Commercial Aircraft Cabin Pressurization Systems Aftermarket Size, Share & Industry Analysis, By Component (Vacuum System (Vacuum Generation, Measuring and Sensing, Monitoring, and Diagnostic) and Oxygen System Component (Crew Oxygen Supply, Passenger Oxygen Supply, Portable Oxygen Equipment), By Offerings ( MRO Services and Refurbished Parts (PMA and USM)), By Aircraft Family (Airbus A220, Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, & Others), and Regional Forecast, 2025-2045

KEY MARKET INSIGHTS

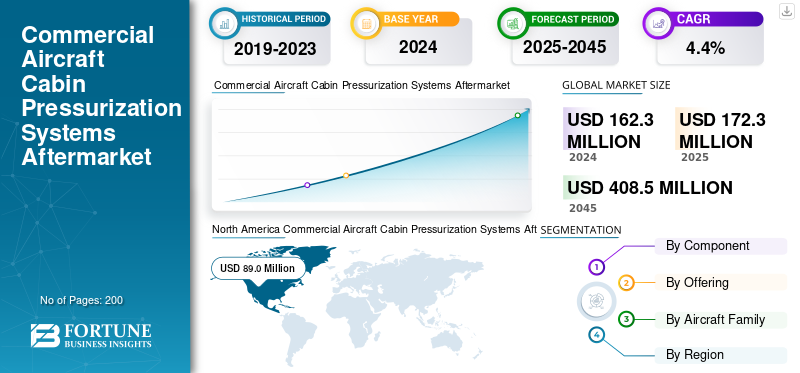

The global commercial aircraft cabin pressurization systems aftermarket size was valued at USD 162.3 million in 2024. The market is projected to grow from USD 172.3 million in 2025 to USD 408.5 million by 2045, exhibiting a CAGR of 4.4% during the forecast period. North America dominated the global commercial aircraft cabin pressurization systems aftermarket with a market share of 54.83% in 2024.

Cabin pressurization systems are crucial for passenger comfort and safety during flight operations at cruising altitude, where there is not enough breathable air to properly oxygenate the body and human function may be impossible. The fourth largest market segment is cabin pressurization systems market, which can be divided broadly into a vacuum/pressurization system and an oxygen system. The vacuum/pressurization system can be further divided into several subcomponents that include vacuum generation units, sensors and diagnostic controllers that help with the control and monitoring system for the use of cabin pressurization. These subcomponents are important to the maintenance of cabin altitude in an acceptable and safe range to avoid hypoxia toward occupants and undue stress to the structure. For all cabin pressurization systems, the oxygen system creates all equipment necessary as an emergency backup for all crew and passengers.

The oxygen system consists of fixed oxygen supply systems that support the crew, portable oxygen bottles for both crew and passengers and breathing masks. Cabin air oxygen system devices typically fall into the maintenance, repair and overhaul (MRO) and refurbished parts segment because airlines and service organizations are interested in taking care of the routine maintenance and compliance inspections, and documenting calibrations, replacing valves and seals, and restoring all equipment (masks, regulators, sensors, etc.) to original equipment manufacturer (OEM) and other acceptable standards established by global authorities or regulators. There exists a global fleet comprised of both dedicated freighter and commercial passenger aircraft, where operators are doing both- adding several and an aging fleet that in need of reliable and low-cost MRO services and refurbished parts to service necessary safety functions and operational compliance especially true in fleet mix operations.

Furthermore, the market encompasses several major players with Collins Aerospace, Honeywell Aerospace, Thales Group, and Safran Electronics & Defense at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

COMMERCIAL AIRCRAFT CABIN PRESSURIZATION SYSTEMS AFTERMARKET KEY TAKEAWAYS

- 2024 Market Size: 162.3 million

- 2025 Market Size: USD 172.3 million

- 2045 Forecast Market Size: USD 408.5 million

- CAGR: 4.4% (2025–2045)

- North America dominated the market with a 54.83% share in 2024.

- Vacuum system is expected to lead the market by component.

- MRO services dominated the market and are projected to hold over 95% share in 2025.

North America

North America valued at USD 89.0 million in 2024, driven by a large commercial fleet and stringent FAA regulations.

Europe

Europe growth is supported by strict EASA safety standards and increasing adoption of certified refurbished components.

Asia Pacific

Asia Pacific rising fleet expansion and growing low-cost carriers are driving demand for MRO and refurbished parts.

U.S.

Strong aftermarket growth is supported by expanding predictive maintenance and pressurization system service capabilities.

Japan

Market growth is supported by increasing commercial aviation activities and rising demand for aircraft maintenance services.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Safety Regulations & Aging Fleets Driving Aftermarket Demand

One of the most significant growth engines for the cabin pressurization systems aftermarket is a positive convergence of stringent safety regulations alongside an aging global commercial aircraft fleet. Pressurization systems are safety critical systems and they create a breathable environment at cruising high altitudes and also protect the aircraft structure. Thousands of narrow-body aircraft (e.g., Airbus A320ceo and Boeing 737NG) for example are nearing midway or end-of-life operating cycles, and as such the airlines need to check, repair, or replace pressurization valves, sensors, oxygen masks, regulators etc. on regular maintenance cycles. The Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) require routine inspection cycles for oxygen systems and pressurization control units that create recurring demand for MRO solutions and refurbished parts. Refurbishment is many time more appealing to operators in emerging markets where the acquisition of new equipment is an onerous capital cost.

- In June 2025, the Australian Transport Safety Bureau highlighted a Gulfstream jet crash linked to a known pressurization fault, emphasizing the dangers of neglecting such systems. This has led to stronger investments in predictive maintenance and condition-based monitoring. With increasing regulatory oversight, airlines are collaborating with OEMs and independent MRO providers to refurbish and modernize these systems. Consequently, the intersection of fleet demographics, regulatory enforcement, and safety imperatives continues to drive consistent growth in this specialized MRO market.

MARKET RESTRAINTS

Technical Limitations & High Downtime to Constrain Market Growth

While the aviation market is exhibiting continuous growth, it nevertheless contends with numerous vectors for restraints. Technical limitations, long downtimes and expensive maintenance cycles are commonplace. More specifically, cabin pressurization and oxygen systems have very tight couplings to avionics systems, pneumatic systems, and environmental control systems which make refurbishment and repair complex challenges. In addition, the preparation of the oxygen and pressure systems includes activities such as retesting sensors, switching valves, and recharging an oxygen cylinder that require a specialized facility and certified personnel therefore delaying and limiting maintenance schedules. It is of particular emphasis that any failure of refurbished components (especially oxygen masks and pressure regulators) not only raises safety concerns for airlines, but also reduces any appetite for airlines to take on third-party refurbished components in lieu of original equipment manufacturer (OEM) supplied components.

MARKET OPPORTUNITIES

Digital Monitoring & Custom Solutions to Create Lucrative Growth Opportunities

MRO market for cabin pressurization systems poses very high upside in digital diagnostics, predictive maintenance and tailored oxygen solutions. The aviation industry is transforming toward IoT-enabled monitoring of cabin air pressure sensors, valves, and oxygen systems, which will allow maintenance providers to view real time health information about components and predict component/component failures early on, improving safety and reducing unplanned downtime, knowing the constituent parts have been allocated properly for function. Thus, the MRO market presents opportunities for value-add services of integrated monitoring and bespoke refurb packages from which MRO peripherals can be added in the future.

- In May 2024, Collins Aerospace introduced its next-generation cabin pressure control system with enhanced health monitoring and longer service intervals, designed for both new aircraft and retrofit markets. Such innovation indicates that the integration of smart systems with traditional MRO and refurbishment processes will become a key growth driver. As sustainability and cost optimization become industry priorities, refurbishment providers that offer digitally enhanced, customized, and regulatory-compliant solutions will capture a significant competitive edge.

MARKET CHALLENGES

High Cost and Regulatory Barriers Present Threats to Aftermarket Providers

High certification costs and bureaucratic regulatory constraints are among the most significant issues that continue to challenge the commercial aircraft cabin pressurization systems aftermarket growth. Although refurbished parts are cost-effective compared to replacing a pressurization or oxygen system, the MRO provider must adhere to FAA, EASA, ICAO, testing, shipping, and certification and documentation for ALL refurbished pressurization/oxygen system parts. The compliance costs are high and are often passed on to the airlines. Refurbished parts, therefore, are more expensive than anticipated. Smaller carriers in Latin America, Africa, and Southeast Asia cannot afford the additional costs, thus limiting the adoption of refurbished parts in the regions that require cost-effective solutions.

COMMERCIAL AIRCRAFT CABIN PRESSURIZATION SYSTEM AFTERMARKET TRENDS

Shift to Smart, Lightweight, and Sustainable Systems to Act as a Major Technological Trend

A significant trend in technology changing this industry is the move to smart, light weight and sustainable pressurization and oxygen systems. Aircraft OEMs and components manufactures are increasingly developing AI-powered monitoring systems for real-time fault detection and automatic pressurization adjustment. This trend is also moving into MRO, where refurbished systems are also adding on digital upgrades and facilitate forward compatibility with newer avionics systems. They are also implementing interactive, lightweight materials (e.g. advanced composites and titanium alloys with possibilities to reduce weight and fuel burn, work to reduce maintenance and operating costs particularly with oxygen cylinders and valves).

- In October 2024, Lufthansa Technik unveiled its enhanced Condition Monitoring Services for cabin systems, which include cabin pressure predictive tracking of components, ensuring minimal disruption and longer maintenance intervals. Similarly, portable oxygen concentrators designed for in-flight use are now being adapted for airline refurbishment cycles. These technological shifts demonstrate a clear movement toward smarter, more efficient, and sustainable solutions that will dominate the cabin pressurization systems aftermarket in the coming decade.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Vacuum System Dominates Due to High Demand for Leak Checks in Older Aircraft

On the basis of component, the market is classified into vacuum system and oxygen system.

The vacuum system dominates the market, this system includes generation units, measurement sensors, and diagnostic controllers, is critical in maintaining safe cabin pressure regardless of altitudes flown. With ongoing safety incidents at the airline level, airlines are leaning more on MRO services for calibration of systems, leak checks and override checks of valves/sensors, especially those operating older fleets. For example, many airlines still operate older models of an aircraft such as an A320ceo or 737NG, both of which occupy a considerable portion of the active global fleet compared to newer aircraft. Extensively operating older aircraft leads to demands for higher maintenance work in this sector. Regulators are also tightening safety standards in the wake of incidents concerning pressurization.

- For instance, in June 2025, reported by the Australian Transport Safety Bureau, that repeated issues were identified with the pressurization of a Gulfstream jet, highlighting the need for systematic and more functioning diagnostics. Predictive-maintenance tools are quickly deployed with user-friendly methods including IoT-enabled pressure monitoring systems. These developments will increase pressurization-refurbishing of pressure controllers and sensors that will continue to develop aftermarket growth.

Oxygen system segment is anticipated to grow at a highest CAGR of 4.7% throughout the forecast period.

By Offerings

Increasing Focus on Preventive Maintenance and Inspection Fuels Growth of MRO Segment

In terms of offerings, the market is categorized into MRO services and refurbished parts.

The MRO services segment captured the largest share of the market in 2024. In 2025, the segment is anticipated to dominate with over 95% share. MRO services account for the majority of cabin pressurization maintenance and repairs, including preventative inspections, leak checking, sensor calibration work, and changing any faulty parts. Airlines are reliant on certified MRO providers to ensure FAA and EASA regulatory requirements and safety standards are met. The expansion of predictive maintenance tools and digital diagnosis are also strengthening this market.

- In February 2025, Lufthansa Technik got MRO approval for cabin systems in Hamburg to handle the demand for MRO services, showing that airlines' increasing reliance on outsourced MRO services are rising as fleets mature and utilization rates go up.

Refurbished parts segment is anticipated to grow at a highest CAGR of 6.5% throughout the forecast period.

By Aircraft Family

To know how our report can help streamline your business, Speak to Analyst

Widespread Usage of Standard Cabin Pressurization Systems MRO & Refurbished Parts Supplemented Airbus A320 Family’s (ceo/neo) Growth

Based on aircraft family, the market is segmented into Airbus A220, Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The airbus A320 family (ceo/neo) segment held the dominating position in 2024. The Airbus A320 family represents one of the largest shares of the global fleet, and it represents a significant contributor to MRO and demand for refurbished parts for cabin pressurization systems. With over 10,000 aircraft delivered and a large percentage still flying, A320ceo models require many possibilities for overhauls of oxygen masks, regulators, and pressurization controllers. Airlines appeal to refurbishments to extended component lifecycle and reduced costs. In January 2025, Airbus entered into a long-term agreement with Safran Aerosystems, to enhance support for A320 oxygen supply and pressurization; this represents the previously outlined growth in aftermarket demand. Because LCCs rely heavily on A320s, so an increase in demand for affordable refurbished parts is expected.

COMAC C919 segment is anticipated to grow at a highest CAGR of 18.7% throughout the forecast period.

Commercial Aircraft Cabin Pressurization Systems Aftermarket Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America & Africa, and the Middle East.

NORTH AMERICA

North America Commercial Aircraft Cabin Pressurization Systems Aftermarket Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant commercial aircraft cabin pressurization systems aftermarket share in 2023 valuing at USD 87.3 million and also took the leading share in 2024 with USD 89.0 million. North America leads cabin pressurization MRO demand due to its large commercial fleet, stringent FAA regulations, and early adoption of predictive maintenance. U.S. carriers prioritize refurbishments to manage rising operating costs. In April 2025, Collins Aerospace expanded its pressurization systems service center in Texas to meet increasing regional demand, underscoring the strong aftermarket growth.

- For instance, in June 2024, Thermo Fisher Scientific Inc. expanded its central laboratory operations in Wisconsin and Kentucky and region with an aim to serve the biotechnology and pharmaceutical and industries.

EUROPE and ASIA PACIFIC

Europe and Asia Pacific are in two very different but complementary market environments which produce a heavy demand for cabin pressurization systems MRO and refurbished parts. Europe has strict and very detailed EASA safety regulations that comply with certified refurbished components as well as predictive diagnostics both for oxygen systems and vacuum systems onboard an aircraft. The Asia Pacific regional dynamic is buoyed by business expansion particularly from low-cost carriers (LCC), such as in India, China and Southeast Asia, that include continued investment and growth to the fleet. Increase in passengers lead to profits; hence, airlines can realize good returns from continuing to operate narrow-body aircraft.

In March 2025, China Southern Airlines awarded Ameco Beijing with more than an USD 100 million cabin systems maintenance contract; indicative of the ever-increasing demand and desire to do business from Airlines in the region. Europe has a program-one fleet while Asia Pacific is growing quickly and seeing massive shifts as well, producing a dual market pull. In Europe, there are COVID regulatory driven refurbishments while Asia Pacific is focused on current fleet utilization. Both markets are relevant segments of MRO due to administration regulation climb, while others are allowing Times/New York Times to take short-term aircraft capital investments, therefore creating a significant portion of the demand on cabin pressurization systems MRO and refurbishment moving into the future.

LATIN AMERICA & AFRICA and MIDDLE EAST

Over the forecast period, Latin America & Africa and the Middle East regions would witness a moderate growth. Latin America & Africa’s market in 2025 is set to record USD 12.8 million as its valuation. In Latin America, the market is cost-driven, as airlines are operating refurbished parts to prolong the lives of aircraft. The Middle East, on the other hand, is benefitting from growing fleets in the Gulf, along with state-backed MRO hubs. In May 2025, Emirates announced they would upgrade the systems on its narrowbody fleet, which created additional demand for support on pressurization components.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings coupled with Strong Distribution Network of Key Companies Supported their Leading Position

The competitive scenario of the commercial aircraft cabin pressurization systems aftermarket is shaped by a group of OEMs, Tier-1 suppliers, and independent MROs. The OEMs Collins Aerospace and Safran Aerosystems are typically strong in this space because they have patent-protected technologies, long-term service contracts, and excellent support capabilities that represent credibility and trust in serving OEM customer requirements.

The independent MROs Lufthansa Technik, AAR Corp, and ST Engineering, are successful as they offer refurbished options at a cost-efficient price point that fits low-cost carriers and regional airlines. HEICO has additionally made progress in this area by supplying FAA apostilled refurbished oxygen and pressurization components at a lower price point. Regional players, including veeding Technic and HAECO, are expanding their capabilities to accommodate growing fleet sizes in emerging markets. There is an element of collaboration and expansion in the competitive structure.

In February 2025, Lufthansa Technik announced that it was upgrading its Hamburg facility to manage increasing demand from the cabin systems discipline. The balance of competitiveness, and overall growth, fostering innovation, while providing value by way of lower-cost post-market.

LIST OF KEY COMMERCIAL AIRCRAFT CABIN PRESSURIZATION SYSTEMS AFTERMARKET COMPANIES PROFILED:

- Collins Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

- Thales Group (France)

- Safran Electronics & Defense (France)

- Liebherr-Aerospace (Germany)

- Moog Inc. (U.S.)

- Parker Aerospace (U.S.)

- Spirit AeroSystems (U.S.)

- ST Engineering Aerospace (Singapore)

- Lufthansa Technik (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Wizz Air integrated Aerogility’s AI maintenance tool for cabin system reliability. Wizz Air adopted Aerogility’s AI-driven digital twin platform to enhance predictive maintenance planning. This includes pressurization sensors and oxygen system diagnostics, reducing downtime and improving operational safety.

- April 2025: AIESL secured EASA certification and announced a wide-body hangar expansion at Thiruvananthapuram. Air India Engineering Services Limited (AIESL) became the first South India MRO to gain EASA Part-145 approval at Thiruvananthapuram Airport. The facility plans to add a new wide-body hangar, enhancing its ability to service advanced cabin systems including pressurization and oxygen supply.

- April 2025: AJW Group expanded its cabin system support portfolio through new airline contracts. At MRO Americas 2025, AJW Group signed a power-by-the-hour deal with Air Transat for A320-series components and partnered with Inter-Tec Aero for cabin pressurization and oxygen system certification services.

- April 2025: HAECO Americas launched drone-assisted MRO inspections for cabin and structural systems. HAECO Americas introduced drone-powered aircraft inspections equipped with computer vision technology. The innovation improves efficiency in identifying structural and cabin pressurization system issues during maintenance cycles.

- March 2025: Hindustan Aeronautics Ltd (HAL) overhauled its first A320neo for IndiGo at its Nashik facility, followed by Embraer E-175 and E-145 projects in April–May. This marks HAL’s major push into civil aircraft MRO, with capacity to deliver over a dozen A320 overhauls annually under DGCA and EASA compliance.

- March 2025: Lufthansa Technik posted its highest-ever revenues supported by cabin system MRO demand. Lufthansa Technik achieved record first-quarter financial results in 2025, driven by surging demand for MRO services, including cabin systems and pressurization components. The company continues to ensure management systems to cater to cost challenges and supply chain pressures.

- February 2025: IndiGo signed an agreement for a large MRO hub at Bengaluru airport. IndiGo announced a USD 126.49 million (₹1,100 crore) investment to establish a new MRO complex at Bengaluru International Airport. Spanning 31 acres, the facility will feature four hangars designed to support A320, A321XLR, and A350 fleets with advanced cabin pressurization system servicing.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 4.4% from 2025-2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component, Offering, Aircraft Family and Region |

|

By Component |

· Vacuum System o Vacuum Generation o Measurement & Sensing o Monitoring & Diagnostics · Oxygen System o Crew Oxygen Supply o Passenger Oxygen Supply o Portable Oxygen Equipment |

|

By Offering |

· MRO Services · Refurbished Parts o PMA o USM |

|

By Aircraft Family |

· Airbus A220 · Airbus A320 Family (ceo/neo) · Airbus A330 (ceo/neo) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 162.3 million in 2024 and is projected to reach USD 408.5 million by 2045.

In 2024, the market value stood at USD 45.1 million.

The market is expected to exhibit a CAGR of 4.4% during the forecast period of 2025-2045.

The MRO services segment led the market by offering.

Safety regulations & aging fleets are the key driving factors.

Collins Aerospace (U.S.), Honeywell Aerospace (U.S.), and Thales Group (France) are some of the prominent players in the market.

North America dominated the market in 2024 in terms of share.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us