Silicon Anode Battery Market Size, Share & Industry Analysis, By Technology (Below 1,500 mAh, 1,500 to 2,500 mAh, and Above 2,500 mAh), By Application (Consumer Electronics, Electric Vehicles (EVs), Energy Storage Systems (ESS), Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

Silicon Anode Battery Market Size and Future Outlook

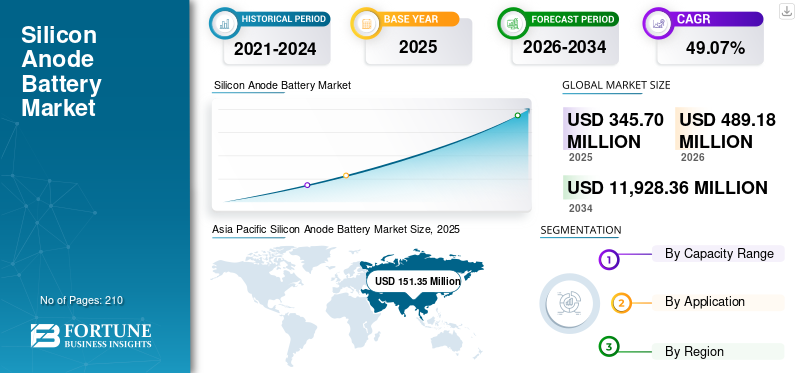

The global silicon anode battery market size was valued at USD 345.70 million in 2025 and USD 489.18 million in 2026. Moreover, the market is projected to reach USD 11,928.36 million by 2034, exhibiting a CAGR of 49.07% during the forecast period of 2021-2034. Asia Pacific dominated the global silicon anode battery market with a market share of 43.78% in 2025. Moreover, the Asia Pacific accounts for the largest market revenue share owing to high demand for EVs and consumer electronics in countries such as China and India.

Silicon anode batteries are a next-generation lithium-ion technology that utilizes silicon in the anode to significantly increase energy storage capacity, resulting in longer battery life and faster charging. While silicon offers a higher theoretical capacity than traditional graphite anodes, its main challenge is the significant volume expansion that occurs during charging, which can cause structural damage and capacity fade. Demand for silicon anode batteries is driven by the need for higher energy density, longer battery life, and faster charging times in electric vehicles (EVs), consumer electronics, and renewable energy storage systems.

- According to the International Energy Agency, EV battery demand is projected to grow 4.5 times by 2030 and nearly 7 times by 2035 compared to 2023 under current policies (STEPS). More ambitious scenarios (APS, NZE) project demand multiplying 5-12 times by 2030 and 2035, driven by rising global EV sales.

Panasonic is a prominent player in the silicon anode battery market, particularly for its role in developing and commercializing next-generation battery technology for electric vehicles and consumer electronics. As the silicon anode battery market continues to grow, driven by high demand for more energy-dense batteries, Panasonic is well-positioned to leverage its expertise and offer improved performance in terms of charging speed and capacity.

Download Free sample to learn more about this report.

Silicon Anode Battery Market Key Takeaways

- 2025 Market Size: USD 345.70 million

- 2026 Market Size: USD 489.18 million

- 2034 Forecast Market Size: USD 11,928.36 million

- CAGR: 49.07% from 2026–2034

- Asia Pacific dominated the silicon anode battery market with a 43.78% share in 2025.

- The above 2,500 mAh segment accounted for a 45.26% market share in 2025.

- The consumer electronics segment held a 35.58% market share in 2025.

North America

North America accounted for USD 86.98 million in 2025 and is projected to reach USD 122.87 million in 2026.

Asia Pacific

Asia Pacific held a 43.78% share in 2025, valued at USD 151.35 million, driven by strong EV adoption and consumer electronics demand.

Europe

Europe held a market value of USD 67.41 million in 2025, driven by growing EV sales, battery R&D investments, and gigafactory expansion.

Latin America

Latin America’s market growth is driven by rising EV adoption, renewable energy investments, and grid modernization

Middle East & Africa

Middle East & Africa market is experiencing significant growth with a CAGR of 43.83%.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rapid Growth in the Adoption of Electric Vehicles to Drive Market Growth

The rapid growth in electric vehicle adoption is significantly driving the silicon anode battery market. As automakers seek higher energy density and longer driving ranges, silicon anodes emerge as a superior alternative to traditional graphite materials. Silicon offers greater lithium-ion storage capacity, enabling faster charging and extended battery life, key requirements for next-generation EVs.

- According to the International Energy Agency, Battery demand reached 850 GWh in 2023, representing a 40% increase from 2022. EVs dominate, accounting for 750 GWh or 90% of total demand, with electric cars representing 80%. Battery storage demand doubled in 2022 and 2023, growing rapidly but from a smaller base.

Government incentives, emission regulations, and the expansion of EV charging infrastructure further accelerate demand. Consequently, battery manufacturers are scaling up production and investing in silicon anode technology to enhance performance, reduce costs, and meet the rising energy efficiency and sustainability needs of the electric mobility market.

High Demand for Consumer Electronics to Propel Market Growth

The rising demand for consumer electronics, including smartphones, laptops, wearables, and tablets, is driving the growth of the silicon anode battery market. These devices require lightweight, compact batteries with higher energy density and longer runtime, which silicon anodes effectively provide. Silicon’s superior lithium-ion storage capacity extends battery life and enhances performance, catering to consumers’ needs for fast charging and durability.

Continuous innovation in portable device design, combined with the rise of 5G technology, is further driving the adoption of advanced energy storage solutions. As a result, electronics manufacturers are increasingly integrating silicon anode batteries to improve product efficiency and user experience.

MARKET RESTRAINTS

High Production Cost Associated with Silicon Anode Battery to Restraint Market Growth

The high production cost associated with silicon anode batteries is a key factor restraining the silicone anode battery market growth. Manufacturing these batteries involves complex material processing and advanced fabrication techniques to manage silicon’s volumetric expansion during charge cycles. This requirement increases production costs and limits large-scale commercialization. Additionally, the need for specialized coatings and composite materials to enhance structural stability further increases expenses. Compared with conventional graphite anodes, silicon-based alternatives face significant cost barriers, particularly in mass production for electric vehicles and consumer electronics. These challenges hinder widespread adoption and slow the transition toward next-generation, high-performance lithium-ion battery technologies.

MARKET OPPORTUNITIES

Expansion into Semi-Solid & Solid-State Batteries to Create Opportunities

The expansion into semi-solid and solid-state battery technologies presents significant opportunities for the silicon anode battery market. Silicon’s high energy capacity and compatibility with next-generation electrolytes make it an ideal material for improving battery safety, stability, and performance. Semi-solid and solid-state systems minimize issues such as dendrite formation, electrolyte leakage, and thermal runaway, thereby enhancing overall durability.

- In October 2025, Toyota announced plans to launch the world's first electric vehicles featuring all-solid-state batteries by 2027-2028. Developed in collaboration with Sumitomo Metal Industries, these batteries offer a longer range, faster charging, increased safety, and enhanced durability, potentially transforming EV performance and driving the global market adoption of silicon anodes.

As research accelerates and commercialization advances, silicon anodes are expected to play a central role in achieving higher energy densities and faster charging. This integration opens new avenues across electric vehicles, aerospace, and consumer electronics, driving innovation and long-term market growth potential for silicon-based batteries.

MARKET CHALLENGES

Competition from Alternative Anode Innovations Creates Challenges for Market Energy & Expansion.

Competition from alternative anode innovations poses a major challenge to the silicon anode battery market. Emerging materials such as lithium metal, tin-based, and graphene anodes offer comparable or superior performance in terms of energy density, stability, and cost. These alternatives attract substantial research and investment, diverting focus from silicon-based developments.

Additionally, ongoing performance improvements in graphite anodes sustain their dominance due to proven reliability and lower costs. This competitive landscape limits the adoption of silicon anodes, pressuring manufacturers to accelerate innovation, enhance cycle life, and reduce production costs to maintain market relevance and expand commercial viability in high-growth battery applications.

SILICON ANODE BATTERY MARKET TRENDS

Shift Toward Silicon-Graphite Blends is Emerging as a Key Trend.

A key trend in the silicon anode battery market is the shift toward silicon-graphite blends, driven by their ability to balance high energy density and stable cycle life. These blends effectively address the challenges of pure silicon anodes, such as volumetric expansion and pulverization, by combining silicon’s high capacity with graphite’s structural stability. Improved formulations, including nanoscale silicon layers and advanced binders, mitigate material degradation and maintain high efficiency over repeated charge cycles. Silicon-graphite composites are being adopted in commercial-scale lithium-ion batteries, enhancing battery performance for electric vehicles and energy storage applications while optimizing manufacturing feasibility and cost.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS ON THE GLOBAL SILICON ANODE BATTERY MARKET

Tariffs have increased costs for the silicon anode battery market by raising the price of raw materials and imported components, while also prompting a strategic realignment of supply chains toward localization, diversification, and onshoring. This has led to higher costs for manufacturers and downstream users, particularly in the automotive and consumer electronics sectors, and is accelerating investment in domestic processing & research and development into alternative methods to reduce reliance on imports.

SEGMENTATION ANALYSIS

By Capacity Range

Above 2,500 mAh are expected to dominate the Market Due to their Prominence in Power Applications

Based on the capacity range, the market is segmented into below 1,500 mAh, 1,500 to 2,500 mAh, and above 2,500 mAh.

Above 2,500 mAh is expected to dominate with a 45.26% of the silicone anode battery market share in 2025, owing to the rising demand for high energy density, extended cycle life, and fast charging, mainly in electric vehicles, power equipment, and industrial energy storage applications.

The below 1,500 mAh segment is expected to witness the fastest growth, driven by rising adoption in wearables, compact IoT devices, and small consumer electronics demanding lightweight, energy-efficient batteries with quick charging capabilities.

By Application

Increasing Demand for Compact and Energy Efficient Batteries in Devices Fuels Consumer Electronics Segment Growth

Based on the application, the market is segmented into consumer electronics, electric vehicles (EVs), energy storage systems (ESS), aerospace & defense, and others.

Consumer Electronics dominated the market in 2025 with a revenue share of 35.58%, driven by demand for compact, energy-dense, fast-charging batteries in smartphones, wearables, tablets, and portable devices. This segment benefits from continuous innovation, improving battery performance while maintaining lightweight and small form factors.

However, the electric vehicle segment will grow at the fastest CAGR of 55.94%, driven by demand for higher energy density, longer driving ranges, and faster charging capabilities. Silicon anode batteries significantly enhance EV performance by enabling greater battery capacity and reducing charge times.

To know how our report can help streamline your business, Speak to Analyst

SILICON ANODE BATTERY MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

The Asia Pacific Silicon Anode Battery market emerged as the largest market with a valuation of USD 151.35 million in 2025. This rapid expansion is driven by strong manufacturing ecosystems, robust electric vehicle adoption, government support, and technological advancements in countries such as China, Japan, South Korea, and India.

Asia Pacific Silicon Anode Battery Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

After Asia Pacific, the North America Silicon Anode Battery Industry was valued at USD 86.98 million in 2025 and is estimated to reach USD 122.87 million in 2026. Growth is driven by increasing electric vehicle production, government incentives for clean energy, and advancements in battery manufacturing technologies. The region hosts robust R&D activities, driving innovation in high-energy, fast-charging batteries for the automotive, consumer electronics, and energy storage sectors. For instance, in November 2024, Honda launched a 295,000 sq. ft. demonstration line for all-solid-state batteries in Sakura City, Japan, with production set to begin in January 2025. This facility aims to refine mass production processes and develop battery cells for electrified models debuting in the late 2020s, thereby supporting Honda’s goal of achieving carbon neutrality by 2050.

Europe

Furthermore, the Europe Silicon Anode Battery Market is expected to account for third third-largest share with a valuation of USD 67.41 million in 2025. Key countries, such as Germany, France, and Norway, lead the growth with extensive EV sales and investments in battery R&D. The region emphasizes localized, ethical supply chains and the expansion of gigafactories. Automotive applications dominate, with consumer electronics and energy storage also making significant contributions.

Latin America and the Middle East & Africa

Latin America’s market growth is driven by rising EV adoption, renewable energy investments, and grid modernization efforts in key countries such as Brazil and Mexico. Policy incentives promoting local battery manufacturing and decarbonization support market expansion. The increasing demand for high-performance batteries in the automotive and consumer electronics sectors further fuels growth, positioning Latin America as an emerging yet rapidly developing region in the global silicon anode battery market. Moreover, the Middle East & Africa market is experiencing significant growth with a CAGR of 43.83%. Growth is driven by the rising adoption of electric vehicles, sustainable energy projects, government incentives, and urban infrastructure development in key countries such as South Africa, the UAE, and Saudi Arabia.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are engaged in partnerships and Collaborations to Increase Market Share in the Future.

The competitive landscape is consolidated, with key players including Sila Nanotechnologies, Group14 Technologies, Amprius Technologies, Enovix Corporation, NanoGraf, and others. For instance, in November 2025, Umicore and Korea’s HS Hyosung Advanced Materials formed a strategic partnership to industrialize and commercialize silicon-carbon composite anode materials for EV lithium-ion batteries. The joint venture, Extra Mile Materials, aims to scale production at an industrial demonstration plant in Belgium by 2026. Such developments are expected to foster market growth over the forecast period.

List of the Key Silicon Anode Battery Companies Profiled

- Sila Nanotechnologies (U.S.)

- Group14 Technologies (U.S.)

- Amprius Technologies (U.S.)

- Enovix Corporation (U.S.)

- NanoGraf (U.S.)

- OneD Battery Sciences (U.S.)

- Panasonic Energy (Japan)

- Samsung SDI (South Korea)

- LG Energy Solution (South Korea)

- CATL (China)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, Sila Nanotechnologies commenced operations at its automotive-scale silicon anode manufacturing facility in Moses Lake, Washington. The plant, spanning over 600,000 sq ft, initially supports 2-5 GWh capacity, with plans to expand up to 250 GWh within five years, aiming to be the world's largest.

- In May 2025, BASF and Group14 Technologies launched a market-ready silicon anode battery solution combining BASF’s Licity 2698 X F binder with Group14’s SCC55 silicon material. This drop-in technology delivers nearly four times the capacity of graphite, faster charging, and extreme durability, maintaining over 1,000 cycles at room temperature and 500 cycles at 45°C, marking a breakthrough for next-gen electric vehicle batteries.

- In April 2025, NEO Battery Materials launched NBMSiDE P-300N, a silicon anode product for EV batteries offering high capacity retention, enhanced stability, and low-cost production. It features a composite coating for improved cycling life and over 99.8% coulombic efficiency for 50 cycles, ready for mass production integration.

- In December 2024, Sionic Energy announced a battery that replaces graphite entirely with a 100 percent silicon anode, unlike EVs such as Tesla, which use only 5-10%. This battery relies on a patented silicon-carbon composite developed by Washington-based Group14 Technologies for superior energy density and performance.

- In October 2024, ProLogium launched the world’s first 100% silicon composite anode battery at the 2024 Paris Motor Show, showcasing higher energy density and longer lifespan, and ultra-fast charging. Certified by TÜV Rheinland and developed with FEV Group, this technology boosts EV range, reduces weight, and lowers costs, revolutionizing electric mobility.

REPORT COVERAGE

The global silicon anode battery market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the Silicon Anode Battery market. Additionally, the report provides regional insights and global market trends & technology, as well as highlights key industry developments. In addition to the factors mentioned above, the report encompasses several other factors and challenges that contributed to the market's growth and decline in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2021-2034 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 49.07% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Capacity Range, By Application, and By Region |

| Segmentation |

By Capacity Range

|

|

By Application

|

|

|

By Region

|

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us