Cancer Profiling Market Size, Share & Industry Analysis, By Product and Services (Instruments, Reagents and Consumables, and Services), By Technology (Immunoassays, Next-Generation Sequencing, Polymerase Chain Reaction, In-situ Hybridization, Microarrays, Mass Spectrometry, and Other Technologies), By Biomarker Type (Genetic Biomarkers, Protein Biomarkers, and Other Biomarkers), By Cancer Type (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, & Others), By Application (Diagnostics, Prognosis & Risk Assessment, & Others), By End-user, and Regional Forecast, 2026-2034

Cancer Profiling Market Size and Future Outlook

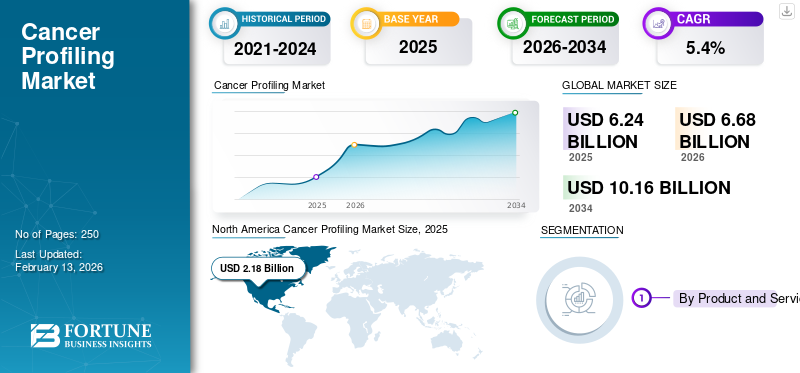

The global cancer profiling market size was valued at USD 6.24 billion in 2025 and is projected to grow from USD 6.68 billion in 2026 to USD 10.16 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. North America dominated the global market with a share of 34.94% in 2025.

Cancer profiling encompasses the tests and software used to read a tumor’s molecular “fingerprint,” from DNA/RNA changes to protein markers, so that clinicians can confirm diagnosis, estimate prognosis, and guide therapy. The market is growing as profiling is moving from a specialist tool for late-stage cases to a routine decision point across diagnosis, therapy selection, and follow-up. At the same time, liquid biopsy enables genomic insights when tissue is limited.

- In February 2024, the WHO reported that more than 35 million new cancer cases are expected in 2050, a 77% increase from an estimated 20 million cases in 2022, underscoring the need for scalable profiling services and faster turnaround times.

Furthermore, Tempus AI, Natera, Inc., Guardant Health, Inc., and Caris Life Sciences held the largest global market share, driven by increasing investments and strategic initiatives, such as new launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

Cancer Profiling Market KEY TAKEAWAYS

- 2025 Market Size: USD 6.24 billion

- 2026 Market Size: USD 6.68 billion

- 2034 Forecast Market Size: USD 10.16 billion

- CAGR: 5.4% from 2026–2034

- North America dominated the cancer profiling market with a 34.94% share in 2025.

- The Next-Generation Sequencing (NGS) segment is projected to hold a 28.1% share in 2026.

- The lung cancer segment is projected to hold a 13.5% share in 2026.

North America

North America held the largest market share in 2025, reaching a valuation of USD 2.18 billion.

Europe

Europe is expected to grow at a CAGR of 4.4% and reach USD 2.01 billion by 2026.

Asia Pacific

Asia Pacific is projected to be valued at USD 1.98 billion in 2026, making it the third-largest regional market.

U.S.

U.S. The market is projected to reach USD 2.08 billion by 2026, supported by advanced oncology research and diagnostics adoption.

Japan

Japan The market is projected to generate approximately USD 0.31 billion in revenue by 2026, driven by increasing demand for precision medicine and cancer diagnostics.

Read More

CANCER PROFILING MARKET TRENDS

Preferential Shift From Single-Gene Tests to Integrated and End-To-End Profiling Pathways to be a New Market Trend

Profiling is steadily shifting from “one biomarker, one test” toward bundled workflows that combine broad panels, reflex testing, and digital reporting. A clear trend is the rise of blood-based profiling alongside tissue-based profiling, especially when time matters or biopsy is risky.

- For instance, in January 2026, Guardant Health said the FDA approved Guardant360 CDx as a companion diagnostic to identify patients with BRAF V600E–mutant metastatic colorectal cancer who may benefit from a specific therapy combination, an example of how CDx labels continue to expand beyond lung into additional solid tumors.

Another trend is greater attention to evolving disease biology and subtype shifts, which increases the value of more comprehensive assays. In February 2025, the International Agency for Research on Cancer (IARC) highlighted that lung adenocarcinoma has become the predominant lung cancer subtype in recent years and noted changing risk patterns, including environmental drivers in some settings. Clinical evidence packages are also becoming more cross-tumor and longitudinal. In October 2025, Foundation Medicine said it would present multiple abstracts at the European Society for Medical Oncology (ESMO) Congress, highlighting the value of biomarker testing across several cancers, reflecting the market’s move toward broader, portfolio-style test menus. As assay complexity grows, providers are packaging interpretation support, variant curation, and structured reports that plug into oncology workflows.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Adoption of Precision Oncology to Fuel Market Growth

Profiling volumes rise when payers and clinicians treat biomarker status as part of the baseline work-up, especially for tumor types with multiple actionable alterations. The macro backdrop is also intensifying as WHO’s February 2024 update highlighted the growing cancer burden and the mounting need for diagnostic services, with more than 35 million new cases predicted in 2050. At the same time, regulators and manufacturers are lowering practical barriers to adoption.

- For instance, in July 2025, Thermo Fisher reported FDA approval of the Oncomine Dx Express Test on the Genexus Dx system as a companion diagnostic and for tumor profiling, supporting faster, more decentralized NGS workflows.

Health systems are also pushing for quicker pathways from imaging to treatment.

- For instance, in March 2024, NHS England expanded a ctDNA pilot for suspected lung cancer. It said the test would be offered to 10,000 patients by the following March, highlighting faster results and the potential to start targeted therapy sooner.

Meanwhile, new screening cases are widening the funnel, as when Guardant said in July 2024 that the FDA approved its Shield blood test as a primary screening option for colorectal cancer, clearing the way for medicare reimbursement. Each time a test becomes embedded in a funded pathway diagnosis, therapy selection, or screening, it “pulls through” demand for logistics, interpretation, and repeat testing at progression in selected patients. Thus, the underlying cancer burden and the expanding patient pool are likely to drive overall market growth.

MARKET RESTRAINTS

Lack of Reimbursement, Evidence Thresholds, and Uneven Access to Limit Market Growth

Cancer profiling is clinically compelling, but adoption can stall when payment rules lag behind science. Many health systems reimburse only for specific indications, stages, or drug-linked companion diagnostics, leaving laboratories to absorb the cost of broader panels, repeat testing, and informatics. Even when a test is on a clear path, it often faces a strong evidence bar.

- For example, Guardant noted in May 2024 that an FDA advisory committee’s recommendation for its Shield colorectal screening test was non-binding, and that Medicare coverage depends on meeting defined performance requirements, signaling that regulators and payers expect robust outcomes data.

Generating that evidence takes time and resources. In May 2025, Foundation Medicine highlighted multiple data abstracts planned for ASCO 2025, reflecting the ongoing need to validate assays across tumors and care settings. Operational realities add friction, such as tissue scarcity, pre-analytical variables affecting results, and cybersecurity and privacy requirements complicating data sharing for real-world evidence. Moreover, labs also face capital constraints, staff shortages, and demands for proficiency testing, which can delay adoption outside major reference centers.

MARKET OPPORTUNITIES

Liquid Biopsy Scale-up and Decentralization of NGS that Improves Diagnostics to Create Significant Growth Opportunities

The next growth wave is likely to come from making profiling easier to order, faster to run, and simpler to interpret. Liquid biopsy is a key lever as it can reduce dependency on tissue adequacy and speed decision-making.

- In May 2025, NHS England said it would roll out a “blood test-first” liquid biopsy pathway for suspected lung cancer across England, aiming to bring targeted therapy forward by weeks for many patients. That kind of system-level adoption creates an opportunity for assay suppliers, reference labs, and informatics vendors to build repeatable workflows at scale from sample logistics to clinical reporting.

Another opportunity is the growing linkage between therapeutics and diagnostics. In January 2026, Guardant Health announced a multi-year strategic collaboration with Merck to develop companion diagnostics and commercialize new cancer therapies using its Guardant Infinity Smart platform. Meanwhile, the push to decentralize NGS could expand testing capacity outside a handful of national centers. In July 2025, Thermo Fisher said its Oncomine Dx Express Test on the Genexus Dx system received FDA approval as a CDx and for tumor profiling, and noted Biodesix would be the first lab to launch the service. Together, these shifts open the door to new service models, regional lab networks, and software layers that standardize interpretation.

MARKET CHALLENGES

Standardization of Tests, Workforce Capacity, and Real-world Integration to Challenge Market Growth

Cancer profiling only adds value when results are accurate, timely, and actionable at the bedside. That puts pressure on the entire chain including specimen quality, pre-analytics, sequencing performance, bioinformatics pipelines, and clinical interpretation. Across regions, labs face uneven access to trained molecular pathologists and bioinformaticians, and many hospitals must decide whether to build in-house capability or rely on reference labs, each with trade-offs in cost, turnaround time, and control over data. Sample shipping, repeat biopsies, and re-tests can also inflate the total cost of care when pathways are poorly coordinated. Data integration is another hurdle as oncology teams want results embedded in electronic records and tumor boards, yet privacy, cybersecurity, and cross-border data rules can slow sharing and automation.

Quality and comparability remain persistent issues as panels evolve; even small differences in coverage, variant calling, and reporting conventions can change treatment decisions. Finally, equity is a practical challenge, not just a policy goal. In February 2024, WHO stressed the “mounting need for services” amid the growing cancer burden, noting that gaps in diagnostic capacity contribute to late diagnosis and poorer outcomes. These conditions make it harder to scale high-complexity profiling beyond major urban centers.

Segmentation Analysis

By Product and Services

Wide Adoption of Cancer Profiling Services to Drive Segment Growth

Based on product and services, the market is segmented into instruments, reagents and consumables, and services.

To know how our report can help streamline your business, Speak to Analyst

Services dominates as most of the value sits in running complex workflows, not just selling products. Profiling typically involves sample logistics, wet-lab processing, sequencing/assay execution, bioinformatics, variant curation, and a clinically formatted report, steps that many hospitals outsource to large reference labs to ensure quality and turnaround time. The trend toward “test-as-a-service” is reinforced by new decentralized platforms that still rely on service infrastructure.

Additionally, the reagents and consumables segment is projected to grow at a CAGR of 7.3% during the forecast period.

By Technology

Wide Next-Generation Sequencing (NGS) Utilisation in Cancer Profiling to Propel Segment Growth

By technology, the market is classified into immunoassays, next-generation sequencing (NGS), polymerase chain reaction (PCR), in-situ hybridization (ISH), microarrays, mass spectrometry, and other technologies.

Next-Generation Sequencing (NGS) segment leads as it consolidates multiple clinically relevant biomarkers into a single run. Single-gene PCR or IHC can answer narrow questions, but NGS panels can detect multiple mutations, fusions, and other variants that influence therapy choice, reducing the need for serial testing and conserving tissue. Moreover, the segment is projected to hold a 28.1% share in 2026.

Additionally, the Polymerase Chain Reaction (PCR) segment is estimated to grow at a CAGR of 4.2% during the forecast period.

By Biomarker Type

Precise Diagnosis and Analysis of Cancer with Help of Genetic Biomarkers to Propel Segment Growth

By biomarker type, the market is classified into genetic biomarkers, protein biomarkers, and other biomarkers.

Genetic biomarkers hold the largest cancer profiling market share as most precision oncology decisions hinge on DNA/RNA alterations that are directly drug-actionable (e.g., mutations, gene fusions) or that guide trial eligibility. Genetic readouts are also easier to standardize across labs than some protein assays when panels are well validated.

Additionally, the protein biomarkers segment is estimated to grow at a CAGR of 3.2% during the forecast period.

By Cancer Type

Rising Burden of Lung Cancer to Propel Segment Growth

By cancer type, the market is classified into breast cancer, lung cancer, colorectal cancer, prostate cancer, melanoma, and other cancer types.

Lung cancer commands a high share as it remains one of the largest global cancer burdens and has a dense set of actionable biomarkers. IARC’s GLOBOCAN 2022 lung fact sheet reports about 2.5 million new lung cancer cases globally in 2022. Clinically, lung pathways increasingly depend on rapid EGFR/ALK/ROS1 and broader genomic profiling to start targeted therapy quickly. Moreover, the segment is projected to hold a 13.5% share in 2026.

Additionally, the colorectal cancer segment is estimated to grow at a CAGR of 6.4% during the forecast period.

By Application

Wide Utilisation of Diagnostic Services in Cancer Detection to Propel Growth

By application, the market is classified into diagnostics, prognosis & risk assessment, treatment selection & monitoring, research applications, and screening & early detection.

Diagnostics is the largest slice as profiling is increasingly ordered at, or close to, initial diagnosis to confirm tumor origin, classify subtype, and establish a baseline biomarker map before first-line therapy. Early profiling avoids delays later, reduces repeat biopsies, and helps clinicians triage patients into targeted drugs or immunotherapy. Moreover, the segment is projected to hold a 35.4% share in 2026.

Additionally, the treatment selection & monitoring segment is estimated to grow at a CAGR of 7.5% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals & Reference Laboratories to Propel Segment Growth

On the basis of end-user, the market is classified into hospitals & reference laboratories, academic & research institutes, pharmaceutical & biotechnology companies, and contract research organizations.

Hospitals and reference laboratories account for the biggest share as they sit where biopsies are taken, diagnoses are signed out, and treatment decisions are made. Many hospitals run front-end pathology (IHC/ISH, triage PCR) and then reflex complex cases to reference labs for comprehensive NGS or liquid biopsy, creating a hub-and-spoke flow. These realities concentrate spending in hospital labs and large reference providers rather than in smaller clinics. Furthermore, the segment is set to hold 60.3% share in 2026.

In addition, the contract research organizations segment is projected to grow at a CAGR of 7.2% during the forecast period.

Cancer Profiling Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cancer Profiling Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 2.03 billion, and reached a valuation of USD 2.18 billion in 2025. North America leads the cancer profiling market by a significant margin, driven by its advanced healthcare infrastructure, high adoption of precision medicine, and strong investment in oncology research. The U.S., in particular, benefits from favorable reimbursement policies, wide utilization of molecular diagnostic technologies, and a robust ecosystem of leading profiling companies and academic research centers. This region also sees intense R&D activity in targeted therapies and companion diagnostics, reinforcing profiling uptake across hospitals and reference labs.

U.S. Cancer Profiling Market

In 2026, the U.S. market is projected to represent USD 2.08 billion, capturing 31.1% of total global revenue.

Europe

Europe is expected to achieve a 4.4% growth rate in the coming years, the second-highest globally, reaching USD 2.01 billion by 2026. Europe’s growth is anchored in strong governmental support for personalized medicine, national genomic initiatives, and rapidly expanding use of multi-biomarker profiling in clinical pathways. The U.K., Germany, and France are pushing genomic medicine strategies and cancer research investments, expanding access to profiling technologies through public healthcare systems. Additionally, rising cancer awareness and structured screening programs are driving demand for advanced profiling to tailor therapy choices. Increasing collaborations between research institutions and profiling providers also contribute to market momentum across Western and Eastern Europe.

U.K. Cancer Profiling Market

The U.K. market is projected to reach USD 0.23 billion by 2026, accounting for 3.5% of the global market revenue.

Germany Cancer Profiling Market

Germany's market is estimated to reach about USD 0.32 billion by 2026, representing roughly 4.8% of global revenue.

Asia Pacific

In 2026, the Asia Pacific cancer profiling market is predicted to be valued at USD 1.98 billion, ranking as the third-largest globally. Asia Pacific is also the fastest-growing region due to rising cancer incidence, rising healthcare expenditures, and improved access to advanced diagnostics in China, India, Japan, and South Korea. Population aging coupled with greater awareness of precision oncology, fuels the adoption of molecular profiling tests. Governmental and private investments in oncology infrastructure, along with technology transfer and partnerships, are expanding profiling services beyond major urban centers. Continued improvements in reimbursement frameworks and lower sequencing costs further enable broader market participation.

Japan Cancer Profiling Market

Japan is projected to generate approximately USD 0.31 billion in revenue by 2026, contributing nearly 4.7% to the global market.

China Cancer Profiling Market

China’s market is estimated to reach approximately USD 0.68 billion by 2026, contributing about 10.1% to global revenues.

India Cancer Profiling Market

India is projected to contribute approximately USD 0.17 billion by 2026, corresponding to about 2.6% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate global cancer profiling market growth, with Latin America expected to reach around USD 0.23 billion by 2026. Latin America’s market growth is nascent but gaining traction as precision oncology awareness rises and research activity increases, particularly in larger healthcare centers. Brazil and Mexico are seeing greater interest in biomarker-driven care and slow but steady investments in genomic capabilities. Expansion of public and private diagnostic labs, and pilot genomic and liquid biopsy programs helps integrate profiling into routine cancer care.

GCC Cancer Profiling Market

By 2026, the GCC is expected to generate approximately USD 0.02 billion, accounting for nearly 0.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Healthy Innovation in Precision Diagnostics to Reinforce Market Position of Prominent Players

The global cancer profiling market is highly competitive and rapidly evolving, marked by a mix of established diagnostics giants, specialized genomic services labs, and nimble biotech innovators. Key players such as Tempus AI, Natera, Inc., Guardant Health, Inc., and Caris Life Sciences compete through diversified portfolios that include comprehensive genomic profiling tests, liquid biopsy assays, bioinformatics platforms, and regulatory-approved companion diagnostics. Their strategies hinge on product innovation, regulatory approvals, strategic partnerships, and expanding global footprints.

Moreover, several emerging players compete through ongoing technological advancements in diagnostics and secure their share in the vast market.

- For instance, Outcomes4Me closed a USD 21 million Series B round in May 2025 to accelerate its AI-driven oncology guidance platform. It expanded into Europe via acquisition, showcasing the rise of digital tools that complement molecular diagnostics with patient-centric decision support.

LIST OF KEY CANCER PROFILING MARKET COMPANIES PROFILED IN REPORT

- Tempus AI (U.S.)

- Natera, Inc. (U.S.)

- Guardant Health, Inc. (U.S.)

- Caris Life Sciences (U.S.)

- NeoGenomics Laboratories (U.S.)

- Exact Sciences Corporation (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Labcorp (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Illumina, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Tempus AI and NYU Langone Health announced a multi-year strategic collaboration aimed at transforming cancer care through advanced molecular profiling and data-driven insights. The collaboration will support NYU Langone Health’s Center for Molecular Oncology at the Laura and Isaac Perlmutter Cancer Center, a comprehensive, pan-cancer initiative to more deeply understand disease biology over time.

- December 2025: Foundation Medicine, Inc., announced it has achieved a historic, unprecedented milestone of 100 approved companion diagnostic indications in the U.S. and Japan across FoundationOne CDx and FoundationOne Liquid CDx.

- Decemebr 2025: Guardant Health and Trial Library, an AI technology company enabling oncology clinical trials as a care option, announced a strategic collaboration to increase access to cancer clinical trials in the U.S.

- July 2025: Thermo Fisher Scientific announced the U.S. Food and Drug Administration (FDA) has approved the Oncomine Dx Express Test on the Ion Torrent Genexus Dx Integrated Sequencer as an In Vitro Diagnostic (IVD) assay for use as a Companion Diagnostic (CDx) for Dizal’s ZEGFROVY (sunvozertinib) and in tumor profiling.

- June 2025: Natera, Inc. announced that its genome-based Signatera MRD assay is now covered by Medicare under LCD L38779.

- April 2025: Illumina and Tempus AI announced a collaboration to accelerate clinical adoption of NGS testing via genomic AI + evidence generation.

- August 2023: QIAGEN announced the U.S. Food and Drug Administration (FDA) approval of its therascreen PDGFRA RGQ PCR kit. This companion diagnostic is intended for use to aid clinicians in identifying patients with Gastrointestinal Stromal Tumors (GIST) who may be eligible for treatment with AYVAKIT (avapritinib).

REPORT COVERAGE

The global cancer profiling market report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product and Services, By Technology, By Biomarker Type, By Cancer Type, By Application, By End-user, and Region |

|

By Product and Services |

· Instruments · Reagents and Consumables · Services |

|

By Technology |

· Immunoassays · Next-Generation Sequencing (NGS) · Polymerase Chain Reaction (PCR) · In-situ Hybridization (ISH) · Microarrays · Mass Spectrometry · Other Technologies |

|

By Biomarker Type |

· Genetic Biomarkers · Protein Biomarkers · Other Biomarkers |

|

By Cancer Type |

· Breast Cancer · Lung Cancer · Colorectal Cancer · Prostate Cancer · Melanoma · Other Cancer Types |

|

By Application |

· Diagnostics · Prognosis & Risk Assessment · Treatment Selection & Monitoring · Research Applications · Screening & Early Detection |

|

By End-user |

· Hospitals & Reference Laboratories · Academic & Research Institutes · Pharmaceutical & Biotechnology Companies · Contract Research Organizations |

|

By Region |

· North America (By Product and Services, By Technology, By Biomarker Type, By Cancer Type, By Application, By End-user, and By Country) o U.S. (By Cancer Type) o Canada (By Cancer Type) · Europe (By Product and Services, By Technology, By Biomarker Type, By Cancer Type, By Application, By End-user, and By Country/Sub-region) o Germany (By Cancer Type) o U.K. (By Cancer Type) o France (By Cancer Type) o Spain (By Cancer Type) o Italy (By Cancer Type) o Scandinavia (By Cancer Type) o Rest of Europe (By Cancer Type) · Asia Pacific (By Product and Services, By Technology, By Biomarker Type, By Cancer Type, By Application, By End-user, and By Country/Sub-region) o China (By Cancer Type) o Japan (By Cancer Type) o India (By Cancer Type) o Australia (By Cancer Type) o Southeast Asia (By Cancer Type) o Rest of Asia Pacific (By Cancer Type) · Latin America (By Product and Services, By Technology, By Biomarker Type, By Cancer Type, By Application, By End-user, and By Country/Sub-region) o Brazil (By Cancer Type) o Mexico (By Cancer Type) o Rest of Latin America (By Cancer Type) · Middle East & Africa (By Product and Services, By Technology, By Biomarker Type, By Cancer Type, By Application, By End-user, and By Country/Sub-region) o GCC (By Cancer Type) o South Africa (By Cancer Type) o Rest of the Middle East & Africa (By Cancer Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.24 billion in 2025 and is projected to reach USD 10.16 billion by 2034.

In 2025, the market value stood at USD 2.18 billion.

The market is expected to exhibit a CAGR of 5.4% during the forecast period of 2026-2034.

The services segment led the market by product and services.

The key factors driving the market are the expanding use of precision oncology in several cancer diagnostics.

Tempus AI, Natera, Inc., Guardant Health, Inc., and Caris Life Sciences are some of the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us