Class 8 Trucks Market Size, Share & Industry Analysis, By Truck Configuration (Tractor Trucks, Rigid Trucks, Dump Trucks, Concrete Mixers, and Other Vocational Trucks), By Application (Long-Haul Freight & Logistics, Construction, Mining & Off-Highway, and Municipal & Utilities), By Propulsion (Diesel, Battery Electric, Hybrid Electric, and Hydrogen Fuel Cell), By Axle Configuration (4×2, 6×4, 8×4, and Others), and Regional Forecast, 2026-2034

Class 8 Trucks Market Size and Future Outlook

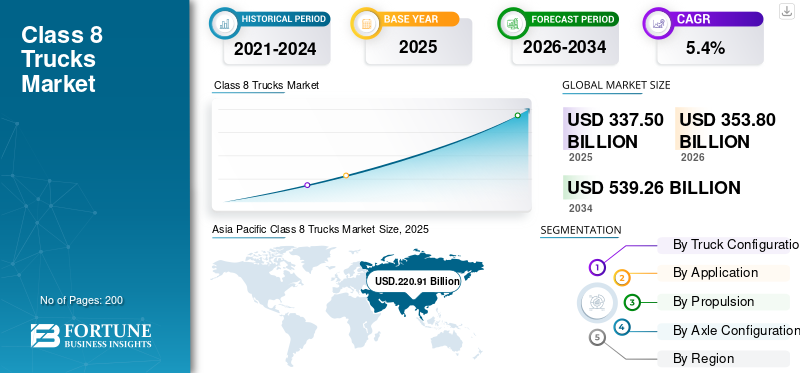

The global class 8 trucks market size was valued at USD 337.50 billion in 2025. The market is projected to grow from USD 353.80 billion in 2026 to USD 539.26 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the class 8 trucks market with a market share of 65.45% in 2025.

Class 8 trucks are heavy-duty commercial vehicles with a Gross Vehicle Weight Rating (GVWR) exceeding 33,000 pounds. They include tractor-trailers, dump trucks, and cement mixers used for long-haul freight and industrial transport. Market drivers include economic expansion, infrastructure development, technological advancements, regulatory support, and rising consumer or industrial requirements.

Major players in the Class 8 trucks market include Daimler Truck (Freightliner and Western Star), Volvo Group, PACCAR Inc., and Traton Group (Scania, MAN, and Navistar), competing through fuel efficiency, advanced safety systems, electrification, telematics integration, and fleet-focused performance solutions.

Download Free sample to learn more about this report.

CLASS 8 TRUCKS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 337.50 billion

- 2026 Market Size: USD 353.80 billion

- 2034 Forecast Market Size: USD 539.26 billion

- CAGR: 0.054% from 2026–2034

- Asia Pacific dominated the class 8 trucks market with a market share of 65.45% in 2025.

- The construction segment is projected to expand at an annual growth rate CAGR of 6.9% during the forecast period.

- The dump trucks segment is projected to grow at a compound annual growth rate of 7.6% during the forecast period.

North America

The North American market represents the third-largest market, supported by robust long-haul freight networks and high truck utilization rates.

Europe

Europe holds the second-largest market share, expanding at a CAGR of 2.6% during the forecast period.

Asia Pacific

Asia Pacific dominates the class 8 trucks market and is projected to register the fastest CAGR during the forecast period.

U.S.

The U.S. market in 2026 is estimated at around USD 51.17 billion.

Japan

The Japanese market in 2026 is estimated at around USD 51.27 billion, accounting for roughly 14.5% of global revenues.

Read More

CLASS 8 TRUCKS MARKET TRENDS

Electrification and Alternative Powertrains Transforming Market Trends

Electrification is emerging as one of the key class 8 trucks market trends, with OEMs investing heavily in battery-electric and hydrogen fuel cell platforms. Sustainability commitments, emission reduction targets, and advancements in battery energy density are reshaping product development strategies. Fleet operators are increasingly testing zero-emission heavy-duty vehicles to align with regulatory frameworks and corporate ESG goals. This transition is influencing the market, as truck manufacturers diversify portfolios and expand charging infrastructure partnerships.

- For instance, in February 2026, Tesla’s Semi electric Class 8 truck was officially updated with a powertrain output of 800 kW, confirmed two range variants (Standard & Long Range), and is nearing mass production this year, marking a major milestone in heavy-duty EV rollout.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Freight Activity and E-Commerce Expansion to Accelerate Market Growth

Growing freight transportation demand, fueled by e-commerce expansion, industrial output, and cross-border trade, is significantly driving the class 8 trucks market growth. Increasing last-mile and long-haul logistics requirements are strengthening market demand for heavy-duty trucks capable of handling large cargo volumes efficiently. Infrastructure investments and supply chain optimization initiatives are further supporting fleet expansion. As logistics operators seek improved uptime and load capacity, manufacturers are benefiting from higher production volumes and long-term procurement contracts.

- For instance, in February 2026, DHL and Westwing expanded their low-carbon logistics partnership to accelerate sustainable e-commerce deliveries across Europe. The collaboration focuses on electric vehicles, sustainable fuels, and carbon-reduced transport solutions, strengthening green supply chains and supporting emission reduction targets in regional freight operations.

MARKET RESTRAINTS

High Costs of Product to Fuel Market Growth

The high upfront cost of class 8 trucks, particularly advanced diesel and electric variants, remains a major restraint in the market. Rising raw materials prices, technology integration expenses, and compliance with emission standards increase vehicle pricing. Small and mid-sized fleet operators often delay replacement decisions due to capital constraints and financing challenges. This slows new vehicle penetration in certain regions, moderating overall market growth despite steady freight demand and increasing operational efficiency requirements.

MARKET OPPORTUNITIES

Connected Fleet Management and Telematics Integration Creating Growth Opportunities

The growing adoption of connected vehicle technologies presents a strong opportunity in the class 8 trucks market demand. Advanced telematics, predictive maintenance systems, and real-time fleet monitoring solutions are improving operational efficiency and reducing downtime. Fleet operators are prioritizing data-driven decision-making to optimize fuel consumption, route planning, and vehicle utilization. These digital advancements are enhancing value-added services and strengthening aftermarket revenue streams, creating long-term expansion opportunities during the forecast period.

- For instance, in February 2026, Daimler Truck North America (DTNA) partnered with Class8 to expand digital services for Freightliner owner-operators. This enhances fleet management, analytics, and uptime solutions through connected data platforms, boosting operational efficiency and support for independent truckers.

MARKET CHALLENGES

Supply Chain Disruptions and Semiconductor Shortages to Challenge Industry Growth

Persistent supply chain disruptions and semiconductor shortages continue to challenge production stability in the class 8 trucks industry. Heavy reliance on global component sourcing exposes manufacturers to delays, increased costs, and unpredictable delivery schedules. Logistics bottlenecks and raw material price fluctuations further impact manufacturing timelines. These factors complicate market analysis and short-term forecasting, as OEMs must balance order backlogs with production capacity while maintaining competitive market share across regions.

Segmentation Analysis

By Application

Rising Industrial Output Leads due to the Long-Haul Freight & Logistics Segment

Based on application, the market is segmented into long-haul freight & logistics, construction, mining & off-highway, and municipal & utilities.

The long-haul freight & logistics segment holds the largest class 8 trucks market share due to sustained freight movement across national and cross-border corridors. Rising industrial output, retail distribution networks, and e-commerce bulk transportation requirements drive consistent market demand. Large fleet operators continuously invest in fuel-efficient and technologically advanced trucks to optimize operating costs. Strong replacement cycles, high annual mileage, and fleet standardization strategies collectively reinforce market share concentration within this segment.

- For instance, in May 2025, Aurora Innovation began commercial driverless Class 8 trucking operations between Dallas and Houston, completing over 1,200 autonomous miles with no driver on public roads. It’s the first U.S. rollout of self-driving freight service, with plans to expand routes to El Paso and Phoenix.

The construction segment is projected to expand at an annual growth rate CAGR of 6.9% during the forecast period. Increasing infrastructure investments, mining activities, and urban development projects are accelerating demand for heavy-duty dump and vocational trucks, strengthening segment growth.

To know how our report can help streamline your business, Speak to Analyst

By Truck Configuration

Tractor Trucks Segment Leads due to itsCritical Role in Long-Haul Freight

Based on truck configuration, the market is segmented into tractor trucks, rigid trucks, dump trucks, concrete mixers, and other vocational trucks.

The tractor trucks segment dominates the market due to its critical role in long-haul freight transportation and trailer-based cargo movement. These vehicles form the backbone of logistics fleets, supporting high-volume interstate and international trade. Strong replacement demand, fleet standardization, and increasing adoption of fuel-efficient powertrains sustain market growth. Their widespread deployment across retail, manufacturing, and bulk commodity transport ensures substantial and stable market share.

- For instance, in Q2 2025, according to the International Council on Clean Transportation (ICCT), the U.S. medium and heavy-duty vehicle market witnessed 116,908 new registrations. However, overall sales contracted year-over-year with 4.6% fewer vehicles and 34.2% fewer zero-emission units compared to Q2 2024, while zero-emission heavy-duty trucks remained below 1% of total registrations.

The dump trucks segment is projected to grow at a compound annual growth rate of 7.6% during the forecast period. Rising infrastructure development, mining expansion, and large-scale construction projects are accelerating demand for heavy-duty vocational trucks, driving segment growth.

By Propulsion

Diesel Segment Dominates due to itsProven Reliability

By propulsion, the market is divided into diesel, battery electric, hybrid electric, and hydrogen fuel cell.

The diesel segment dominates the market owing to its proven reliability, high torque output, and widespread refueling infrastructure. Diesel-powered trucks remain the preferred choice for long-haul freight and heavy-load applications due to superior range and operational efficiency. Fleet operators prioritize diesel platforms for predictable performance and lower upfront costs compared to alternative powertrains. Strong aftermarket support and global service networks further reinforce market growth.

- For instance, in May 2025, Revoy introduced its retrofitted diesel-electric hybrid solution for Class 8 trucks, enabling fleets to convert existing diesel tractors into hybrid systems. The technology aimed to reduce fuel consumption and emissions while extending vehicle life and lowering the total cost of ownership.

The battery electric segment is projected to grow at a CAGR of 8.0% during the market forecast period. Increasing emission regulations, corporate sustainability goals, and advancements in battery technology are accelerating market demand.

By Axle Configuration

Optimal Balance Between Load-Carrying Capacity Boosts 6x4 Axle Configuration Segment Growth

By axle configuration, the market is categorized into 4×2, 6×4, 8×4, and others.

The 6x4 segment dominates the market due to its optimal balance between load-carrying capacity, traction performance, and fuel efficiency. Widely deployed in long-haul and regional freight operations, 6x4 trucks provide enhanced stability for heavy loads while maintaining operational cost-efficiency. Fleet operators favor this configuration for its versatility across highways and varied terrains, reinforcing its strong market share and sustained contribution to overall market growth.

- For instance, in September 2025, Volvo Trucks North America opened orders for its redesigned Volvo VNR regional haul Class 8 truck, available in multiple axle configurations, including 4x2 and 6x4. The model features improved fuel efficiency, enhanced safety technologies, and upgraded connectivity solutions for regional freight operations.

The 8x4 axle configuration is projected to grow at a CAGR of 6.2% during the forecast period. Rising construction, mining, and infrastructure activities are increasing demand for higher load-bearing trucks, strengthening market demand.

Class 8 Trucks Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific dominates the class 8 trucks market and is projected to register the fastest CAGR during the forecast period. Strong industrialization, expanding manufacturing output, and large-scale infrastructure development across China, India, and Southeast Asia are accelerating market demand. Growing cross-border trade and logistics network expansion further support market growth. Additionally, increasing fleet modernization and rising domestic consumption contribute to sustained market share, strengthening the region’s overall market analysis outlook.

Asia Pacific Class 8 Trucks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

For instance, in January 2026, Windrose Electric’s Class 8 truck achieved homologation in the U.S., EU, and China, clearing regulatory approval for commercial operations across major markets. The all-electric heavy-duty truck targets long-haul and regional freight segments with zero-emission performance.

China Class 8 Trucks Market

The Chinese market in 2026 is estimated at around USD 151.54 billion, accounting for roughly 42.8% of global revenues. Strong manufacturing output, infrastructure expansion, and domestic freight demand sustain market growth and reinforce its dominant market share globally.

Japan Class 8 Trucks Market

The Japanese market in 2026 is estimated at around USD 51.27 billion, accounting for roughly 14.5% of global revenues. Stable replacement cycles, advanced technology adoption, and efficient logistics networks support steady market growth across the forecast period.

India Class 8 Trucks Market

The Indian market in 2026 is estimated at around USD 20.05 billion, accounting for roughly 5.7% of global revenues. Rapid infrastructure development, rising industrialization, and freight corridor expansion further drive market growth.

Europe

Europe holds the second-largest market share, expanding at a CAGR of 2.6% during the forecast period. Stable freight activity, structured fleet replacement cycles, and stringent emission regulations shape regional market trends. Demand is largely driven by the modernization of existing fleets and the gradual adoption of low-emission vehicles. Strong regulatory frameworks and established logistics networks support consistent market growth despite moderate economic expansion across key countries.

- For instance, in January 2026, Daimler Truck outlined plans to begin pilot production of its hydrogen-powered fuel cell trucks in Germany, advancing zero-emission heavy-duty mobility. The initiative supports large-scale testing, infrastructure coordination, and gradual commercialization of hydrogen-based long-haul transport solutions across Europe.

Germany Class 8 Trucks Market

The Germany market in 2026 is estimated at around USD 8.75 billion, accounting for roughly 2.5% of global revenues. Strong export activity, structured fleet modernization, and emission-compliant vehicle adoption sustain consistent market demand.

U.K. Class 8 Trucks Market

The U.K. market in 2026 is estimated at around USD 5.76 billion, accounting for roughly 1.6% of global revenues. Replacement-driven procurement, logistics optimization, and regulatory compliance initiatives further support market growth.

North America

The North American market represents the third-largest market, supported by robust long-haul freight networks and high truck utilization rates. The presence of major OEMs, large fleet operators, and advanced telematics integration sustains market demand. Replacement cycles, driven by mileage intensity and regulatory compliance, contribute to stable market growth. Expanding e-commerce distribution and cross-border trade between the U.S., Canada, and Mexico further influences regional market growth.

- For instance, in March 2023, Nikola announced it would become the first U.S. truck manufacturer to integrate the PlusDrive next-generation safety system into its Class 8 electric trucks. This enhances driver assistance capabilities, collision mitigation, and advanced highway automation features for improved fleet safety and performance.

U.S. Class 8 Trucks Market

The U.S. market in 2026 is estimated at around USD 51.17 billion, accounting for roughly 14.5% of global revenues. High freight intensity, large fleet operators, and technological integration reinforce strong market demand.

Rest of the World

The Rest of the World region, including South America and the Middle East & Africa, demonstrates gradual market growth driven by infrastructure investments and resource-based industries. Mining, construction, and energy projects are key contributors to market expansion. Although economic volatility influences procurement cycles, improving logistics networks and trade corridors supports long-term expansion. Market trends in this region indicate rising fleet upgrades and increasing participation of global manufacturers.

- For instance, in October 2024, Emirates Transport partnered with Al Ghurair Motors at GITEX Global to test hydrogen and electric commercial vehicles. This advances zero-emission mobility initiatives in the UAE and supports pilot deployments of alternative-fuel heavy-duty trucks within public sector fleets.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Electrification to Strengthen Differentiation

The market is moderately consolidated, with a few global OEMs holding significant market share. Key players such as Daimler Truck, Volvo Group, PACCAR, and Traton Group compete through fuel-efficient platforms, advanced safety systems, and connected fleet technologies. Companies focus on electrification, autonomous driving capabilities, and telematics integration to strengthen differentiation. Strategic partnerships, localized production, and long-term fleet contracts enhance competitive positioning. Increasing investments in battery-electric and hydrogen-powered trucks further intensify competition during the forecast period.

- For instance, in July 2025, Torc Robotics announced the opening of a new engineering center in Ann Arbor, Michigan, to accelerate the development and validation of autonomous Class 8 truck technology. This strengthens its software, systems integration, and commercialization capabilities for future driverless freight operations.

LIST OF KEY CLASS 8 TRUCKS COMPANIES PROFILED

- Daimler Trucks AG (Germany)

- Volvo Group (Sweden)

- PACCAR Inc. (Kenworth, Peterbilt, DAF) (U.S.)

- Traton Group (Germany)

- Isuzu Motors Limited (Japan)

- Hino Motors, Ltd. (Japan)

- FAW Jiefang Automotive Co., Ltd. (China)

- Dongfeng Commercial Vehicle Co., Ltd. (China)

- Sinotruk (China National Heavy Duty Truck Group) (China)

- Foton Motor Group (China)

- Ashok Leyland (India)

- Tata Motors Limited (India)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Hyundai Motor said its XCIENT Fuel Cell Class 8 fleet surpassed 20 million kilometers driven across Europe (as of January 2026), highlighting multi-country deployments and positioning hydrogen trucks as scalable alternatives for logistics, distribution, and specialized heavy-duty operations.

- February 2026: Class8 launched its platform with Daimler Truck North America to bring cost-reducing digital tools to Freightliner fleets, including solutions such as ELD support, dispatch, and load recommendations, and AI-enabled workflow tools designed to improve efficiency in challenging freight conditions.

- May 2025: Aurora Innovation began commercial driverless trucking in Texas, running regular Dallas-Houston customer deliveries and reporting over 1,200 autonomous miles without a driver, marking a key milestone for self-driving Class 8 freight services and setting expansion plans to additional lanes.

- May 2025: Mack Trucks intensified competition in the market, challenging Tesla Semi’s positioning by expanding its battery-electric portfolio and targeting vocational and regional haul segments with robust, purpose-built zero-emission heavy-duty solutions.

- April 2025: Kenworth introduced the battery-electric T880E for vocational applications and unveiled the next-generation T680E for regional haul operations. This strengthens its Class 8 electrification strategy with improved range, performance, and advanced driver-focused technologies.

- March 2025: KAG Canada and Innovative Fuel Systems (IFS) reported commercial operation of a hydrogen dual-fuel Class 8 truck, hauling fuel to Edmonton International Airport since December 2024, aiming to cut emissions and improve fuel economics using IFS’ multi-fuel platform.

- May 2024: Honda announced it would debut a Class 8 hydrogen fuel cell truck concept at ACT Expo 2024, launching a new demonstration initiative and seeking collaboration partners for future North American production of fuel cell-powered heavy-duty products.

REPORT COVERAGE

The global class 8 trucks market analysis provides an in-depth study of the market size & forecast by all the market segments included in the vehicle security components market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.4% from 2026 to 2034 |

| Unit | Value (USD Billion) and Volume (Units) |

| Segmentation | By Truck Configuration, By Application, By Propulsion, By Axle Configuration, and By Region |

| By Truck Configuration |

|

| By Application |

|

| By Propulsion |

|

| By Axle Configuration |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 337.50 billion in 2025 and is projected to reach USD 539.26 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 220.91 billion.

The market is expected to exhibit a CAGR of 5.4% during the forecast period (2026-2034).

The long-haul freight & logistics segment leads the market in terms of application.

Rising freight activity and e-commerce expansion are the key factors driving market growth.

Key players such as Daimler Truck, Volvo Group, PACCAR, and Traton Group.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us