Xanthan Gum Market Size, Share & Industry Analysis, By Grade (Food Grade, Industrial Grade, and Pharmaceutical Grade), By Application (Food & Beverages, Oil & Gas, Pharmaceuticals, Personal Care, Industrial, and Others), and Regional Forecast, 2026-2034

Xanthan Gum Market Overview

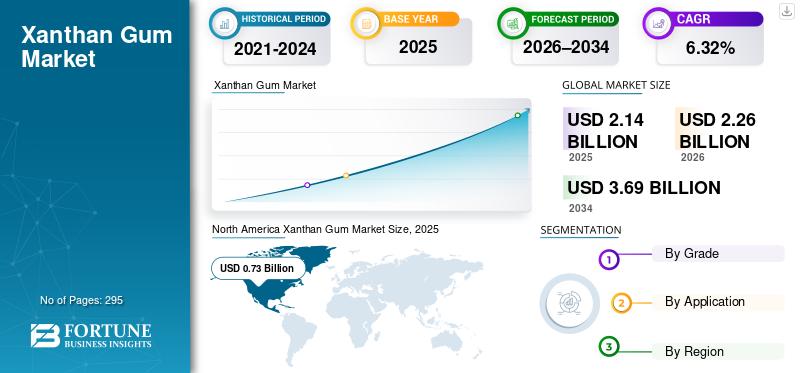

The global xanthan gum market size was valued at USD 2.14 billion in 2025. The market is projected to grow from USD 2.26 billion in 2026 to USD 3.69 billion by 2034, exhibiting a CAGR of 6.32% during the forecast period. North America dominated the xanthan gum market with a market share of 34.11% in 2025.

Xanthan gum is a microbial polysaccharide produced through fermentation of carbohydrates by Xanthomonas campestris. It is widely used as a thickening agent, stabilizing, and suspending agent due to its ability to maintain viscosity under varying temperatures, pH levels, and shear conditions. Its versatility across food, pharmaceuticals, personal care, oil & gas, and industrial applications makes it one of the most commercially important hydrocolloids globally.

The increasing consumption of processed, packaged, and ready-to-eat foods is a primary driver for xanthan gum demand.

Therefore, expanding urban populations and changing dietary habits are structurally increasing food-grade xanthan gum consumption.

Furthermore, many key industry players, including CP Kelco, Archer Daniel Midland, Solvay, and Cargill Incorporated, operating in the market, are focusing on developing innovative products to meet the increasing demand.

Download Free sample to learn more about this report.

Xanthan Gum Market Key Takeaways

- 2025 Market Size: USD 2.14 billion

- 2026 Market Size: USD 2.26 billion

- 2034 Forecast Market Size: USD 3.69 billion

- CAGR: 6.32% from 2026–2034

- North America dominated the xanthan gum market with a 34.11% share in 2025.

- The food grade segment accounted for the largest market share in 2025.

- The pharmaceutical grade segment is projected to register the fastest growth with a CAGR of 7.52% during the forecast period.

Asia Pacific

Asia Pacific is expected to reach USD 0.75 billion in 2026.

North America

North America is projected to remain the largest regional market in 2026 with a valuation of approximately USD 0.77 billion.

Europe

Europe is projected to reach USD 0.59 billion in 2026, growing at a CAGR of 5.84%.

U.S.

The U.S. xanthan gum market is projected to reach approximately USD 0.68 billion by 2026.

Japan

Japan’s xanthan gum market is projected to reach approximately USD 0.06 billion by 2026.

Read More

XANTHAN GUM MARKET TRENDS

Shift Toward Clean-Label and Gluten-Free Products is Latest Trend

The shift toward clean-label and gluten-free food products has emerged as a key trend shaping the global market. Consumers are increasingly seeking food products with simple, recognizable, and natural ingredients, free from artificial additives, preservatives, and allergens. This behavioral shift is driven by heightened awareness of health, food intolerances, and transparency in food labeling.

Xanthan gum, being a fermentation-derived, plant-based hydrocolloid, aligns well with clean-label requirements and is widely accepted by regulatory authorities for food use. Unlike synthetic stabilizers, it offers functional benefits while maintaining label-friendly positioning. As a result, food manufacturers increasingly prefer xanthan gum over chemically modified alternatives in reformulated products.

In gluten-free applications, xanthan gum plays a critical structural role by mimicking the elasticity and binding properties of gluten. It is extensively used in gluten-free bakery products, sauces, dressings, and ready-to-eat meals to improve texture, moisture retention, and shelf stability. The growing prevalence of celiac disease, gluten sensitivity, and lifestyle-driven gluten avoidance is further reinforcing this trend.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growth of Processed and Convenience Foods to Boost Market Growth

The rapid growth of processed and convenience foods is a major factor driving xanthan gum market growth globally. Urbanization, rising disposable incomes, and increasingly busy lifestyles have led consumers to favor ready-to-eat, ready-to-cook, and packaged food products that offer convenience, longer shelf life, and consistent quality. This shift is particularly pronounced in emerging economies across Asia Pacific and Latin America, as well as in mature markets where demand for premium convenience foods continues to rise.

Xanthan gum plays a critical functional role in processed foods formulations by acting as a thickener, stabilizer, and emulsifier. It is widely used in sauces, dressings, bakery products, beverages, frozen foods, and dairy alternatives to enhance texture, viscosity, and mouthfeel, while also preventing ingredient separation during storage and transportation. Its effectiveness at low concentrations makes it cost-efficient for large-scale food processing.

Additionally, the expansion of convenience foods often requires ingredients that perform reliably under temperature fluctuations, mechanical stress, and extended shelf-life conditions. Xanthan gum’s high stability across varying pH levels and temperatures makes it particularly suitable for these applications. Therefore, the sustained growth of processed and convenience foods continues to underpin long-term demand for food-grade xanthan gum.

Expansion of Pharmaceutical and Healthcare Applications to Bolster Market Growth

The expanding use of xanthan gum in pharmaceutical and healthcare applications is an important driver supporting market growth. Xanthan gum is widely used as a suspending agent, binder, and viscosity modifier in oral liquids, topical formulations, and controlled-release drug systems. Its high stability across a wide range of pH levels and temperatures ensures consistent drug dispersion and dosage accuracy, which is critical for pharmaceutical formulations.

Growth in generic drug manufacturing, particularly in Asia Pacific, has increased demand for cost-effective and reliable excipients such as xanthan gum. In addition, the rising preference for liquid and semi-solid dosage forms especially for pediatric and geriatric populations has further strengthened its adoption. Xanthan gum’s biocompatibility and regulatory acceptance across major pharmacopoeias enhance its suitability for healthcare use.

MARKET RESTRAINTS

Cyclical Demand from Oil & Gas Industry to Hamper Market Growth

Cyclical demand from the oil and gas industry represents a key restraint for the market, particularly for industrial-grade applications. Xanthan gum is widely used as a rheology modifier in drilling and completion fluids, where its consumption is directly linked to drilling activity levels. However, oil and gas exploration and production are highly sensitive to crude oil price fluctuations, geopolitical factors, and regulatory policies, resulting in uneven demand patterns.

Periods of low oil prices often lead to reduced drilling activity, project postponements, and lower chemical consumption, causing sudden declines in xanthan gum demand. Conversely, demand spikes during high-price cycles are often short-lived and difficult for producers to plan around. This volatility creates challenges for capacity utilization, inventory management, and long-term investment decisions for xanthan gum manufacturers.

MARKET OPPORTUNITIES

Advancements in Fermentation Technology and Process Optimization May Create Lucrative Opportunities

Advancements in fermentation technology and process optimization are creating a significant growth opportunity for the market by improving production efficiency, cost competitiveness, and product quality. Xanthan gum is produced through microbial fermentation, and continuous improvements in strain selection, nutrient optimization, and process control are enabling higher yields and shorter fermentation cycles. These enhancements allow manufacturers to produce more xanthan gum per unit of raw material, directly reducing production costs.

Process optimization techniques such as automation, real-time monitoring, and improved downstream recovery methods are further enhancing operational efficiency and consistency. Improved purification and drying processes help achieve tighter viscosity and microbial specifications, which is particularly important for food-grade and pharmaceutical-grade applications. As a result, manufacturers can better meet stringent regulatory and customer quality requirements while minimizing batch variability.

In addition, innovations aimed at reducing energy consumption, water usage, and waste generation support sustainability goals and regulatory compliance. These improvements are especially valuable in cost-sensitive and high-volume markets. Therefore, continued investment in fermentation and process technologies enables producers to strengthen margins, expand capacity, and address rising demand for high-quality, bio-based hydrocolloids such as xanthan gum.

MARKET CHALLENGES

Intensifying Price Competition Pose a Critical Challenge to Market Growth

Intensifying price competition has emerged as a major challenge in the global market, primarily driven by large-scale production capacity in Asia Pacific, particularly China. Chinese manufacturers benefit from economies of scale, lower production costs, and integrated access to fermentation feedstocks, enabling them to supply xanthan gum at highly competitive prices in international markets. This export-oriented supply has increased global availability and exerted sustained downward pressure on prices, especially for food-grade and industrial-grade products.

As a result, global buyers often prioritize cost over brand or technical differentiation, leading to commoditization of standard xanthan gum grades. This environment significantly compresses margins for producers outside Asia Pacific, including those in North America and Europe, where higher labor, energy, and compliance costs limit pricing flexibility. Even established manufacturers face challenges in passing on cost increases to customers due to intense supplier competition.

Segmentation Analysis

By Grade

Widespread Use in Processed and Convenience Foods Led to Dominance of Food Grade Segment

Based on grade, the market is segmented into food grade, industrial grade, and pharmaceutical grade.

The food grade segment accounted for the largest xanthan gum market share in 2025 due to its widespread use in processed and convenience foods, Food-grade xanthan gum is extensively used to improve texture, mouthfeel, and shelf stability in food formulations.

The pharmaceutical grade segment is anticipated to grow at the fastest CAGR of 7.52% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Highly Suitable for Dressings, Baked Goods, and Beverages Led to Dominance of Food & Beverages Segment

Based on application, the market is segmented into food & beverages, oil & gas, pharmaceuticals, personal care, industrial, and others.

Among these, the food & beverages segment accounted for the dominant market share in 2025 driven by the extensive use of xanthan gum as a thickening, stabilizing, and emulsifying agent in a wide range of processed and convenience foods. Its ability to maintain viscosity and stability under varying temperature and pH conditions makes it highly suitable for dressings, baked goods, beverages, and dairy alternatives. Additionally, rising demand for clean-label and gluten-free food products has further strengthened the adoption of xanthan gum in food formulations.

Pharmaceuticals segment is the fastest growing segment with a CAGR of 6.1% over the forecast period driven by its increasing use as a suspending agent, binder, and controlled-release excipient in oral and topical drug formulations. Rising demand for liquid and semi-solid dosage forms, particularly for pediatric and geriatric populations, has significantly increased the adoption of pharmaceutical-grade xanthan gum. In addition, the rapid expansion of generic drug manufacturing, especially in Asia Pacific, has boosted demand for cost-effective, high-performance excipients.

Xanthan Gum Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Xanthan Gum Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is expected to hold a largest share in 2026, valued at around USD 0.77 billion, driven by steady demand from food & beverages and oil & gas applications. The U.S. accounts for the majority of regional consumption due to high usage in clean-label food products, gluten-free formulations, and drilling fluids.

U.S. Xanthan Gum Market

The U.S. market can be analytically approximated at around USD 0.68 billion in 2026. The U.S. accounts for the dominant share of the North American market, reflecting the country’s strong consumption base across key end-use industries. The growth is driven by high demand from the various end-use sectors. In the food and beverage industry, widespread use of xanthan gum in clean-label, gluten-free, and processed food products continues to support large-volume consumption. Additionally, the presence of a well-established pharmaceutical manufacturing ecosystem has increased demand for high-purity pharmaceutical-grade xanthan gum.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

Asia Pacific market is estimated to reach USD 0.75 billion in 2026 and secure its position as the second largest region in the market. This growth is primarily supported by strong demand from the food & beverages and pharmaceutical sectors, driven by rapid urbanization, changing dietary patterns, and rising consumption of processed and convenience foods across China, India, and Southeast Asia.

Japan Xanthan Gum Market

The Japan market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 2.9% of global revenues. The country’s well-developed food processing industry emphasizes quality, safety, and clean-label compliance, driving market growth.

China Xanthan Gum Market

China’s market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.40 billion, representing roughly 17.9% of global sales. The growth is driven by its extensive production capacity and strong domestic consumption. The country hosts several large-scale xanthan gum manufacturers that benefit from cost-competitive fermentation processes, integrated raw material availability, and export-oriented supply chains.

India Xanthan Gum Market

The India market in 2026 is estimated at around USD 0.13 billion, accounting for roughly 5.9% of global revenues. India represents a high-growth but still developing market, driven primarily by pharmaceuticals expansion.

Europe

Europe is projected to grow at 5.84% over the coming years and reach a valuation of USD 0.59 billion by 2026. The primary growth driver for the xanthan gum market in Europe is the strong and expanding demand for clean-label, plant-based, and specialty food products. European consumers increasingly prefer food formulations with natural, recognizable ingredients and minimal chemical modification, encouraging manufacturers to adopt fermentation-derived hydrocolloids such as xanthan gum

U.K Xanthan Gum Market

The U.K. market in 2026 is estimated at around USD 0.08 billion, representing roughly 3.8% of global revenues.

Germany Xanthan Gum Market

Germany’s market is projected to reach approximately USD 0.12 billion in 2026, equivalent to around 5.1% of global sales.

Latin America and Middle East & Africa

Latin America represents a steadily growing market for xanthan gum, primarily driven by expanding food and beverage processing industries in Brazil and Mexico. Rising urbanization and increasing consumption of packaged and convenience foods have supported demand for food-grade xanthan gum. The Latin America market is set to reach a valuation of USD 0.09 billion in 2026.

The Middle East & Africa market is largely influenced by oil and gas drilling activities, especially in GCC countries such as Saudi Arabia and the UAE, where xanthan gum is used in drilling and completion fluids. The Middle East & Africa reached a valuation of USD 0.04 billion in 2025.

GCC Xanthan Gum Market

The GCC market is projected to reach around USD 0.02 billion in 2026, representing roughly 0.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Innovations by Key Players to Propel Market Progress

The global market is moderately consolidated, characterized by the presence of a few large multinational ingredient suppliers alongside a wide base of cost-competitive regional manufacturers, particularly in Asia Pacific. Competition is primarily driven by price, product quality, regulatory compliance, and application expertise, rather than product differentiation. CP Kelco, Archer Daniel Midland, Solvay, and Cargill Incorporated are the largest players in the market.

Other notable market players include IFF, Fufeng Group Company Limited, Deosen Biochemical Ltd., Meihua Holdings Group Co., Ltd., Hebei Xinhe Biochemical Co., Ltd. and Jungbunzlauer Suisse AG.

LIST OF KEY XANTHAN GUM COMPANIES PROFILED IN REPORT

- CP Kelco (U.S.)

- Tate & Lyle (U.S.)

- IFF (U.S.)

- Fufeng Group Company Limited (China)

- Deosen Biochemical Ltd. (China)

- Meihua Holdings Group Co., Ltd. (China)

- Hebei Xinhe Biochemical Co., Ltd. (China)

- Jungbunzlauer Suisse AG (Switzerland)

- Archer Daniels Midland – ADM (U.S.)

- Cargill, Incorporated (U.S.)

- Solvay SA (Belgium)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Tate & Lyle and CP Kelco completed the acquisition, forming a leading global specialty food and beverage solutions business with an expanded portfolio of functional ingredients. The combination brings together Tate & Lyle’s expertise in food systems, sweeteners, and texturants with CP Kelco’s strong capabilities in fermentation-derived ingredients, including xanthan gum, pectin, and cellulose-based solutions. This integration strengthens the company’s ability to offer end-to-end formulation support to food and beverage manufacturers.

- October 2024: Jungbunzlauer commenced construction of a USD 150 million facility, which is expected to become Canada’s first production site for xanthan, a fermentation-derived gum used in food, cosmetic, and pharmaceutical applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.32% from 2026 to 2034 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Grade, Application, and Region |

| By Grade |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.14 billion in 2025 and is projected to reach USD 3.69 billion by 2034.

In 2025, the market value in the North America stood at USD 0.73 billion.

The market is expected to grow at a CAGR of 6.32% over the forecast period of 2026-2034.

By grade, the food grade segment is expected to lead the market.

The growing demand from the pharmaceuticals industry is expected to be the key driver of the market.

CP Kelco, Archer Daniel Midland, Solvay, and Cargill Incorporated are the major players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 295

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us