Cable Fault Locator Market Size, Share & Industry Analysis, By Product Type (Time Domain Reflectometers, Surge Pulse Fault Locator, Acoustic Fault Locator, Bridge Method Fault Locator, Multi-functional/Integrated Fault Locator, & Others), By Cable Type (Low Voltage (LV) Cables, Medium Voltage (MV) Cables, High Voltage (HV) Cables, Communication & Fiber Optic Cables, Control & Instrumentation Cables, & Others), By End-User (Utilities, Telecommunication, Industrial & Manufacturing, Oil & Gas, Railways & Transportation, Construction & Infrastructure Contractors), & Regional Forecast, 2026-2034

Cable Fault Locator Market Size and Future Outlook

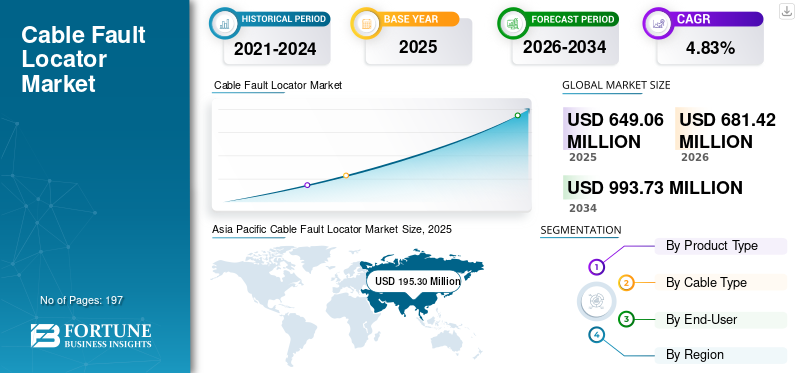

The global cable fault locator market size was valued at USD 649.06 million in 2025. The market is projected to grow from USD 681.42 million in 2026 to USD 993.73 million by 2034, exhibiting a CAGR of 4.83% during the forecast period. Asia Pacific dominated the cable fault locator market with a market share of 30.08% in 2025.

A cable fault locator is a diagnostic device used to detect, identify, and pinpoint faults in electrical cables and wiring systems. These instruments play a critical role in maintaining the reliability and safety of power distribution and communication networks by enabling quick and accurate fault detection. It is widely used across utilities, telecommunications, industrial facilities, and infrastructure projects to minimize downtime, reduce repair costs, and enhance operational efficiency. By accurately locating faults such as short circuits, open circuits, and insulation failures, these devices help streamline maintenance activities and ensure uninterrupted system performance.

The demand for the product is growing steadily, driven by several structural developments in global infrastructure and energy systems. One of the primary drivers is the increasing investment in grid modernization and underground cabling, particularly in urban areas where reliability and safety are critical. The rapid expansion of telecommunications networks, including fiber optic infrastructure, is also contributing to higher adoption of advanced fault location technologies. Additionally, the aging of existing electrical infrastructure across developed regions has increased the need for efficient maintenance and fault detection solutions. The rising emphasis on minimizing downtime in industrial operations, coupled with stricter regulatory standards for electrical safety and reliability, is further supporting market growth.

The global market is moderately fragmented, comprising a mix of established electrical equipment manufacturers and specialized diagnostic solution providers. Key players such as Megger Group, BAUR GmbH, SebaKMT (a Megger company), Hubbell Incorporated, Fluke Corporation, and Radiodetection Ltd. hold a notable presence in the market, particularly in regions with advanced infrastructure. These companies are focusing on technological advancements such as the integration of digital diagnostics, portable cable fault locators, and multifunctional devices, and enhanced accuracy in fault detection. Strategic initiatives, including product innovation, expansion into emerging markets, and incorporation of smart and automated features, are shaping the competitive landscape and driving long-term market growth.

Download Free sample to learn more about this report.

Cable Fault Locator Market Key Takeaways

- 2025 Market Size: USD 649.06 million

- 2026 Market Size: USD 681.42 million

- 2034 Forecast Market Size: USD 993.73 million

- CAGR: 4.83% from 2026–2034

- Asia Pacific dominated the cable fault locator market with a 30.08% share in 2025.

- The time domain reflectometers (TDR) segment accounted for a leading 28.90% market share in 2025.

- The utilities segment held a dominant 32.83% market share in 2025.

Asia Pacific

Asia Pacific led the global market in 2025, supported by rapid urbanization, expansion of underground cabling networks, and increasing investments in power and telecommunication infrastructure.

North America led the global market in 2025, supported by advanced healthcare infrastructure, high blood donation screening standards, and widespread adoption of diagnostic technologies.

North America secured a significant market position due to aging electrical infrastructure, growing grid modernization investments, and rising adoption of predictive maintenance technologies.

Europe

Europe maintained strong market growth driven by regulatory focus on grid reliability, renewable energy integration, and expansion of underground cable systems.

U.S.

The U.S. cable fault locator market was valued at approximately USD 160.11 million in 2025, supported by investments in grid resilience and telecommunications infrastructure expansion.

Japan

Japan is witnessing growing adoption of advanced cable fault detection technologies due to increasing investments in smart grid infrastructure and expanding telecommunications networks.

Read More

Cable Fault Locator Market Trends

Increasing Investments in Grid Modernization and Underground Cabling to Drive Market Growth

The increasing investments in grid modernization and the expansion of underground cabling infrastructure are significantly driving the cable fault locator market growth. As utilities and governments focus on improving the reliability, efficiency, and resilience of power distribution networks, there has been a strong shift toward replacing overhead lines with underground cables, particularly in urban and high-density regions. This transition necessitates advanced diagnostic tools such as a cable fault locator to efficiently detect and repair faults that are otherwise difficult to identify in buried networks. These devices enable utilities to minimize outage durations, reduce operational costs, and enhance service reliability, making them an essential component of modern grid infrastructure.

Furthermore, the rising adoption of renewable energy sources and distributed energy systems has increased the complexity of electrical networks, thereby elevating the need for precise fault detection solutions. Aging grid infrastructure in developed regions, coupled with increasing electricity demand in emerging economies, is also contributing to the need for proactive maintenance and monitoring tools. The product plays a crucial role in predictive maintenance strategies by enabling early detection of potential failures, thereby preventing large-scale disruptions.

For instance, in March 2026, several European utility operators initiated large-scale underground cable replacement projects as part of their grid modernization programs, incorporating advanced cable fault location systems to improve operational efficiency and reduce downtime. This trend highlights the growing importance of the product in supporting the transition toward more reliable and intelligent power networks.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Investment in Power Infrastructure and Grid Reliability is Driving Market Growth

The increasing investment in power infrastructure and the growing focus on grid reliability are major drivers of the market. Utilities and governments worldwide are prioritizing the modernization of aging electrical networks and expanding transmission and distribution systems to meet rising electricity demand. This has led to a significant increase in the deployment of underground and high-voltage cable networks, which require efficient fault detection solutions. The product enables quick identification and repair of faults, thereby minimizing downtime and improving overall network reliability.

In addition, the rising integration of renewable energy sources such as solar and wind into power grids is increasing network complexity, further driving the need for advanced diagnostic tools. These systems require continuous monitoring and maintenance to ensure stable operations, making the product essential for preventive and predictive maintenance strategies. The emphasis on reducing outage durations and improving service quality is encouraging utilities and industrial operators to adopt advanced fault location technologies across their operations.

For instance, in 2026, multiple utility companies across North America and Europe increased investments in underground cabling projects as part of grid resilience programs, incorporating advanced cable fault locator systems to enhance operational efficiency and reduce service interruptions.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Initial Cost and Technical Complexity are Restraining Market Growth

The high initial cost of advanced cable fault locator systems and their associated technical complexity are key restraints for market growth. Modern fault location equipment, particularly multifunctional and high-precision systems, involves significant capital investment, which can be a barrier for small utilities, contractors, and industrial users. In addition to equipment costs, expenses related to training, maintenance, and calibration further increase the total cost of ownership.

Moreover, operating the product often requires skilled personnel with technical expertise in electrical systems and diagnostics. The lack of trained professionals in certain regions can limit the effective utilization of these devices, particularly in developing markets. Complexity also arises in accurately diagnosing faults in mixed cable environments, where different cable types and aging infrastructure can make fault detection more challenging.

For instance, in 2025, several industry participants highlighted the need for specialized training programs to address the skill gap in operating advanced cable diagnostic equipment, emphasizing the challenges associated with complex fault detection technologies.

MARKET OPPORTUNITIES

Expansion of Telecommunications Infrastructure is Creating New Market Opportunities

The rapid expansion of telecommunications infrastructure, particularly fiber optic networks, is creating significant growth opportunities for the cable fault locator market. The increasing demand for high-speed internet, 5G deployment, and data center connectivity is driving large-scale installation of communication cables across both developed and emerging regions. These networks require precise and efficient fault detection solutions to ensure uninterrupted data transmission and minimize downtime.

In addition, the growing adoption of smart cities and digital infrastructure is further accelerating the deployment of communication and control cables, increasing the need for advanced fault location technologies. The product is becoming an essential tool for telecom operators and service providers to maintain network performance and quickly address faults in complex cable systems.

For instance, in 2026, telecom operators across Asia Pacific and Europe expanded their fiber optic networks as part of 5G rollout strategies, incorporating advanced cable testing and fault location equipment to enhance network reliability and reduce maintenance time.

MARKET CHALLENGES

Difficulty in Fault Detection in Complex and Underground Cable Networks is Challenging Market Expansion

The increasing complexity of cable networks, particularly underground and high-density urban installations, presents a significant challenge for the market. Fault detection in underground cables is inherently more difficult compared to overhead systems, as faults are not visible and often require advanced diagnostic techniques to locate accurately. Variations in cable types, insulation materials, and installation conditions further complicate the fault detection process.

Additionally, in densely populated urban areas, multiple cable layers and congested infrastructure can make it challenging to isolate and identify faults without disrupting surrounding systems. Environmental factors such as moisture, soil conditions, and electromagnetic interference can also affect the accuracy of fault detection equipment.

Segmentation Analysis

By Product Type

Time Domain Reflectometers (TDR) Segment Led the Market due to their High Accuracy and Widespread Applicability

Based on product type, the global market is segmented into time domain reflectometers, surge pulse fault locator, acoustic fault locator, bridge method fault locator, multi-functional/ integrated fault locator, and others.

The time domain reflectometers (TDR) segment dominated the market, accounting for 28.90% share in 2025, driven by their high accuracy, ease of use, and widespread applicability across both power and communication cable networks. TDR devices are widely preferred for their ability to quickly detect and locate faults such as open circuits and impedance variations, making them essential tools for utilities, telecom operators, and maintenance service providers. Moreover, continuous advancements in digital diagnostics and portable TDR systems are further enhancing their adoption across field operations.

The multi-functional/integrated fault Locator segment is expected to grow at a CAGR of 5.25% during the forecast period. The growth is supported by the increasing demand for versatile and efficient diagnostic solutions. These systems combine multiple fault detection technologies, enabling users to handle a wide range of cable faults using a single device, thereby improving operational efficiency and reducing equipment costs.

Surge pulse and acoustic fault Locator hold a notable share, particularly in high-voltage and underground cable applications where precise fault pinpointing is required.

By Cable Type

Medium Voltage Cables Segment Dominated the Market, Driven by their Extensive Use in Power Distribution Networks

Based on cable type, the global market is segmented into low voltage (LV) cables, medium voltage (MV) cables, high voltage (HV) cables, communication & fiber optic cables, control & instrumentation cables, and others.

The medium voltage (MV) cables segment captured the dominant cable fault locator market share, accounting for 30.51% in 2025, driven by their extensive use in power distribution networks across urban and industrial environments. MV cables are widely deployed in utilities and infrastructure projects, where maintaining reliability is critical, thereby increasing the demand for efficient fault detection solutions. The growing investments in grid modernization and underground cabling are further supporting the product adoption for MV applications.

The communication and fiber optic cables segment is witnessing strong growth, driven by the rapid expansion of telecommunications networks, including 5G and broadband infrastructure. The product is increasingly being used to ensure uninterrupted data transmission and quick fault resolution, supporting the segment’s growth at a CAGR of approximately 5.98% during the forecast period. The control and instrumentation cables segment contributes a smaller share, while the other segments remain minimal due to their limited application scope.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Utilities Segment Led the Market, Supported by Infrastructure Modernization and Growing Focus on Grid Reliability

Based on end-user, the global market is segmented into utilities, telecommunication, industrial & manufacturing, oil & gas, railways & transportation, construction & infrastructure contractors, and others.

The utilities segment dominated the market, accounting for 32.83% share in 2025, driven by the increasing focus on grid reliability, infrastructure modernization, and the expansion of underground cable networks. Utilities rely heavily on the product to quickly identify and repair faults, minimize outages, and ensure a continuous power supply. The growing integration of renewable energy sources and the need for predictive maintenance are further strengthening demand in this segment.

The telecommunication segment exhibited a CAGR of 6.18% share in 2025. The growth is supported by the rapid expansion of fiber optic networks and increasing demand for high-speed data connectivity. The product is essential for maintaining network uptime and ensuring efficient fault resolution in complex communication infrastructures.

The industrial & manufacturing segment accounts for a notable share, driven by the need to maintain uninterrupted operations and minimize downtime in production facilities.

Cable Fault Locator Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Cable Fault Locator Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the global market, accounting for approximately USD 195.30 million in 2025 and is expected to reach USD 206.69 million by 2026. The market in the region is growing due to rapid urbanization, increasing investments in power transmission and distribution infrastructure, expansion of underground cabling, and rising deployment of telecommunications networks across countries such as China, India, Japan, and Southeast Asia. Government initiatives focused on grid modernization, electrification, and digital infrastructure development are further supporting market growth.

China Cable Fault Locator Market

In 2025, the Chinese market reached approximately USD 67.80 million, driven by strong investments in power grid expansion, increasing underground cable deployment in urban areas, and rapid growth in telecommunications infrastructure. The presence of large-scale manufacturing capabilities and ongoing smart grid initiatives is further driving market expansion.

India Cable Fault Locator Market

The Indian market in 2025 stood at around USD 38.09 million, accounting for a significant share of the Asia Pacific market. The market is growing due to rapid urban development, increasing electrification, expansion of transmission and distribution networks, and rising investments in telecom and digital infrastructure. Government initiatives promoting reliable power supply and infrastructure development are further supporting market growth.

North America

North America was valued at approximately USD 181.78 million in 2025 and is expected to reach USD 190.76 million by 2026. The market in the region is growing due to aging electrical infrastructure, increasing investments in grid modernization, and the widespread adoption of underground cabling systems. The region is witnessing a rising demand for advanced diagnostic tools to improve maintenance efficiency and reduce downtime.

U.S. Cable Fault Locator Market

The U.S. market can be analytically valued at around USD 160.11 million in 2025 and is expected to reach USD 167.86 million by 2026. The U.S. market is growing due to strong investments in grid resilience, increasing adoption of predictive maintenance technologies, and expansion of telecommunications infrastructure.

Europe

The Europe region accounted for USD 173.06 million in 2025 and is likely to touch USD 181.49 million by 2026. The market in Europe is growing due to strong regulatory focus on grid reliability, increasing investments in renewable energy integration, and expansion of underground cable networks. The European Union’s emphasis on reducing outages and improving infrastructure resilience is encouraging the adoption of advanced fault detection solutions.

U.K. Cable Fault Locator Market

The U.K. in 2025 stood at around USD 32.66 million, due to increasing investments in smart grid infrastructure, rising underground cabling projects, and a strong focus on network reliability.

Germany Cable Fault Locator Market

Germany’s market in 2025 stood at around USD 40.97 million, driven by strong industrial infrastructure, expansion of renewable energy projects, and increasing investments in grid modernization.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa accounted for approximately USD 58.58 million and USD 40.34 million in 2025, respectively.

The market in Latin America is growing due to increasing investments in power infrastructure, rising urbanization, and the expansion of electrical networks. Countries such as Brazil and Mexico are witnessing increased deployment of underground cables and modernization of power systems, driving demand for fault detection solutions.

The market in Middle East & Africa is growing due to expanding infrastructure development, rising investments in energy projects, and increasing deployment of underground cable networks across commercial and utility sectors.

GCC Cable Fault Locator Market

The GCC market in 2025 stood at around USD 18.94 million. The market is growing due to increasing investments in smart city projects, expansion of transmission and distribution infrastructure, and rising adoption of advanced diagnostic technologies across countries such as the UAE, Saudi Arabia, and Qatar.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players in the Global Market are Focusing on Advanced Diagnostic Technologies and Integrated Fault Detection Solutions

The cable fault locator market vendors are undertaking various developments to support market growth by focusing on product innovation, integration of advanced diagnostic technologies, and expansion of multifunctional fault detection solutions. Major players such as Megger Group, BAUR GmbH, SebaKMT (a Megger company), Hubbell Incorporated, Fluke Corporation, Radiodetection Ltd., and ABB Ltd. are investing in high-precision fault location equipment, including time domain reflectometers (TDR), surge pulse systems, and integrated diagnostic platforms. These companies are continuously enhancing product capabilities by incorporating features such as digital interfaces, real-time data analysis, portability, and improved fault detection accuracy to support utilities, telecom operators, and industrial users.

For instance, in March 2026, Megger Group introduced an advanced cable fault location system integrating TDR and surge pulse technologies with enhanced digital diagnostics, designed to improve fault detection accuracy and reduce downtime in utility networks. This development highlights the growing focus on integrated and high-performance diagnostic solutions in the market.

LIST OF KEY CABLE FAULT LOCATOR COMPANIES PROFILED

- Megger Group Limited (U.K.)

- BAUR GmbH (Austria)

- Hubbell Incorporated (U.S.)

- Radiodetection Ltd. (U.K.)

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- OMICRON electronics GmbH (Austria)

- HD Electric Company (U.S.)

- Fluke Corporation (U.S.)

- Kepco Inc. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- April 2026: BAUR GmbH launched an advanced cable diagnostic system integrating fault location and condition monitoring capabilities, aimed at improving maintenance efficiency in medium and high-voltage networks.

- March 2026: Megger Group introduced a next-generation cable fault locator combining TDR and surge pulse technologies with enhanced digital analytics for improved accuracy and faster fault identification.

- January 2026: Radiodetection Ltd. expanded its portfolio of cable and pipe locators with upgraded fault-finding capabilities, focusing on improving usability and field performance for utility and telecom applications.

- November 2025: Fluke Corporation introduced advanced handheld diagnostic tools for electrical testing and cable fault detection, targeting industrial maintenance and field service applications.

- September 2025: Hubbell Incorporated enhanced its utility solutions portfolio by introducing improved fault location equipment designed for underground cable networks, supporting faster fault detection and reduced downtime.

REPORT COVERAGE

The global cable fault locator market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.83% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product Type, By Cable Type, By End-User, and Region |

| By Product Type |

|

| By Cable Type |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 649.06 million in 2025 and is projected to reach USD 993.73 million by 2034.

The market is expected to exhibit a CAGR of 4.83% during the forecast period (2026-2034).

The utilities segment led the market in terms of end-user.

Increasing investment in power infrastructure and grid reliability is a key factor driving the market.

Megger Group Limited, BAUR GmbH, Hubbell Incorporated, ABB Ltd., and other companies are among the prominent players in the market.

Asia Pacific dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 197

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us