Clean-Label Ingredients Market Size, Share & Industry Analysis, By Form (Dry and Liquid), By Type (Natural Colors, Natural Flavors, Sweeteners & Starch, Flours, Malts, and Others), By Certificates (Organic, Non-GMO, Gluten-Free, and Others), By Application (Food & Beverages [Bakery & Confectionery, Dairy Products, Prepared Meals/RTE Meals, Snacks & Cereals, Meat & Seafood, and Others], Dietary Supplements, and Animal Feed), and Regional Forecast, 2026–2034

(Offer valid till 15th Aug 2026)

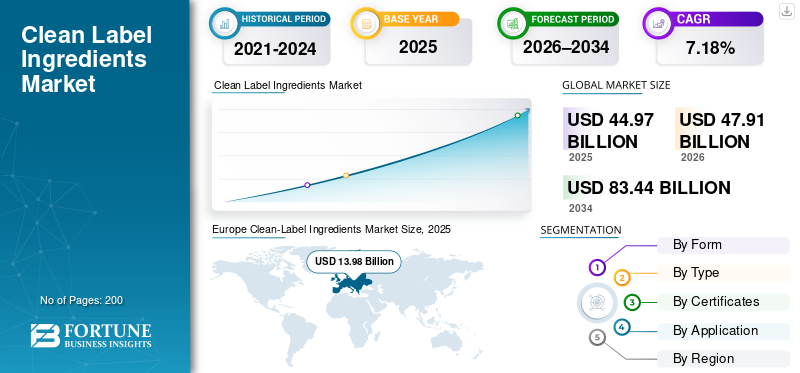

Clean-Label Ingredients Market Size and Future Outlook

The global clean-label ingredients market size was valued at USD 44.97 billion in 2025. The market is projected to grow from USD 47.91 billion in 2026 to USD 83.44 billion by 2034, exhibiting a CAGR of 7.18% during the forecast period. Europe dominated the clean-label ingredients market with a market share of 31.08% in 2025.

Clean-label ingredients include naturally derived colors, flavors, sweeteners, starches, flours, malts, and functional ingredients that are minimally processed and free from risks associated with artificial additives. These ingredients are widely used across food & beverages, bakery & confectionery, dairy, snacks & cereals, prepared meals, meat & seafood alternatives, dietary supplements, and animal feed.

The market growth is primarily driven by ingredient transparency mandates, increasing consumer distrust of synthetic additives, regulatory pressure on artificial ingredients, and the rapid adoption of natural formulations by global food manufacturers. The market is dominated by Kerry Group, DSM-Firmenich, Ingredion Incorporated, Cargill Incorporated, and Archer-Daniels-Midland Company (ADM).

Download Free sample to learn more about this report.

Clean Label Ingredients Market Takeaways

- 2025 Market Size: USD 44.97 Billion

- 2026 Market Size: USD 47.91 Billion

- 2034 Forecast Market Size: USD 83.44 Billion

- CAGR: 7.18% from 2026–2034

- Europe dominated the clean-label ingredients market with a 31.08% share in 2025.

- The flours segment led the market with a value of USD 20.32 billion in 2025.

- The liquid segment is projected to grow at the fastest CAGR of 8.10% during the forecast period.

North America

North America reached USD 12.17 billion in 2025 and is expected to expand at a CAGR of 6.37% during the forecast period.

Europe

Europe led the global market with a valuation of USD 13.98 billion in 2025 and is projected to grow at a CAGR of 5.85% through 2034.

Asia Pacific

Asia Pacific accounted for USD 12.96 billion in 2025 and is the fastest-growing regional market, registering a CAGR of 9.23%.

U.S.

The U.S. clean-label ingredients market was valued at approximately USD 9.57 billion in 2025.

Japan

Japan is witnessing increasing adoption of clean-label ingredients, driven by consumer preference for natural, minimally processed food formulations.

Read More

Clean-Label Ingredients Market Trends

Rising Demand for Ingredient Transparency and Natural Formulations

The surging demand for ingredient transparency and natural formulations is fundamentally reshaping the food, beverage, nutraceuticals, and alternative proteins markets by compelling manufacturers to prioritize clean-label products with recognizable, minimally processed ingredients. Consumers, particularly millennials and Gen Z, increasingly scrutinize labels for synthetic additives, preservatives, and ultra-processed elements, driven by health concerns, skepticism toward "ultra-processed foods" (UPFs), and a preference for authenticity and sustainability, indirectly accelerating clean-label adoption.

- According to the Food and Agriculture Organization (FAO), ultra-processed foods account for over 50% of the total caloric intake in several developed economies, prompting governments and consumers to reassess ingredient quality and processing levels.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Consumer Health Awareness and Regulatory Scrutiny to Accelerate Market Growth

The surging consumer health awareness and intensifying regulatory scrutiny are propelling the clean-label ingredients market growth by fostering the demand for natural, transparent products and enforcing stricter compliance standards. Health-conscious consumers, empowered by digital access to nutritional information, increasingly reject artificial additives, preservatives, and synthetic flavors, opting for recognizable, minimally processed ingredients that align with wellness trends such as clean eating and preventive nutrition.

- For instance, regulatory bodies such as the U.S. FDA and the European Food Safety Authority (EFSA) have progressively reviewed and restricted the use of certain synthetic emulsifiers, colors, and preservatives, encouraging food manufacturers to shift toward natural alternatives.

Market Restraints

Higher Processing Costs and Raw Material Price Volatility to Limit Market Expansion

Despite strong demand, clean-label ingredients often carry higher production and sourcing costs compared to synthetic counterparts. Natural ingredients are sensitive to climatic variability, crop yields, and regional supply disruptions, creating pricing volatility.

- The U.S. Department of Agriculture (USDA) reported that prices for key clean-label feedstocks, including corn, wheat, and specialty crops used in natural sweeteners and starches, rose by 25–60% between 2020 and 2022, significantly increasing input costs for ingredient processors.

Market Opportunities

Expansion of Clean-Label Applications in Functional Foods and Premium Nutrition Products to Unlock New Growth Avenues

The expansion of clean-label applications into functional foods and premium nutrition products unlocks substantial growth opportunities by meeting the consumer demand for health benefits delivered through transparent, natural ingredients. Functional foods, such as fortified beverages and gut-health snacks, increasingly incorporate plant-based fibers, prebiotics, probiotics, and natural vitamins from sources such as pea, oat, and fermentation-derived elements, enabling "food as medicine" claims without synthetic additives. Premium nutrition segments, including protein powders and organic kids' foods, leverage clean-label positioning for premium pricing, expanded retail access, and loyalty among wellness-focused demographics.

- For instance, in November 2020, BENEO launched Remypure S52 P, the first instant functional native rice starch designed specifically for clean-label applications, enabling food manufacturers to create products with simple, recognizable ingredient lists. The new product is a healthy ingredient that supports clean-label claims, aligning with the rising demand for transparency in functional foods.

SEGMENTATION ANALYSIS

By Form

Dry Segment Dominated the Market With Ease of Transportation

On the basis of form, the market is segmented into dry and liquid.

The dry segment dominated the global market in 2025, with a value of USD 32.09 billion, supported by extended shelf life, ease of transportation, and broad usage across bakery, snacks, and dry mixes. Dry forms such as powders excel due to their superior shelf life, lower microbial risks, and ease of storage/transportation compared to liquids, making them ideal for bakery, snacks, and beverages where preservatives are minimized.

The liquid segment is projected to grow at the fastest CAGR of 8.10% over the forecast period, driven by the rising demand for natural liquid flavors, syrups, extracts, and beverage applications.

To know how our report can help streamline your business, Speak to Analyst

By Type

Flours Segment Led the Market with Wide Usage in Bakery & Confectionery Products

Based on type, the market is subdivided into natural colors, natural flavors, sweeteners & starch, flours, malts, and others.

The flours segment dominated the global clean-label ingredients market share, reaching a value of USD 20.32 billion in 2025. The extensive use in bakery, confectionery, and clean-label processed foods are anticipated to drive segment growth. The expansion is driven by the surging demand in bakery, confectionery, and processed foods. Clean-label flours such as organic wheat, rice, and corn flours appealed to manufacturers reformulating for minimal additives amid the expansion of the processed food industry.

The natural colors segment is expected to register the fastest CAGR of 9.06% over the analysis period. The segmental expansion is fueled by the global removal of artificial dyes and increasing adoption in beverages, confectionery, and dairy products.

By Certificates

Non-GMO Segment Leads While Organic Certification Gains Momentum

On the basis of certificates, the market is segmented into organic, non-GMO, gluten-free, and others.

The non-GMO segment led the market in 2025 with a value of USD 17.68 billion, reflecting strong consumer trust and regulatory acceptance. Non-GMO verification supports clean-label claims in products such as flours and flavors. This bolsters the demand for such plant-derived products amid transparency regulations.

The organic segment is projected to grow at a CAGR of 7.95% over the forecast period. This is supported by expanding organic farming acreage and government-backed certification programs.

By Application

Food & Beverages Segment Dominated Owing to Large-scale Reformulation Initiatives

By application, the market spans food & beverages (bakery & confectionery, dairy products, prepared meals/RTE, snacks & cereals, meat & seafood, and others), dietary supplements, and animal feed.

The food & beverages segment dominated the market in 2025, accounting for USD 39.21 billion. The segmental expansion is driven by large-scale reformulation initiatives by multinational food brands. Rising consumer focus on minimally processed items fueled adoption across processed foods. The segment is dominant, supported by technological advancements and reformulations avoiding synthetics.

The dietary supplements segment is projected to grow at a CAGR of 5.63% over the forecast period.

Clean-Label Ingredients Market Regional Outlook

Regionally, the report covers the market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Clean-Label Ingredients Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe led the global market with a value of USD 13.98 billion in 2025 and is projected to grow at a CAGR of 5.85% over 2026–2034. The region’s leadership is underpinned by stringent EFSA regulations on artificial additives, high consumer awareness of food labeling, and strong penetration of organic and non-GMO food products across retail and foodservice channels. European food manufacturers are at the forefront of reformulation, accelerating the demand for natural colors, flavors, starches, and flours.

U.K. Clean-Label Ingredients Market

The U.K. market was valued at approximately USD 2.86 billion in 2025 and is expected to expand at a CAGR of 5.89% during the forecast period. Growth is driven by mandatory front-of-pack labeling, strong consumer preference for additive-free foods, and aggressive reformulation initiatives by leading U.K.-based and multinational food companies to eliminate artificial colors, preservatives, and emulsifiers.

Germany Clean-Label Ingredients Market

The Germany market was valued at USD 2.92 billion in 2025, supported by strong organic food consumption and retail penetration.

North America

The North America market accounted for a value of USD 12.17 billion in 2025 and is projected to grow at a CAGR of 6.37% over the forecast period. The market expansion is supported by FDA-led labeling transparency initiatives, strong organic food consumption, and the widespread adoption of clean-label formulations across packaged foods, beverages, and dietary supplements. Large multinational ingredient suppliers continue to invest in natural ingredient capacity within the region.

U.S. Clean-Label Ingredients Market

The U.S. accounted for a value of approximately USD 9.57 billion in 2025, driven by FDA-aligned labeling norms, organic product expansion, and premium food innovation.

Asia Pacific

Asia Pacific accounted for a valuation of USD 12.96 billion in 2025 and is the fastest-growing region, registering a CAGR of 9.23% over the analysis period. The regional growth is fueled by urbanization, rising disposable incomes, and increasing awareness of food safety.

India Clean-Label Ingredients Market

The India market was valued at USD 2.43 billion in 2025, driven by traditional natural ingredients usage and expanding packaged food markets.

China Clean-Label Ingredients Market

The China market reached a value of USD 5.10 billion in 2025, supported by regulatory tightening and domestic food quality initiatives.

South America and the Middle East & Africa

The South America market accounted for USD 3.79 billion in 2025 and is poised to expand at a CAGR of 7.73% over the forecast period, supported by strong agricultural raw material availability.

The Middle East & Africa market reached a value of USD 2.07 billion in 2025. The market is poised to grow at a CAGR of 5.05% over the analysis period, driven by food security initiatives and premium imported food demand.

South Africa Clean-Label Ingredients Market

The South Africa market was valued at approximately USD 0.59 billion in 2025 and is projected to grow at a CAGR of 4.05% during 2026–2034. The market growth is underpinned by the rising demand for naturally sourced flours, starches, sweeteners, and flavors across bakery, dairy, beverages, and processed food categories.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Portfolio Expansion and Clean-Label Reformulation to Solidify Market Footing

Leading players in the global clean-label ingredients market are increasingly repositioning their portfolios to align with evolving regulatory standards and shifting consumer preferences toward transparency, natural sourcing, and minimal processing. Multinational ingredient manufacturers are investing heavily in clean-label reformulation, replacing artificial colors, flavors, and preservatives with plant-derived, fermentation-based, and enzymatic alternatives that meet clean-label, non-GMO, and organic certification requirements. Strategic partnerships and acquisitions remain a core competitive lever.

Key Players in the Clean-Label Ingredients Market

|

Rank |

Company Name |

|

1 |

Kerry Group |

|

2 |

DSM-Firmenich |

|

3 |

Ingredion Incorporated |

|

4 |

Cargill, Incorporated |

|

5 |

Archer-Daniels-Midland Company (ADM) |

List of Key Clean-Label Ingredients Companies Profiled

- Kerry Group (Ireland)

- DSM-Firmenich (Netherlands/Switzerland)

- Ingredion Incorporated (U.S.)

- Cargill, Incorporated (U.S.)

- Archer-Daniels-Midland Company (ADM) (U.S.)

- Tate & Lyle PLC (U.K.)

- Corbion N.V. (Netherlands)

- Roquette Frères (France)

- Sensient Technologies Corporation (U.S.)

- Givaudan S.A. (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Kemin Food Technologies expanded its Olessence range of natural flavorings with Olessence P Dry for meat and poultry products and Olessence G Liquid for sauces, dips, and bakery items, targeting clean-label demands in Europe and the Middle East & Africa.

- August 2025: Hasegawa launched Hasecitrus using natural flavor technology to stabilize citrus flavors in beverages by protecting against oxidation caused by oxygen, pH shifts, and temperature changes. It enables clean-label, preservative-free products without needing refrigeration or special packaging.

- July 2025: Prodalim, a global supplier of juice solutions and specialty ingredients, launched VivaPro Coloring Foodstuffs and NaturaPro Natural Colors. These upcycled, plant-based solutions meet the rising demand for clean-label colorants in food and beverages.

- February 2024: Ingredion launched NOVATION Indulge 2940, a functional native corn starch recognized as its first clean-label option with gelling and improved mouthfeel properties. This non-GMO starch targets dairy, alternative dairy products, desserts, batters, and breadings, offering a simple "corn starch" label that consumers prefer over hydrocolloids such as gelatin or carrageenan.

- September 2020: Chr. Hansen launched FruitMax Yellow 1000 WSS, a clean-label coloring food derived from turmeric extract. This product delivers a bright yellow hue with minimized off-taste, targeting applications such as ice cream, confectionery, snacks, bakery, and meals.

REPORT COVERAGE

The global clean-label ingredients market report analyzes the market in depth and highlights crucial aspects such as market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the research report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.18% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Form

|

|

By Type · Natural Colors · Natural Flavors · Sweetners & Starch · Flours · Malts · Others |

|

|

By Certificates · Organic · Non-GMO · Gluten-Free · Others |

|

|

By Application · Food & Beverages o Bakery & Confectionery o Dairy Products o Prepared Meals/RTE Meals o Snacks & Cereals o Meat & Seafood o Others · Dietary Supplements · Animal Feed |

|

|

By Region · North America (By Form, Type, Certificates, Application, and Country) • U.S. (By Form) • Canada (By Form) • Mexico (By Form) · Europe (By Form, Type, Certificates, Application, and Country) • Germany (By Form) • Spain (By Form) • Italy (By Form) • France (By Form) • U.K. (By Form) • Rest of Europe (By Form) · Asia Pacific (By Form, Type, Certificates, Application, and Country) • China (By Form) • Japan (By Form) • India (By Form) • Australia (By Form) • Rest of Asia Pacific (By Form) · South America (By Form, Type, Certificates, Application, and Country) • Brazil (By Form) • Argentina (By Form) • Rest of South America (By Form) · Middle East & Africa (By Form, Type, Certificates, Application, and Country) • South Africa (By Form) • UAE (By Form) • Rest of the Middle East & Africa (By Form) |

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 44.97 billion in 2025 and is anticipated to reach USD 83.44 billion by 2034.

The global market is projected to exhibit steady growth at a CAGR of 7.18% over the forecast period.

By form, the dry segment led the market in 2025.

Europe held the largest market share in 2025.

Rising consumer health awareness and regulatory scrutiny are key factors driving market growth.

Kerry Group, DSM-Firmenich, Ingredion Incorporated, Cargill Incorporated, Archer-Daniels-Midland Company (ADM), and others are the leading companies in the market.

The rising demand for ingredient transparency and natural formulations is a key trend in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us