Decoy Flares Market Size, Share & Industry Analysis, By Type (Pyrotechnic Flares, Pyrophoric Flares, Infrared Decoy Flares, Spectral Flares, and Others), By Platform (Aircraft (Fixed Wing Combat Aircraft, Rotary Wing Aircraft, Transport & Special Mission Aircraft, and Others) and Naval (Surface Combatants, Patrol Vessels, and Others)), By Storage Configuration (Cartridge Type Flares, Modular Magazines, and others), By Technology (Conventional IR Flares, Spectral/Multi-Spectral Flares, Kinematic Flares, and Others), By End User (Army, Air Force, and Navy), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

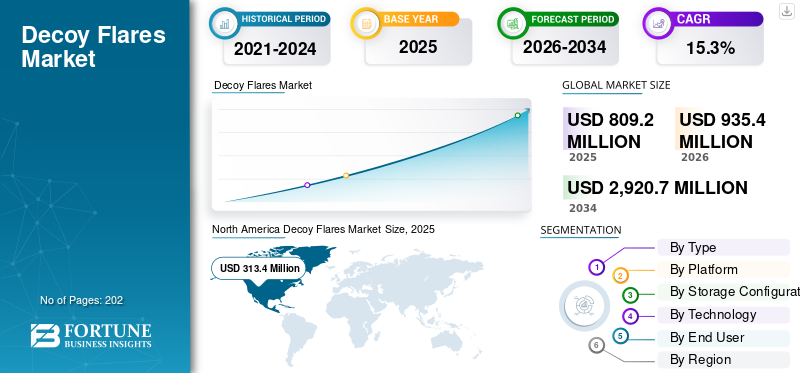

The global decoy flares market size was valued at USD 809.2 million in 2025. The market is projected to grow from USD 935.4 million in 2026 to USD 2,920.7 million by 2034, exhibiting a CAGR of 15.3% during the forecast period. North America dominated the global decoy flares market with a market share of 38.72% in 2025.

Decoy flares are expendable devices carried by military aircraft or ships to protect them from heat‑seeking missiles. When a missile is detected, the platform ejects several burning flares that produce an intense infrared (heat) signature, often hotter than the engines. They are integrated into the platform’s defensive‑aids suite and are fired automatically or manually when a missile threat is detected. Modern warfare countermeasures increasingly rely on advanced decoy flares integrated with threat detection and warning systems to protect aircraft against evolving infrared-guided missile threats. In many new military programmes, decoy flares are managed as part of a defensive aids suite, working alongside tactical deception equipment such as towed decoys and jammers to create layered survivability for frontline air platforms.

Major players in the industry include Rheinmetall, BAE Systems, Chemring/Armtec, Lacroix Defense, and Elbit Systems, among others. Rheinmetall supplies qualified IR flare systems for European and NATO fast jets, transports, and helicopters. BAE Systems and Chemring/Armtec provide broad portfolios of NATO‑standard IR flares for AN/ALE‑47 and other dispensers on U.S. and allied aircraft.

Download Free sample to learn more about this report.

Decoy Flares MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 809.2 Million

- 2026 Market Size: USD 935.4 Million

- 2034 Forecast Market Size: USD 2,920.7 Million

- CAGR: 15.3% from 2026–2034

- North America dominated the decoy flares market with a 38.72% share in 2025.

- The pyrotechnic flares segment held the largest market share due to cost-effective and high-temperature burn efficiency.

- The air force segment accounted for the dominant end-user share driven by widespread fighter jet deployment and survivability systems.

North American

North America led the market with USD 313.4 Million in 2025, supported by large combat aircraft fleets and continuous modernization programs.

Europe

Europe is witnessing strong growth driven by NATO-standard fleet upgrades and increased defense spending post Russia–Ukraine conflict.

Asia Pacific

Asia Pacific is emerging as a high-growth region due to rising defense budgets and expansion of air and naval forces in China, India, Japan, and South Korea.

U.S.

Market growth is driven by modernization of combat aircraft fleets and rising adoption of advanced spectrally tuned flare countermeasures.

Japan

Increasing investment in air and naval defense systems is supporting adoption of advanced decoy flare technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rise in Defense Expenditure is Expected to Drive Market Growth

A major direct driver for the market growth is the rise in global defense expenditure including air and naval modernization. For instance, the world military expenditure rose to about USD 2.7 trillion in 2024, which is an up of 9.4% from 2023. As the defense budget increases, the governments of various countries allocate more funding to upgrade combat aircraft and surface fleets with modern self‑protection suites. Higher defense spending also increases the procurement of consumption and creates steady replacement demand. Moreover, rise in the budget makes it easier for military forces to move from basic conventional flares to more advanced spectral and CCM‑resistant products.

MARKET RESTRAINTS

Regulatory and Export-Control Constraints to Limit Market Expansion

A key restraint in the market is the stringent export controls and safety regulations. Many governments classify thermal decoy devices and associated components as sensitive military items. This can delay contract execution, restrict access to certain high‑growth regions, and make demand more volatile. Moreover, stricter rules on explosives storage, range safety, and environmental impact increase the compliance and certification costs for both manufacturers and operators which are expected to hamper the market growth.

MARKET OPPORTUNITIES

Retrofit and Life‑Extension of Aircraft & Naval Fleet Presents Opportunities for the Market Growth

The air forces and navies across the globe are keeping older platforms in service longer while upgrading their avionics and self‑protection suites, rather than replacing the fleets. This creates demand for modern, dispenser‑compatible flares especially spectral, kinematic, and multi‑event designs that can significantly enhance survivability without major structural modifications. Decoy flare manufacturers supply advanced flares on legacy dispensers, provide integration of advanced countermeasure systems in new fleet which is expected to present lucrative opportunities for the market.

MARKET CHALLENGES

Rapidly Advancing Missile Seeker Technology Acts a Challenge for the Market Growth

A key market challenge in the decoy flares market growth is rapidly advancing missile seeker technology. Modern infrared-guided missile defense seekers and imaging seekers use sophisticated counter‑countermeasure (CCM) algorithms, multi‑band sensing, and trajectory discrimination, which can quickly erode the effectiveness of existing flare inventories. This forces manufacturers to frequently invest in high‑cost R&D cycles to develop spectral, kinematic, and multi‑event flares that remain credible against new threat generations.

DECOY FLARES MARKET TRENDS

Strategic Partnerships and Collaborations Is a Significant Trend in the Market

Strategic partnerships and collaborations are emerging as a key trend in the market as stakeholders seek to deliver integrated, platform‑level protection solutions. System integrators, flare manufacturers, and electronic warfare systems providers increasingly form long‑term agreements. They collaborate jointly to develop, qualify, and market complete self‑protection suites for specific aircraft and naval programs, which is propelling market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Cost-Effective Integration into Existing Fighter Fleets Drives Pyrotechnic Flares Segment Growth

By type, the market is segmented into pyrotechnic flares, pyrophoric flares, infrared decoy flares, spectral flares, and others.

The pyrotechnic flares segment holds the largest decoy flares market share due to advantages of such flares including high-temperature burns that effectively lure early IR-guided missiles. Militaries favor them for their cost-effective integration into existing fighter fleets during upgrades. Growing demand for advanced pyrotechnic decoys to protect military aircraft against modern infrared-guided missile threats drives segment growth.

- For instance, in, September 2025, Germany’s Bundeswehr awarded Rheinmetall a USD 54.4 million contract to deliver more than 470,000 Birdie (Bispectral Infrared Decoy) aircraft pyrotechnic protection flares.

Spectral flares segment is fastest growing segment and is projected to grow at a highest CAGR. The factors responsible for segment growth is rapid expansion of spectral flares for advanced threats and missile seekers. They produce cleaner burns with less smoke for stealthier operation which drives their demand.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Growing Procurement & Deliveries of Fifth Generation Aircraft Drives Aircraft Segment Growth

Based on platform, the market is segmented into aircraft and naval.

Aircraft account for the largest market share due to surging deliveries of fifth-gen fighters which requires dispenser upgrades. Fleet modernization across NATO allies boosts flare-compatible systems which is also fueling the segment growth. Companies are focusing on advancement of flares for combat jets, rotary-wing aircraft, and large transport/special-mission aircraft.

- For instance, in December 2025, Lacroix Defense unveiled a new generation of expendable countermeasures and multi-spectral and combined pyrotechnic decoys, along with a steerable dispenser and smart countermeasures interface.

Naval segment is expected to have a fastest growth rate owing to increasing demand for chaff flares for protecting ships and vessels against modern anti-ship and MANPADS-class missiles during ASW and surface warfare missions. Smaller surface combatants and patrol boats in Indo-Pacific are adding compact and modular flare launchers as they operate closer to hostile shore-based missile batteries.

By Storage Configuration

Emerging UAV Swarm Operations Requiring Advanced Flares Drive Cartridge Type Flares Segment Growth

Based on storage configuration, the market is segmented into cartridge type flares, modular magazines, and multi-row & directional magazines.

Cartridge type flares segment dominates the market as they are gaining traction owing to their standardized dimensions that fit dispensers on both older jets such as the F-16 and newer UAVs. Emerging UAV swarm operations in contested areas demand high-volume, quick-dispense cartridges to sustain persistent threats which is driving segment growth.

Modular magazines are forecasted to be the fastest‑growing storage configurations, driven by bolt-on designs that adapt to rotary-wing helicopters such as the Apache or fixed-wing fighters. As they hold more flares than fixed units which is driving their demand during high risk zones and patrolling areas.

By Technology

Cost Effectiveness & Fleet Sustainment Programs Drive Conventional IR Flares Segment Growth

Based on technology, the market is segmented into conventional IR flares, spectral/multi-spectral flares, kinematic flares, multi-event & high capacity flares, and others.

Conventional IR flares segment dominates the market as they sustain growth through their low unit costs, making them ideal infrared countermeasures for portable MANPADS like the Igla or Stinger. Ongoing replacements for legacy jets drives consistent demand for conventional flares during fleet sustainment programs.

Spectral or multi-spectral flares are forecasted to be the fastest‑growing segment as they emit signatures that match aircraft engine plumes across IR and UV bands, fooling advanced seekers on missiles. Moreover, the widespread expansion of smart, imaging IR missiles from Russia and China forces upgrades on platforms such as the Eurofighter and Rafale which accelerates the segment growth.

By End User

Fighter Jet Vulnerability to MANPADS in Contested Low-Level Missions Areas Support Air Force Segment Growth

Based on end user, the market is segmented into army, air force, and navy.

Air force segment dominates the market as the as fighter jets remain vulnerable to portable MANPADS in low-level missions over contested areas. Moreover, air force equip integrated chaff-flare pods on jets such as F-15s and Su-30s for automated defense bursts during high-risk situation. The airforce sector invests heavily in the military aviation defense systems for combat aircraft protection.

- For instance, in September 2022, Kilgore Flares and Armtec Countermeasures received a USD 225 million IDIQ contract from the U.S. Department of Defense to produce MJU-61A/B infrared flare countermeasures for the U.S. Air Force

Navy is forecasted to be the fastest‑growing end user, driven by development of advanced anti-ship missiles with sophisticated IR and multi-spectral seekers. This is encouraging navies to strengthen navy capabilities with the integration of aircraft survivability equipment such as decoy flares and related expendables.

- For instance, in April 2024, The UK Ministry of Defence awarded a USD 180.75 million contract to Systems Engineering & Assessment (SEA), along with Chess Dynamics and Frazer-Nash Consultancy, to supply the Royal Navy with new Trainable Decoy Launcher systems.

Decoy Flares Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

North America

North America Decoy Flares Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America region holds the largest share in the market, valued at USD 313.4 million in 2025, and is expected to grow at a significant CAGR during the forecast period. The growth of the market in the region is driven by large combat and support aircraft fleet and sustained investment in aircraft and ship self‑protection upgrades. Ongoing procurement of fifth‑generation fighters, tanker/transports and rotary‑wing platforms drives the growth of the market in the region.

- For instance, in January 2025, U.S awarded a contract to Boeing worth USD 7.15 billion including a USD 4.68 billion firm-fixed-price contract from the Army to deliver new-build AH-64E Apache attack helicopters, Longbow crew trainers.

In the U.S., the market growth is supported by continuous modernization of legacy and next‑generation combat aircraft fleets, which require upgraded expendable countermeasures suites. Moreover, the rising sophisticated infrared-guided threats pushes the country to adopt more advanced, spectrally tuned flare formulations driving further market growth.

Europe

Europe is witnessing accelerated growth driven by higher defense spending following the Russia Ukraine conflict and a wave of fighter, transport, and helicopter modernization programmes across NATO and non‑NATO states. As European air forces integrate new aircraft such as F‑35 and upgraded Eurofighter/Rafale fleets and navies field modern frigates and OPVs, there is a strong pull for qualified, NATO‑standard flare systems and naval decoy system which is anticipated to fuel market demand in the region.

- For instance, in March 2025, Rafael Advanced Defence Systems and Elbit Systems secured a four‑year contract to equip five new NATO European frigates with an integrated Naval Decoy Control & Launching System.

Asia Pacific

Asia Pacific is emerging as one of the fastest‑growing regions, reflecting increases in military expenditure and rapid expansion of air and naval power in China, India, Japan, South Korea, and several Southeast Asian states. Regional tensions in the Western Pacific and Indian Ocean are pushing these countries to equip large and increasingly modern aircraft fleets and surface combatants with robust missile countermeasure systems, driving demand for both basic IR flares and more sophisticated spectral/kinematic variants. Countries in the region are investing heavily in deception and survivability tools for aircrafts.

- For instance, in October 2025, South Korean firm Seawolf Marine developed inflatable F-35 defense decoy systems that can be rapidly deployed in about 10 minutes by two personnel. The radar decoys emit radar and infrared signatures and can be remotely controlled to simulate realistic flight patterns.

Latin America and Middle East & Africa

Latin America is a smaller but steady market, where decoy flare demand is closely tied to selective fleet recapitalization rather than broad‑based rearmament. A limited number of countries operate modern fighter, light‑attack and transport aircraft with integrated airborne countermeasure dispensers, and flare procurement tends to track individual aircraft upgrade or replacement projects. Middle East & Africa market is driven mainly by Middle Eastern states that operate advanced fighter, helicopter and naval fleets in a persistent high‑threat missile environment.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation, Platform Integration, and Safety Focused Upgrades Drive Competitive Dynamics in the Market

The decoy flares market is characterized by companies including Rheinmetall (Germany), BAE Systems (U.S./U.K.), Chemring/Armtec (U.K./U.S./Canada), Lacroix Defense (France), Elbit Systems (Israel/U.K.) , among others and a limited number of regional specialists. These firms supply infrared decoy flares qualified for standard aircraft and naval dispensers, spanning conventional IR rounds, spectral/multi‑spectral and kinematic flares, multi‑event/high‑capacity cartridges, and naval IR decoy munitions integrated with soft‑kill suites.

To strengthen their market positions, leading players are investing in advanced spectral and CCM‑resistant flare designs, improved kinematic performance, and low‑smoke, safety‑enhanced compositions, often co‑developed with defensive‑aids system integrators and platform OEMs. Competitors are also focusing on advanced countermeasure dispensing systems CMDS tailored to standard dispenser formats and current MANPADS threats.

LIST OF KEY DECOY FLARES COMPANIES PROFILED

- Rheinmetall AG (Germany)

- Chemring Group Plc (U.K.)

- Armtec Defense Technologies (U.S.)

- BAE Systems Plc (U.K.)

- SaaB (Sweden)

- LACROIX Defense (France)

- Elbit Systems Ltd. (Israel)

- Leonardo S.p.A. (Italy)

- MBDA (France)

- Owen International (Australia)

KEY INDUSTRY DEVELOPMENTS

- July 2025: The U.S. Navy announced its plans to procure up to 6,000 Active Expendable Decoys (AEDs) and active protection measures from Leonardo UK to equip its F-35 and F/A-18 aircraft.

- March 2025: The US State Department approved a possible USD 165 million Foreign Military Sale to Australia for aircraft countermeasures.

- August 2024, The U.S. Air Force awarded Armtec Countermeasures a contract worth USD 11.7 million for RR-196 countermeasure flares/chaff for the F-22 Raptor.

- January 2024, Germany’s Bundeswehr awarded Rheinmetall a USD 58.56 million contract to supply over 470,000 Birdie-series infrared decoy flares between 2023 and 2029. The IR-Birdie 118 BS and 218 BS systems will enhance aircraft protection by emitting heat signatures that divert infrared-guided missiles away

- January 2024, The U.S. Department of Defense has awarded a USD 31 million contract modification to Chemring Australia to supply 19,570 MJU-68/B infrared decoy flares for F-35 aircraft across multiple allied nations.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.3% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Type, By Platform, By Storage Configuration, By Technology, By End User, and Region |

|

By Type |

· Pyrotechnic Flares · Pyrophoric Flares · Infrared Decoy Flares · Spectral Flares · Others |

|

By Platform |

· Aircraft o Fixed Wing Combat Aircraft o Rotary Wing Aircraft o Transport & Special Mission Aircraft o Unmanned Aerial Vehicles (UAVs) o Others · Naval o Surface Combatants o Patrol Vessels o Others |

|

By Storage Configuration |

· Cartridge Type Flares · Modular Magazines · Multi-row & Directional Magazines |

|

By Technology |

· Conventional IR Flares · Spectral/Multi-Spectral Flares · Kinematic Flares · Multi-event & High Capacity Flares · Others |

|

By End User |

· Army · Air Force · Navy |

|

By Region |

· North America (By Type, By Platform, By Storage Configuration, By Technology, By End User, and Country) o U.S. (By End User) o Canada (By End User) · Europe (By Type, By Platform, By Storage Configuration, By Technology, By End User, and Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By Type, By Platform, By Storage Configuration, By Technology, By End User, and Country) o China (By End User) o Japan (By End User) o India (By End User) o South Korea (By End User) o Rest of Asia Pacific (By End User) · Latin America (By Type, By Platform, By Storage Configuration, By Technology, By End User, and Country) o Brazil (By End User) o Mexico (By End User) o Rest of Latin America (By End User ) · Middle East & Africa (By Type, By Platform, By Storage Configuration, By Technology, By End User, and Country) o UAE (By End User) o Saudi Arabia (By End User) o Rest of Middle East & Africa (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 809.2 million in 2025 and is projected to reach USD 2,920.7 million by 2034.

In 2025, the market value stood at USD 313.4 million.

The market is growing at a CAGR of 15.3% during the forecast period.

The pyrotechnic segment led the market by type in 2025.

The key factors driving the market are growth of market are rising demand for strong connectivity in remote and underserved areas.

Rheinmetall AG (Germany), Chemring Group Plc (UK), Armtec Defense Technologies (U.S.)and among others are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us