Synthetic Polymer Waxes Market Size, Share & Industry Analysis, By Type (Homopolymer Waxes (Polyethylene Wax (Standard PE Waxes, Oxidized PE Waxes (HDPE-based and LDPE-based))), and Polypropylene Waxes (Standard PP Wax, and Functionalized PP Wax))), Copolymer Waxes (Ethylene–Vinyl Acetate Wax, Ethylene–Acrylic Acid Wax, Ethylene–Butyl Acrylate Wax, Polypropylene–Maleic Anhydride Wax, and Others), Fischer–Tropsch Waxes, and Others), By End-Use (Plastics & Polymer Processing, Adhesives & Sealants, Paints, Coatings & Printing Inks, Paper & Packaging, and Others), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

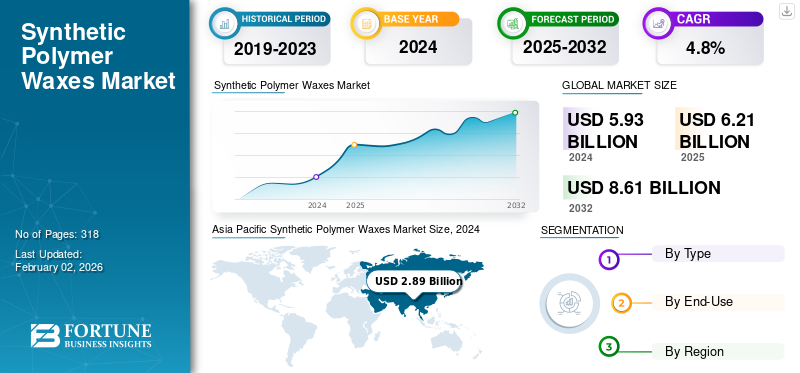

The global synthetic polymer waxes market size was valued at USD 5.93 billion in 2024. The market is projected to grow from USD 6.21 billion in 2025 to USD 8.61 billion by 2032, exhibiting a CAGR of 4.8% during the forecast period. The Asia Pacific dominated global market with a share of 48.74% in 2024.

Synthetic polymer waxes are artificially produced waxes with engineered polymer structures. They offer enhanced properties such as improved abrasion resistance, durability, gloss, and water repellency compared to natural waxes. They are produced through polymerization using materials such as polyethylene, polypropylene, and Fischer-Tropsch waxes. These waxes offer superior heat stability, chemical resistance, and consistency compared to natural wax, enhancing performance in diverse applications such as plastics processing, coatings, and cosmetics. Their engineered properties, including tunable melt points and controlled particle sizes, allow for better formulation control and superior outcomes, including improved lubrication, release, and surface properties. Hence, these waxes are used in various end-use areas, including paints and coatings, plastics, cosmetics, and adhesives, to modify surface characteristics and improve product performance.

There are several top companies in the market, including Clariant, Honeywell International Inc., Sasol Ltd., Micro Powder Inc., and Nanjing Tianshi New Material Technology Co., Ltd. (Tianshi Wax) at the forefront. Broad product portfolio, expansion of production capacities, and strong geographic presence have maintained their supremacy in the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand from PVC Processing & Masterbatch to Propel Market Growth

Synthetic polymer waxes are widely used in plastics processing, especially in PVC applications and masterbatch production, due to their ability to act as lubricants, dispersants, and processing aids. In PVC processing, they balance internal and external lubrication, enabling controlled fusion, smooth extrusion, reduced plate-out, and improved product finish, making them vital for manufacturing pipes, profiles, cables, and films. In masterbatch, they enhance pigment and filler dispersion, support higher loadings, and ensure thermal stability for consistent color strength and surface quality. With PVC remaining one of the most consumed thermoplastics across the construction, automotive, and packaging industries, and the masterbatch sector witnessing steady expansion, the growing use of the product as an essential additive for improving productivity, quality, and efficiency is expected to drive the synthetic polymer waxes market growth.

MARKET RESTRAINTS

Regulatory Pressure on Plastic-Based Products and Substitution Risk to Sluggish Market Growth

Synthetic polymer waxes, primarily derived from polyethylene, polypropylene, and other fossil-based feedstocks, are widely used in plastics, coatings, adhesives, and packaging. However, growing environmental concerns and strict regulations targeting plastic-based products create challenges for producers. Policies such as the EU’s Single-Use Plastics Directive (2019/904) and the U.S. EPA’s recycling and waste reduction initiatives aim to reduce plastic consumption and increase recycled content, indirectly affecting wax demand due to their close link with plastic processing. Additionally, industries are exploring alternatives such as carnauba, beeswax, and rice bran wax, driven by regulatory preference for green materials.

MARKET OPPORTUNITIES

Growing Demand for Micronized and Functionalized Waxes to Create Lucrative Opportunities

Micronized and functionalized polymer waxes are gaining steady attention as industries look for materials that offer higher performance and reliability in coatings, inks, plastics, and adhesives. These advanced waxes provide excellent dispersion, improved scratch and abrasion resistance, and better matting control, helping manufacturers achieve smoother finishes, fewer surface defects, and greater processing efficiency. In coatings, they serve as effective matting agents and slip enhancers. Additionally, functionalized types such as oxidized or grafted waxes improve adhesion and compatibility with polar resins, making them valuable in adhesives, sealants, and inks. In plastics and masterbatch production, they help reduce plate-out, improve melt flow, and support higher pigment loadings. As industries prioritize efficiency and sustainability, these waxes play an important role in simplifying formulations, increasing durability, and extending product performance.

MARKET CHALLENGES

Raw Material and Petrochemical Price Volatility Impacting Market Stability

The market is highly dependent on petrochemical feedstocks such as polyethylene, polypropylene, and other fossil-based derivatives. Fluctuations in crude oil prices and instability in global petrochemical supply chains directly influence production costs and profit margins for manufacturers. Factors such as geopolitical tensions, trade restrictions, and energy market disruptions often cause unpredictable swings in raw material availability and pricing. These cost variations make it difficult for producers to maintain consistent pricing strategies and long-term supply commitments. Additionally, increasing demand for alternative energy sources and recycled polymers is further reshaping feedstock dynamics. As a result, managing raw materials and petrochemical price volatility has become a critical challenge for manufacturers, affecting both operational planning and market competitiveness.

SYNTHETIC POLYMER WAXES MARKET TRENDS

Growing Innovation in Bio-Based and Hybrid Synthetic Polymer Waxes is a Key Trend

The market is steadily moving toward more sustainable and eco-friendly solutions as industries emphasize reducing environmental impact and meeting stricter regulatory standards. Manufacturers are increasingly developing bio-based and hybrid waxes derived from renewable feedstocks that deliver superior performance to traditional synthetic waxes. These next-generation formulations are being tailored for use in coatings, plastics, adhesives, and packaging applications, where functionality and sustainability are becoming critical. In addition, advancements in polymer chemistry and processing technologies allow producers to fine-tune properties such as melting point, hardness, and compatibility with other materials. This shift toward cleaner, more efficient, and responsible wax formulations shows how the industry is evolving to meet both performance demands and environmental goals.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Homopolymer Waxes Led Market Due to Broad Usage and Reliable Performance

On the basis of by type, the market is classified into Homopolymer Waxes (Polyethylene Wax (Standard PE Waxes, Oxidized PE Waxes (HDPE-based and LDPE-based))), and Polypropylene (PP) Waxes (Standard PP Wax, and Functionalized PP Wax))), Copolymer Waxes (Ethylene–Vinyl Acetate (EVA) Wax, Ethylene–Acrylic Acid (EAA) Wax, Ethylene–Butyl Acrylate (EBA) Wax, Polypropylene–Maleic Anhydride (PP–MA) Wax, and Others), Fischer–Tropsch (FT) Waxes, and Others.

Homopolymer waxes held the dominant synthetic polymer waxes market share in 2024, due to their versatility, stable performance, and cost-effectiveness. This category includes polyethylene (PE) waxes and polypropylene (PP) waxes, available in standard and functionalized forms. PE waxes, both HDPE- and LDPE-based, offer excellent lubrication, thermal stability, and chemical resistance, while oxidized grades enhance adhesion and dispersion. PP waxes provide higher melting points, superior hardness, and better compatibility with polyolefin systems, making them ideal for masterbatch, fiber, and film applications. Owing to their wide industrial use and consistent quality, homopolymer waxes continue to lead the global market.

Copolymer waxes, including Ethylene–Vinyl Acetate (EVA), Ethylene–Acrylic Acid (EAA), Ethylene–Butyl Acrylate (EBA), and Polypropylene–Maleic Anhydride (PP–MA) waxes, are increasingly being adopted for their improved functionality and compatibility across diverse applications. These waxes provide excellent adhesion, dispersion, and surface protection, making them suitable for coatings, adhesives, inks, and polymer processing. EVA and EAA waxes are valued for their strong bonding and film-forming properties, while PP–MA waxes offer better interaction with polar resins. Their ability to enhance processing efficiency and deliver consistent performance is contributing to the rising demand for copolymer waxes in advanced and specialized industrial uses.

By End-Use

To know how our report can help streamline your business, Speak to Analyst

Rising Demand for High-performance Plastic Components Across Industries Fuels Plastics & Polymer Processing Segment Growth

Based on end-use, the market is segmented into plastics & polymer processing, adhesives & sealants, paints, coatings & printing inks, paper & packaging, and others.

The plastics & polymer processing segment dominates the market, driven by increasing use of these waxes as lubricants, dispersants, and processing aids in polymer manufacturing. It plays a crucial role in improving melt flow, reducing friction, and enhancing the surface quality of finished products. They are widely used in PVC, masterbatch, film extrusion, and injection molding applications, where precise control over lubrication and fusion is essential. In PVC processing, they help balance internal and external lubrication, prevent plate-out, and ensure smooth extrusion, while in masterbatch production, they improve pigment dispersion and thermal stability. The growing demand for lightweight, durable, and high-performance plastic components across industries such as construction, automotive, and packaging continues to strengthen the use in this segment. Furthermore, the segment is projected to grow at a CAGR of 5.3% during the study period.

The paints, coatings, and printing inks segment held a 23.2% share in 2024. Increasing demand for high-performance, durable, and aesthetically appealing surface finishes is driving the use of synthetic polymer waxes in this segment. These waxes enhance scratch and abrasion resistance, improve slip, and provide precise gloss control, resulting in smoother and longer-lasting coatings. The growing adoption of advanced micronized and functionalized waxes for improved dispersion and chemical resistance further supports the segment’s strong growth outlook.

Synthetic Polymer Waxes Market Regional Outlook

By region, the market is divided into Latin America, North America, Asia Pacific, the Middle East & Africa, and Europe.

Asia Pacific

Asia Pacific Synthetic Polymer Waxes Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the leading share in 2023, valued at USD 2.72 billion. It also took the largest share in 2024 with USD 2.89 billion, and is anticipated to maintain its dominance during the forecast period. The anticipated growth is on the back of countries such as China, India, South Korea, and Japan, which are major consumers in the region. China, being the manufacturing hub of a few major end-user industries such as plastics, adhesives, and coatings, will act as a growth lever in the regional market. Growing urbanization, industrial growth, and increasing infrastructure projects in the region are creating high demand for synthetic polymer waxes.

To know how our report can help streamline your business, Speak to Analyst

Europe

The market in Europe is set to register a prominent growth over the forecast period. It is expected to rise at a CAGR of 4.2%, the second-highest among all regions, and reach USD 1.39 billion by 2025. In Europe, market demand is driven by the presence of large end-use industries, including automotive, industrial coatings, and packaging sectors. Countries such as Germany, Italy, and France are major markets for plastics and chemical manufacturing, where polymer waxes are extensively used as processing aids and dispersing agents. The region also places a high focus on eco-friendly and high-performance materials, supporting the shift toward sustainable polymer wax applications. Supported by these aspects, countries such as the U.K. are predicted to touch the valuation of USD 0.15 billion, Germany to witness USD 0.33 billion, and France to record USD 0.18 billion in 2025.

North America

North America is expected to touch a valuation of USD 1.25 billion in 2025 and mark the position of the third-largest region in the market. In North America, the U.S. dominates the market, with increasing demand from the plastics, adhesives, and printing inks industries. Also, the region benefits from strong automotive production, packaging innovation, and advanced construction materials. The rising adoption of sustainable coatings and adhesives is fostering new growth opportunities in the region. In 2025, the U.S. market is estimated to reach USD 1.02 billion.

Latin America

Latin America is projected to witness USD 0.30 billion in 2025. Market expansion in the region is driven by rising industrialization and expanding packaging and construction activities. Countries such as Brazil and Mexico are key markets, with demand for adhesives, coatings, and paper packaging steadily increasing. The presence of multinational manufacturers and growing investments in downstream chemical industries are expected to support regional growth during the forecast period.

Middle East & Africa

The Middle East & Africa market is expected to grow at a 4.9% CAGR during the forecast period. Countries such as the GCC and South Africa are witnessing huge demand for coatings, adhesives, and plastic processing materials due to large-scale infrastructure and construction projects. Countries such as Saudi Arabia, the UAE, and Qatar are investing billions in large-scale construction projects and smart cities, including NEOM in Saudi Arabia. Synthetic waxes are essential for high-performance coatings, additives, and asphalt modification in these projects. GCC is expected to achieve the value of USD 0.06 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Companies Emphasize Collaborations and Acquisitions to Maintain Their Dominance

Industry giants push ahead using their scale, innovative research, and green initiatives, while regional firms excel in agility, affordability, and their proximity to local infrastructure. The field features major players such as Nanjing Tianshi New Material Technology Co., Ltd. (Tianshi Wax), Honeywell International Inc., Sasol Ltd., Clariant, and Micro Powder Inc. These companies are actively expanding, acquiring, and teaming up across markets.

LIST OF KEY SYNTHETIC POLYMER WAX COMPANIES PROFILED

- BASF SE (Germany)

- Clariant (Switzerland)

- Lubrizol (U.S.)

- Honeywell International Inc. (U.S.)

- Evonik Industries AG (Germany)

- Nucera Solutions (U.S.)

- Mitsui Chemicals Inc. (Japan)

- DEUREX AG (Germany)

- Sasol Ltd. (South Africa)

- SCG Chemicals Public Company Limited (Thailand)

- Westlake Corporation (U.S.)

- Shamrock Technologies (U.S.)

- Innospec (U.S.)

- Micro Powders Inc. (U.S.)

- Qingdao Sainuo Chemical Co., LTD. (China)

- GMT Corporation (South Korea)

- Marcus Oil (India)

- Nanjing Tianshi New Material Technology Co., Ltd. (Tianshi Wax) (China)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Sasol Chemicals expanded its micronized waxes line by introducing SASOLWAX LC Spray 30 G and LC Spray 30 G-EF, achieving a 32% lower Product Carbon Footprint than standard grades. These products are specifically designed for use in coatings, inks, and packaging applications. The key feature of these new waxes is their significantly lower carbon footprint compared to standard Sasol waxes, achieved through optimizations in the Gas-to-Liquid (GTL) Fischer-Tropsch (FT) production process.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 4.8% from 2025-2032 |

|

Unit |

Value (USD Billion), Volume (Kilotons) |

|

Segmentation |

By Type, End-Use, and Region |

|

By Type |

|

|

By End-Use |

|

|

By Region |

North America (By Type, End-Use, and Country)

Europe (By Type, End-Use, and Country/Sub-region)

Asia Pacific (By Type, End-Use, and Country/Sub-region)

Latin America (By Type, End-Use, and Country/Sub-region)

Middle East & Africa (By Type, End-Use, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.93 billion in 2024 and is projected to reach USD 8.61 billion by 2032.

In 2024, the market value stood at USD 2.89 billion.

The market is expected to exhibit a CAGR of 4.8% during the forecast period of 2025-2032.

Homopolymer waxes led the market by type.

The key factor driving the market is the rising demand from PVC Processing & Masterbatch.

Clariant, Honeywell International Inc., Sasol Ltd., Micro Powder Inc., and Nanjing Tianshi New Material Technology Co., Ltd. are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

Increased demand for high-performance and sustainable wax formulations across the coatings, plastics, and adhesives industries is expected to favor product adoption.

- 2019-2032

- 2024

- 2019-2023

- 318

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us