Digital Phase Shifters Market Size, Share & Industry Analysis, By Channel Count (Single Channel and Multi-Channel), By Application (Radar Systems, Electronic Warfare Systems, Communication Systems, Test and Measurement Equipment, and Aerospace and Defense), By Output Power (Low Power (below 1W), Medium Power (1-10W), and High Power (above 10W)), By Phase Shift Type (Analog Phase Shifter, Digital Phase Shifter, and Time Delay Phase Shifter), By Frequency Range (0-3 GHz, 3-6 GHz, 6-12 GHz, 12-18 GHz, 18-26 GHz, and Above 26 GHz) and Regional Forecast, 2026-2034

Digital Phase Shifters Market Size and Future Outlook

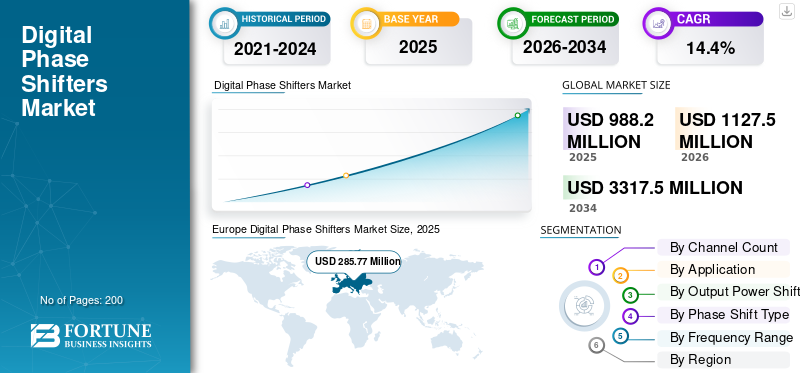

The global digital phase shifters market size was valued at USD 988.2 million in 2025. The market is projected to grow from USD 1,127.5 million in 2026 to USD 3,317.5 million by 2034, exhibiting a CAGR of 14.4% during the forecast period. Europe dominated the digital phase shifters market, with a market share of 28.86% in 2025.

Digital phase shifters are a critical segment of the RF and microwave electronics market, enabling precise control of signal phase in applications such as phased array antennas, radar systems, and telecommunications. These devices adjust the phase of RF signals digitally, offering advantages over analog counterparts, such as higher accuracy, programmability, and immunity to temperature variations, making them ideal for beamforming in 5G base stations and satellite communications. The market thrives on surging demand from defense sectors for advanced radar and electronic warfare, where beam steering enhances target tracking and jamming resistance. In aerospace, they support avionics and satellite payloads, while automotive ADAS leverages them for radar-based collision avoidance and adaptive cruise control.

Key players includes Analog Devices, Inc. (U.S.), Murata Manufacturing Co., Ltd. (Japan), Qorvo, Inc. (U.S.), Texas Instruments Incorporated (U.S.), NXP Semiconductors (Netherlands), and Mercury Systems (U.S.), dominating through RF expertise and phased array innovations.

Download Free sample to learn more about this report.

Digital Phase Shifters Market Key Takeaways

- 2025 Market Size: USD 988.2 million

- 2026 Market Size: USD 1,127.5 million

- 2034 Forecast Market Size: USD 3,317.5 million

- CAGR: 14.4% from 2026–2034

- Europe dominated the digital phase shifters market with a 28.86% share in 2025.

- The multi-channel segment is projected to grow at a 14.2% CAGR during the forecast period.

- The electronic warfare systems segment is expected to expand at a 15.7% CAGR over the forecast period.

Europe

Europe led the market with USD 285.27 million in 2025.

North America

North America is projected to reach USD 351.2 million in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 391.2 million in 2026 at a 15.1% CAGR.

U.S

The market is estimated at USD 304.3 million in 2026.

Japan

The market is projected to reach USD 66.0 million in 2026.

Read More

DIGITAL PHASE SHIFTERS MARKET TRENDS

Beamforming Innovations is Shaping Evolution in Market

A shift toward integrated, programmable architectures enhances adaptability in phased array antennas and software-defined systems. Focus on miniaturization and power efficiency supports deployment in compact devices such as IoT and wearables. Expansion into augmented reality and AI-driven adaptive control broadens applications. Advanced materials improve reliability for high-frequency telecom and radar uses.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for 5G and Advanced Wireless Technologies to Drive Market Growth

Proliferation of 5G and advanced wireless technologies necessitates precise phase control for beamforming, driving demand for digital phase shifters in telecommunications infrastructure. Advancements in radar systems for defense and satellite communications require reliable beam steering, further accelerating adoption. Growth in automotive ADAS and electronic warfare applications increases demand for efficient RF signal management, fostering market momentum. Semiconductor miniaturization reduces costs, enabling broader integration across sectors. This drives digital phase shifters market growth.

MARKET RESTRAINTS

High Costs Limit Accessibility Which Hinders Market Growth

Elevated manufacturing expenses for sophisticated components restrict adoption by smaller firms and emerging markets. Complex production processes increase barriers to scalability and entry. Supply chain vulnerabilities exacerbate pricing pressures, hindering widespread deployment. These factors consolidate the market among established players with deep resources.

MARKET OPPORTUNITIES

Infrastructure, Autonomy, Innovation, and Policy Shifts Provide Growth Opportunities

Infrastructure buildouts in developing regions for telecom and defense create demand for high-frequency components. Automotive autonomy and space programs in the Asia Pacific and Latin America offer untapped potential. Technological material innovations enable cost-effective, high-performance solutions. Policy investments and geopolitical shifts favor growth in strategic applications.

MARKET CHALLENGES

Design Complexities Hinder Performance and Challenge the Market Growth

Achieving high accuracy at elevated frequencies requires intricate engineering, which can lead to signal loss and phase errors. Integration into existing systems poses compatibility issues and extended development cycles. Environmental sensitivities such as temperature fluctuations compromise reliability. Lack of industry standardization complicates interoperability and innovation.

Segmentation Analysis

By Channel Count

Single Channel Segment Dominates Due to Legacy Platforms and Cost-Sensitive Systems

Based on channel count, the market is segmented into single channel and multi-channel.

The single channel segment is anticipated to account for the largest market share. Demand remains steady for labs, legacy radar upgrades, and cost-sensitive platforms that need simple beam control. Buyers prefer quick integration, low BOM, and deterministic calibration where multi-channel complexity isn’t justified.

The multi-channel segment is anticipated to rise with a CAGR of 14.2% over the forecast period.

By Application

Radar Systems Segment is Expanding Due to AESA Modernization and Counter-UAS

Based on application, the market is segmented into radar systems, electronic warfare systems, communication systems, test and measurement equipment, and aerospace and defense.

In 2025, the radar systems segment dominated the global market. The growth of this segment is driven by AESA modernization, counter-UAS, air defense, naval surveillance, and fire-control upgrades. Digital phase shifting enables agile beams, low sidelobes, and fast track updates under dense threat environments.

The electronic warfare systems segment is projected to grow at a CAGR of 15.7% over the forecast period.

By Output Power

Strong Demand from Phased-Array and SATCOM Applications Boosts Medium Power (1-10W) Segment Growth

Based on output power, the market is segmented into low power (below 1W), medium power (1-10W), and high power (above 10W).

The medium power (1-10W) segment is anticipated to hold a dominant market share over the forecast period. Demand is pulled by phased-array front-ends, balancing range and thermal limits. It fits most AESA tiles, SATCOM terminals, and high-power radios where efficiency, linearity, and reliability matter.

The high power (above 10W) segment is projected to grow at a high CAGR of 15.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Phase Shift Type

Digital Phase Shifter Demand is rising Due to Modern Arrays are Moving to Software-Defined Beamforming

Based on phase shift type, the market is segmented into analog phase shifter, digital phase shifter, and time delay phase shifter.

The digital phase shifter segment dominated with the largest market share. Demand accelerates as systems shift to software-defined beamforming and closed-loop calibration. Digital control improves repeatability, production yield, and field reconfiguration, which are critical for AESA radar, EW, and multi-beam SATCOM.

In addition, delay phase shifter segment is expected to grow at a CAGR of 14.2% during the forecast period.

By Frequency Range

6–12 GHz Demand is Growing Due to X-band-centric Radar and Sensing Programs are Scaling

Based on frequency range, the market is segmented into 0-3 GHz, 3-6 GHz, 6-12 GHz, 12-18 GHz, 18-26 GHz, and above 26 GHz.

The 6-12 GHz segment held the largest digital phase shifters market share. X-band dominates many radars and sensors, while mid-band SATCOM and defense links expand. This range balances antenna size, propagation, and resolution, driving volume deployments.

In addition, above 26 GHz are projected to grow at a CAGR of 17.9% during the forecast period.

Digital Phase Shifters Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Digital Phase Shifters Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2024, valued at USD 252.04 million, and also maintained the leading share in 2025, with USD 285.27 million. Demand is pulled by air-defense recapitalization, AESA upgrades, and a sovereign capability push across radar, EW, and secure communications. Export-control realities and supply-chain localization are increasing domestic sourcing and multi-band phased-array deployments.

U.K. Digital Phase Shifters Market

The U.K. market is estimated to reach a valuation of USD 63.0 million in 2026, representing a CAGR of 14.1% during the forecast period. Demand is driven by air and maritime surveillance upgrades, electronic protection needs, and allied interoperability requirements. Procurement favors proven suppliers, but phased-array modernization and secure communications sustain steady digital phase shifter adoption.

Germany Digital Phase Shifters Market

Germany’s market is projected to reach around USD 68.9 million in 2026. Demand rises with integrated air and missile defense, ground-based radar upgrades, and secure tactical communications. A strong industrial base and emphasis on sovereign supply chains push multi-channel architectures and higher-performance RF front-ends.

North America

North America is estimated to reach USD 351.2 million in 2026 and secure the position of second largest region in the market. Demand for digital phase shifters is driven by sustained defense radar/EW modernization, resilient SATCOM procurement, and high-volume integration into AESA platforms. Mature suppliers, rapid prototyping culture, and program funding stability keep multi-channel digital adoption accelerating.

U.S. Digital Phase Shifters Market

Based on North America’s strong input and the U.S. dominance in the region, the U.S. market is set to reach USD 304.3 million in 2026, accounting for roughly 14.7% of global sales. Demand is anchored by large AESA radar and EW programs, upgrades across naval/air platforms, and high-end SATCOM terminals. Advanced test infrastructure and rapid fielding cycles favor digital, multi-channel, tightly calibrated phase control.

Asia Pacific

Asia Pacific is projected to record a growth rate of 15.1% during the forecast period, which is the third highest among all regions, and reach a valuation of USD 391.2 million by 2026. Demand is expanding fastest as regional militaries scale up air and maritime surveillance, counter-UAS, and electronic attack capabilities. Strong manufacturing ecosystems, rising SATCOM adoption, and aggressive modernization timelines are accelerating digital phase shifter volumes and higher-frequency adoption.

Japan Digital Phase Shifters Market

The Japan market share in 2026 is estimated at around USD 66.0 million, recording a CAGR of 14.4% during the forecast period. Demand is driven by maritime-domain awareness, air-defense radar refresh, and secure communications modernization. High reliability standards and advanced electronics ecosystems favor compact, low-drift digital phase shifters for dense phased-array architectures.

China Digital Phase Shifters Market

China’s market is projected to be one of the largest in the Asia Pacific, with 2026 revenues estimated at around USD 140.5 million. Demand scales through the rapid deployment of phased-array radars, electronic warfare systems, and SATCOM terminals. Large domestic manufacturing capacity and high system volumes accelerate multi-channel integration and expansion into higher-frequency ranges.

India Digital Phase Shifters Market

The Indian market in 2026 is estimated at around USD 72.8 million. Demand accelerates from indigenous radar/EW programs, air-defense expansion, and growing SATCOM ground segments. Make-in-country procurement and platform modernization push local integration of digital phase shifters across multiple frequency bands.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. These regions are expected to experience moderate growth in this market during the forecast period. The Middle East & Africa and Latin America market is expected to reach a valuation of USD 33.7 million and USD 26.8 million in 2026. Demand is driven by border security, air-defense procurement, and emerging SATCOM ground infrastructure. Buying is program-based and uneven, but rising threat perception and localized assembly partnerships steadily expand phased-array deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Accelerate Innovation While Security Needs Outpace Solutions

Analog Devices, Inc. (U.S.) leads with precision RF integrated circuits and programmable phase shifters for radar and 5G beamforming, leveraging decades of analog expertise. Murata Manufacturing Co., Ltd. (Japan) excels in compact ceramic-based components, ideal for telecom infrastructure and automotive radar modules. Qorvo, Inc. (U.S.) dominates high-power GaAs/GaN solutions for defense and satellite applications, emphasizing low-loss performance. Texas Instruments Incorporated (U.S.) offers cost-effective, versatile drivers integrated into broader DSP platforms for phased arrays. NXP Semiconductors (Netherlands) focuses on automotive-grade and IoT connectivity shifters with robust safety features. Mercury Systems (U.S.) specializes in ruggedized systems for aerospace and electronic warfare, providing turnkey radar subsystems. These firms drive innovation through R&D, partnerships, and vertical integration, capturing major market share via superior phase accuracy and scalability.

LIST OF KEY DIGITAL PHASE SHIFTERS COMPANIES PROFILED

- Analog Devices, Inc. (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- Qorvo, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- NXP Semiconductors (Netherlands)

- Mercury Systems (U.S.)

- MACOM Technology Solutions (U.S.)

- Crane Aerospace & Electronics (U.S.)

- Narda-MITEQ (U.S.)

- Astra Microwave Products Limited (India)

KEY INDUSTRY DEVELOPMENTS

- February 2026: OCCAR signed a co-funding agreement for REACT II, an electronic attack program led by Indra, backed by seven European nations.

- September 2025: Safran Electronics & Defense and Rheinmetall Electronics signed a new framework agreement at DSEI London to deepen long-term cooperation, simplify procurement, and support upcoming joint projects.

- August 2025: BEL and Centum Electronics signed an MoU to jointly design, develop, and manufacture advanced electronic modules, subsystems, and systems for defense, focused on EW, radar, and secure military communications.

- February 2025: Rafael and Centum Electronics signed a Teaming Agreement to work together on spectrum dominance, spectrum situational awareness, and AI-based intelligence/decision-support suites for the Indian Armed Forces.

- December 2024: Mitsubishi Electric entered a MoU with Bharat Electronics Limited (BEL) and MEMCO Associates (India) to explore joint business opportunities in selected defense and space areas.

REPORT COVERAGE

The digital phase shifters market report lays out a clear snapshot of market size and forward forecasts across all major segments. It breaks down the demand engine what’s speeding up adoption, what’s slowing it down, where the biggest opportunities are, and which trends are likely to steer the market through the forecast window. To explain competitive behavior, it applies Porter’s Five Forces to gauge rivalry intensity and the bargaining power of both suppliers and buyers. It also assesses retrofit and upgrade cycles that can lift aftermarket revenues, and tracks key competitive actions such as partnerships, strategic deals, mergers, and acquisitions, and other material developments. The report contrasts regional presence across major geographies and concludes with a competitive landscape that includes estimated.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.4% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Channel Count, By Application, By Output Power, By Phase Shift Type, By Frequency Range and Region |

| By Channel Count |

|

| By Application |

|

| By Output Power |

|

| By Phase Shift Type |

|

| By Frequency Range |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 988.2 million in 2025 and is projected to reach USD 3,317.5 million by 2034.

In 2025, the Europes market value stood at USD 285.27 million.

The market is expected to exhibit a CAGR of 14.4% during the forecast period.

By single channel segment is expected to dominate the market.

Rising demand for 5G and advanced wireless technologies are the key factors driving market growth.

Analog Devices, Inc. (U.S.), Murata Manufacturing Co., Ltd. (Japan), Qorvo, Inc. (U.S.), Texas Instruments Incorporated (U.S.), NXP Semiconductors (Netherlands), Mercury Systems (U.S.) are few major players in the global market.

Europe dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us