Automated Machine Tending Systems Market Size, Share & Industry Analysis, By System Type (Industrial Robots, Collaborative Robots, Vision-Guided Systems, and Others), By Function (Loading & Unloading, Material Handling, Inspection & Quality Control, and Others), By End User (Automotive, Aerospace & Defense, Electronics & Semiconductors, Metal & Machinery, Medical Devices, and Others), and Regional Forecast, 2026-2034

Automated Machine Tending Systems Market Size and Future Outlook

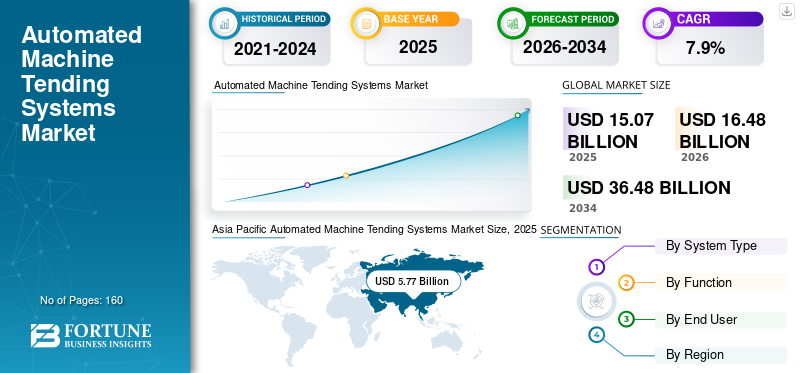

The global automated machine tending systems market size was valued at USD 15.07 billion in 2025. The market is projected to grow from USD 16.48 billion in 2026 to USD 36.48 billion by 2034, exhibiting a CAGR of 10.4% during the forecast period. Asia Pacific dominated the automated machine tending systems market with a market share of 38.29% in 2025.

The market is witnessing steady expansion as manufacturers increasingly deploy automation solutions to address labor shortages and enhance operational efficiency. These solutions integrate industrial robots, vision technologies, and system integration services to automate repetitive machine loading, unloading, and handling tasks across manufacturing environments.

Adoption is further supported by advancements in artificial intelligence, which enable greater flexibility and adaptability in handling variable parts and production workflows. Increasing demand for automation, particularly in automotive electronics and precision manufacturing, is driving investments in complete machine tending solutions that reduce labor dependency and improve machine utilization rates. Over the long term, continued focus on productivity, consistency, and scalable automation is expected to sustain market growth.

Key players such as ABB, FANUC, KUKA, Universal Robots, and Yaskawa Electric are expanding their portfolios with application-focused machine tending cells and software-enabled platforms to support faster deployment and wider adoption across industrial sectors.

Download Free sample to learn more about this report.

AUTOMATED MACHINE TENDING SYSTEMS MARKET TRENDS

Rapid Shift toward Turnkey and Modular Machine Tending Solutions is a Prominent Market Trend

The market is increasingly moving from custom-engineered projects toward turnkey, modular cells that reduce deployment time and integration risk for manufacturers. This transition is supported by the growing availability of pre-engineered machine tending packages that combine robot hardware, safety systems, end-of-arm tooling interfaces, and simplified programming workflows into integrated solutions. Adoption is further supported by the broader scaling of industrial robotics globally.

- The International Federation of Robotics reported that more than 4.28 million robots were operating in factories worldwide, and 70% of new robot deployments in 2023 were installed in Asia. This scale of automation deployment directly supports demand for machine tending solutions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Need to Improve Machine Utilization are Accelerating Market Growth

A key driver for the market is the need to improve machine utilization while reducing reliance on manual, repetitive tending tasks. Manufacturers continue to prioritize automation solutions that increase spindle uptime, reduce changeover losses, and enable longer operating hours with consistent throughput. This is particularly relevant in CNC machining, metalworking, and high-volume component manufacturing, where loading and unloading activities often become the main production bottleneck. In addition, the global expansion of industrial robot deployments continues to support growth in machine tending systems as a high-ROI automation application.

- For example, Okuma America launched its Okuma Robot Loader (ORL) series to automate loading and unloading workpieces on CNC equipment, targeting productivity and operator efficiency improvements.

MARKET RESTRAINTS

High Cost of Product and Integration Complexity Can Restrict Market Expansion

While demand is expanding, adoption can be constrained by the total installed cost of a machine tending system. This cost typically includes the robot, grippers, safety guarding, sensors, feeders, conveyors, control integration, commissioning, and workforce training. Many manufacturers, especially small and mid-sized machine shops, face challenges related to capital budgeting, application engineering capability, and the operational disruption associated with integrating automation into active production environments. During softer macro cycles, companies may also delay automation investments due to higher financing costs and increased ROI scrutiny.

- Industry data indicates that robot orders in North America fell sharply in 2023 as manufacturers faced weaker production volumes and higher interest rates, reflecting how cyclicality can affect automation investment timing.

MARKET OPPORTUNITIES

Expansion of Vision-Guided and Software-Enabled Machine Tending Systems Creates Long-Term Growth Opportunities

A major market opportunity lies in the rising adoption of vision-guided machine tending systems and advanced software layers that enable faster setup, adaptive part handling, and improved cell performance monitoring. Vision guidance addresses variability in part positioning and reduces reliance on fixed fixturing, expanding the feasibility of machine tending in high-mix production. In parallel, cloud-connected design and deployment platforms are enabling manufacturers to configure automation cells faster and standardize deployment across multiple sites.

- For instance, in February 2024, Vention partnered with Flexxbotics to combine modular automation hardware and cloud tools with machine tending software and professional services aimed at accelerating deployment and supporting lights-out operations.

Segmentation Analysis

By System Type

Industrial Robots Hold the Largest Share Supported by Strong Suitability For High-Duty Cycle Applications

Based on system type, the market is divided into industrial robots, collaborative robots, vision-guided systems, and others.

In 2025, the industrial robots segment accounted for the highest market share due to its strong suitability for high-duty cycle applications such as CNC machining, metal cutting, and repetitive loading and unloading operations. Industrial robot-based tending systems are preferred where manufacturers need higher payloads, faster cycle times, and robust repeatability over continuous shifts.

Industrial robot ecosystems also offer mature safety integration and broad compatibility with feeders, pallet systems, and multi-machine cells, which increases adoption in automotive component manufacturing and metalworking.

- For example, Okuma’s ORL automation line is built around industrial robotics to load and unload workpieces for CNC machines, reflecting the continued dominance of industrial robot-based tending in production environments.

The vision-guided systems segment is anticipated to rise with a CAGR of 11.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Function

Loading and Unloading Segment Accounted for the Highest Share due to its Ability to Reduce Operator Idle Time

Based on function, the market is segmented into loading & unloading, material handling, inspection & quality control, and others.

In 2025, loading and unloading held the highest share, as it represents the most direct and widely applicable method for increasing machine utilization and reducing operator idle time. For many manufacturers transitioning toward lights-out machining, loading and unloading automation is typically the first step due to its measurable and immediate productivity gains. Loading and unloading systems are also commonly packaged as standardized cells, making them easier to deploy compared to complex in-line material handling or full inspection automation.

- For example, ABB’s OmniVance machine tending cell is specifically designed to simplify repetitive machine tending tasks, supporting fast adoption of loading and unloading-focused solutions.

The inspection & quality control segment is expected to grow at a CAGR of 11.1% over the forecast period.

By End User

Automotive Leads Demand Due to High Automation Intensity Across Powertrains

Based on end user, the market is segmented into automotive, aerospace & defense, electronics & semiconductors, metal & machinery, medical devices, and others.

In 2025, automotive accounted for the highest automated machine tending systems market share due to high automation intensity across powertrain, chassis, braking, and structural component manufacturing, where CNC machining and repetitive handling are common. Automotive suppliers prioritize consistent cycle time, predictable quality, and utilization gains, which align strongly with machine tending system ROI. The segment also benefits from broader robotics systems adoption trends, particularly in high-volume manufacturing regions.

- IFR data shows large-scale industrial robot deployment globally, with Asia accounting for the majority of new installations, supporting the manufacturing base that includes major automotive production and supplier ecosystems.

The electronics & semiconductors segment is expected to grow at a CAGR of 11.4% over the forecast period.

Automated Machine Tending Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Automated Machine Tending Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market is expected to reach USD 4.23 billion in 2026. The market in this region is driven by advanced manufacturing practices, reshoring initiatives, and rising demand for enhancing productivity. Manufacturers across the region are investing in flexible automation solutions to enhance operational efficiency and reduce workforce dependency.

U.S Automated Machine Tending Systems Market

The U.S. market in 2026 is expected to reach USD 3.59 billion, supported by demand from automotive suppliers, aerospace machining, and general metalworking. Increasing availability of packaged machine tending solutions from OEMs and integrators continues to improve adoption among mid-sized manufacturers.

Europe

Europe market is expected to reach valuation of USD 4.65 billion in 2026, supported by a strong industrial base and early adoption of advanced automation technologies. Countries such as Germany, Italy, and France continue to invest in robotic automation to improve efficiency and maintain competitiveness in manufacturing operations.

U.K Automated Machine Tending Systems Market

The U.K. market in 2026 is projected to reach USD 0.73 billion, representing roughly 4.4% of global revenues.

Germany Automated Machine Tending Systems Market

Germany’s market is projected to reach USD 1.16 billion in 2026, equivalent to around 7.1% of global sales.

Asia Pacific

Asia Pacific held a dominant position in the market in 2024 and continued to maintain its leading position in 2025, with a market valuation of USD 5.77 billion. The region’s dominance is supported by extensive manufacturing activity, rapid industrial automation, and strong investments in automotive, electronics, and metalworking industries. IFR reported that 70% of newly deployed robots in 2023 were installed in Asia, supporting strong demand for machine tending systems as a core automation application for machining and production lines.

Japan Automated Machine Tending Systems Market

The Japan market in 2026 is projected to reach USD 1.34 billion, accounting for roughly 8.1% of global revenue.

China Automated Machine Tending Systems Market

The China market in 2026 is projected to reach USD 2.20 billion, accounting for roughly 13.3% of global revenue.

India Automated Machine Tending Systems Market

The Indian market in 2026 is projected to reach USD 0.66 billion, accounting for roughly 4.0% of the global market.

South America and the Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate automated machine tending systems market growth during the forecast period. South America is projected to reach a market valuation of USD 0.59 billion in 2026. Growth in the region is supported by gradual industrial automation, particularly in the automotive and metal processing industries. The Middle East & Africa market is expected to reach a valuation of USD 0.67 billion in 2026. Increasing investments in industrial diversification, manufacturing infrastructure, and automation initiatives are supporting the adoption of the product across selected markets.

GCC Automated Machine Tending Systems Market

The GCC market is projected to reach around USD 0.28 billion in 2026, representing roughly 1.7% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Turnkey Automation Cells to Strengthen Their Market Positions

The automated machine tending systems market is moderately consolidated at the robot OEM level and fragmented at the system integration layer. Competition is driven by manufacturers focusing on delivering turnkey machine tending solutions that reduce engineering effort, shorten commissioning time, and improve return on investment for end users. Key players such as ABB, FANUC, Yaskawa Electric, Universal Robots, and KUKA hold strong positions due to their broad robotics portfolios, global service networks, and established relationships with machine tool builders and system integrators. These companies are increasingly shifting from standalone robot sales toward application-specific machine tending cells, integrated software platforms, and standardized automation packages. Emphasis on ease of programming, vision integration, and modular system design is enabling wider adoption among small and mid-sized manufacturers, while also supporting scalability across multi-machine and lights-out production environments.

LIST OF KEY AUTOMATED MACHINE TENDING SYSTEMS COMPANIES PROFILED

- ABB Ltd. (Switzerland)

- Nachi-Fujikoshi Corp. (Japan)

- FANUC Corporation (Japan)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Yaskawa Electric Corporation (Japan)

- Epson Robots (Seiko Epson Corporation) (Japan)

- KUKA AG (Germany)

- Omron Corporation (Japan)

- Universal Robots A/S (Denmark)

- Stäubli International AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Stäubli Robotics launched the MTC-900 Machine Tending Cart, a new plug-and-play automated machine tending solution designed to enhance productivity, safety, and flexibility in industrial settings such as metalworking and injection molding, with seamless integration and rapid deployment features for manufacturers.

- August 2024: Okuma America introduced the Okuma Robot Loader (ORL) series, offering a standardized robotic loading and unloading solution for CNC machines to improve spindle utilization and production efficiency.

- May 2024: ABB launched the OmniVance Collaborative Machine Tending Cell, a pre-engineered solution designed to simplify deployment and reduce setup time for machine tending applications in high-mix manufacturing environments.

- February 2024: Flexxbotics announced a partnership with Vention to deliver integrated robotic machine tending solutions that combine modular automation hardware with digital workcell and machine connectivity software.

- June 2023: Universal Robots launched PolyScope X, a new software platform aimed at simplifying programming and improving flexibility for machine tending and other industrial automation tasks.

REPORT COVERAGE

The global automated machine tending systems market analysis includes a comprehensive study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details strategic partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By System Type, Function, End User, and Region |

| By System Type |

|

| By Function |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 15.07 billion in 2025 and is projected to reach USD 36.48 billion by 2034.

In 2026, the market is expected to reach USD 4.23 billion.

The market is expected to exhibit a CAGR of 10.4% during the forecast period (2026-2034).

By end user, the automotive segment led the market.

The market is driven by the growing need to boost machine utilization and reduce dependence on manual labor through automation in CNC and industrial manufacturing.

ABB, FANUC, Yaskawa Electric, Universal Robots, and KUKA are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us