Spine Biologics Market Size, Share & Industry Analysis, By Product Type (Bone Graft Substitutes {Allografts, Demineralized Bone Matrix (DBM), Synthetic, Xenograft}, Platelet Rich Plasma (PRP), Growth Factors, Cell-based Matrices, Bone Marrow Aspirate Concentrates (BMAC), and Others), By Application (Spinal Fusion, Non Fusion Procedures, Fracture Repair, Scoliosis Correction, and Others), By End User (Hospitals & ASCs, Specialty Orthopedic & Spine Clinics, and Others), and Regional Forecast, 2026-2034

Spine Biologics Market Size and Future Outlook

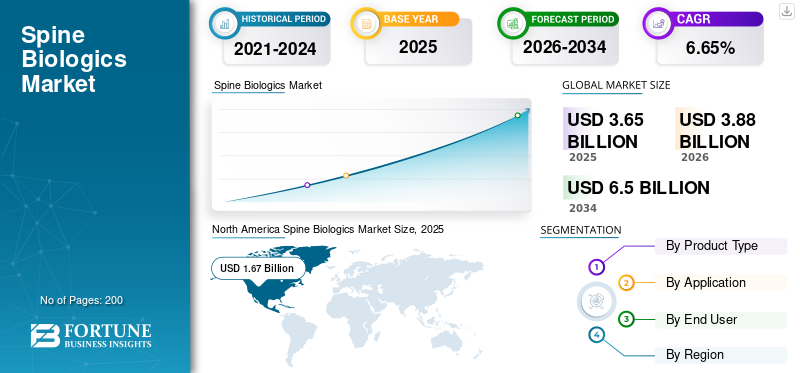

The global spine biologics market size was valued at USD 3.65 billion in 2025. The market is projected to grow from USD 3.88 billion in 2026 to USD 6.50 billion by 2034, exhibiting a CAGR of 6.65% during the forecast period. North America dominated the global spine biologics market with a market share of 45.75% in 2025.

Spine biologics include substances used in spinal surgery to promote bone healing and fusion. The market is poised for considerable growth over the forecast period owing to the rising incidence of spinal disorders across the globe. In addition, the shift toward surgical techniques with minimally invasive approaches increases the demand for advanced, reliable biologic solutions. Additionally, advancements in the market are reducing complications associated with traditional bone grafting methods, in turn supporting the overall growth of the market. Moreover, numerous product launches and major collaborations among key operational players support the market growth.

- For instance, in April 2023, PUR Biologics, a subsidiary of HippoFi, Inc., launched PURcoreTM, a moldable synthetic with an interconnected micro-pore structure for spine surgery. PURcoreTM allows for the rapid colonization of the patient's own cells and growth factors, which promote bone regeneration and healing.

Additionally, the market is dominated by various key operating players, including Medtronic, Stryker, Johnson & Johnson, and Globus Medical, which direct their resources toward strategic mergers and acquisitions and new product launches to strengthen their market position.

Download Free sample to learn more about this report.

SPINE BIOLOGICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.65 billion

- 2026 Market Size: USD 3.88 billion

- 2034 Forecast Market Size: USD 6.50 billion

- CAGR: 6.65% from 2026–2034

- North America dominated the spine biologics market with a 45.75% share in 2025.

- The bone graft substitute segment held the largest share by product type in 2025.

- The spinal fusion segment led the market and is projected to account for 66.6% of the market in 2026.

North America

North America remained the leading regional market, reaching USD 1.67 billion in 2025, supported by high spinal surgery volumes and advanced reimbursement systems.

Europe

Europe is projected to reach USD 1.12 billion in 2026, growing at a CAGR of 5.42% due to steady adoption of demineralized bone matrix and synthetic substitutes.

Asia Pacific

Asia Pacific is expected to reach USD 0.76 billion in 2026, with growth supported by expanding healthcare infrastructure and increasing spinal procedures across emerging economies.

U.S.

The market is estimated to reach USD 1.58 billion in 2026, driven by strong healthcare infrastructure, reimbursement support, and ongoing biologics innovation.

Japan

The market is expected to grow steadily, supported by an aging population, increasing incidence of degenerative spinal disorders, and rising demand for spinal fusion procedures.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Surgical Procedures for Degenerative Spine Disorders to Drive Market Growth

The rising number of surgeries for degenerative spine disorders is a major factor driving the growth of the market. With the increasing prevalence of spinal disorders, patients experience chronic pain and require intervention such as spinal fusion or others. These surgical interventions are driving the demand for products such as allografts, DBM, synthetic grafts, BMAC, and cell-based matrices for bone healing and fusion. In addition, surgeons increasingly prefer biologics over traditional autograft to reduce complications, improve patient outcomes, and reduce recovery times. As a result, higher degenerative surgery volumes translate into consistent, sustained demand for advanced spine biologics worldwide.

- For instance, in February 2025, the American Spine Registry (ASR) released its first edition Annual Report. The report reviewed procedures performed between 2015 and 2023, and collected data on 112,683 cervical spine procedures and 230,159 lumbar spine procedures. Such high number of surgical procedures increase the product demand and drive the global spine biologics market growth.

MARKET RESTRAINTS:

Reimbursement Variability across Healthcare Systems to Restrain the Market Growth

One of the significant factors restraining the market growth is the variability across various healthcare systems for reimbursement. Many healthcare payers deny or restrict coverage for premium biologic grafts, leading surgeons to opt for lower-cost alternatives, such as autograft or simpler allograft, to ensure reimbursement. This uncertainty for reimbursement discourages patients from adoption novel, safer biologic alternatives, limiting their adoption. These factors limit the market growth. Thus, reimbursement variability acts as a structural restraint on the uptake of premium spine biologics products.

- For instance, in October 2025, a settlement stemming from a 2019 lawsuit that was initially dismissed, where Plaintiffs Brian Hendricks and Andrew Sagalongos were denied coverage of lumbar artificial disc replacement. The insurer classified the procedure experimental or investigational. They were later entitled to a reimbursement of USD 55,000 after the lawsuit.

MARKET OPPORTUNITIES:

Technological Advancements in Cell-Based and Regenerative Biologics to Offer Significant Growth Avenues

Advances in cell-based matrices, stem cell-engineered grafts, and regenerative scaffolds present a significant opportunity for the market. Traditional biologics present certain risks, such as variable donor quality and limited ability to repair biologically compromised bone. With these newer technologies, these challenges can be overcome by using viable stem cell populations, optimized extracellular matrices, and biologically active synthetic scaffolds. They provide more predictable fusion and improved bone regeneration. As clinical evidence and regulatory clarity improve, the increasing adoption of regenerative biologics offers significant market growth avenues. Underscoring these advantages, many key companies are directing their resources toward new product launches of cell-based matrices and grafts.

- For instance, in September 2024, Xtant Medical Holdings, Inc. launched OsteoVive Plus, a moldable, viable bone matrix used in a variety of grafting procedures. Such development offers a market growth opportunity.

SPINE BIOLOGICS MARKET TRENDS:

Growing Adoption of Minimally Invasive Procedures is a Prominent Market Trend

The rising adoption of minimally invasive spine surgery is emerging as a significant global spine biologics market trend. These minimally invasive techniques reduce tissue disruption, postoperative pain, and blood loss, leading to better patient outcomes. As more procedures shift to MIS, surgeons increasingly rely on biologics that are easy to deliver. These factors remove the need for extensive graft harvesting. Additionally, medical societies and hospital systems continue to publish supportive clinical data validating MIS outcomes, strengthening confidence in these methods. As MIS becomes standard practice in lumbar and cervical fusion, biologics designed for minimally invasive workflows gain increasing market traction. Such factors also encourage new product launches by key companies to facilitate minimally invasive procedures.

- For instance, in August 2025, Kuros Biosciences launched the magnetos MIS delivery system. This system features, sterile, prefilled, and single-use delivery system helpful for MIS (Minimally Invasive Surgery), especially in spine procedures.

MARKET CHALLENGES:

Limitations of Allografts Restraint to Pose a Significant Challenge for Market Growth

Allografts are subjected to various limitations due to inconsistent supply availability and scalability issues. Variability in donor quality and biological potency also leads to unpredictable osteogenic performance, making fusion outcomes less reliable compared to next-generation biologics. As a result, the limitations of allografts continue to hinder the optimal adoption of more advanced biologic solutions and restrict growth potential across regions. Allografts have certain drawbacks. They are mildly osteoinductive and osteoconductive as they are derived from human origin. However, due to the sterilizing process, allografts do not have osteogenic qualities or live cells. The low risk of HBV or HCV infection from the donor and the possibility of unfavorable alterations in the composition of the bone matrix during the radiation and chemical sterilization process are two other drawbacks of allografts.

- For instance, in November 2020, NIH published a study titled ‘Comparative Effectiveness and Safety of Allografts and Autografts in Posterior Cruciate Ligament Reconstruction Surgery: A Systematic Review’ that reported the limitations of allografts, such as potential graft rejection, weakening of graft structure due to sterilization, delayed healing and remodeling, and limited graft availability with associated costs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Broad Adoption in Surgical Procedures and Ongoing Product Innovations Collectively Drives Bone Graft Substitute Segment Growth

Based on product type, the market is segmented into bone graft substitutes, Platelet-Rich Plasma (PRP), growth factors, cell-based matrices, Bone Marrow Aspirate Concentrates (BMAC), and others.

To know how our report can help streamline your business, Speak to Analyst

In 2025, the bone graft substitute segment dominated the market for spine biologics on the basis of product type. The segment accounted for the largest market share due to its utilization in all the surgical and trauma repair procedures. Additionally, the established presence of graft substitutes such as allografts and demineralized bone matrix supports the market dominance. These products are also preferred in minimally invasive surgeries due to their ease of handling and predictable performance. As a result, bone graft substitutes represent the highest-volume biologics category globally. Moreover, key companies are focusing on new product launches to expand their product offerings and restore the segment’s dominance.

- For instance, in October 2025, Aurora Spine Corporation launched Aurora Biologics, a new division dedicated to advancing spinal fusion success through biologic innovation. Such development supports segmental growth.

On the other hand, the cell-based matrix segment is expected to grow at a CAGR of 9.67% during the forecast period.

By Application

Increasing Number of Procedures to Propel Spinal Fusion Segmental Growth

On the basis of application, the market is classified into spinal fusion, non-fusion procedures, fracture repair, scoliosis correction, and others.

Among these, the spinal fusion segment accounted for the largest spine biologics market share in 2025. In 2026, the segment is anticipated to dominate with a 66.6% share. These spinal fusion surgeries are performed mainly for degenerative disc disease and spinal disease, trauma, and deformity. They represent the vast majority of biologic usage globally. Fusion procedures require a grafting material in nearly all cases, making biologics an essential component of the surgery. Rising aging populations, high prevalence of degenerative disc disease, and expanding use of minimally invasive fusion techniques all contribute to the scale of this segment. Further, the market is anticipated to grow with the rising number of spinal fusion surgeries.

- For instance, in November 2024, Mayo Clinic reported that its orthopedic surgeons and neurosurgeons perform more than 2,300 spinal fusions each year. Such larger volumes of surgeries are expected to drive segmental growth.

The non-fusion procedures segment is expected to grow at a CAGR of 8.77% over the forecast period.

By End User

High Surgical Volume in Hospitals to Propel the Hospitals and ASCs Segmental Growth

Based on end user, the market is categorized into hospitals & ASCs, specialty orthopedic & spine clinics, and others.

The hospitals & ASCs segment dominated the market based on end user in 2025. In 2026, the segment is anticipated to dominate with a 75.9% share. Most spine surgeries are performed in hospitals due to the shift toward minimally invasive procedures. Hospitals control the majority of biologics procurement budgets. ASCs, on the other hand, are rapidly growing contributors due to increasing surgeon preference for same-day spine procedures. In addition, increasing partnerships among key operating entities supports the segmental growth. These factors lead to the segmental growth.

- For instance, in October 2025, BIOBank partnered with Spineart, aiming to enhance access to high-quality allogenic bone substitutes for hospitals and spine surgeons in Switzerland and France.

The specialty orthopedic & spine clinics segment is expected to grow at a CAGR of 9.12% over the forecast period.

Spine Biologics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Spine Biologics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant share in 2024, valued at USD 1.56 billion, and also maintained the leading share in 2025, with USD 1.67 billion. The region accounted for the dominant market due to high spinal surgery volumes, advanced reimbursement systems, and early adoption of novel biologics and cell therapies. In 2026, the U.S. market is estimated to reach USD 1.58 billion. In the U.S., the robust healthcare infrastructure and reimbursement promote adoption and support the market growth. Additionally, due to such high potential, various key companies focus on new product launches to further strengthen their market position, leading to the market growth in the country.

- For instance, in January 2025, LifeNet Health launched PliaFX Flo, an innovative addition to its PliaFX portfolio of advanced fiber demineralized bone matrices. The product amplifies the healing potential, resulting in better outcomes for patients.

Europe and Asia Pacific

Regions, such as Europe and the Asia Pacific, are expected to experience notable growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 5.42%, the second-highest among all regions, and reach a valuation of USD 1.12 billion by 2026. The growth in Europe is attributed to a mature market with steady adoption of demineralized bone matrix and synthetic substitutes. Backed by these factors, the U.K. is anticipated to record a valuation of USD 0.24 billion, Germany to record USD 0.21 billion, and France to record USD 0.16 billion in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 0.76 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are estimated to reach USD 0.20 billion and USD 0.12 billion in 2026.

Latin America and the Middle East & Africa

During the forecast period, the Latin America and the Middle East & Africa regions are expected to witness moderate growth. The Latin America market, in 2026, is set to reach a valuation of USD 0.15 billion. The growth in this region is driven by improvements in surgical infrastructure and increased availability of allograft and synthetic products. In the Middle East & Africa, the GCC is set to reach a value of USD 0.04 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Collaborations and Acquisitions by Key Players supported their Leading Position

The market for spine biologics exhibits a consolidated market structure, with a few companies dominating the market with diverse product offering. These players along with diverse product offering also participate in numerous strategic activities such as collaborations, acquisitions, and mergers. Medtronic, Stryker, Globus Medical., Xtant Medical, and Biomatlante and, Companion Spine LLC are some of the major players in the market. These companies offer a wide range of systems for the numerous biologics used for spine along with graft substitutes.

- For instance, in July 2025, Companion Spine LLC acquired the Coflex Interlaminar Stabilization device and CoFix Posterior MIS Fusion System implants from Xtant Medical Holdings, Inc. The development strengthened the product offering of the company in posterior dynamic spine stabilization and spine motion preservation.

Other notable players in the market include Johnson & Johnson, ChoiceSpine LLC., Zimmer Biomet, and others. These companies are undertaking various strategic initiatives, such as investments to expand their product offerings.

LIST OF KEY SPINE BIOLOGICS COMPANIES PROFILED:

- Medtronic (Ireland)

- Stryker (U.S.)

- Johnson & Johnson (U.S.)

- Globus Medical (U.S.)

- Xtant Medical (U.S.)

- Zimmer Biomet (U.S.)

- Biogennix, LLC. (U.S.)

- ChoiceSpine LLC. (U.S.)

- Biomatlante. (France)

- Biogennix, LLC. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Aurora Spine Corporation launched Aurora Biologics, a new division dedicated to advancing spinal implants and biologics.

- April 2025: Spine Wave completed the limited market release of Tempest DCF Demineralized Cortical Fibers of the spinal allograft market. The development broadened the company’s position in the market.

- October 2023: Orthofix Medical Inc. received 510k clearance and a full commercial launch of OsteoCove, a bioactive synthetic graft. This synthetic graft provided superior bone-forming capabilities for a wide range of spine and orthopedic procedural applications.

- August 2023: Xtant Medical Holdings, Inc. acquired Surgalign Holdings, Inc.’s biologics and spinal fixation business for USD 5.0 million. The development expanded the company’s offering in the market.

- October 2020: Orthofix Medical Inc. launched its new O-GENESIS Graft Delivery System, designed for delivering synthetic bone graft, autograft, or allograft to orthopedic surgical sites. The company also rolled out the AlloQuent Structural Allograft Q-Pack, a ready-to-use and hydrated form of lumbar and cervical spacers for allograft procedures.

REPORT COVERAGE

The market analysis provides a detailed study of the market size and forecast for all the market segments included in the report. It also encompasses details on the market dynamics and trends expected to drive the market during the forecast period. It also provides overviews of technological advancements, product development, key industry developments, mergers, and acquisitions, and strategic insights into market growth. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.65% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Application, End User, and Region |

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.65 billion in 2025 and is projected to reach USD 6.50 billion by 2034.

In 2025, the North America market value stood at USD 1.67 billion.

The market is expected to exhibit a CAGR of 6.65% during the forecast period of 2026-2034.

The bone graft substitute segment dominated the market by product type in 2025.

The increasing volumes for spinal surgeries is the key factor driving market growth.

Medtronic, Stryker, Johnson & Johnson, and Xtant Medical are among the prominent players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us