Voluntary Carbon Credit Market Size, Share & Industry Analysis, By Project Type (Avoidance or Reduction Projects, Nature-Based Solutions, and Carbon Removal), By Buyer Type (Corporate, SME, Government, and Others), By End User (Aviation, Oil & Gas, Technology & Data Centers, Industrial, and Others), and Regional Forecast, 2026-2034

Voluntary Carbon Credit Market Size and Future Outlook

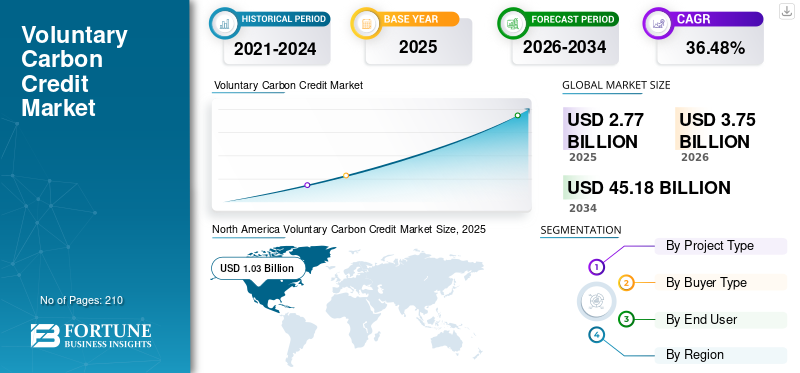

The global voluntary carbon credit market size was valued at USD 2.77 billion in 2025. The market is projected to grow from USD 3.75 billion in 2026 to USD 45.18 billion by 2034, exhibiting a CAGR of 36.48% during the forecast period. North America dominated the voluntary carbon credit market with a market share of 37.18% in 2025.

Companies are increasingly using voluntary carbon credits to address offset emissions that cannot yet be eliminated through operational decarbonization. The growing adoption of corporate climate targets and expansion of voluntary carbon offset projects are key drivers of the market growth. According to the Science Based Targets initiative (SBTi), as of 2024, more than 4,200 companies globally have validated or committed to science-based climate targets, reflecting strong corporate alignment with the Paris Agreement. Many of these organizations incorporate carbon credits within broader climate strategies to compensate for residual emissions reductions while transitioning to low-carbon operations. Cap and trade indirectly influences the market by setting carbon price benchmarks and encouraging companies to offset the emissions beyond regulatory requirements.

At the same time, the supply of voluntary carbon credits has grown through large-scale offset projects, including forest conservation, afforestation and reforestation, renewable energy development, and methane capture initiatives. Data from Verra indicates that by 2023, the Verified Carbon Standard (VCS) program had issued over 1 billion carbon credits globally, demonstrating the expanding scale of voluntary carbon mitigation projects. In addition, governments and international organizations are increasingly encouraging private-sector participation in climate finance and nature-based solutions, particularly in emerging economies.

- For instance, in April 2023, Microsoft expanded its voluntary carbon credit procurement as part of its commitment to become carbon negative by 2030. The company signed agreements to purchase carbon removal credits from several projects, including reforestation, Bioenergy With Carbon Capture And Storage (BECCS), and direct air capture initiatives.

Some of the leading companies operating in the industry include Ecosecurities and Puro.earth, Biofílica Ambipar, BioCarbon Partners, and others. EcoSecurities is a global environmental company specializing in the development, sourcing, and commercialization of carbon credits and climate mitigation projects. The company supports governments, corporations, and financial institutions in implementing nature-based and technology-based carbon offset projects across sectors such as forestry, renewable energy, and land-use management. Carbon prices in the market are determined by project type, credit quality, certification standard, and buyer demand, typically varying widely based on environmental integrity and co-benefits.

Download Free sample to learn more about this report.

Voluntary Carbon Credit Market Takeaways

- 2025 Market Size: USD 2.77 Billion

- 2026 Market Size: USD 3.75 Billion

- 2034 Forecast Market Size: USD 45.18 Billion

- CAGR: 36.48% from 2026–2034

- North America dominated the voluntary carbon credit market with a 37.18% share in 2025.

- The carbon removal segment is projected to register the highest growth at a CAGR of 38.10% during the forecast period.

- The technology & data centers segment is expected to grow at a CAGR of 38.40% from 2026–2034.

North America

North America led the market in 2025 with a valuation of USD 1.03 billion and is projected to reach USD 1.38 billion in 2026.

Europe

Europe reached USD 0.85 billion in 2025 and is projected to record a strong CAGR of 37.09% during the forecast period.

Asia Pacific

Asia Pacific generated USD 0.57 billion in 2025.

U.S.

The U.S. market was valued at approximately USD 0.92 billion in 2025, accounting for around 33.19% of global market revenue.

Japan

The Japan market reached approximately USD 0.17 billion in 2025, representing about 6.21% of global market revenues.

Read More

VOLUNTARY CARBON CREDIT MARKET TRENDS

Growing Digital Infrastructure and Transparency Mechanisms is the Prominent Market Trend

A major trend shaping the market is the rapid development of digital infrastructure and transparency mechanisms to improve credit traceability and market integrity. Carbon registries and exchanges are increasingly adopting digital Monitoring, Reporting, And Verification (MRV) systems, blockchain-enabled registries, and satellite-based monitoring to ensure accurate measurement of emission reductions and prevent double counting of carbon credits. Clean energy projects such as wind, solar, hydro, and biomass generate carbon credits by reducing or avoiding greenhouse gas emissions compared to fossil fuel-based energy sources.

For instance, in June 2023, the Integrity Council for the Voluntary Carbon Market (ICVCM) released its Core Carbon Principles (CCPs) framework to establish global quality benchmarks for carbon credits and improve transparency in the market (Source: ICVCM). Similarly, in September 2023, Verra introduced updates to its Verified Carbon Standard (VCS) program, strengthening rules for project monitoring, credit issuance, and risk management to enhance market credibility (Source: Verra Registry Updates).

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Nature-Based Carbon Offset Projects to Drive the Market Growth

A key driver of the market is the rapid expansion of nature-based carbon offset projects, particularly those focused on forest conservation, reforestation, and land-use management. These projects generate verified emission reductions while also supporting biodiversity protection and community livelihoods. According to Verra, as of December 2023, more than 2,000 projects were registered under the Verified Carbon Standard (VCS) globally, with forestry and land-use projects representing a significant share of issued voluntary carbon credits (Source: Verra Registry Database).

In addition, in October 2023, the World Bank highlighted that nature-based solutions could deliver up to 30% of the global mitigation needed by 2030 to meet climate goals (Source: World Bank Climate and Nature Report). These projects are attracting increasing participation from corporations seeking high-quality carbon offsets while contributing to sustainable development objectives. These factors are anticipated to drive the CAGR during the forecast period.

MARKET RESTRAINTS

Concerns Over Credit Quality and Market Integrity to Hamper the Market Demand

A significant restraint in the market is the growing scrutiny over the environmental integrity and quality of certain carbon offset projects, particularly those linked to avoid deforestation and land-use activities. Questions regarding additionality, permanence, and accurate emissions measurement have led to increased market caution among buyers.

For instance, in January 2023, according to Verra forest projects, an investigation highlighted concerns about the credibility of some rainforest carbon credits issued under voluntary programs, prompting calls for stronger verification frameworks and transparency standards. In response to such concerns, registries and governance bodies have begun tightening methodologies and monitoring procedures to strengthen credit credibility.

MARKET OPPORTUNITIES

Integration of Carbon Credits with Global Carbon Removal Technologies to Propel Market Growth Opportunities

A major opportunity in the market is the growing integration of carbon removal technologies such as direct air capture (DAC), bioenergy with carbon capture and storage (BECCS), and enhanced mineralization, which can generate high-quality carbon removal credits. These technologies are attracting increasing investment as corporations seek durable carbon removal solutions to meet long-term climate commitments.

For instance, in September 2023, Climeworks announced the expansion of its Mammoth direct air capture plant in Iceland, which is expected to capture up to 36,000 tons of CO₂ annually once fully operational. Projects like these create verified carbon removal credits that can be sold in voluntary carbon markets. Additionally, governments and international climate initiatives are supporting carbon removal technologies as part of broader decarbonization strategies.

MARKET CHALLENGES

Uncertainty In Regulatory Frameworks And Carbon Market Alignment To Hinder Market Growth

A major challenge in the voluntary carbon credit market growth is the uncertainty surrounding regulatory frameworks and the alignment between voluntary and compliance carbon markets. Governments and international climate bodies are still developing policies that define how voluntary carbon credits can be used alongside global emissions reduction commitments under the Paris Agreement.

For instance, in November 2022, discussions during COP27 highlighted the ongoing need to clarify the implementation of Article 6 of the Paris Agreement, which governs international carbon trading mechanisms and corresponding adjustments between countries. These evolving rules create uncertainty for project developers and corporate buyers regarding how these credits may be recognized within future compliance systems.

Segmentation Analysis

By Project Type

Avoidance or Reduction Projects Dominated Due to Lower Costs and Faster Credit Generation

Based on project type, the market is classified into avoidance or reduction projects, nature-based solutions, and carbon removal.

In 2025, avoidance or reduction projects dominated the market share as they generate carbon credits more quickly and at lower costs compared to removal-based projects. These projects focus on preventing carbon emissions that would otherwise occur, such as through renewable energy deployment, improved cookstoves, methane capture, or forest conservation.

The carbon removal segment is set to experience highest growth rate of 38.10%.

To know how our report can help streamline your business, Speak to Analyst

By Buyer Type

Corporate is Dominant Buyer Type Due to Corporate Net-Zero and ESG Commitments

Based on the buyer type, the market is classified into corporate, SME, government, and others.

In 2025, the corporate segment dominated the global market as companies increasingly use carbon credits to meet net-zero, carbon neutrality, and broader ESG commitments. Many multinational corporations have pledged emission-reduction targets aligned with frameworks such as the Science Based Targets initiative (SBTi) and the Paris Agreement. While firms focus on reducing emissions within their operations and supply chains, voluntary carbon credits are used to offset residual emissions that cannot yet be eliminated.

The government segment is expected to grow at a CAGR of 36.94% during the forecast period.

By End User

Oil & Gas Holds The Leading Share Due To High Regulatory Compliance And Discharge Monitoring

On the basis of the end user, the market is classified into aviation, oil & gas, technology & data centers, industrial, and others.

In 2025, the oil & gas segment dominated the global market as companies in this industry face significant scrutiny from regulators, investors, and environmental groups to reduce their carbon footprint. While many firms are investing in operational efficiency, methane reduction, carbon capture, and renewable energy integration, achieving complete decarbonization remains challenging in the short term.

The technology & data centers segment is expected to grow at a CAGR of 38.40% from 2026 to 2034.

VOLUNTARY CARBON CREDIT MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Voluntary Carbon Credit Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the highest share in 2025, valued at USD 1.03 billion, and expected to reach USD 1.38 billion in 2026. North America dominates the voluntary carbon credit market share primarily due to strong corporate climate commitments, well-established carbon market infrastructure, and active participation from large multinational companies. The U.S. and Canada host many global corporations that have adopted net-zero and carbon neutrality targets, increasing demand forcarbon credits to offset residual emissions. Additionally, the region has a mature ecosystem of carbon registries, project developers, and financial institutions that facilitate credit generation, trading, and verification. Organizations such as Verra, the American Carbon Registry, and Climate Action Reserve play a key role in supporting project certification and market transparency.

U.S. Voluntary Carbon Credit Market

Based on North America’s strong contribution and the U.S.’s dominance within the region, the U.S. market was analytically approximated at around USD 0.92 billion in 2025, accounting for roughly 33.19% of the global market size.

Europe

Europe is projected to record a growth rate of 37.09% in the coming years, which is the second-highest among all regions and reached a valuation of USD 0.85 billion in 2025. Europe holds a significant position in the market due to strong climate policies, ambitious emission reduction targets, and widespread corporate sustainability initiatives. The European Union’s commitment to achieving climate neutrality by 2050 has encouraged companies to actively participate in carbon markets to offset residual emissions.

Germany Voluntary Carbon Credit Market

The Germany market in 2025 was valued around USD 0.20 billion 2025 and is estimated at around USD 0.28 billion in 2026, representing roughly 7.26% of the global market revenues. Germany is an active participant in the market, driven by strong corporate decarbonization commitments and the country’s goal to achieve climate neutrality by 2045.

Asia Pacific

Asia Pacific reached USD 0.57 billion in 2025. In the region, India and China both reached USD 0.10 billion and USD 0.06 billion, respectively, in 2025. Asia Pacific is an important and rapidly growing region in the market due to the large availability of nature-based and renewable energy projects. Indonesia, India, China, and Australia host numerous carbon offset projects, including forestry conservation, clean cookstoves, and methane reduction initiatives.

Japan Voluntary Carbon Credit Market

The Japan market in 2025 was around USD 0.17 billion, accounting for roughly 6.21% of global market revenues. Japan is an active buyer in the market, driven by corporate decarbonization targets and country’s commitment to achieving net-zero emissions by 2050.

China Voluntary Carbon Credit Market

China’s market is projected to be significant country, with 2025 around USD 0.06 billion, representing roughly 2.06% of the global market.

India Voluntary Carbon Credit Market

The India voluntary carbon credit market in 2025 is estimated at around USD 0.10 billion, accounting for roughly 3.60% of global revenues.

Latin America

The Latin America market is set to reach a valuation of USD 0.19 billion in 2025 and is expected to witness moderate growth during the forecast period. Latin America plays a significant role in the market due to its vast natural ecosystems that support large-scale nature-based carbon projects. Brazil, Peru, and Colombia host numerous forestry, REDD+, and land-use conservation projects that generate substantial volumes of carbon credits.

Brazil Voluntary Carbon Credit Market

Brazil's market was worth USD 0.12 billion in 2025, representing roughly 4.33% of the market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market reached a valuation of USD 0.13 billion in 2025. The Middle East & Africa is an emerging region in the market, supported by growing climate commitments and sustainability initiatives. Countries such as the UAE, Saudi Arabia, Kenya, and South Africa are increasingly investing in carbon offset projects, including renewable energy, reforestation, and land restoration.

GCC Voluntary Carbon Credit Market

The GCC market was around USD 0.08 billion in 2025, representing roughly 2.73% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Are Expanding Their Market Shares Via Partnerships, Business Expansion, And Technological Advancements

The global voluntary carbon credit market holds a consolidated market structure, constituting Ecosecurities, Puro.earth, Biofílica Ambipar, BioCarbon Partners, and others as its prominent players. They are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other strategies.

- For instance, in July 2024, Google signed a long-term agreement with Holocene, a U.S.-based carbon removal company, to purchase 100,000 tons of direct air capture (DAC) carbon removal credits. The agreement supports Google’s strategy to neutralize hard-to-abate emissions while helping scale emerging carbon removal technologies.

Other key players in the global market include BURN Manufacturing, AB Verra, Indus Delta Capital Limited, Terrasos, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY VOLUNTARY CARBON CREDIT COMPANIES PROFILED

- EcoSecurities (U.K.)Puro.earth (Finland)

- Biofílica Ambipar (Brazil)

- EKI Energy Services Ltd. (formerly EnKing International) (India)

- BURN Manufacturing (Kenya)

- AB Verra (U.S.)

- Terrasos (Colombia)

- Climate Impact Partners (U.K.)

- EcoAct (France)

- 3Degrees (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2024: Microsoft announced a long-term agreement with 1PointFive, a subsidiary of Occidental, to purchase 500,000 tons of carbon removal credits from a direct air capture facility being developed in Texas. The agreement represents one of the largest corporate commitments to engineered carbon removal and highlights increasing demand for durable carbon credits. Such contracts help finance large-scale carbon capture infrastructure while enabling companies to address residual emissions.

- March 2024: Amazon announced an agreement with Orbital Materials and other climate project developers to purchase carbon removal credits as part of its Climate Pledge commitment to reach net-zero carbon by 2040. The initiative focuses on supporting projects that capture or remove carbon dioxide from the atmosphere, including engineered carbon removal technologies. By committing to advance purchases of carbon removal credits, Amazon aims to stimulate the growth of emerging carbon removal solutions.

- January 2024: Singapore-based Climate Impact X (CIX) expanded its digital marketplace for voluntary carbon credits, enabling corporations to purchase high-quality carbon offsets from verified projects globally. The platform integrates standardized contracts and transparent project information to improve price discovery and credit traceability. This expansion reflects increasing institutional interest in structured carbon trading platforms designed to support the scaling of market.

- December 2023: The Integrity Council for the Voluntary Carbon Market (ICVCM) approved the first group of carbon credit methodologies under its Core Carbon Principles (CCP) label. The initiative aims to establish globally recognized benchmarks for high-quality carbon credits and improve trust. The CCP label helps corporate buyers identify credible carbon credits that meet stringent environmental and governance standards, supporting the development of a more transparent and reliable voluntary carbon credit ecosystem.

- October 2023: Shell signed agreements to purchase carbon credits generated from nature-based projects focused on forest conservation and restoration in Southeast Asia and Latin America. The initiative is part of Shell’s broader strategy to invest in natural carbon sinks while supporting local biodiversity and community development. Such large-scale corporate participation demonstrates how energy companies are increasingly using voluntary carbon credits to complement their emissions reduction pathways.

REPORT COVERAGE

The global voluntary carbon credit market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 36.48% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Project Type, Buyer Type, End User, and Region |

| By Project Type |

|

| By Buyer Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.77 billion in 2025 and is projected to reach USD 45.18 billion by 2034.

In 2025, the market value stood at USD 0.57 billion.

The market is expected to exhibit a CAGR of 36.48% during the forecast period.

The avoidance or reduction projects segment led the market by project type.

Increasing corporate net-zero commitments, expansion of nature-based and carbon removal projects are the key factors driving the market.

Ecosecurities, Puro.earth, and Biofílica Ambipar are some of the prominent players in the market.

North America dominated the market in 2025.

Corporate net-zero targets, increasing climate regulations, expansion of carbon offset projects, and rising ESG commitments are major factors.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us