Water Treatment Polymers Market Size, Share & Industry Analysis, By Product Type (Polyacrylamides, PolyDADMAC, Polyamines, Bio-based Polymers, and Others), By End Use (Municipal Water Treatment, Industrial Water Treatment, Mining & Mineral Processing, and Others), and Regional Forecast, 2026-2034

Water Treatment Polymers Market Size and Future Outlook

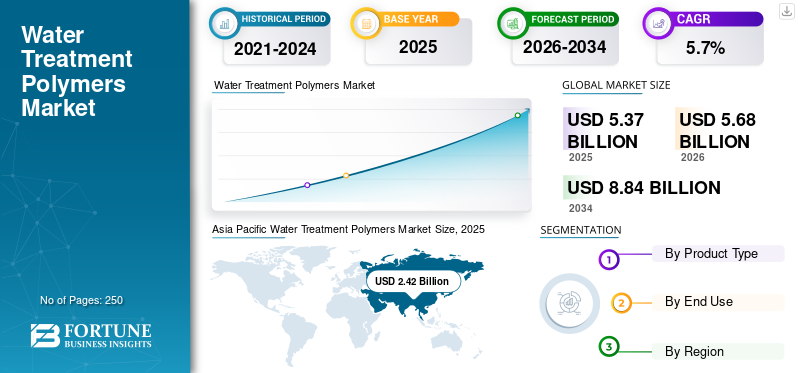

The global water treatment polymers market size was valued at USD 5.37 billion in 2025. The market is projected to grow from USD 5.68 billion in 2026 to USD 8.84 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the water treatment polymers market with a market share of 45.06% in 2025.

Water treatment polymers are specialty water-soluble polymers used to improve solid-liquid separation, clarification, coagulation, flocculation, sludge conditioning, and sludge dewatering in municipal and industrial water systems. These polymers include polyacrylamide-based flocculants, PolyDADMAC, polyamines, bio-based polymers, and specialty polymer blends. Such polymers enhance water quality by acting as powerful coagulants and flocculants that bind small particles, colloids, and contaminants into larger clusters (flocs) for easy removal. Tightening regulations on industrial effluent discharge necessitate advanced water treatment, driving the demand for water treatment polymers. Depletion of fresh water sources forces industries and municipalities to recycle water, requiring effective water treatment technologies. Hence, the rising pressure on municipalities and industries to improve wastewater treatment efficiency, reduce sludge disposal volumes, and increase water reuse is driving the global market.

A mix of large multinational water-chemical suppliers and regional polymer manufacturers, including SNF Group, Kemira, Solenis, Ecolab, and Veolia Water Technologies, shapes the global market. These companies compete through product performance, support for treatment-plant optimization, sludge dewatering expertise, local supply reliability, and application-specific formulations.

Download Free sample to learn more about this report.

Water Treatment Polymers Market Key Takeaways

- 2025 Market Size: USD 5.37 billion

- 2026 Market Size: USD 5.68 billion

- 2034 Forecast Market Size: USD 8.84 billion

- CAGR: 5.7% from 2026–2034

- Asia Pacific dominated the market with a 45.06% share in 2025.

- Polyacrylamides segment held the largest market share in 2025.

- Municipal water treatment segment held the largest market share in 2025.

North America

The market reached USD 1.21 billion in 2025, driven by wastewater infrastructure and industrial demand.

Asia Pacific

The market reached USD 2.42 billion in 2025, driven by wastewater infrastructure expansion.

Europe

The market reached USD 1.14 billion in 2025, supported by strict wastewater regulations.

U.S.

The market is projected to reach USD 1.12 billion by 2026, driven by wastewater treatment demand.

Japan

The market is expected to grow steadily, supported by water reuse and wastewater treatment.

Read More

WATER TREATMENT POLYMERS MARKET TRENDS

Momentum Toward Biobased and Lower-Residual Polymer Alternatives is a Key Market Trend

The market is seeing growing interest in bio-based, low-residual polymer alternatives as municipalities and industries seek safer, more sustainable water treatment solutions. Conventional synthetic polymers, especially polyacrylamide-based products, continue to dominate due to their strong performance in flocculation, clarification, and sludge dewatering. However, growing attention toward residual monomer content, biodegradability, and environmental discharge quality is encouraging suppliers to develop more sustainable products. As a result, naturally derived products such as chitosan, starch, cellulose, and tannin-based polymers, as well as lower-residual, renewable product options, are gaining relevance in sensitive applications such as drinking water treatment, food processing wastewater, and environmentally regulated industrial effluents. Although bio-based polymers remain a small-volume segment, their adoption is expected to increase as performance improves and sustainability becomes a stronger procurement criterion.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stricter Industrial Effluent Regulations and Growing Demand from Industrial Sectors are Set to Drive Market Growth

Stricter industrial effluent discharge regulations are increasing the need for polymer-based clarification, solids removal, and sludge conditioning across manufacturing sectors. As industries face tighter limits on suspended solids, color, oil and grease, organic load, and sludge disposal quality, they need more dependable treatment chemicals to maintain compliance. Water treatment polymers help plants improve floc formation, reduce turbidity, enhance dissolved air flotation performance, and increase sludge dewatering efficiency, enabling faster and more consistent contaminant removal.

The regulatory pressure is especially important for chemicals, textiles, food and beverage, pulp and paper, metals, oil and gas, and power generation, where wastewater composition is complex and variable. As a result, industrial users are shifting from basic treatment practices toward optimized polymer-based treatment programs. Therefore, stricter industrial effluent regulations and rising demand from various industrial sectors are set to drive the global water treatment polymers market growth.

- For instance, as per India's CPCB Effluent Norms 2026, strict limits on Total Suspended Solids (TSS) of 100 mg/L for surface water and 600 mg/L for sewers, forcing manufacturing units to use cationic polymers for sludge dewatering.

MARKET RESTRAINTS

Environmental Concerns over Residual Monomers and Synthetic Polymer Persistence Limit Adoption in Sensitive Applications

Environmental concerns related to residual monomers and the persistence of synthetic polymers may limit adoption in sensitive water treatment applications. Polyacrylamide-based polymers are widely used due to their strong flocculation and dewatering performance. Still, residual acrylamide content remains a key quality and regulatory consideration, particularly in drinking water and environmentally sensitive discharge applications.

Concerns around the long-term fate of synthetic polymer residues in sludge, treated water, and receiving environments are encouraging closer scrutiny from utilities, industries, and regulators. These concerns do not eliminate demand, but they increase the need for stricter product specifications, lower-residual grades, careful dosing, and application-specific approvals. As a result, suppliers may face higher compliance requirements and pressure to develop safer or more biodegradable alternatives.

MARKET OPPORTUNITIES

Water Reuse and Zero-Liquid Discharge Projects Create Opportunities for Market Players

Water reuse and zero-liquid discharge (ZLD) projects are creating opportunities for advanced polymer treatment solutions across municipal and industrial facilities. As water scarcity increases and industries aim to reduce freshwater withdrawal, treatment systems are increasingly designed to recover, recycle, and reuse water. Polymers play an important role in these systems by improving suspended-solids removal, reducing turbidity, supporting clarification, protecting downstream filters or membranes, and enhancing sludge dewatering. In zero-liquid discharge facilities, effective solids separation becomes even more critical, as poor pretreatment can increase scaling and fouling and increase operating costs. This creates demand for high-performance flocculants, organic coagulants, and customized polymer programs that can handle variable wastewater chemistry. Growth in reuse and ZLD projects, therefore, opens a higher-value opportunity beyond conventional wastewater treatment.

Segmentation Analysis

By Product Type

Polyacrylamides Dominate Market Owing to Their Extensive Use in Flocculation, Clarification, and Sludge Dewatering

Based on product type, the market is segmented into polyacrylamides, PolyDADMAC, polyamines, bio-based polymers, and others.

Polyacrylamides account for the largest global water treatment polymers market share due to their widespread use in municipal wastewater treatment, sludge dewatering, industrial effluent clarification, mining tailings treatment, and raw water clarification. These polymers are available in anionic, cationic, non-ionic, and amphoteric forms, allowing treatment plants to select grades based on sludge type, suspended solids, water chemistry, and separation equipment. Their strong floc-forming ability, high molecular weight, and compatibility with centrifuges, belt presses, thickeners, and clarification systems continue to support their dominant market position.

The PolyDADMAC segment is projected to grow at 6.0% CAGR during 2026–2034, supported by its role as a cationic organic coagulant in raw water treatment, wastewater clarification, filtration support, and sludge conditioning. It is commonly used where charge neutralization is required to destabilize colloids and improve the removal of turbidity, suspended solids, and organic matter. Segment growth is driven by adoption in municipal drinking water plants, industrial effluent systems, and treatment facilities seeking alternatives or complements to inorganic coagulants.

Bio-based polymers represent a small but rapidly growing segment of the market. The segment includes chitosan-based, starch-based, cellulose-based, tannin-based, and other modified natural polymers used as coagulants, flocculants, or sludge-conditioning aids. These products are gaining attention as municipalities and industries look for lower-toxicity, biodegradable, and renewable alternatives to conventional synthetic polymers. The segment is projected to expand at a 7.1% CAGR during 2026–2034, making it the fastest-growing product category, although adoption remains selective due to performance, cost, and availability considerations.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Municipal Water Treatment Leads Market Due to Recurring Demand from Wastewater, Drinking Water, and Sludge Systems

Based on end use, the market is segmented into municipal water treatment, industrial water treatment, mining & mineral processing, and others.

Municipal water treatment accounts for the largest global market share, supported by the continued use of continuous polymers in municipal wastewater treatment, sewage treatment plants, drinking water treatment, sludge thickening, sludge dewatering, raw water clarification, and potable water systems. Municipal facilities use polymers to improve solids settling, reduce turbidity, enhance sludge cake dryness, and increase the efficiency of dewatering equipment. Since these chemicals are consumed regularly in plant operations rather than only during capital projects, municipal water treatment remains the most stable and dominant demand base.

Industrial water treatment is a major demand segment for water treatment polymers, covering food and beverage, pulp and paper, chemicals, textiles, metals, power generation, oil and gas, refining, pharmaceuticals, and general manufacturing wastewater. These industries use polymers for suspended solids removal, DAF support, process water clarification, sludge conditioning, color reduction, and discharge compliance. The segment is expected to grow at a 5.9% CAGR during 2026–2034, supported by stricter effluent norms, higher water reuse targets, and the need to stabilize treatment performance across complex and variable industrial wastewater streams.

Mining and mineral processing represent a technically distinct end-use segment as polymer demand is linked to large-volume solid-liquid separation. Water treatment polymers are used in tailings settling, mineral-fines removal, coal washing, ore-processing water, thickening, clarification, and process-water recovery. Anionic polyacrylamide-based flocculants are especially important in this segment due to their ability to accelerate the settling of mineral particles and improve water recycling. The segment is expected to grow at a 6.3% CAGR from 2026 to 2034, supported by tailings management requirements and water conservation in mining operations.

Water Treatment Polymers Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Water Treatment Polymers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 2.42 billion, and is expected to remain the leading regional market due to its large municipal wastewater base, expanding industrial water treatment demand, and strong presence of mining, textile, pulp & paper, chemical, and manufacturing industries. The region is projected to grow at a CAGR of 6.2% during 2026-2034, supported by wastewater infrastructure expansion in China and India, stricter industrial discharge requirements, and rising use of polyacrylamide-based polymers in sludge dewatering, clarification, and process-water recovery applications.

China Water Treatment Polymers Market

China is estimated to generate sales value worth USD 1.33 billion in 2026, representing around 23.4% of global revenues. The country remains the largest national market due to its extensive municipal wastewater network, large industrial manufacturing base, textile and chemical wastewater volumes, and strong domestic polymer production ecosystem. Demand is supported by continuous investment in wastewater treatment upgrades, sludge handling, water reuse, and industrial effluent compliance across major manufacturing provinces.

To know how our report can help streamline your business, Speak to Analyst

India Water Treatment Polymers Market

India is anticipated to reach around USD 0.39 billion in 2026, accounting for nearly 6.9% of global revenues. The market is supported by rapid urban wastewater infrastructure development, expansion of sewage treatment capacity, and stronger enforcement of industrial effluent treatment across textiles, chemicals, food processing, pulp & paper, and pharmaceuticals. The increasing deployment of sludge dewatering systems and packaged effluent treatment plants is also driving higher consumption of flocculants and organic coagulants.

North America

North America reached USD 1.21 billion in 2025, supported by mature municipal wastewater infrastructure, high sludge dewatering intensity, and strong demand from industrial water treatment, food & beverage, oil & gas/refinery, mining, and pulp & paper applications. The regional market is expected to grow at a CAGR of 5.3% during 2026-2034. Growth is volume-led and supported by higher-value polymer formulations used for sludge conditioning, solids separation, wastewater clarification, and water treatment processes in regulated environments.

U.S. Water Treatment Polymers Market

The U.S. market is expected to reach USD 1.12 billion in 2026, accounting for about 19.7% of global revenues. The country remains the main contributor to North American demand due to its large municipal wastewater treatment base, recurring chemical consumption for sludge dewatering, and broad industrial use across refining, food processing, chemicals, power, mining, and manufacturing. Aging water infrastructure upgrades and rising treatment efficiency requirements further support demand.

Europe

Europe reached USD 1.14 billion in 2025, growing at a CAGR of 5.0% from 2026 to 2034. The region represents a mature yet high-value market, where stringent wastewater discharge standards, advanced sludge management practices, and robust municipal and industrial compliance requirements shape demand. Polymer consumption is closely linked to municipal sewage treatment, drinking water clarification, sludge dewatering, pulp & paper wastewater, food processing, chemicals, and specialty industrial applications. Higher adoption of optimized, low-residual polymer solutions also supports value growth.

Germany Water Treatment Polymers Market

Germany is set to account for around USD 0.30 billion in 2026, representing approximately 5.3% of global revenues. Advanced municipal wastewater systems, strong industrial water treatment activity, and demand from chemicals, automotive manufacturing, food processing, pulp & paper, and power-related wastewater applications support the country’s market.

U.K. Water Treatment Polymers Market

The U.K. is expected to reach around USD 0.17 billion in 2026, contributing around 3.0% of global revenues. Demand is mainly driven by municipal wastewater treatment, drinking water clarification, sewage sludge dewatering, and industrial effluent treatment. The country’s mature water utility structure and ongoing need to improve wastewater discharge quality support consistent polymer consumption, especially in sludge conditioning and clarification applications.

Latin America

Latin America stood at USD 0.32 billion in 2025 and is projected to expand at a CAGR of 5.7% during 2026-2034. The regional market is smaller than Asia Pacific, North America, and Europe. Still, demand is supported by municipal wastewater expansion, mining activity, food & beverage processing, pulp & paper operations, and industrial effluent treatment. Polymer usage is particularly relevant in sludge dewatering, mineral processing water, suspended-solids removal, and clarification applications.

Brazil Water Treatment Polymers Market

Brazil is projected to generate sales revenue of USD 0.15 billion in 2026, representing around 2.7% of global revenues. Demand is supported by municipal wastewater treatment, pulp & paper, food processing, mining, and broader industrial water treatment applications. The country’s large population, water infrastructure needs, and industrial wastewater generation make it the leading national market in Latin America.

Middle East & Africa

The Middle East & Africa region reached USD 0.28 billion in 2025, expanding at a CAGR of 6.0% from 2026 to 2034. The region remains smaller in absolute value but is expected to grow steadily due to water scarcity, municipal wastewater development, industrial wastewater treatment, oil & gas/refinery operations, mining, and water reuse initiatives. Demand is concentrated in GCC countries, South Africa, and selected industrial and mining hubs, where polymers are used for clarification, sludge dewatering, oily wastewater treatment, and process-water recovery.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacity Expansion, Acquisitions, and Bio-based Innovations are Identified as Key Strategies to Strengthen Market Competition

The global water treatment polymers market is moderately consolidated, with competition led by multinational water chemical suppliers, specialty polymer producers, and regional flocculant manufacturers. Key players include SNF Group, Kemira, Solenis, Ecolab, and Veolia Water Technologies. Recent developments show that companies are strengthening their positions through capacity expansion, acquisitions, digital water treatment solutions, and renewable polymer innovation. In addition, suppliers are focusing on polyacrylamide-based flocculants, PolyDADMAC, polyamines, sludge dewatering aids, color-removal polymers, and bio-based alternatives for municipal, industrial, and mining & mineral processing water treatment. Product performance, application testing, sludge dewatering expertise, regional supply reliability, and customized formulations remain key competitive differentiators.

LIST OF KEY WATER TREATMENT POLYMER COMPANIES PROFILED

- SNF Group (France)

- Kemira (Finland)

- Solenis (U.S.)

- Veolia Water Technologies (France)

- Ecolab (U.S.)

- Kurita Water Industries (Japan)

- Buckman (U.S.)

- USALCO (U.S.)

- IXOM (Australia)

- Accepta (U.K.)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Dorf-Ketal Chemicals India entered the industrial water treatment sector by acquiring the water treatment business of Vasu Chemicals LLP. The acquisition strengthens Dorf-Ketal’s presence in industrial water treatment and expands its ability to serve customers requiring chemical treatment programs for process water, effluent treatment, and industrial wastewater management.

- November 2025: SNF Flopam India announced an investment of approximately USD 95 million to expand capacity at its Gujarat facility. The expansion covers acrylamide monomer, polyacrylamide powder, liquid polymers, and emulsions, supporting rising demand in water treatment, oil and gas, mining, and industrial applications in India.

- November 2024: Solenis completed the acquisition of BASF’s mining flocculants business. The acquisition expanded Solenis’ product offering for mining and mineral processing customers, including flocculant solutions used in tailings management, mineral fines separation, and process-water recovery.

- September 2024: Kemira and IFF completed a market-entry-scale industrial polymer plant in Finland as part of their strategic cooperation to commercialize renewable alternatives to fossil-based products. The collaboration supports Kemira’s need for renewable polymer solutions across pulp, paper, packaging, and industrial and municipal water treatment applications.

- August 2024: USALCO announced the construction of a new water treatment chemicals production facility in California. The investment supports the company’s geographic expansion and supply reliability for municipal and industrial water treatment customers in the western U.S.

REPORT COVERAGE

The global water treatment polymers market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026 to 2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Product Type, End Use, and Region |

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 5.37 billion in 2025 and is projected to reach USD 8.84 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 2.42 billion.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The municipal water treatment end use segment leads the market.

Stricter industrial effluent regulations and growing demand from industrial sectors are driving market growth.

SNF Group, Kemira, Solenis, Ecolab, and Veolia Water Technologies are among the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Momentum toward bio-based, lower-residual polymer alternatives to drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us