Canned Tuna Market Size, Share & Industry Analysis, By Species (Skipjack, Albacore, Yellowfin, Bigeye, and Others), By Type (Canned Light Tuna and Canned White Tuna), By Preservation Method (Water and Brine and Oil), By Shape (Flakes, Chunks, Fillets, and Others), By Distribution Channel (Foodservice and Retail {Supermarket/Hypermarket, Convenience Stores, Specialty Stores, and Online Retail}, and Regional Forecast, 2026–2034

(Offer valid till 15th Aug 2026)

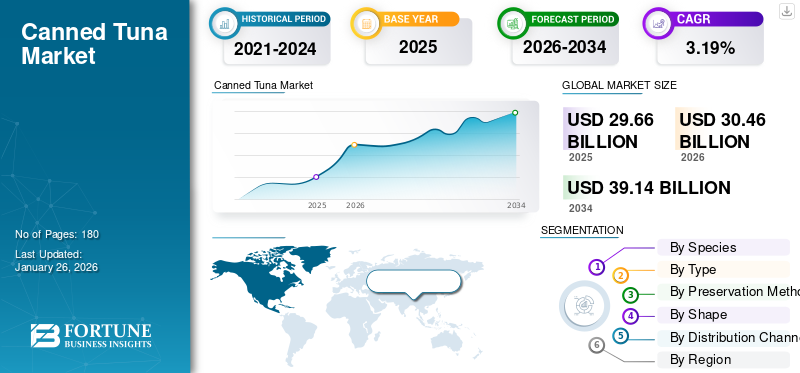

CANNED TUNA MARKET SIZE AND FUTURE OUTLOOK

The global canned tuna market size was valued at USD 29.66 billion in 2025 and is projected to grow from USD 30.46 billion in 2026 to USD 39.14 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 3.19% over the forecast period. Europe dominated the canned tuna market with a market share of 43.96% in 2025.

Some of the prominent manufacturers include Bolton Group, Century Pacific Foods Inc., Grupo Albacore S.A., Bumble Bee Foods LLC , Thai Union Group Inc., and others

The market growth is mainly fueled by the increasing consumption of various packaged food products and beverages. Canned foods consist of various meats, fruits, vegetables, and fish, are precooked or ready to cook, providing convenience and easy consumption. The demand for convenience food products has spurred in recent years owing to busy lifestyles and the rise in the working population, which directly aids in the growth of this market.

Download Free sample to learn more about this report.

CANNED TUNA MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 29.66 billion

- 2026 Market Size: USD 30.46 billion

- 2034 Forecast Market Size: USD 39.14 billion

- CAGR: 3.19% from 2026–2034

- Europe dominated the market with a 43.96% share in 2025.

- Skipjack tuna will account for 66.58% of the market in 2026.

- Canned light tuna will hold 87.33% of the market in 2026.

North America

North America generated USD 8.25 billion in 2025 and is expected to reach USD 8.45 billion in 2026.

Europe

Europe accounted for USD 13.04 billion in 2025 and is projected to reach USD 13.35 billion in 2026, representing 43.96% of the global market.

Asia Pacific

Asia Pacific recorded USD 5.61 billion in 2025 and is projected to reach USD 5.81 billion in 2026.

U.S.

The market is projected to reach USD 6.70 billion by 2026.

Japan

The market is expected to contribute USD 2.10 billion by 2026. China is projected to reach USD 1.15 billion and India USD 0.22 billion by 2026.

Read More

Canned Tuna Market Trends

Growing Incorporation of High-Nutrition Foods in Daily Diets to Bolster Market Development

The growing emphasis on incorporating high-nutrition foods into daily diets to improve health has led to an increase in the consumption of tuna. Consumers are inclined toward such processed products as it is a rich and affordable source of protein and convenient to use. Tuna contains healthy fatty acids crucial for growth and development and is often recommended to pregnant and breastfeeding women to fulfill their nutritional requirements. The wide availability and the increased consumption of tuna play a vital role in boosting the market’s growth.

Download Free sample to learn more about this report.

Impact of COVID-19

The current situation of the market is expected to be affected due to the global COVID-19 pandemic. Since most of the countries went under lockdown in 2020 to stop the transmission of the virus, the availability of processed food products declined due to many production units being shut down. The loss of jobs and increased unemployment negatively affected the purchasing power of consumers across several countries, which in turn affected the sales performance of processed food products.

The rise in product prices and reduced stock of various food products in many emerging economies pose a threat to the market. However, the market is predicted to regain momentum as consumers rely on various packaged and canned food products due to their convenience and easy availability.

- For instance, Thai Union, one of the largest market players in the tuna industry, reported a revenue growth of 5.9% during the first nine months of 2020. The company also expressed optimism about decent sales growth in the coming years. Moreover, the hygiene benefits of canned goods, coupled with the wide consumption of packaged food products, is anticipated to boost market growth in the forthcoming years.

MARKET DYNAMICS

Market Drivers

Rising Consumer Dependency on Ready-to-Cook and Ready-to-Eat Foods to Aid Market Development

Consumers are highly dependent on ready-to-cook and ready-to-eat food products due to the convenience of cooking offered by them. The rise in the working women population and the less time spent on cooking have led to wide utilization of such products including canned foods & beverages. The millennial population is highly inclined toward such convenience food products as they are easy to prepare, offer good nutrition value, and save food preparation time. Many manufacturers are focusing on innovative product launches and certifications to provide consumers with quality products and to serve them better. For instance, in February 2019, Chicken of the Sea launched a new resealable, single-serve recyclable cup of wild-caught tuna to cater to the growing demand for on-the-go food among millennials.

Expanding E-Commerce Channels to Boost Market Expansion

Growing e-commerce channels and the strengthening of the supply chain in the food industry have positively impacted the demand for such products. Online food purchasing platforms have grown in recent times as they have eased access to processed food products. The growing familiarity with the internet has paved new ways for e-commerce. The millennial population is highly tech-savvy and prefers to purchase their products from various online platforms due to convenient purchasing.

In recent years, many new malls and convenience stores have been established, drawing consumers’ attention. This has strengthened supply chains and increased the sales of tuna and other processed food products. Moreover, during situations such as the COVID-19 pandemic, when consumers avoided going to supermarkets and physical stores, sales of canned products through e-commerce channels grew significantly.

Market Restraints

Increasing Demand for Plant-based Food Products to Hinder Market Growth

Consumers demand for plant-based food products has hampered global canned tuna market growth. The mounting environmental and animal welfare concerns among consumers have influenced them to shift toward plant-based products. The growing vegan trend in developing economies has also contributed to the increased utilization of plant-based products. For instance, according to a report published by the World Economic Forum, China’s “free from meat” and “plant-based products” reached a value of approximately USD 12 billion in 2023. The increasing availability of various plant-based fish meat alternatives, which closely replicate the taste and flavor of traditional products, has also nudged consumers to opt for them. For instance, according to the Good Food Institute, the plant-based meat segment of the plant-based foods in the U.S. witnessed a sales growth of 45% in 2020.

Market Opportunities

Launch of Flavored Product to Offer Growth Opportunities

Product innovation is the key driver of success across industries, and the canned seafood market is no exception. Globally, the demand for flavored and innovative products is growing at a higher pace, prompting market players to capitalize on such opportunities to generate higher profits.

- For instance, in January 2020, Thai Union, a Thailand-based seafood producer, partnered with Pa Waen, a local chili paste firm, to introduce spicy tuna flakes in turmeric, pepper, and lemongrass flavors.

Experimental consumption is growing popularity among consumers, prompting manufacturers to explore innovative ways to present their products and expand their market presence.

- In January 2021, Thai Union, one of the leading manufacturers of processed tuna, partnered with After Yum, a food service provider, to launch a DIY spicy tuna salad in a can in supermarket stores. This packaged product consists of lime juice, chili, and other salad ingredients, which consumer can add as per their choice to create a customized meal.

Market Challenges:

Mislabelling of Canned Tuna Fish Products to Erode Consumer Confidence in Products

Mislabeing and adulteration are major challenges faced by the global population. Some producers add adulterants or mislabel their products and sell them in the market. With respect to such canned products, species adulteration and mislabelling are the main hurdles that erode consumer trust in the products. Pseudo-tuna species such as oriental bonito, kawakawa, bullet tuna, and frigate tuna are being used in place of legally recognized tuna species such as skipjack, albacore, and others. Thus, stringent regulatory guidelines need to be established to prevent adulteration of such products.

SEGMENTATION ANALYSIS

By Species

Skipjack Segment Held Majority Market Share, Owing to Wider Availability

Based on species, the market is segmented into skipjack, albacore, yellowfin, bigeye, and others.

The skipjack segment is expected to lead the market, contributing 66.58% globally in 2026. Among these species, skipjack accounts for the highest market share owing to the wide availability of such tuna species globally. The species is of high commercial importance and is commonly found in tropical and subtropical ocean water. Moreover, these tuna species grows rapidly, making its farming for commercial usage comparatively easier than other species.

Yellowfin tuna is another major tuna species which is used for the manufacturing of canned products. These tuna species have a strong meaty structure and flavor and can be used in a wide range of dishes.

Other tuna species used in canned form include albacore, bigeye tuna, and others. These species are rich in protein and omega-3 fatty acids, offering an affordable sources of protein for consumers.

To know how our report can help streamline your business, Speak to Analyst

By Type

Canned Light Segment Set to Dominate Market Backed by Its Numerous Health Benefits

By type, the market is categorized into canned light tuna and canned white tuna.

The canned light tuna segment will account for 87.33% market share in 2026. Light tuna is obtained from skipjack or yellowfin tuna and has a light tan or pink-colored flesh soft texture. It is more flavourful than white tuna, which makes it a desirable choice of fish meat. They are also a great source of essential nutrients such as omega 3 and 6 fatty acids, proteins, and vitamin D. Various food chains and restaurants are utilizing canned light tuna in many culinary dishes such as pasta and tuna casseroles to enhance the taste and flavor of the food. The storage and utility of canned light are easier, saving preparation time before cooking. The younger cohort often prefers foods incorporating exotic fish due to the improved taste, texture, and high nutritional value. Many manufacturers are engaging in the production of canned light tuna and expanding their production facilities due to the high demand.

The canned white tuna segment is projected to grow at a CAGR of 2.73% from 2025 to 2032, owing to its easy availability and low-calorie content. White tuna is obtained from albacore tuna, has a whitish appearance, and the meat is firmer compared to the light tuna. The canned white tuna helps fulfill the nutritional requirements of the body as it is rich in vitamins, minerals, proteins, and essential fatty acids.

By Preservation Method

Oil Segment to Hold Major Market Share as It Enhances Flavor of Products

Based on the preservation method, the market is segregated into water and brine and oil.

The oil segment is expected to account for 70.98% of the market in 2026. Oil such as olive oil and sunflower oil is used in canning to add flavor and enhance the richness of the product. The inclusion of oil in canned products helps to keep them soft and tender.

The water & brine preservation method is forecasted to expand at a CAGR of 2.56% during the forecast period. Water and brine is another major preservation method used in canned seafood products. The use of water helps maintain the original flavor of the tuna while also reducing the calorie content of the packaged products.

By Shape

Chunks Segment to Register Major Market Share Due to Its Appealing Size

Based on shape, the market is segmented into flakes, chunks, fillets, and others.

The chunks segment is anticipated to hold a dominant market share of 61.26% in 2026. These shapes are popular among consumers owing to their huge size and visual appeal. Chunked tuna is suitable for making sandwiches, salads, and wraps, making it more widely used compared to other shapes.

The flakes segment is projected to rise at a CAGR of 2.68% from 2025 to 2032. Tuna shreds are also used one of the major forms of products and are used for preparing a wide range of products, which include past, snacks, wraps, salads and others.

Other shapes in which these products are available in the market include fillet, paste, and others.

By Distribution Channel

Retail Segment Set to Dominate Market Owing to Its Affordability

Based on distribution channels, the market is divided into foodservice and retail {supermarket/hypermarket, convenience stores, specialty stores, and online retail}.

The retail segment is projected to grow at a CAGR of 3.36% during the forecast period of 2025 – 2032. The retail channels account for the highest market share, owing to increased affordability and wider product availability in canned format. Supermarkets/hypermarkets are the preferred channels for purchasing essential and non-essential products due to the wide range of products available under a single roof. The presence of product-distinct aisles and various bundling schemes of tuna offered by the mass merchandisers enhance consumers' purchasing experience. Along with this, these outlets offer convenient purchasing options, as various tuna products are available in different brands and price ranges. The rapid urbanization and changing lifestyles have led to many new mass merchandisers being established, drawing consumers' attention. The emergence of allergen-free and gluten-free bakery products has also created a positive impact on the market. Marketers are focusing on developing the modern trade and retailing sectors to provide a convenient and affordable shopping experience to consumers.

The specialty stores and e-commerce channels are also gaining popularity due to the wide exposure of consumers to various product purchasing platforms on the internet and in specialty retail outlets.

Online retail offers a diverse range of products from numerous brands at a discounted price range, along with the ease of doorstep delivery options, which is expected to boost the sales of the product through this channel.

The food service channel also uses such products as they have a longer shelf life, require limited preparation, and can be used to make dishes such as salads and sandwiches quickly and sell them to consumers.

CANNED TUNA MARKET REGIONAL OUTLOOK

Geographically, the global canned tuna market is analyzed across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Canned Tuna Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Europe market accounted for USD 13.04 billion in 2025, representing 43.96% of the global industry, and is expected to reach USD 13.35 billion in 2026.The global market is experiencing an upward growth trend due to the extensive consumption of processed food products and beverages. Market growth in Europe is attributed to the growing demand for ready-to-eat seafood from the millennial population. The rise in the proportion of working women and busy lifestyles has led to less time being invested in cooking. This has led to increased reliance on various ready-to-eat/cook food products as they save time while fulfilling nutritional requirements.

The U.K. tuna market is anticipated to reach a valuation of USD 1.56 billion by 2026. The leading tuna-consuming markets in the region are Spain, Italy, France, and Portugal. France is projected to record a market size of USD 1.90 billion by 2025. Germany is expected to contribute USD 1.22 billion to the tuna market in 2026.

According to a study by the European Market Observatory for Fisheries and Aquaculture Products (EUMOFA), tuna is the most consumed fish in the region. The per capita consumption of tuna in the year 2018 was 2.78 kg, accounting for an 11% share of all the fishery and aquaculture products. However, due to the COVID-19 pandemic, there has been a dip in the consumption of tuna, especially in the most affected countries, Spain and Italy.

North America

In 2025, North America generated USD 8.25 billion, contributing 27.80% to global market revenue, and is projected to grow to USD 8.45 billion in 2026. North America, the second-largest market for the product, is a developed region with a huge consumer base. The region is experiencing a significant rise in the number of working professionals. The established supply chains and the increasing demand for convenience food will aid market growth. Many multinationals are expanding their production units in the U.S. and Canada, which has led to collaborations with many local players. The presence of a large migrant population in the region leads to a high demand for multi-cuisines and restaurants offering diverse options.

The rise in the cross-culture food consumption trend in the region has led to the widening consumption of various cuisines, such as Japanese and Indian that offer preparations such as tekkadon, sushi, and curries. A steep downfall in the market was observed due to the global outbreak of the COVID-19 pandemic, attributed to low demand for the product from the foodservice industry of the region, especially in the U.S. Many canned food manufacturing companies had shut down, halting production and hampering regional market growth.

The U.S. market is projected to generate USD 6.7 billion in 2026, making it a key contributor to global demand. The U.S. is the largest consumer of canned seafood, including tuna, which is nutritious, convenient, and popular for its cost-effectiveness. Import activities from Thailand, Ecuador, Vietnam, China, Philippines, and others mainly fulfill the domestic demand for canned tuna fish. For instance, the “Vietnam Association of Seafood Exporters and Producers,” an association of seafood in Vietnam, stated that the imports of canned tuna to the U.S. reached 33,000 tons in the first half of 2024.

Asia Pacific

Asia Pacific recorded a market size of USD 5.61 billion in 2025, capturing 18.91% of the global market share, and is projected to reach USD 5.81 billion in 2026. Asia Pacific holds the third-largest market share owing to the large consumer base in the region. China’s tuna market is predicted to reach USD 1.15 billion in 2026. The growing millennial population in the region and its rising inclination toward convenience food have contributed to boosting market growth. Rapid urbanization and the incorporation of Western lifestyles have increased the demand for canned foods. Consumers now widely use them for food preparations due to their convenience of cooking and longer shelf life. This trend has further fueled the market’s growth in the region. India is anticipated to generate USD 0.22 billion in market value by 2026. Japan is expected to contribute USD 2.10 billion to the tuna market in 2026.

South America and Middle East & Africa

The Middle East & Africa market generated USD 0.77 billion in 2025, representing 2.61% of the global market landscape, and is expected to reach USD 0.79 billion in 2026. Latin America accounted for USD 1.99 billion in 2025, representing 6.72% of the global market share, and is projected to reach USD 2.05 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Focus on New Product Launches for Development of Canned Tuna

Leading players are focusing on launching innovative and exotic seafood variants to address the rising demand among consumers. These players are collaborating with ingredients and seasonings producers to develop exotic products. For instance, In January 2020, Thai Union partnered with a local producer of mixed chili paste to launch five new flavors of spicy tuna flakes for the Thai market. The “SEALECT” spicy tuna flakes come in five flavors, combining key Thai spices such as galangal, turmeric, bird’s eye chili, pepper, and lemongrass. Bolton Group, Century Pacific Foods Inc., Grupo Albacore S.A., Thai Union Group PCL, Bumble Bee Foods LLC, American Tuna Inc. Ocean, and StarKist Co. are the prominent market players in global canned tuna market.

Major Players in the Canned Tuna Market

To know how our report can help streamline your business, Speak to Analyst

Bolton Group, Century Pacific Foods Inc., Grupo Albacore S.A., Bumble Bee Foods LLC, and Thai Union Group Inc. are some of the key players in the market. The global market is semi-fragmented, with the top 5 players accounting for around 40% of the global canned tuna market share.

LIST OF KEY MARKET PLAYERS PROFILED:

- Thai Union Group PLC (Thailand)

- StarKist Co. (U.S.)

- E.C. Canning Company Limited (Thailand)

- American Tuna Inc. (U.S.)

- Bumble Bee Foods LLC (U.S.)

- Century Pacific Food Inc. (Philippines)

- Crown Prince Inc. (U.S.)

- Grupo Albacora SA (Spain)

- Wild Planet Foods Inc. (U.S.)

- Golden Prize Canning Co. Ltd. (Thailand)

- Ocean's (Canada)

- Dongwon Enterprise Co., Ltd. (South Korea)

KEY INDUSTRY DEVELOPMENTS:

- December 2023 - Tonnito, a leading U.S. canned tuna brand, launched six canned tuna products in the tuna category. The product lineup includes premium yellowfin tuna chunks with sweet corn in water, premium yellowfin tuna with carrots & peas in vegetable oil and others available in Walmart grocers in U.S.

- May 2023 - Thailand seafood manufacturer Thai Union Group launched canned tuna products targeting health-conscious consumers. The canned tuna steak in Himalayan pink brine, a part of the Sealect brand, is rich in protein, selenium, and omega 3.

- March 2021 - Turkish company Dardanel, a leading manufacturer of canned and frozen seafood, completed the acquisition of Greek seafood manufacturer G. Kallimanis SA.

- February 2020 - Fong Chun Formosa Fishery Company (FCF), a Taiwanese canned tuna manufacturer, acquired the U.S. brand “Bumble Bee Foods” for USD 928 million.

- November 2019 - Grupo Jealsa Rianxeira SAU, a Spanish company, launched a new line of 100% sustainable tuna. The product bears a blue label, indicating wild, traceable fish from fisheries certified by the Marine Stewardship Council (MSC) Fisheries Standard.

Investment Analysis and Opportunities

There is a significant opportunity for manufacturers and new entrants to launch new products in this segment. The growing cross-cultural food trend is expected to support the growth of the global canned tuna market. As e-commerce penetration in developing economies is increasing, manufacturers can expand their market presence in such countries and increase their overall revenue.

REPORT COVERAGE

The canned tuna market research report includes qualitative and quantitative insights into the industry. It also offers a detailed analysis of the market size and growth rate for all possible segments. Various key insights presented in the report give an overview of related markets, competitive landscape, recent industry developments such as mergers & acquisitions, the regulatory scenario in critical countries, and key industry trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.19% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Species

|

|

By Type

|

|

|

By Preservation Method

|

|

|

By Shape

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the value of the market was USD 29.66 billion in 2025 and is projected to reach USD 39.14 billion by 2034.

Growing at a CAGR of 3.19%, the market will exhibit steady growth in the forecast period.

Based on type, the canned light tuna segment leads the segment.

Rising consumer inclination toward convenience food is a key factor that drives the growth of the market.

Thai Union Group PCL, Bumble Bee Foods LLC, StarKist Co., and American Tuna Inc. are some of the top players in the market.

Europe dominated the canned tuna market with a market share of 43.96% in 2025.

By distribution channel, the retail segment leads the market.

The increased demand for affordable and nutritious, protein-rich food, especially in developing economies, is a key market trend.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us