AI in Precision Medicine Market Size, Share & Industry Analysis, By Component (Hardware/Devices and Software & Services), By Deployment (Cloud-Based, On Premise & Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing, & Others), By Indication (Oncology, Rare Diseases, Cardio-metabolic, Neurology, Immunology/Autoimmune, Infectious Diseases & Others), By Application (Clinical Variant Interpretation & Reporting, Therapy Selection/Clinical Decision Support, Clinical Trial Matching & Patient Stratification, & Others), By End User, and Regional Forecast, 2026-2034

AI in Precision Medicine Market Size and Future Outlook

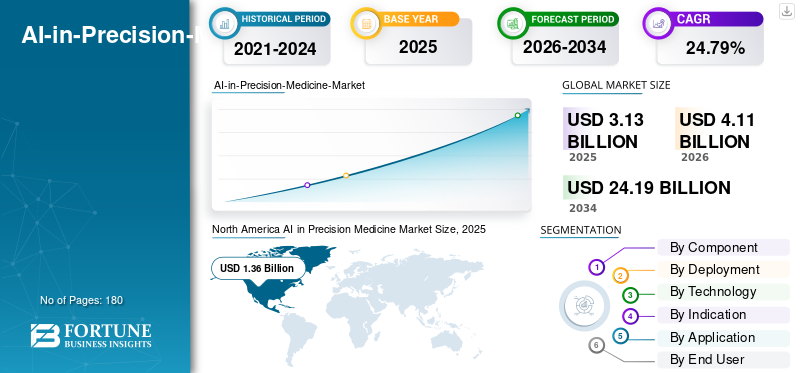

The global AI in precision medicine market size was valued at USD 3.13 billion in 2025. The market is projected to grow from USD 4.11 billion in 2026 to USD 24.19 billion by 2034, exhibiting a CAGR of 24.79% during the forecast period. North America dominated the AI in precision medicine market with a market share of 43.45% in 2025.

The global AI in precision medicine market is poised for significant growth over the upcoming years. The market focuses on AI software and services that help healthcare providers, diagnostic labs, and life-science companies use patient data, such as genetic and biomarker results, to make more personalized care decisions. With the rising adoption of precision medicine and patients' shift toward targeted therapies, the market is poised for significant growth. Precision medicine is moving from specialist centers to broader clinical use, increasing the volume of complex test results that must be interpreted quickly and consistently. AI helps convert this health data into practical insights by supporting faster patient identification for testing, clearer interpretation of results, and better matching of patients to the most suitable therapy or clinical trial. As a result, organizations are increasingly adopting AI to reduce delays and improve patient care.

- For instance, in November 2025, Complete Genomics collaborated with SOPHiA GENETICS to launch and co-market MSK-ACCESS and MSK-IMPACT, powered by SOPHiA DDM, on Complete Genomics' DNBSEQ-T1+ sequencing platform. The development aimed to integrate genomic sequencing and AI analytics to accelerate the adoption of precision medicine. Such developments are anticipated to boost the overall market growth.

Furthermore, leading market players, such as Tempus AI, Inc., Foundation Medicine, Inc., Guardant Health, Inc., and Caris Life Sciences, Inc., are directing their resources toward technological advancements and new product launches to strengthen their market positions.

Download Free sample to learn more about this report.

AI in Precision Medicine Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.13 billion

- 2026 Market Size: USD 4.11 billion

- 2034 Forecast Market Size: USD 24.19 billion

- CAGR: 24.79% from 2026–2034

- North America dominated the AI in precision medicine market with a 43.45% share in 2025.

- The hardware/devices segment is expected to witness significant growth during the forecast period.

- The rare diseases segment is projected to register strong growth throughout the forecast period.

North America

North America maintained its leading position in 2025 and is estimated to reach USD 1.36 billion in 2026.

Europe

Europe is projected to reach USD 1.12 billion by 2026, supported by strong market expansion across the region.

Asia Pacific

Asia Pacific is estimated to reach USD 0.85 billion in 2026, making it the third-largest regional market.

U.S.

U.S. The market is estimated to reach USD 1.64 billion in 2026, accounting for approximately 36.94% of the global market.

Japan

Japan The market is estimated at USD 0.15 billion in 2026, representing approximately 3.70% of the global market.

Read More

AI IN PRECISION MEDICINE MARKET TRENDS

Growing Partnerships Between AI Platforms and Pharma/Biotechnology Companies is a Key Market Trend

A prominent market trend is the growing number of partnerships between AI platform companies and life-science/diagnostics leaders, as no single player can scale precision medicine with a single type of data. As testing expands across diseases, providers and pharma need solutions that reliably connect molecular profiling, clinical records, and outcomes evidence, and partnerships help combine these strengths faster than building everything in-house. These collaborations also reduce adoption friction as joint offerings can improve data access, standardize evidence generation, and create clearer pathways for clinical use at multiple sites. As a result, partnerships are becoming a practical route to scale precision medicine programs, expand use cases beyond pilots, and demonstrate real-world value more quickly, supporting broader, faster market growth.

- For instance, in April 2025, Illumina, Inc. collaborated with Tempus AI, Inc. to accelerate the clinical adoption of precision medicine by generating insights on the clinical benefits of molecular profiling across major disease categories. Such developments are expected to boost market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Cardiovascular Disease Burden and Aging Population Are Driving Market Growth

A significant market driver is the growing adoption of biomarker-driven and targeted therapies, increasing the volume and complexity of molecular testing. As more therapies require specific biomarkers, health systems and laboratories dealing with larger NGS panels generate more fragmented data. Traditional workflows such as manual chart review, disconnected lab reports, and back-and-forth interpretation can delay testing, create variability in results interpretation, and ultimately slow therapy selection. These factors are pushing providers and life-science partners to use AI-enabled precision medicine platforms to automate workflows and translate complex results into actionable insights. As a result, AI improves turnaround time, reduces missed testing opportunities, and supports faster patient matching to targeted therapy, making precision care easier to scale across sites.

Key companies are focusing on new product launches with innovative AI features integrated into their offering to capitalize on the AI in precision medicine market growth.

- For instance, in June 2024, Tempus collaborated with AstraZeneca to use Tempus Next to support guideline-directed biomarker testing in NSCLC, including using AI to scan clinical data and help identify patients who may be eligible for testing, supporting timely targeted treatment decisions. Such factors highlight the expected drivers of market growth.

MARKET RESTRAINTS

High Implementation and Ongoing Model Maintenance Costs Limits Market Growth

A key restraint for the market is the high cost of implementation and ongoing model maintenance, making it difficult for many hospitals and payers to scale. Precision medicine AI typically needs deep integration with EHRs, lab/NGS systems, imaging repositories, and data governance workflows. These integration projects require significant upfront IT and informatics effort. Once deployed, these models must be monitored continuously and updated. This creates recurring costs for revalidation, cybersecurity, and workflow redesign, which can be hard to justify when budgets are already tight. As a result, adoption can remain limited to large centers with stronger data and healthcare infrastructure, slowing broad-market penetration and delaying ROI realization across routine care settings.

- For instance, in November 2025, Health Informatics published an article titled 'Barriers and Solutions to Efficient Health Care AI Implementation'. The article reported that stakeholders must understand how models will be maintained to combat model drift, framing this challenge against a backdrop of funding cuts and increasing demand for individualized care. This highlights why ongoing maintenance can become a practical barrier to adopting new technologies.

MARKET OPPORTUNITIES

Supporting Rare Disease Diagnosis with Faster Data Review to Offer Lucrative Growth Opportunities

A significant market opportunity is to enable faster data review for rare disease diagnosis. Rare disease patients often face long diagnostic journeys where specialists must manually review complex genetic data and connect it to symptoms. As more hospitals expand genetic testing, the number of variants to evaluate increases sharply, and manual interpretation can create backlogs, inconsistent conclusions, and delayed treatment decisions. This pushes healthcare providers to adopt AI tools that quickly screen large volumes of genetic information, highlight the most likely disease-causing signals, and help clinicians focus their time on the highest-value findings. These applications of AI shorten diagnostic timelines, reduce repeat testing and referrals, making rare disease programs easier to scale.

- For instance, in May 2025, Illumina, Inc., in collaboration with PromoterAI, designed an AI algorithm to help identify disease-causing regulatory variants in noncoding promoter regions, aiming to accelerate insights that support rare disease diagnosis. Such developments offer market growth opportunities.

MARKET CHALLENGES

Limited Interoperability Across EHR, Lab, and Omics Data Systems to Pose a Significant Challenge for Market Growth

A major market challenge is limited interoperability across EHR, lab, and omics systems. Precision medicine decisions depend on bringing multiple data sources together at the right time in the clinical workflow. When genomic results, pathology findings, and clinical history sit in separate systems with different formats and identifiers, teams spend more time on manual data collection and reconciliation. This increases delays, creates gaps in patient identification for testing, and makes it harder to apply consistent rules for treatment selection across hospitals. As a result, AI tools may perform well in isolated pilots but struggle to scale across sites, as the data pipes and workflows needed to feed the models are not consistently in place. These factors collectively slow broader adoption.

- For instance, in June 2024, a JMIR Bioinformatics paper on integrating electronic health records and genomic data explains that genomic data is fundamentally different from routine clinical data and requires special considerations for use in digital health settings. These factors highlight that EHR-genomics integration and interoperability remain practical barriers to the deployment of precision medicine.

Segmentation Analysis

By Component

Rising Need for AI-Driven Data Integration and Analysis Drives Software & Services Segment Growth

Based on the component, the market is categorized into hardware/devices and software & services.

Among these, the software & services segment accounted for the largest AI in precision medicine market share. The segment’s growth is driven by the shift toward AI-enabled platforms capable of managing rapidly expanding complex patient and molecular datasets. As genomics, biomarker tests, imaging, and clinical records increase in volume, traditional workflows are being replaced. As teams rise, the risk of delays and inconsistent interpretation increases. Software platforms and associated services solve this by creating a more standardized workspace where data can be integrated, analyzed, and converted into actionable outputs such as reports, therapy options, and trial matches. This reduces turnaround time, improves repeatability across sites, and makes precision medicine programs easier to scale, so the global market demand is concentrated more on software and services.

Additionally, new product launches by key companies to digitalize manufacturing workflows are driving the segment growth.

- For instance, in September 2024, SOPHiA GENETICS launched a new generation of the Sophia DDM Platform, designed to compute large amounts of data at scale and provide integrated access to multimodal analytics modules. Such developments are supporting broader adoption of precision medicine, driving the segment's growth.

The hardware/devices segment is expected to grow at a CAGR of 25.20% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Strategic Partnership and Innovative Product Launches in Cloud-Based Platforms to Drive the Segmental Growth

Based on deployment, the market is segmented into cloud-based, on-premise, and hybrid.

Among these, the cloud-based segment accounted for the largest market share. A factor supporting the segment’s growth is that precision medicine programs generate large volumes of patient and molecular data that must be shared across hospitals, labs, and research teams in near real time. When data stays on local servers, teams often face slower access, limited collaboration, and higher IT overhead for upgrades and security. Cloud deployment overcomes these challenges and makes it easier to connect datasets, run advanced analysis at scale, and roll out updates quickly across multiple sites. These advantages reduce turnaround time, improve consistency of insights, and support faster expansion of precision medicine programs. Highlighting these factors, key companies are shifting toward cloud-based models to enhance scalability and focusing on strategic collaboration and product launches in the segment.

- For instance, in October 2025, Foundation Medicine partnered with Manifold to bring enhanced AI capabilities to FoundationInsights, a cloud-based data analytics and visualization platform.

In addition, the hybrid segment is projected to grow at a CAGR of 22.39% over the forecast period.

By Technology

Advancements in Supporting AI Technologies Enabling Scalable Healthcare Deployment Drives Others’ Segment Growth

Based on the technology, the market is segmented into machine learning & deep learning, natural language processing, and others.

In 2025, the others segment dominated the market in terms of technology. The segment comprises innovative technologies such as computer vision, statistics and probabilistic models, scheduling, and analytics, among others. Precision medicine requires a range of supporting technologies that make data usable and deployable across real healthcare settings. Hospitals and national programs are focusing on tools such as data integration layers, secure infrastructure, workflow automation, and large-scale analytics. These AI enabled technologies work reliably across many locations. When these supporting technologies improve, AI solutions become easier to implement, safer to run, and faster to scale. Such factors drive the segment's growth.

- For instance, in May 2025, Oracle, Cleveland Clinic, and G42 announced a partnership to launch an AI-based healthcare delivery platform focused on secure, scalable data integration and clinical AI applications.

The natural language processing segment is projected to grow at a CAGR of 26.85% during the forecast period.

By Indication

Growing Prevalence of Oncology to Fuel Demand and Support Segmental Growth

Based on the indication, the market is segmented into oncology, rare diseases, cardio-metabolic, neurology, immunology/autoimmune, infectious diseases, and others.

In 2025, the oncology segment dominated the market. The segment's largest share is driven by its increasing prevalence and incidence. Cancer care increasingly depends on biomarker testing and fast treatment decisions. Cancer pathways often require combining pathology, genomics, imaging, and clinical history, which makes manual interpretation slow and inconsistent across sites. AI helps organize complex evidence, support tumor board decisions, and improve patient matching to targeted therapies and trials. As a result, oncology becomes the first and largest area for value creation and investment potential. Highlighting these factors, key companies are participating in strategic collaborations for research and development.

- For instance, in January 2026, OncoLens, in collaboration with The Jackson Laboratory, launched a program to expand Molecular Tumor Boards in community oncology centers to improve treatment recommendations and clinical trial access, using digital workflows and genomic expertise.

The rare diseases segment is projected to grow at a CAGR of 26.57% during the forecast period.

By Application

Wide Utilization of Clinical Variant Interpretation & Reporting to Fuel Segmental Growth

Based on the application, the market is segmented into clinical variant interpretation & reporting, therapy selection/clinical decision support, clinical trial matching & patient stratification, biomarker discovery & target identification, companion diagnostics, real-world evidence & outcomes analytics, and others.

In 2025, the clinical variant interpretation & reporting segment dominated the market. The growth is attributed to clinical variant interpretation & reporting, which is the most frequent and repeatable step in the precision medicine workflow. AI-supported interpretation and standardized reporting reduce repetitive effort, improve consistency, and speed up turnaround time for clinicians. As a result, this application experiences the strongest routine demand and has become a widely adopted use case. Underscoring these varied advantages, key companies are directing their resources toward strategic collaborations and new product launches to capitalize on the segment's growth potential.

- For instance, in November 2025, QIAGEN highlighted enhancements to QCI Interpret to streamline variant interpretation and improve clinical reporting workflows.

The companion diagnostics is projected to grow at a CAGR of 25.47% during the forecast period.

By End User

Revenue Generation Potential for Healthcare Providers to Drive the Segment Growth

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, healthcare providers, CROS & CDMOS, diagnostic laboratories, and others.

By end user, the healthcare providers dominated the market as they are the point where critical precision medicine decisions are made. Also, these settings demonstrate the greatest impact on treatment choice, pathway adherence, and patient outcomes. As providers expand genomics and biomarker testing, they need tools that help clinicians interpret results faster and apply them consistently, without adding more specialist burden. AI platforms support this by turning complex data into clearer recommendations and reports that fit clinical workflows. As a result, hospitals and health systems become the largest adopters as they try to scale precision medicine beyond a few expert teams. Recognizing the critical applications, the market is witnessing strategic collaborations between AI solution providers and healthcare providers to increase the adoption of these tools.

- For instance, in November 2025, Tempus AI, Inc. announced it will acquire Intelerad to expand cloud-enabled enterprise imaging and workflow solutions across care settings, demonstrating how major vendors are investing to scale AI and cloud-driven imaging informatics.

The pharma & biotech companies segment is projected to grow at a CAGR of 24.41% over the forecast period.

AI in Precision Medicine Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Precision Medicine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 1.03 billion, and maintained its leading position in 2025 with a valuation of USD 1.36 billion. The market in North America is expected to grow significantly over the forecast period, as the region faces a volume of precision medicine clinical trials, rising research and development, and complex results, pushing hospitals to adopt AI to interpret and act faster.

U.S. AI in Precision Medicine Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 1.64 billion in 2026, accounting for roughly 36.94% of the global market.

Europe

Europe is projected to grow at 24.61% over the coming years, the second-highest among all regions, and reach a valuation of USD 1.12 billion by 2026. The region is expected to experience robust growth driven by expanding public health systems and genomic and cancer programs.

U.K. AI in Precision Medicine Market

The U.K. market in 2026 is estimated at around USD 0.23 billion, representing roughly 5.30% of the global market.

Germany AI in Precision Medicine Market

Germany's market is projected to reach approximately USD 0.27 billion in 2026, equivalent to around 6.11% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.85 billion in 2026 and secure the position of the third-largest region in the market. The region's growth is driven by rapid growth in cancer burden, rising middle-class healthcare spending, and expanding hospital networks, which are increasing demand for targeted therapies and biomarker testing.

Japan AI in Precision Medicine Market

The Japanese market in 2026 is estimated at around USD 0.15 billion, accounting for approximately 3.70% of the global market.

China AI in Precision Medicine Market

China's market is projected to be among the largest worldwide, with 2026 revenues estimated at around USD 0.30 billion, representing approximately 7.32% of global sales.

India AI in Precision Medicine Market

The Indian market is estimated at around USD 0.11 billion in 2026, accounting for roughly 2.71% of global revenue.

Latin America and the Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.23 billion in 2026. The region is experiencing market growth driven by private hospital groups, and leading cancer centers are scaling advanced diagnostics. In the Middle East & Africa, the GCC is set to reach USD 0.07 billion in 2026.

South Africa AI in Precision Medicine Market

The South African market is projected to reach approximately USD 0.02 billion by 2026, accounting for roughly 0.38% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Progress

The global AI in precision medicine market is highly consolidated, with companies such as Tempus AI, Inc., Foundation Medicine, Inc., Guardant Health, Inc., and Caris Life Sciences, Inc. holding a considerable market share. Strategic partnerships, new product launches, technological advancements, and increased investments and strategic acquisitions in the sector drive these companies' market share gains.

- For instance, in May 2025, Illumina unveiled PromoterAI, an AI algorithm designed to help identify disease-causing regulatory variants in noncoding regions, supporting faster insights that can improve rare disease diagnosis by early detection and precision care decisions. Such developments are aimed at driving market growth.

Other notable players in the global market include SOPHiA GENETICS SA, Illumina, Inc., and QIAGEN GmbH. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their position during the forecast period.

LIST OF KEY AI IN PRECISION MEDICINE COMPANIES PROFILED

- Tempus AI, Inc. (U.S.)

- Foundation Medicine, Inc. (U.S.)

- Guardant Health, Inc. (U.S.)

- Caris Life Sciences, Inc. (U.S.)

- SOPHiA GENETICS SA (Switzerland)

- QIAGEN GmbH (Germany)

- Illumina, Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- PathAI, Inc. (U.S.)

- Fabric Genomics, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENT

- April 2025: Tempus announced multi-year strategic agreements with AstraZeneca and Pathos AI to develop a large multimodal foundation model in oncology, aimed at generating deeper clinical and biological insights to support precision therapy development and use.

- April 2025: Illumina and Tempus announced a collaboration to drive genomic AI innovation and generate evidence on the clinical benefits of molecular profiling, supporting broader clinical adoption of precision testing across major disease areas.

- June 2024: Tempus announced an expanded collaboration with AstraZeneca to use Tempus Next to support guideline-directed biomarker testing in NSCLC, helping clinicians identify the right patients for testing faster and apply updated guidelines more consistently.

- September 2023: QIAGEN announced it extended the AI capabilities of QCI Interpret by adding AI-enhanced coverage of thousands of rare-disease genes, strengthening clinical interpretation and reporting workflows that are central to precision medicine.

- June 2023: Caris Life Sciences and ConcertAI expanded their partnership to create a prospectively matched clinico-genomic research platform that combines molecular profiling with clinical data to support AI-driven precision oncology research and development.

- January 2023: Guardant Health introduced Guardant Galaxy, a suite of advanced AI analytics intended to enhance the performance and clinical utility of its cancer testing portfolio and to accelerate biomarker and drug discovery.

REPORT COVERAGE

The global AI in precision medicine market analysis includes a comprehensive study of market size and forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers, and acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 24.79% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Indication, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Indication |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.13 billion in 2025 and is projected to reach USD 24.19 billion by 2034.

In 2025, the North American market value stood at USD 1.36 billion.

The market is expected to grow at a CAGR of 24.79% over the forecast period.

By component, the software & services segment led the market.

The increasing adoption of precision medicine is the key factor driving the market.

Tempus AI, Inc., Foundation Medicine, Inc., Guardant Health, Inc., and Caris Life Sciences, Inc. are the major players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us