Retail Banking Market Size, Share & Industry Analysis, By Type (Public Sector Banks, Private Sector Banks, Foreign Banks, and Community Development or Cooperative Banks), By Service Type (Deposits & Accounts, Retail Lending & Financing, Cards & Payments, Wealth Management & Investment Services, Insurance & Bancassurance, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

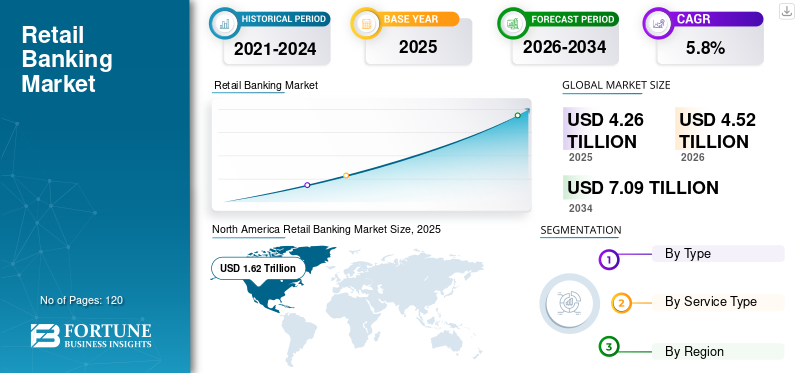

The global retail banking market size was valued at USD 4.26 trillion in 2025. The market is projected to grow from USD 4.52 trillion in 2026 to USD 7.09 trillion by 2034, exhibiting a CAGR of 5.8% during the forecast period. North America dominated the global retail banking market with a market share of 38.02% in 2025.

The retail banking sector is witnessing consistent growth driven by heightened consumer interest in digital banking services, growing smartphone and internet accessibility, economic development, and the implementation of advanced technologies, such as AI and data analytics. The increasing middle-class demographics and initiatives aimed at enhancing financial inclusion are driving up retail banking services. Moreover, tailored and personalized products, comprehensive omnichannel banking approaches, and favorable regulatory environments are enhancing customer engagement and contributing to market growth.

- For instance, in July 2025, HSBC opened its retail banking branch in India. This expansion aimed to strengthen the bank’s retail presence by offering services such as savings and current accounts, personal loans, and wealth management solutions.

Additionally, several major industry stakeholders, including HSBC, JP Morgan Chase, Emirates NBD, Standard Chartered, Commonwealth Bank of Australia, CaixaBank, and Bank of China, are active in the global market. These key players are emphasizing a digital-first and omnichannel banking approach to improve customer relationships and scale operations effectively.

Download Free sample to learn more about this report.

RETAIL BANKING MARKET TRENDS

Rising Cyber Threats and Technology Disruptions Driving Stronger Digital Resilience Emerges as a Market Trend

As financial institutions become increasingly reliant on digital platforms, even minor technology disruptions can have significant consequences for customers, revenues, and trust. The rising frequency of cyberattacks, system failures, and issues with third-party technologies is prompting traditional banks to enhance their digital operational resilience. This involves implementing strong cybersecurity measures, continuous monitoring, and swift recovery capabilities to maintain uninterrupted services.

- For example, in March 2022, JPMorgan Chase announced an investment increase in its cybersecurity technology as part of its strategy to combat rising cyber threats. The retail banking giant committed approximately USD 15 billion annually to technology, with a considerable share allocated to cybersecurity, fraud prevention, and digital resilience across its consumer banking platforms.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Financial Inclusion Initiatives Driving Broader Access and Growth in Retail Banking Demand

Government-driven initiatives for financial inclusion, combined with regulatory backing, are significantly increasing the demand for retail banking services, particularly in developing countries. These factors aim to integrate untapped and underbanked individuals by providing access to fundamental savings accounts, payment options, and credit facilities. The implementation of streamlined KYC regulations, digital identity frameworks, and Direct Benefit Transfer (DBT) programs by governments has further increased account ownership and access to retail banking. The increasing number of account holders drives demand for deposits, micro-loans, insurance, and digital payment solutions. This broadens the retail customer market and opens up long-term growth prospects for financial institutions.

- For instance, in 2025, Wells Fargo continued its decade-long Banking Inclusion Initiative, which aims to expand access to affordable banking services for unbanked and underbanked communities across the U.S.

MARKET RESTRAINTS

Rising Cybersecurity Risks and Regulatory Pressure Limiting Market Growth

Digitalization in retail banking has significantly heightened vulnerability to cyberattacks, data breaches, and fraud, posing a considerable obstacle to retail banking market growth. As cyber threats evolve in complexity, banks are compelled to invest in robust security systems, compliance measures, and risk management strategies. Concurrently, increasing regulatory demands elevate operational intricacies and expenses, particularly for smaller financial institutions.

MARKET OPPORTUNITIES

Fintech Collaboration and Open Banking Adoption Offers Market Growth Opportunities

The adoption of fintech solutions alongside open banking systems is generating significant growth prospects for retail banks. By exposing APIs and partnering with fintech companies, banks can introduce innovative offerings such as digital payments, instant loans, and personal finance applications. This will improve customer experience while reducing the time needed to bring new services to market. Open banking also facilitates a more effective use of customer data (with consent), enhancing personalization and opportunities for cross-selling. Consequently, retail banks can broaden their revenue sources and stay competitive in a rapidly changing digital environment.

- For instance, in June 2022, HSBC accelerated its open banking and fintech collaboration strategy by expanding API-based partnerships across payments, lending, and personal finance management. The bank invested its significant portion of its USD 6 billion technology budget, allocating funds to open banking platforms and digital innovation.

MARKET CHALLENGES

Legacy IT Infrastructure Increasing Transformation Costs and Operational Risk to Create Market Challenges

Few retail banks still depend on outdated core banking systems that lack adaptability and scalability. Several legacy systems hinder the integration of new digital services, delay response to customer demands, and restrict competition with fintech companies. During the transformation process, banks also encounter increased risks of service interruptions and customer dissatisfaction. Consequently, legacy IT poses a significant structural obstacle to growth and innovation in this sector.

- For instance, in August 2024, Banco do Brasil encountered significant challenges related to its legacy IT infrastructure while attempting to accelerate its digital transformation. The bank announced plans to invest approximately USD 600 million through 2026 to modernize its core banking systems and improve digital service delivery.

Segmentation Analysis

By Type

Digital Agility and Diversified Offerings Driving Private Sector Banks Segment Growth

Based on the type, the market is divided into public sector banks, private sector banks, foreign banks, and community development or cooperative banks.

Private sector banks account for the largest revenue share in the market, due to their increasing focus on profitability, customer-centric, and innovative offerings. Private sector banks adopt advanced digital technologies faster than public or cooperative banks, enabling efficient service offerings and lower operating costs. These banks provide diversified product portfolios spanning retail lending, credit cards, wealth management, and fee-based services, which help generate higher non-interest income. Additionally, agile decision-making, targeted marketing, and superior customer experience allow private sector banks to attract and retain high-value retail customers, driving sustained revenue growth.

- For instance, in January 2024, JPMorgan Chase reinforced its position as the largest private sector retail bank globally by reporting record revenues from its Consumer & Community Banking segment. The bank invested over USD 17 billion annually in technology and digital banking capabilities, enabling strong growth in deposits, credit cards, and consumer lending.

The private sector banks are anticipated to grow with the CAGR of 6.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Service Type

Strong Consumer Credit Demand and High Interest Yields Drives the Retail Lending & Financing Segment Growth

Based on service type, the market is segmented into deposits & accounts, retail lending & financing, cards & payments, wealth management & investment services, insurance & bancassurance, and others.

Retail lending & financing, which are further categorized into home loans and personal loans & mortgages, dominate the global market. Retail banking revenues are largely driven by lending and financing activities, as demand for credit remains consistently strong across housing, consumer spending, and automobile purchases. Offerings such as mortgages, personal credit, vehicle loans, and revolving credit facilities typically deliver greater interest earnings than standard deposit products. Factors including rapid urban growth, higher household incomes, and the convenience of digitally enabled lending have significantly increased borrowing activity. Moreover, extended repayment periods along with the bundling of insurance products and other fee-based services further strengthen margins, positioning retail lending as a primary source of bank profitability.

- For instance, in April 2024, India’s HDFC Bank reported that retail lending remained its largest revenue-generating segment, driven by strong growth in home loans, personal loans, and vehicle financing. The bank recorded double-digit growth in its retail loan book, primarily driven by increasing urban housing demand and consumer spending.

The cards and payments segment is expected to grow at the fastest pace within the market, owing to widespread adoption of digital payment method and reduced demand for cash transactions. The surge in online shopping, broader usage of debit and credit cards, and the increasing availability of contactless and mobile payment technologies are driving a steady rise in transaction activity. Alongside, government-backed public policies encouraging digital payment ecosystems and consumers’ growing demand for speed and ease are expected to further sustain this momentum, with the segment expanding at an estimated CAGR of about 7.2% during the forecast period.

Retail Banking Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Retail Banking Market Size, 2025 (USD Trillion) To get more information on the regional analysis of this market, Download Free sample

North America emerged as the leading regional market in 2025, generating revenues of approximately USD 1.62 trillion, and continued to remain dominant in 2026 with a valuation of USD 1.72 trillion. The region’s strong performance is supported by a well-established banking ecosystem, legacy infrastructure, extensive customer access to financial services, and the early embrace of digital banking innovations. Robust demand for consumer credit, along with the widespread adoption of card-based and digital payment solutions, has further strengthened the market. In addition, major privately owned banks with broad retail offerings play a key role in driving revenues. Ongoing investments in areas such as cybersecurity, artificial intelligence, and integrated omnichannel platforms continue to enhance North America’s competitive advantage.

U.S. Retail Banking Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market generated revenue of USD 1.28 trillion in 2025. Major private-sector banks such as JPMorgan Chase, Bank of America, and Wells Fargo generate substantial revenues from consumer banking, credit cards, and mortgages.

Europe

Europe is projected to grow at a rate of around 3.4% over the forecast period and is projected to reach a market size of approximately USD 0.99 trillion by 2026. The region’s retail banking landscape is relatively mature, marked by robust regulatory frameworks and broad access to financial services. Rising demand for digital payment solutions, established banking infrastructures, and the expanding implementation of open banking initiatives continue to support market development. At the same time, banks are largely emphasizing fee-driven offerings, wealth advisory services, and eco-friendly financial products.

U.K. Retail Banking Market

The U.K. retail banking market in 2026 is estimated at around USD 0.18 trillion, representing roughly 4.0% of global retail banking revenues.

Germany Retail Banking Market

Germany’s retail banking market is projected to reach approximately USD 0.20 trillion in 2026, equivalent to around 4.5% of global Retail Banking sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.56 trillion in 2026 in the global market. In the region, India and China are estimated to reach USD 0.31 trillion and USD 0.52 trillion, respectively, in 2026. Countries such as China, India, and Japan are experiencing strong demand for retail loans, payments, and basic banking services. Government-led financial inclusion initiatives and mobile-first banking models are boosting customer acquisition. The region’s young, tech-savvy population further supports long-term growth of retail banking.

Japan Retail Banking Market

The Japan retail banking market in 2026 is estimated at around USD 0.22 trillion, accounting for roughly 5.0% of global retail banking revenues.

China Retail Banking Market

China’s retail banking market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 0.52 trillion, representing roughly 11.6% of global retail banking sales.

India Retail Banking Market

The India retail banking market in 2026 is estimated at around USD 0.31 trillion, accounting for roughly 6.8% of global retail banking revenues.

South America

The South America region is expected to witness moderate growth in this market during the forecast period. The region is set to reach a valuation of USD 0.16 trillion in 2026. The market growth is supported by the increasing use of digital wallets, mobile payments, and consumer credit products.

Middle East & Africa

In the Middle East & Africa, banks are investing in fintech partnerships to reach underbanked populations and reduce operational costs. Governments and banks are promoting mobile banking, digital wallets, and Islamic banking products to expand access to financial services. Tech-savvy young population and growing smartphone penetration are driving the adoption of digital payments.

GCC Countries Retail Banking Market

The GCC Countries retail banking market is projected to reach around USD 0.04 trillion in 2026, representing roughly 0.9% of global retail banking revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Digital Accounts and Mobile-led Banking Models to Enhance Key Players’ Market Presence

The retail banking market is moderately consolidated, with a few key players including JPMorgan Chase, Bank of America, and HSBC, among others. These key players are strongly focusing on leveraging mobile banking, digital-first strategies, AI, and data analytics to expand their reach beyond their domestic geographies. In order to penetrate underbanked markets, these players are adopting financial inclusion initiatives, offering low-cost digital accounts, and implementing mobile-led banking models to expand their customer base. Additionally, regional players are collaborating with fintech firms to offer personalized products tailored to regional needs. This further helps banks scale efficiently and capture new retail customers in emerging markets.

- For instance, In July 2023, DBS Bank (Singapore) adopted a digital-first expansion strategy to strengthen its position in the market and penetrate underbanked customer segments. The bank focused on scaling its mobile-only banking services, AI-driven customer engagement tools, and paperless account opening to reach younger and digitally savvy consumers.

LIST OF KEY RETAIL BANKING COMPANIES PROFILED

- JPMorgan Chase (U.S.)

- Emirates NBD (UAE)

- Standard Chartered (U.K.)

- Commonwealth Bank of Australia (Australia)

- CaixaBank (Spain)

- Bank of China (China)

- HSBC (U.K.)

- United Overseas Bank (UOB)(Singapore)

- First National Bank (South Africa)

- Bank of America (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Japan’s Mitsubishi UFJ Financial Group (MUFG), announced an investment of about USD 4 billion to acquire approximately 20% of Shriram Finance retail-oriented NBFC.

- November 2024: Santander Group (Spain) strengthened its retail lending portfolio in Latin America by introducing AI-based credit scoring models to improve loan accessibility and risk management.

- September 2024: Bank of America Corp. (U.S.) increased investments in cybersecurity and real-time fraud prevention systems to safeguard its expanding digital retail banking customer base.

- July 2024: DBS Bank Ltd. (Singapore) scaled its digital-only retail banking offerings in Southeast Asia to target underbanked populations through mobile-first savings and micro-lending products.

- May 2024: HSBC Holdings plc (U.K.) accelerated its open banking strategy by launching new API-enabled retail payment and account aggregation services across Europe and Asia.

- March 2024: JPMorgan Chase & Co. (U.S.) expanded its AI-driven consumer banking platform to enhance personalized lending, fraud detection, and digital customer engagement across its retail banking operations.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.8% from 2026-2034 |

|

Unit |

Value (USD Trillion) |

|

Segmentation |

By Type, Service Type, and Region |

|

By Type |

· Public Sector Banks · Private Sector Banks · Foreign Banks · Community Development or Cooperative Banks |

|

By Service Type |

· Deposits & Accounts o Savings & Checking Account o Transactional Account o Deposits · Retail Lending & Financing o Home Loans o Personal Loans & Mortgages · Cards & Payments · Wealth Management & Investment Services · Insurance & Bancassurance · Others |

|

By Region |

· North America (By Type, Service Type, and Country) o U.S. (By Type) o Canada (By Type) o Mexico (By Type) · Europe (By Type, Service Type, and Country/Sub-region) o Germany (By Type) o U.K. (By Type) o France (By Type) o Spain (By Type) o Italy (By Type) o BENELUX (By Type) o Nordics (By Type) o Russia (By Type) o Rest of Europe · Asia Pacific (By Type, Service Type, and Country/Sub-region) o China (By Type) o Japan (By Type) o India (By Type) o South Korea (By Type) o ASEAN (By Type) o Oceania (By Type) o Rest of Asia Pacific · South America (By Type, Service Type, and Country/Sub-region) o Brazil (By Type) o Argentina (By Type) o Rest of South America · Middle East & Africa (By Type, Service Type, and Country/Sub-region) o GCC Countries (By Type) o South Africa (By Type) o North Africa (By Type) o Israel (By Type) o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.26 trillion in 2025 and is projected to reach USD 7.09 trillion by 2034.

In 2025, the market value stood at USD 1.62 trillion.

The market is expected to exhibit a CAGR of 5.8% during the forecast period of 2026-2034.

By type, the private sector banks segment is leading the market.

Financial inclusion initiatives driving broader access and growth in retail banking demand are the key factors driving the market.

HSBC, JP Morgan Chase, CaixaBank are the major players in the global market.

North America dominated the market in 2025, with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us