Submarine Payload Market, Size, Share & Industry Analysis by Product Type (Conventional Submarine, Nuclear Submarine, Air-Independent Propulsion (AIP), & Special Mission Submarines), By Launch Mechanism (Vertical Launch Systems (VLS), Inclined Launch Systems, Horizontal Launch Systems, & Canister Launch Systems), By Payload Type (Weapon Payloads, Sensor Payloads, Surveillance & Reconnaissance Equipment, Electronic Warfare Systems, Unmanned Underwater Vehicles (UUVs), & Others), By Application (Naval Defense Forces, Research - Exploration, & Maritime Security), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

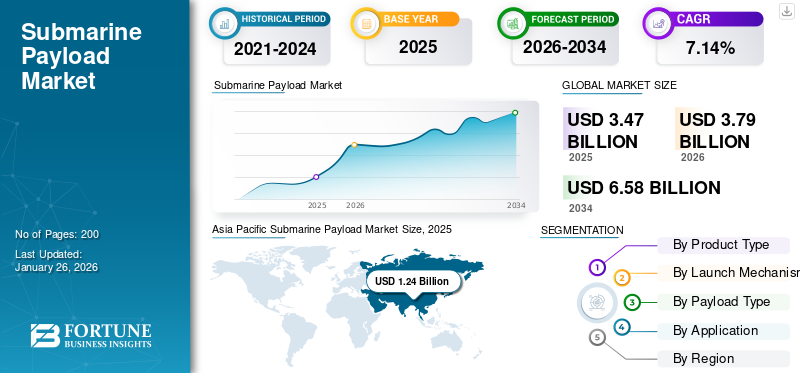

The global submarine payload market size was valued at USD 3.47 billion in 2025. The market is projected to grow from USD 3.79 billion in 2026 to USD 6.58 billion by 2034, exhibiting a CAGR of 7.14% during the forecast period.

Submarine payload refers to any mission-equipment that a submarine launches, carries, or harbors to perform operations such as weapons (torpedoes, cruise/ballistic missiles, mines), sensors (hull/towed sonars, ESM), communications/navigation packages, and mission modules (Dry-Deck Shelters, payload bays) and deployable unmanned systems (UUV/AUV) and scientific equipment.

Nations across the globe are embarking on ambitious naval modernization programs with submarine forces at the core of strategic deterrence and combat readiness. Investments in more advanced payload systems, such as autonomous underwater vehicles (UUVs), advanced sensors, and modular payload configurations, are broadening operational capabilities and are likely to fuel the growth of the global market growth over the upcoming years.

The market encompasses several major players with broad portfolio with innovative products and strong initiatives focused on expanding regional presence have supported the dominance of these companies in the market. Major players are BAE System, Raytheon Technologies, General Dynamics, and Lockheed Martin, among others.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Naval Modernization and Geopolitical Tensions Fueling Naval Modernization Programs to Drive the Market Growth

The market is witnessing high growth fueled by rising geopolitical tensions and global naval modernization initiatives. Nations are spending huge amounts of money on sophisticated submarine systems to retain maritime superiority and strategic deterrence capabilities in a progressively contested global atmosphere. Heightened tensions in vital regions such as the South China Sea, Indo-Pacific, and the Baltic Sea are forcing nations to improve underwater warfare capabilities through advanced payload systems.

The U.S., China, Russia, and European nations are aggressively building up their submarine forces with focus on advanced torpedoes, ballistic missiles, cruise missiles, and detection systems with tactical and strategic value. Government defense budgets have surged, with the U.S. Navy alone spending more than USD 18 billion on Virginia-class submarine contracts in 2025, while European nations are joining together on next-generation submarine technology in initiatives such as AUKUS. This continuous investment in submarine capabilities is an indicator of the absolute value of submarines in upholding national security and extending power through all maritime regions globally.

- For instance, in February 2025, NIT Rourkela and DRDO joined hands to design cutting-edge underwater tiles that minimize sonar detectability, thereby increasing the stealth of submarines, furthering India's indigenous defense capabilities and aiding industries such as marine exploration and oil exploration.

Market Restraints

High Development Expenditures and Budget Limitations Could Hamper the Market Growth

The submarine payload market growth is hampered by the rising cost of development and budget constraints that limit procurement and innovation for naval forces across the globe. Advanced payload systems must be developed with tremendous investments in research, advanced materials, manufacturing facilities, and talented workforce, with each program potentially costing billions of dollars during its lifetime. The technical complexity of contemporary submarine systems, with multiple advanced technologies demanding integration such as nuclear power, stealth, and advanced weapons systems, pushes costs beyond the capabilities of many countries with limited defense budgets.

Cost overruns have become the rule in submarine programs, such as the U.S. Columbia-class submarine program seeing cost growth six times greater than contractor projections, potentially adding hundreds of millions of dollars to the cost of individual vessels. These fiscal pressures compel countries to allocate scant resources, sometimes leading to decreased fleet numbers, delayed modernization programs, or diluted capability demands. The long lead times of submarine programs, typically taking 10-15 years from design through delivery, induce further fiscal risks as technologies improve and the bill grows higher than originally estimated.

Market Opportunity

Growing Adoption of Autonomous Systems and Unmanned Vehicle Integration to Propel Market Expansion over Upcoming Years

The fast-paced evolution of autonomous underwater vehicles (AUVs) and unmanned systems creates significant opportunity for growth in the submarine payload market. AUVs are being increasingly sent out from submarines using torpedo tubes and dedicated launch mechanisms, projecting their operational range and intelligence-gathering ability while staying covert and minimizing crew risk. The embedding of swarm intelligence technologies enables autonomous vehicles to collaborate on a variety of complex missions, from mine warfare to reconnaissance operations, opening up new tactical options for submarine commanders. Sophisticated UUVs with AI-enabled sensors and communications can stay at sea for weeks, offering persistent underwater presence and real-time intelligence that maximizes submarine effectiveness.

Emerging economies and new naval powers are major growth prospects for submarine payload systems as they modernize their fleets and build underwater warfare capacity. Those in Asia Pacific, the Middle East, and Latin America are investing in submarine programs to defend territorial waters, secure sea lanes, and project regional power, generating the demand for affordable payload solutions. India's USD 8.4 billion Project 75(I) submarine project and comparable projects in nations such as Brazil, Turkey, and South Korea illustrate the enormous market potential in maturing defense markets.

- For instance, in September 2025, Germany's ThyssenKrupp Marine Systems initiated official contract talks with India for Project 75(I), six advanced conventional submarines worth around USD 8.4 billion, representing one of the biggest submarine procurement deals in emerging markets.

Submarine Payload Market Trends

Artificial Intelligence and Machine Learning Technologies’ Integration into Payload Systems

The integration of artificial intelligence and machine learning technologies in submarine payload systems is transforming submarine operations underwater and opening up new market spaces centered on smart autonomous systems. Artificially intelligent advanced sonar interpretation systems have the ability to analyze enormous amounts of acoustic data in real-time, allowing submarines to detect and categorize targets with unprecedented precision at the cost of fewer false alarms and decreased operator workload. Machine learning systems are being incorporated in torpedo guidance, autonomous vehicle navigation, and threat capabilities, boosting mission accomplishment and operational performance rates.

Swarm coordination by AI provides several autonomous vehicles and weapons with the capability to work together in a coordinated effort, adjusting to tactical dynamics and maximizing mission success based on distributed intelligence.

The creation of AI-based maintenance and predictive analytics solutions is enhancing submarine availability and lowering lifecycle expenditure through the prediction of component failures and the optimization of maintenance timetables. Edge computing technologies are allowing for AI processing capacity to be integrated directly into submarine systems, minimizing reliance on outside communications and building operational security in hostile environments.

- For instance, in July 2025, China's revolutionary innovation in magnetic detection technology is set to overturn conventional submarines' stealth features, potentially transforming the future of naval warfare and strategic military planning.

Market Challenges

International Regulations, Export Controls, and Technology Transfer Restrictions Create Significant Barriers for Market Expansion

International rules, export controls, and technology transfer restrictions pose high entry barriers to the development of the submarine payload market and cross-border cooperation. The International Traffic in Arms Regulations (ITAR) and other like-minded export control regimes place severe restrictions on the dissemination of submarine technologies, even between allied countries, making joint development programs and integration of technologies more difficult. These regulatory barriers restrict access to markets for foreign suppliers, limit competition, and raise development costs by compelling nations to build indigenous capacities instead of utilizing available technologies.

The intricacy of procuring regulatory clearances on submarine systems, especially those with nuclear technologies or advanced weapons, causes long delays and program duration uncertainty. Export licensing controls tend to limit the freedom of defense contractors to join foreign submarine programs, restricting market opportunities and impeding technology transfer that could speed innovation. The tight security standards for submarines also discourage smaller suppliers and technology firms from entry, consolidating market power among a few large experienced defense contractors with security clearances and regulation compliance skills.

- For instance, in September 2021, the AUKUS partnership underscored the export control reform challenges, with Australia and the U.K. voicing concerns that existing ITAR rules could delay timely submarine capability delivery and cooperative technology development under the trilateral defense pact.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Sustained High Speed and Power Density offered by Nuclear Powered Submarine to Drive Segment Growth

The global market, by product type, is classified into conventional submarine, nuclear submarine, air-independent propulsion (AIP), and special mission submarines.

The nuclear submarine segment is estimated to be the fastest-growing segment with the highest CAGR of 9.8% during the forecast period of 2025-2032. The segment is expanding rapidly as they provide unmatched endurance, sustained high-speed, and power density that support long-range power projection and large sensor/weapon payloads navies’ value as they pursue blue-water reach. Strategic imperatives (great-power competition, sea-based deterrence, and long-range strike) have compelled major navies to invest in SSNs and new SSBN classes, generating multi-decade procurement programs that increase nuclear build rates.

The conventional submarine segment accounts for the largest market share with 41.06% in 2026 and is estimated to grow at a CAGR of 6.0% during the forecast period. Traditional submarines hold the dominant market share in terms of fleet quantities due to their much lower cost, availability for export, and versatility for navies in local regions. With their low costs of acquisition compared to other next-generation submarines, they enable Asia Pacific, European, and Latin American nations to exercise credible submarine capabilities without access issues of political, industrial, and compliance concerns associated with nuclear propulsion.

- For instance, in April 2022, as part of India's P-75 Scorpène project with Naval Group, India commissioned the INS Vagsheer (final Scorpène-class), bolstering the nation's conventional submarine fleet.

By Launch Mechanism

Increasing Demand for Naval Fleet Modernization to Catalyze the VLS Segmental Growth

The global market, by launch mechanism, is segmented into vertical launch systems (VLS), inclined launch systems, horizontal launch systems, and canister launch systems.

The vertical launch system (VLS) segment is estimated to be the fastest growing segment with the highest CAGR of 9.0% during the forecast period of 2025-2032. The expansion is driven by the increasing naval fleet modernization and need for universal, response-centric platforms. VLS allows submarines to launch a range of advanced missiles such as cruise, ballistic, anti-ship, and hypersonic missiles in the vertical direction, giving them the capability to conduct rapid simultaneous launch to enhance significantly the offensive capability and operational flexibility. The embedding of VLS cells outside the pressure hull maximizes space planning, allowing submarines to load more salvo of missiles but with torpedoes still readily accessible for anti-sub warfare operations.

- For instance, in September 2025, the U.S. Navy pushed forward with the Virginia class submarines Block V program, adding the Virginia Payload Module featuring four large-diameter VLS tubes that can each fire up to seven Tomahawk cruise missiles. This builds total missile capacity by 76%, building on the trend toward larger VLS-capable platforms to maintain strategic flexibility and firepower.

The horizontal launch systems segment is expected to capture the largest submarine payload market share with a 70.64% in 2026. The segment is projected to grow at a CAGR of 7.6% during the forecast period. This is due to their established reliability, worldwide compatibility, and affordability, which make them a must-have for navies everywhere, especially those with conventional and smaller submarine force levels. Horizontal launch systems are simpler to integrate, service, and reload in mission, capable of both torpedo and tube-launched missile variants. Modularity is paramount in the case of multi-role platforms and regional navies that are limited by budget or ship size.

- For instance, in September 2025, Mazagon Dock Shipbuilders (MDL) and ThyssenKrupp Marine Systems began negotiating the contracts for India's Project 75(I) with a focus on six advanced conventional submarines featuring mostly horizontal tube launch systems. This multi-billion-dollar purchase reflects the ongoing demand for horizontal launch technology and operational applicability across Asian and allied regional navies.

By Payload Type

Significant Rate of Integration of UUVs in Submarines for Different Operations Drives the Segmental Growth

The global market, by payload type, is segmented into weapon payloads, sensor payloads, surveillance and reconnaissance equipment, electronic warfare systems, unmanned underwater vehicles (UUVs), and others.

The unmanned underwater vehicles (UUVs) segment is estimated to be the fastest growing segment with the highest CAGR of 9.1%during the forecast period of 2025-2032. This growth path places UUVs as the most vibrant and fast-growing element of submarine payload systems, fueled by their revolutionary contribution to underwater operations and strategic capabilities. Growing use in military and civilian missions for reconnaissance, mine detection, and underwater mapping. Evolving UUV technologies, such as artificial intelligence integration, autonomous navigation systems, and advanced sensor payloads, are transforming submarine operations by increasing operational reach without sacrificing platform stealth or reducing crew risk exposure.

- For instance, in July 2025, the U.S. Naval Research Laboratory awarded General Dynamics Mission Systems a USD 21.5 million contract to modernize and maintain Black Pearl-class autonomous underwater vehicles to accommodate newly developed mission and sensor payloads for emerging undersea warfare studies. The contract comprises the construction of five upgraded Black Pearl UUVs with improved payload capacity and full operational support.

The weapon payload segment is expected to emerge as the leading segment with a 51.37% share in 2026. The segment is projected to grow at a CAGR of 7.1% over the forecast period. The dominance is due to the value to blue-water deterrence operations where advanced warheads and long ranges continue to be the decisive tactical edge. The segment includes torpedoes, cruise missiles, ballistic missiles, and mine systems, all of which are central submarine combat capabilities that frame platform effectiveness and strategic worth. The integration of advanced weapons systems, such as vertical launch capability for Tomahawk cruise missiles and submarine-launched ballistic missiles, guarantees weapon payloads as the key to submarine procurement and modernization decisions.

- For instance, in February 2025, General Atomics Electromagnetic Systems won a contract from General Dynamics Electric Boat to produce and deliver three shipsets of Virginia Payload Tubes (VPT) for Block VI Virginia-class submarines, each shipset comprising two payload tubes and delivery completion by the end of 2030. This contract reflects ongoing commitment to advanced weapon payload launch systems for future submarine platforms.

To know how our report can help streamline your business, Speak to Analyst

By Application

Naval Defense Forces are Continually Upgrading Their Fleet to Remain Dominant in the Market

The market is segmented by application into naval defense forces, research and exploration, and maritime security.

The naval defense forces segment holds a dominant market share of 81.62% in 2026 with a value of USD 2.66 billion. In addition, the segment is estimated to be the fastest growing segment with a CAGR of 7.8% during the forecast period. This pre-eminence is supported by ongoing fleet-modernization budgets demonstrated such as by the FY-2025 U.S. Navy request of USD 18 billion for submarine building and payload modernization and by a wave of similar investments throughout the Indo-Pacific, Europe, and the Middle East. Weaponries swarms of UUVs, long-duration AUVs, and modular sensor packages are allowing navies to push ISR range, perform stand-off strike, and execute clandestine mine-countermeasures while ensuring crew safety. Technological convergence of AI-driven autonomy, low-probability-of-intercept communications and hybrid propulsion is speeding the adoption of capability. Strategic focus on seabed warfare, undersea infrastructure security, and nuclear deterrence underscore that naval defense will be both the largest and the fastest-growing end-use segment over the coming decade.

- For instance, in July 2025, the U.S. Defense Innovation Unit issued a solicitation for one-way attack submarine-launched UUVs with autonomous target identification and kinetic effects, a definitive move toward lethal unmanned undersea strike systems.

The research and exploration segment is projected to emerge as the second fastest growing segment with a CAGR of 7.1% during the forecast period of 2025-2032. Commercial exploration and scientific research represent the second-most-vibrant application group with significant growth as governments, academics, and energy majors seek increased, longer and less expensive ocean penetration. Autonomous and remote-controlled vehicles have reduced the cost of acquiring high-resolution bathymetry, biodiversity surveys and subsea-asset inspection, driving the research and exploration segment of the UUV market.

- For instance, in August 2023, NOAA procured two REMUS 620 mid-class UUVs from HII with 110-hour lifespan and synthetic-aperture sonar to extend high-resolution seafloor mapping for Gulf-of-Mexico restoration, emphasizing the agency's transition toward autonomous deep-ocean science platforms.

Submarine Payload Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Submarine Payload Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 1.24 billion in 2025, representing 35.64% of the global industry, and is expected to reach USD 1.35 billion in 2026.

Nations throughout the region are emphasizing range extension and payload flexibility to tackle varied maritime challenges, generating a strong market for modular payload systems and next-generation sensor systems. The strategic emphasis of the region on indigenous capacity building through technology transfer arrangements and foreign partnerships guarantees ongoing market growth while minimizing the need to rely on foreign suppliers.

China holds the highest market share of 43.26% in the region, which is a result of its enormous naval modernization drive and strategic focus on undersea warfare capabilities. The Asia Pacific region's leadership is attributed to thorough-going submarine fleet expansion programs by more than one nation, with China, India, Japan, and South Korea all investing in both nuclear and conventional submarine capabilities at the same time. Regional security issues, South China Sea territorial claims, and the development of maritime power projection have fueled protracted investment in local payload systems such as cutting-edge torpedoes, cruise missiles, and intelligence-surveillance-reconnaissance capabilities. The Japan market is projected to reach USD 0.23 billion by 2026, the China market is projected to reach USD 0.58 billion by 2026, and the India market is projected to reach USD 0.18 billion by 2026.

North America

North America maintained a strong presence in the global market, reaching USD 0.66 billion in 2025, accounting for 19.15% share, and is expected to reach USD 0.74 billion in 2026. North America's market drive is a result of considerable investments in state-of-the-art submarine technology, such as advanced sonar technologies, unmanned underwater vehicles, electronic warfare suites, and advanced communication modules that provide underwater dominance. The region's focus on the development of stealth technologies, AI-based targeting systems, and next-generation weapon platforms puts North American defense contractors at the pinnacle of submarine payload innovation.

Furthermore, strategic defense programs such as the AUKUS alliance generate new demand streams through Australian personnel training in American shipyards and joint development initiatives for next-generation submarine technologies.

The U.S. Navy Columbia-class SSBN program, the largest submarine acquisition in U.S. history with 12 submarines priced at USD 126.4 billion, generates enormous payload system requirements such as Trident II missile systems and advanced sensor suites. The U.S. market is projected to reach USD 0.7 billion by 2026.

- In April 2025, following two years of talks, the U.S. Navy granted contracts totaling as much as USD 18.5 billion to General Dynamics and HII for the construction of the last two Block V Virginia-class attack submarines. In addition to the detailed design and construction contract for the future Baltimore (SSN-212) and Atlanta (SSN-813), the Navy has also included contracts focused on workforce development that will increase wages for shipbuilders at both facilities.

Europe and the rest of the World

In 2025, Europe generated USD 0.99 billion, contributing 28.57% to global market revenue, and is projected to grow to USD 1.09 billion in 2026, which is fueled by NATO modernization initiatives and upgrades to national submarines in Germany, France, Italy, and the U.K. European defense spending is shifting more toward advanced payload systems such as Thales' CAPTAS sonar suites and Naval Group's F21 heavyweight torpedoes to provide undersea deterrence and interoperability within allied fleets. The UK market is projected to reach USD 0.09 billion by 2026, while the German market is projected to reach USD 0.06 billion by 2026.

- For instance, in July 2025, the U.K.'s Defense Equipment and Support contracted BAE Systems for USD 456 million to provide Sonar 2076 upgrade modules for the Astute and Vanguard class of the Royal Navy, adding to Europe's payload modernization drive.

Rest of the World accounted for USD 0.58 billion in 2025, representing 16.64% of the global market share, and is projected to reach USD 0.61 billion in 2026. The expansion is driven by submarine purchases in Brazil, Turkey, and South Africa under licensed-build and foreign-aid schemes. Emerging players are adding payloads such as Scorpion-class torpedoes and Chinese Y-8 ASW suites to enhance coastal defense and guard offshore assets.

COMPETITIVE LANDSCAPE

Key Market Players

Leading Companies Invest in R&D Activities and Expansion Initiatives to Strengthen Industry Positions

The market expansion of submarine payloads is marked by fierce competition among established defense primes, technology specialists emerging from new technologies, and system integrators. Strategic expansion initiatives include R&D expenditure, mergers & acquisitions, joint ventures, and geographical extension.

Defense manufacturers heavily invest in future-generation payload systems to secure long-term contracts and ensure technological superiority. Such initiatives allow for the fast reconfiguration of missions via standardized interfaces, such as the U.S. Virginia Payload Module and ThyssenKrupp's HDW Class 212A modular UUV launch bays. Companies are also integrating machine learning for target detection, sensor fusion, and adaptive mission planning into UUVs and torpedo guidance systems, combat system with Northrop Grumman's Manta Ray AUV and L3Harris's Iver 4 series at the forefront. They are also creating submarine-launched hypersonic missiles and electric-drive torpedoes to outrun enemy defenses, spearheaded by Lockheed Martin's CPS hypersonic system and MK 54 electric torpedo modernizations.

To diversify capability portfolios and reach new markets, top companies seek M&A and strategic partnerships. For instance, in April 2025, General Dynamics Electric Boat and Huntington Ingalls Industries established a joint industrial base partnership to organize Virginia-class production and supply chain harmonization. Additionally, the September 2021 AUKUS partnership promotes tri-lateral technology exchange among BAE Systems, General Atomics, and Australia's ASC, with accelerated integration of UUVs and VLS architectures. Furthermore, in May 2025, ThyssenKrupp Marine Systems secured a majority stake in South Korea's DSME submarine business, expanding its shipbuilding presence and AIP technology transfer for Asia Pacific projects.

List of Key Global Submarine Payload Companies Profiled

- BAE System PLC (U.K.)

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- General Dynamics Electric Boat (U.S.)

- Northrop Grumman Corporation (U.S.)

- ThyssenKrupp Marine Systems AG (Germany)

- Naval Group (France)

- L3Harris Technologies, Inc. (U.S.)

- Thales Group (Germany)

- Ultra Maritime (U.S.)

- Saab AB (Sweden)

- Huntington Ingalls Industries (HII) (U.S.)

- Kongsberg Gruppen AS (Norway)

- Hanwha Group (South Korea)

- MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan)

- Hensoldt AG (Germany)

COMPETITIVE LANDSCAPE

- August 2025:- The race to construct Canada's upcoming submarine fleet intensified as the South Korean contender reaffirmed its commitment to provide more vessels at a quicker pace than its German competitor. The alternative bidder for the project, which could exceed USD 20 billion, is ThyssenKrupp Marine Systems (TKMS) based in Kiel, Germany. Canada anticipates that the selected shipbuilder will supply the first submarine by the year 2035.

- June 2025:- Hanwha Ocean unveiled the Ocean 2000 submarine, a novel mid-sized diesel-electric attack vessel designed for international markets. Known as the DSME-2000, this submarine enhances the technological heritage of South Korea’s homegrown KSS-III program while being specifically tailored to meet the increasing demand from foreign navies for smaller, highly efficient, and versatile underwater platforms.

- June 2025:- Oceaneering International, Inc. (OII) was awarded a significant firm-fixed-price, indefinite-delivery/indefinite-quantity (IDIQ) contract by the U.S. Navy. With a value of USD 33.13 million, this contract, identified as N64498-25-D-4007, represents a strategic acquisition aimed at providing essential infrastructure and mission-specific equipment for the Navy’s Virginia-class submarine fleet.

- April 2025:- BAE Systems was awarded a contract worth USD 70 million by General Dynamics Electric Boat for the manufacturing of VPM (Virginia Payload Module) missile tubes intended for Block VI Virginia-class submarines. These missile tubes provide essential firepower to the Virginia-class submarine fleet, which is fundamental to U.S. national security.

- January 2025:- The Congressional Budget Office (CBO) report regarding the Navy's FY2025 30-year shipbuilding plan indicated that, when adjusted for constant FY2024 dollars, the average unit procurement cost of the SSN(X) is estimated to be USD 7.1 billion according to the Navy and USD 8.7 billion according to the CBO. The CBO's estimate is approximately 23% greater than that of the Navy. According to the CBO report, this estimate takes into account that the SSN(X) design would have a submerged displacement of around 10,100, which is roughly 11% more than the displacement of the SSN-21 design.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on market trends and market dynamics expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.14% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Product Type · Conventional Submarine · Nuclear Submarine · Air-Independent Propulsion (AIP) · Special Mission Submarines By Launch Mechanism · Vertical Launch Systems (VLS) · Inclined Launch Systems · Horizontal Launch Systems · Canister Launch Systems By Payload Type · Weapon Payloads · Sensor Payloads · Surveillance and Reconnaissance Equipment · Electronic Warfare Systems · Unmanned Underwater Vehicles (UUVs) · Others By Application · Naval Defense Forces · Research and Exploration · Maritime Security By Geography North America (By Product Type, By Launch Mechanism, By Payload Type, By Application, By Country) · U.S. (By Product Type) · Canada (By Product Type) Europe (By Product Type, By Launch Mechanism, By Payload Type, By Application, By Country) · U.K. (By Product Type) · France (By Product Type) · Italy (By Product Type) · Germany (By Product Type) · Russia (By Product Type) · Northern Countries (By Product Type) · Rest of Europe (By Product Type) Asia Pacific (By Product Type, By Launch Mechanism, By Payload Type, By Application, By Country) · China (By Product Type) · India (By Product Type) · Japan (By Product Type) · South Korea (By Product Type) · Australia (By Product Type) · Rest of Asia Pacific (By Product Type) Rest of the World (By Product Type, By Launch Mechanism, By Payload Type, By Application, By Sub-Region) · Middle East & Africa (By Product Type) · Latin America (By Product Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.79 billion in 2026 and is projected to reach USD 6.58 billion by 2034

In 2025, the Europe market value stood at USD 0.99 billion.

The market is expected to exhibit a CAGR of 7.14% during the forecast period of 2026-2034.

The nuclear submarine segment is expected to hold the highest CAGR over the forecast period.

The rising naval modernization and geopolitical tensions fueling the naval modernization programs at the global level are key factors driving the market growth.

Raytheon Technologies, Lockheed Martin, ThyssenKrupp Marine Systems, Thales Group, General Atomics, and among others are top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us