24.7% of total global revenues.

Europe

Europe is expected to achieve a 2.4% growth rate in the coming years, the second-highest globally, reaching USD 5.24 billion in 2026. Europe’s growth is driven by steady demand for rapid diagnostics across chronic disease monitoring, infectious disease screening, pregnancy and fertility testing, and hospital-based point-of-care testing. Countries such as Germany, the U.K., France, Italy, and Spain have well-developed healthcare systems and large diabetic and aging populations, supporting regular use of rapid biochemical and urine-based tests.

U.K. Rapid Test Kits Market

The U.K. market is projected to reach USD 0.92 billion in 2026, accounting for 4.3% of the global revenues.

Germany Rapid Test Kits Market

Germany's market is expected to reach about USD 1.15 billion in 2026, representing roughly 5.4% of global revenues.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 5.03 billion, ranking as the third-largest globally. Asia Pacific is expected to grow faster due to its large patient population, rising diabetes prevalence, improved healthcare access, and increased adoption of affordable rapid diagnostic kits. China, India, Japan, Australia, South Korea, and Southeast Asian countries are seeing growing use of rapid tests for diabetes and metabolic monitoring, infectious disease detection, pregnancy and fertility testing, and routine screening.

Japan Rapid Test Kits Market

Japan is projected to generate approximately USD 1.14 billion in revenue in 2026, contributing nearly 5.4% to global revenues.

China Rapid Test Kits Market

China’s market is set to reach approximately USD 1.56 billion in 2026, contributing about 7.4% to global revenues.

India Rapid Test Kits Market

India is expected to reach USD 0.77 billion in 2026, corresponding to about 3.6% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate market growth, with Latin America expected to reach around USD 1.94 billion in 2026. Latin America’s growth is supported by rising demand for affordable, accessible diagnostic solutions, particularly for diabetes monitoring, infectious disease screening, pregnancy testing, and toxicology testing. Brazil and Mexico are the major contributors due to their large populations, expanding private healthcare sectors, and rising chronic disease burden.

The Middle East & Africa market is growing due to a combination of infectious disease testing needs, diabetes prevalence, expanding healthcare infrastructure, and public health screening programs. In Africa, rapid test kits are important for malaria, HIV, hepatitis, respiratory infections, and maternal health screening, especially in areas where laboratory access is limited. In the Middle East, particularly the GCC countries, market growth is supported by higher healthcare spending, modernization of hospitals and clinics, and increasing demand for diabetes and metabolic testing.

GCC Rapid Test Kits Market

In 2026, the GCC is expected to generate approximately USD 0.99 billion in the market, accounting for nearly 4.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce Market Positions of Prominent Players

The global rapid test kits market is moderately fragmented, with a mix of large multinational diagnostics companies, diabetes care specialists, point-of-care testing providers, and low-cost regional manufacturers. Leading players such as Abbott Laboratories, F. Hoffmann-La Roche Ltd., LifeScan, Inc., Ascensia Diabetes Care Holdings AG, and Siemens Healthineers compete across rapid infectious disease tests, glucose strips, urine-based tests, cardiac markers, toxicology, pregnancy/fertility kits, and rapid molecular diagnostics. Top companies hold significant market share due to strong brands, regulatory approvals, global distribution networks, hospital contracts, and broad product portfolios.

Other key players, such as QuidelOrtho Corporation, Danaher Corporation, Becton, Dickinson and Company, and SD Biosensor, Inc., compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve procedural outcomes.

LIST OF KEY RAPID TEST KIT COMPANIES PROFILED

- Abbott Laboratories (U.S.)

- Hoffmann-La Roche Ltd. (Switzerland)

- LifeScan, Inc. (U.S.)

- Ascensia Diabetes Care Holdings AG (Switzerland)

- Siemens Healthineers AG (Germany)

- QuidelOrtho Corporation (U.S.)

- Danaher Corporation (U.S.)

- Becton, Dickinson and Company (U.S.)

- SD Biosensor, Inc. (South Korea)

- ARKRAY, Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS

- July 2025: BD received FDA 510(k) clearance for the BD Veritor System for SARS-CoV-2, a rapid point-of-care COVID-19 antigen test designed to provide results in about 15 minutes.

- July 2024: Hoffmann-La Roche Ltd. completed the acquisition of LumiraDx’s point-of-care technology, expanding its POC diagnostics platform across clinical chemistry, immunochemistry, coagulation, and molecular testing.

- April 2024: FDA cleared ACON’s Flowflex COVID-19 Antigen Home Test through the traditional premarket pathway; FDA described it as the first OTC COVID-19 antigen home test cleared for marketing.

- April 2024: QuidelOrtho received FDA 510(k) clearance for the QuickVue COVID-19 Test, supporting use in home and CLIA-waived medical facility settings.

- August 2023: BD received FDA 510(k) clearance for its COVID-19, Influenza A/B, RSV molecular combination test for the BD MAX System.

REPORT COVERAGE

The rapid test kits market report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology, Sample Type, Application, End-user, and Region |

| By Technology |

|

| By Sample Type |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 20.39 billion in 2025 and is projected to reach USD 29.09 billion by 2034.

In 2025, the market value in North America stood at USD 5.69 billion.

The market is expected to exhibit a CAGR of 4.1% during the forecast period of 2026-2034.

The rapid biochemical segment leads the market by technology.

The key factor driving the market is the rising demand for quick, accessible, and decentralized diagnostics.

Abbott Laboratories, F. Hoffmann-La Roche Ltd., LifeScan, Inc., Ascensia Diabetes Care Holdings AG, and Siemens Healthineers are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us