Space-Based Data Center Market Size, Share & Industry Analysis, By Offering (Space Segment Hardware, Ground Segment & Terminals, Software & Cybersecurity, and Services), By Orbit (LEO, MEO, and GEO), By Power Capacity (< 1 kW, 1–5 kW, 5–20 kW, and > 20 kW), By End User (Commercial, Government (civil), Defense & Intelligence, Research & Academia, and Critical Infrastructure & Enterprise), By Data Source (Onboard-Generated Data, Crosslinked from Other Satellites, Uplinked from Ground, and In-situ Cislunar), and Regional Forecast, 2026-2034

Space-Based Data Center Market Size and Future Outlook

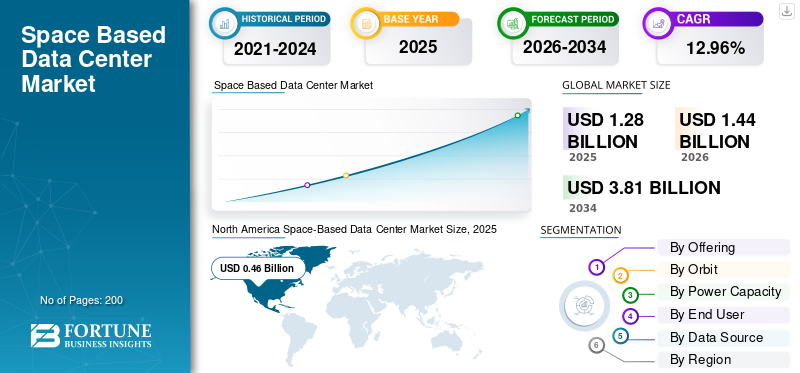

The global space-based data center market size was valued at USD 1.28 billion in 2025. The market is projected to grow from USD 1.44 billion in 2026 to USD 3.81 billion by 2034, exhibiting a CAGR of 12.96% during the forecast period. North America dominated the space based data center market with a market share of 35.93% in 2025.

Space based data centers involve deploying computing infrastructure such as servers, GPUs, storage, and radiation-hardened hardware in satellites or orbital stations to process data directly in space. These systems encompass modular satellite clusters with solar energy power, radiative cooling, inter-satellite optical links, and edge AI infrastructure and processing capabilities. They serve applications such as real-time Earth observation analysis, AI model training for remote sensing, in-orbit data centers from LEO constellations, and cloud services for space stations, reducing downlink bandwidth needs. Key drivers include scalable expansion without land constraints, surging AI compute demand amid Earth grid constraints, and so on.

Leading players include Starcloud (formerly Lumen Orbit), Axiom Space, and SpaceX. These players are planning to test GPU satellites for AI edge computing, build orbital data centers with optical links on their stations, and others.

Download Free sample to learn more about this report.

SPACE-BASED DATA CENTER MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.28 Billion

- 2026 Market Size: USD 1.44 Billion

- 2034 Forecast Market Size: USD 3.81 Billion

- CAGR: 12.96% from 2026–2034

- North America dominated the global market with a 35.93% share in 2025.

- The services segment held the largest market share in 2025.

- The LEO segment dominated the market in 2025 due to strong commercial and government investments in satellite infrastructure.

North America

North America led the market with USD 0.46 billion in 2025.

Europe

Europe is projected to reach USD 0.40 billion in 2026, growing at a CAGR of 12.66%.

Asia Pacific

Asia Pacific is expected to reach USD 0.41 billion in 2026.

U.S.

The market is projected to reach approximately USD 0.32 billion in 2026.

Japan

The market is projected to reach approximately USD 0.07 billion in 2026.

Read More

SPACE-BASED DATA CENTER MARKET TRENDS

Real Time LEO Imagery Analysis is a Prominent Market Trend

Real-time LEO imagery analysis processes high-resolution satellite photos onboard or via edge computing in low Earth orbit, enabling instant insights without ground transmission delays. This trend accelerates in 2026 for disaster detection, spotting floods or wildfires within minutes to guide emergency response and precision agriculture, tracking crop stress via multispectral data for yield optimization. Defense applications include border surveillance and tactical retasking of assets, while environmental monitoring detects deforestation or oil spills near-instantly.

RUSSIA UKRAINE WAR IMPACT

The Russia-Ukraine war disrupted space-based data center market growth by severing critical supply chains for rocket engines and satellite components from Ukrainian firms such as Yuzhmash, forcing Western providers to seek alternatives amid launch delays. Moreover, sanctions halted Roscosmos partnerships, canceling OneWeb satellite launches and ESA payload missions, while Russia's Viasat cyberattack highlighted orbital infrastructure vulnerabilities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Investments for Carbon-Neutral Data Centers to Drive Market Growth

Increasing investments in sustainability for carbon-neutral data centers propel market growth as governments impose stricter energy reporting and efficiency mandates, blocking fossil-fuel reliant ground projects. Orbital systems deliver continuous solar power without weather interruptions or backup generators, inherently aligning with net-zero regulations that prioritize renewable integration. Investors favor these zero-emission platforms to meet stakeholder demands for green infrastructure amid rising scrutiny on data center emissions.

MARKET RESTRAINTS

High Initial Cost is a Key Factor Restraining the Market Growth

High initial costs restrain the market growth, primarily from expensive launches despite reusable rockets such as Starship. Deploying rack scale servers, solar arrays, and massive radiators demands multiple heavy-lift missions, increasing ground construction expenses. Moreover, radiation hardened components, essential for orbital reliability, cost orders of magnitude more than commercial chips and are supplied by only a few companies.

MARKET OPPORTUNITIES

Increased Usage of Edge Computing Creates New Market Opportunities

Increased use of edge computing creates significant market opportunities by enabling ultra-low latency processing directly in orbit for time-critical applications. LEO satellites host AI inference at the data source, such as real-time imagery from Earth observation constellations, eliminating downlink delays that bottleneck ground analysis. This supports autonomous systems, disaster monitoring, and defense surveillance where milliseconds matter, while reducing bandwidth costs for operators managing petabytes of daily satellite data.

MARKET CHALLENGES

Limitations in Maintenance Activities Present a Major Market Challenge

Limitations in in-space maintenance activities challenge the market growth, eliminating routine hardware swaps or upgrades available at ground facilities. Orbital systems launch with full redundancy, since failed drives or GPUs cannot receive on site technician intervention, forcing the premature deorbiting of entire satellites. Furthermore, rapid processor obsolescence, where new chips are introduced with double performance mid-mission, creates issues with updating data centers while still in orbit.

Segmentation Analysis

By Offering

High-Value Data Processing Needs to Boost the Services Segmental Growth

Based on the offering, the market is segmented into space segment hardware, ground segment & terminals, software & cybersecurity, and services.

The services segment is anticipated to account for the largest market share. The rise in demand for services is fueled by the need for real time, high value data analytics in sectors such as defense, Earth observation, and satellite communications.

The software & cybersecurity segment is anticipated to rise with a CAGR of 13.01% over the forecast period.

By Orbit

Government and Commercial Investment to Boost LEO Segment Growth

Based on orbit, the market is segmented into LEO, MEO, and GEO.

In 2025, the LEO segment dominated the global market. The rapid expansion of LEO infrastructure is being driven by significant investment from commercial actors (Kuiper, Starlink) and governments for defense (secure communications, surveillance).

The MEO segment is projected to grow at a CAGR of 12.90% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Power Capacity

Low Launch Costs to Boost < 1 kW Segment Growth

Based on the power capacity, the market is segmented into < 1 kW, 1–5 kW, 5–20 kW and > 20 kW.

The < 1 kW segment is anticipated to witness a dominating space-based data center market share over the forecast period. Compared to larger, power-hungry alternatives, smaller, lower-power (<1 kW) data centers are significantly more economically viable since they are simpler to launch and require less physical infrastructure.

The > 20 kW segment is projected to grow at the highest CAGR of 14.62% over the forecast period.

By End User

Emergence of New Commercial Players to Boost the Commercial Segment Growth

Based on end user, the market is segmented into commercial, government (civil), defense & intelligence, research & academia, and critical infrastructure & enterprise.

The commercial segment dominated with the largest market share. The emergence of new players such asStarCloud/Lumen Orbit, Lonestar Data Holdings, and D-Orbit are investing and implementing orbital infrastructure for data storage, backup, and artificial intelligence workloads.

In addition, defense & intelligence segment is projected to grow at the highest CAGR of 13.58% during the forecast period.

By Data Source

Rise of AI and ML Driven In-Orbit Analytics to Boost the Onboard-Generated Data Segment Growth

Based on data source, the market is segmented into onboard-generated data, crosslinked from other satellites, uplinked from ground, and in-situ cislunar.

The onboard-generated data segment dominated the market. The segmental growth is due to the adoption of Artificial Intelligence (AI) and Machine Learning (ML) in space, enabling data services from satellites directly in orbit.

In addition, crosslinked from other satellites segment is projected to grow at a CAGR of 13.57% during the forecast period.

Space-Based Data Center Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Space-Based Data Center Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 0.41 billion, and also maintained the leading share in 2025, with USD 0.46 billion. North America leads space-based data center development through private aerospace innovation and AI hyperscaler investments.

U.S. Space-Based Data Center Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.32 billion in 2026, accounting for roughly 13.37% CAGR over the forecast period. The U.S. market dominates with vertically integrated firms planning orbital AI clusters powered by domestic launch vehicles. Government defense contracts drive secure in-space processing for national security applications.

Europe

Europe is projected to record a steady growth rate during the forecast period of 12.66%, which is the second highest among all regions, and reach a valuation of USD 0.40 billion by 2026. Europe focuses on regulatory frameworks for sustainable orbital infrastructure amid terrestrial power constraints.

U.K. Space-Based Data Center Market

The U.K. market in 2026 is estimated at around USD 0.12 billion, representing roughly 13.11% CAGR during the forecast period. The U.K. market pursues sovereign orbital compute through the defense ministry’s R&D for real-time intelligence processing. Post-Brexit space agency initiatives fund inter-satellite laser links for low-latency networks.

Germany Space-Based Data Center Market

Germany’s market is projected to reach approximately USD 0.11 billion in 2026. Germany channels Fraunhofer Institute research into radiation-tolerant processors for space data nodes. Furthermore, Bavaria's aerospace cluster develops modular satellite racks for European satellite constellations.

Asia Pacific

Asia Pacific region is estimated to reach USD 0.41 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the forecast period. Asia Pacific is accelerating LEO mega-constellations that require onboard analytics, spurring regional orbital compute demand.

Japan Space-Based Data Center Market

The Japan market in 2026 is estimated at around USD 0.07 billion, accounting for roughly 13.66% of the CAGR during the forecast period. Japan advances JAXA-led prototypes for quake detection via real-time orbital processing. Moreover, key player such as Mitsubishi Heavy Industries develop solar arrays for sustained low-power data nodes.

China Space-Based Data Center Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.12 billion. China deploys national orbital data platforms through the state space agency for secure AI sovereignty. Massive LEO swarms demand in-space imagery analysis to manage downlink bandwidth.

India Space-Based Data Center Market

The Indian market in 2026 is estimated at around USD 0.10 billion. India's space agency tests CubeSat compute nodes for disaster monitoring edge AI. Growing private launch sector lowers barriers for domestic orbital pilots.

Rest of the World

The rest of the world include the Middle East & Africa and Latin America. Latin America leverages equatorial launch sites for cost-effective LEO deployments serving regional monitoring. Middle East & Africa sovereign funds explore oilfield analytics in orbit amid desert power limits. The Middle East & Africa and Latin America markets are set to reach valuations of USD 0.06 billion and USD 0.04 billion, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Orbital Edge Computing Innovations Drive Market Growth

The space-based data center market shows a consolidating landscape led by pioneering aerospace tech firms. Major key players include Starcloud, Axiom Space, Kepler Communications, SpaceX, Google project Suncatcher, Blue Origin, Skyloom Global, Lumen Orbit, and xAI, which together control development pipelines via integrated compute constellations and orbital infrastructure.

Key players strengthen market positions through orbital edge computing innovations in radiation hardened AI processing and inter-satellite laser networking. For instance, Axiom Space's partnerships with Kepler Communications integrate optical data relays for real-time analytics on its commercial station. Starcloud advances GPU satellite prototypes for in-orbit model training, meeting surging demand for low-latency space data processing amid terrestrial power constraints

LIST OF KEY SPACE-BASED DATA CENTER COMPANIES PROFILED

- Starcloud (U.S.)

- Axiom Space (U.S.)

- Kepler Communications (Canada)

- SpaceX (U.S.)

- Google (U.S.)

- Blue Origin (U.S.)

- Skyloom Global (U.S.)

- Thales Alenia Space (France)

- Madari Space (UAE)

- Sophia Space (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: The first operational tranche of Kepler Communications' next-generation optical data relay constellation has been successfully launched. Ten 300-kilogram-class satellites were successfully launched into a Sun-Synchronous Orbit (SSO) during the operation, which was conducted aboard a SpaceX Falcon 9 rocket from Vandenberg Space Force Base.

- January 2026: In order to power Artificial Intelligence (AI), Elon Musk's SpaceX submitted an application to launch a million satellites into Earth's orbit. According to the application, "orbital data centers" are the most economical and energy-efficient way to meet the growing demand for AI processing power.

- January 2026: Blue Origin unveiled TeraWave, a satellite communications network intended to provide symmetrical data speeds of up to 6 Tbps anywhere on Earth. Moreover, the TeraWave architecture consists of 5,408 optically interconnected satellites in Low Earth Orbit (LEO) and Medium Earth Orbit (MEO).

- April 2025: In an effort to expand its work on commercial space stations and create space-based cloud computing services, Axiom Space will launch two data centers aboard Kepler Communications satellites.

- December 2023: In order to install and test high data rate Optical Intersatellite Links (OISLs) on the first module of Axiom Space's commercial space station, Axiom Station, the Houston-based company signed agreements with Kepler Communications US Inc. and Skyloom Global Corp.

REPORT COVERAGE

The global space-based data center industry analysis includes a comprehensive study table of contents of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, Porter’s Five Forces Analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers, and acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.96% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Orbit, Power Capacity, End User, Data Source and Region |

| By Offering |

|

| By Orbit |

|

| By Power Capacity |

|

| By End User |

|

| By Data Source |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.28 billion in 2025 and is projected to reach USD 3.81 billion by 2034.

In 2025, the North Americas market value stood at USD 0.46 billion.

The market is expected to exhibit a CAGR of 12.96% during the forecast period.

By offering, the service segment is expected to dominate the market.

Increasing Investments for carbon-neutral data centers are the key factors driving market growth.

include Starcloud, Axiom Space, Kepler Communications, SpaceX, Google (Suncatcher), Blue Origin, Skyloom Global, and Lumen Orbit, are few key players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us