Dual Incretin Agonists Market Size, Share & Industry Analysis, By Drug (Tirzepatide, Survodutide, and Others), By Disease Indication (Type 2 Diabetes, Obesity, MASH/NASH, and Others), By Age Group (Pediatric and Adults), By Type (Branded and Generics), By Route of Administration (Subcutaneous, Oral, and Others), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, Specialty Pharmacies, and Online Pharmacies) and Regional Forecast, 2026-2034

Dual Incretin Agonists Market Size and Future Outlook

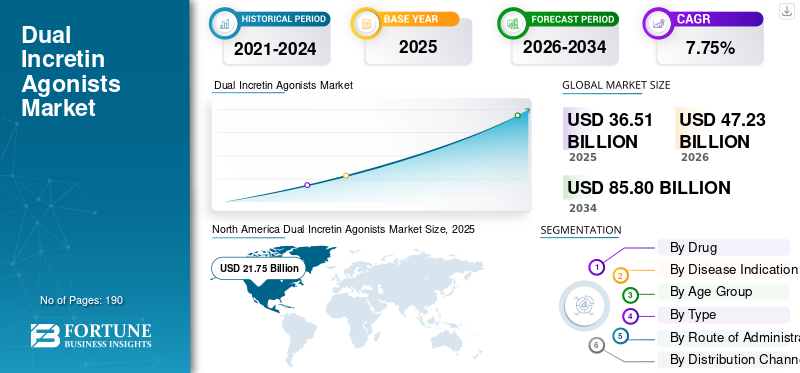

The global dual incretin agonists market size was valued at USD 36.51 billion in 2025. The market is projected to grow from USD 47.23 billion in 2026 to USD 85.80 billion by 2034, exhibiting a CAGR of 7.75% during the forecast period. North America dominated the dual incretin agonists market with a market share of 59.57% in 2025.

The global dual incretin agonists market includes therapies that act on two metabolic hormone pathways to improve blood sugar control and support meaningful weight reduction, mainly in patients with type 2 diabetes, obesity, and related cardio-metabolic conditions. The market is expanding as healthcare systems see strong demand for therapies that address both glycemic control and body-weight management through a single treatment approach. As clinical evidence continues to improve and approved products gain wider physician acceptance, companies are increasing investments in label expansion, access programs, and next-generation pipeline development, which is further strengthening the global market growth.

- For instance, in September 2025, Eli Lilly and Company announced that Mounjaro (tirzepatide), a GIP/GLP-1 dual receptor agonist, met the primary and all key secondary endpoints in the SURPASS-PEDS Phase 3 trial in children and adolescents with type 2 diabetes. Such continued lifecycle expansion of dual incretin agonists beyond existing adult use, which can widen the treatable patient pool and strengthen long-term commercial adoption of this therapy class.

Furthermore, major players, such as Eli Lilly and Company, Innovent Biologics, Inc., Boehringer Ingelheim International GmbH, and Zealand Pharma A/S, are expanding their offerings.

Download Free sample to learn more about this report.

DUAL INCRETIN AGONISTS MARKET TRENDS

Rising Preference for Dual-Action Therapies in Metabolic Disease Management Is an Emerging Trend Observed

The global market is witnessing this trend as healthcare providers and drug developers increasingly focus on therapies that address multiple metabolic problems through a single treatment approach. Dual incretin agonists are gaining attention because they can support better blood sugar control, meaningful weight reduction, and broader cardio-metabolic benefits, making them more attractive than many conventional single-mechanism therapies. As treatment expectations shift from glucose-lowering alone to more comprehensive metabolic management, demand is moving toward dual-action products, which are strengthening clinical adoption, pipeline expansion, and commercial investment across the market.

- For instance, in November 2025, Eli Lilly and Company announced an agreement with the U.S. government to expand access to its obesity medicines and reduce patient costs. This development enabled broader access support for obesity therapies can improve treatment uptake, expand the eligible patient base, and further accelerate the shift toward advanced dual-action metabolic therapies in routine care.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Global Burden of Obesity and Type 2 Diabetes Driving Demand for Dual Incretin Therapies

The global market is growing because obesity and type 2 diabetes care is increasing together in many countries, which is creating demand for therapies that can manage blood sugar and body weight at the same time. This is pushing drug developers and healthcare providers toward dual incretin agonists, as these therapies are being positioned as higher-value treatment options for patients who need broader metabolic benefit than conventional glucose-lowering drugs alone. As a result, rising disease burden is directly supporting stronger clinical development, greater physician interest, and higher commercial investment in this market. Thus, these factors are driving global dual incretin agonists market growth.

- For instance, in October 2025, Innovent Biologics, Inc. announced that mazdutide demonstrated superiority over semaglutide for glycemic control and weight loss in the Phase 3 DREAMS-3 trial in patients with type 2 diabetes.

MARKET RESTRAINTS

High Therapy Cost and Access Barriers Restricting Market Penetration Restrain Market Growth

The global market faces this restraint because these therapies remain expensive and are not yet uniformly covered across payer systems, which limits how quickly eligible patients can start treatment. When out-of-pocket burden, prior authorization rules, and reimbursement restrictions remain high, patient access becomes narrower and real-world uptake slows even when clinical demand is strong. This directly reduces prescription conversion, delays treatment initiation, and restricts broader market expansion, especially in obesity care, where coverage remains more limited than clinical interest.

- For instance, in March 2025, NHS England announced interim commissioning guidance for tirzepatide (Mounjaro), under which access for obesity management would be introduced in a phased rollout, with prescribing initially limited to prioritized cohorts due to service capacity and demand-management needs. Such instances demonstrate that even after clinical acceptance, access remains restricted by funding and system capacity, which can slow patient uptake and delay broader market penetration for dual incretin agonists.

MARKET OPPORTUNITIES

Expansion into Obesity and Adjacent Metabolic Indications Creating New Growth Opportunities

The global dual incretin agonists market is poised for strong growth as companies expand these therapies beyond type 2 diabetes into obesity and related metabolic diseases, potentially significantly widening the addressable patient pool. When the same drug class shows potential across multiple high-burden conditions, companies can expand commercial reach, strengthen product positioning, and create longer-term revenue opportunities from a single therapeutic platform. Such factors are making dual incretin agonists more attractive not only as glucose-lowering drugs, but also as broader metabolic therapies with multi-indication potential.

- For instance, on 26 February 2024, Boehringer Ingelheim announced that survodutide, a glucagon/ glp-1 therapies, achieved statistically significant Phase II results in metabolic dysfunction-associated steatohepatitis (MASH), with up to 83.0% of treated adults showing improvement compared with placebo. Such expanding pipeline to offer growth opportunities for the market.

MARKET CHALLENGES

Scaling Manufacturing Capacity and Broad Patient Access Remain a Key Market Challenge

The global market is facing this challenge owing to demand for these therapies rising faster than the market’s ability to expand manufacturing output and patient access at the same pace. When supply scale-up, distribution planning, and reimbursement readiness do not progress quickly enough, companies can face delayed treatment availability, uneven market penetration, and slower conversion of clinical demand into actual sales. This makes commercial execution more difficult, especially in a market where demand is strong but long-term growth depends on reliable product availability and wider access across regions.

- For instance, on 21 June 2024, Eli Lilly and Company announced that it was increasing its manufacturing investment at its Indiana site to USD 9.00 billion to boost active pharmaceutical ingredient production for tirzepatide and other pipeline medicines.

Segmentation Analysis

By Drug

Wide Prescription Volume of Tirzepatide to Enable Segmental Dominance

Based on the drug, the market is categorized into tirzepatide, survodutide, and others.

Among these, the tirzepatide segment held the largest dual incretin agonists market share. Tirzepatide dominated the market as it is the most commercially established dual incretin agonist in this space, with broader clinical validation, stronger physician familiarity, and actual market availability across major metabolic indications. Since survodutide is still largely pipeline-led, tirzepatide has gained an early-mover advantage in prescriptions, brand visibility, and real-world adoption. As a result, its stronger commercialization base helped it capture the leading market share.

- For instance, in November 2023, Eli Lilly and Company announced that Zepbound (tirzepatide) became available in U.S. pharmacies for adults with obesity or overweight with at least one weight-related condition. This development strengthened tirzepatide’s market position by expanding its use from diabetes to obesity care, widening its commercial reach, and reinforcing its dominance in the market.

The others segment is expected to grow at a CAGR of 21.43% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Increasing Prevalence of Type 2 Diabetes to Lead to Dominance of the Segment

Based on the disease indication, the market is segmented into type 2 diabetes, obesity, MASH/NASH, and others.

In 2025, type 2 diabetes dominated the market because dual incretin agonists were first established and adopted in this indication, where the need for better glycemic control and weight management is already very high. Physicians are more willing to prescribe newer metabolic therapies in diabetes when they show strong A1C reduction and broader cardiometabolic benefit. Because of this, earlier treatment acceptance and clearer clinical positioning, type 2 diabetes remained the largest indication in the market.

- For instance, in July 2025, Eli Lilly and Company announced that Mounjaro (tirzepatide) delivered cardiovascular protection in the SURPASS-CVOT trial in adults with type 2 diabetes and established cardiovascular disease. The development reinforced tirzepatide’s value in the core diabetes patient population, supporting continued physician confidence and keeping type 2 diabetes as the leading demand segment in the market.

The MASH/NASH segment is projected to grow at a CAGR of 22.49% during the forecast period.

By Age Group

Larger Adult Patient Pool to Boost Segmental Growth

Based on age group, the market is segmented into pediatric and adults.

In 2025, the adults segment dominated the market because the currently commercialized dual incretin agonist opportunity has been centered mainly on adult patients with type 2 diabetes, obesity, and related cardiometabolic disorders. Pediatric use remains more limited and is gradually expanding with additional clinical evidence and regulatory progress. As a result, the adult population continues to account for the largest treated base and the highest prescription volume in this market.

- For instance, in September 2025, Eli Lilly and Company showcased positive results from Phase 3 SURPASS-PEDS studies for Mounjaro in children and adolescents with type 2 diabetes. The announcement itself showed pediatric expansion is still emerging, while adult use was already established.

The pediatric segment is projected to grow at a CAGR of 22.00% during the forecast period.

By Type

Commercial Stages of Dual Incretin Agonist to Boost Branded Segmental Growth

Based on type, the market is segmented into branded and generics.

In 2025, the branded product type accounted for the largest share of the market. Branded products dominated the market because this therapy class is still in an early commercial stage and is led by patented innovator drugs, especially tirzepatide. There is no broad, generic competition yet for the leading dual incretin agonist products, and pipeline assets such as survodutide are also being developed as branded, innovative therapies. Because of this innovation-led structure, branded products captured the majority of market revenue and usage.

- For instance, in March 2025, Eli Lilly and Company launched Mounjaro in India in a single-dose vial presentation for obesity, overweight, and type 2 diabetes. The development supported the dominance of the branded segment.

The generic segment is projected to grow at a CAGR of 19.85% during the forecast period.

By Route of Administration

Expanding Pipeline of Subcutaneous Route of Administration to Boost Segmental Growth

Based on route of administration, the market is segmented into subcutaneous, oral, and others.

In 2025, the subcutaneous administration dominated the market owing to the leading commercial and pipeline dual incretin agonists have primarily been developed as injectable therapies, supporting controlled weekly dosing and established bioavailability. Since oral dual incretin options remain limited or are under development, injectable products have remained the most practical and widely used route in current clinical practice. This has made subcutaneous delivery the dominant route across the market.

- For instance, in January 2024, Eli Lilly and Company received marketing authorization in Great Britain from the MHRA for tirzepatide (Mounjaro) in an alternative KwikPen presentation for two indications. This development strengthened the product’s injectable delivery format and facilitated easier administration in routine care, further reinforcing the dominance of the subcutaneous segment.

The others segment is projected to grow at a CAGR of 22.79% during the forecast period.

By Distribution Channel

Increasing Trend of Digital Order Placement to Support the Dominance of Online Pharmacies

Based on the distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, specialty pharmacies, and online pharmacies.

By distribution channel, the online pharmacies dominated the market because dual incretin agonists are high-value specialty therapies, for which patients increasingly prefer digital ordering, home delivery, transparent self-pay pricing, and manufacturer-linked access platforms. Companies are also using direct-to-patient digital channels to improve reach, especially for self-pay obesity care. Because of this shift toward convenience and digitally enabled fulfillment, online pharmacy channels gained a stronger share in this market.

- For instance, on October 2025, Eli Lilly and Company collaborated with Walmart Inc. to expand access to LillyDirect pricing for Zepbound vials and to extend broader retail pickup access. The development reflects how digitally enabled pharmacy access models are becoming a major distribution route for dual incretin therapies, helping online-linked channels strengthen their position in the market.

The specialty pharmacies segment is projected to grow at a CAGR of 9.91% over the forecast period.

Dual Incretin Agonists Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Dual Incretin Agonists Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 10.12 billion and maintained its leading position in 2025 at USD 21.75 billion. The market is growing strongly in North America as the region has a large diagnosed population with obesity and type 2 diabetes, high awareness of advanced metabolic therapies, and expanding commercial availability.

U.S. Dual Incretin Agonists Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 24.74 billion in 2026, accounting for roughly 52.38% of the global market.

Europe

Europe is projected to grow at 9.12% over the coming years, the second-highest among all regions, and expected to reach a valuation of USD 9.30 billion by 2026. Europe is growing due to dual incretin agonists gaining regulatory and clinical acceptance for both diabetes and weight management, which is improving physician confidence and patient uptake.

U.K. Dual Incretin Agonists Market

The U.K. market is estimated at around USD 1.27 billion in 2026, representing roughly 2.70% of the global market.

Germany Dual Incretin Agonists Market

Germany's market is projected to reach approximately USD 1.66 billion in 2026, equivalent to around 3.51% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 7.37 billion in 2026 and secure the position of the third-largest region in the market. Asia-Pacific is growing quickly because the region has a large diabetes burden, and companies are actively expanding access through product launches and local approvals.

Japan Dual Incretin Agonists Market

The Japanese market in 2026 is estimated at around USD 1.64 billion, accounting for approximately 3.48% of the global market.

China Dual Incretin Agonists Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 2.06 billion, representing approximately 4.35% of global sales.

India Dual Incretin Agonists Market

The Indian market in 2026 is estimated at around USD 0.81 billion, accounting for roughly 1.72% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The market in Latin America is estimated to reach a valuation of USD 1.76 billion in 2026. Latin America is growing due to increasing prevalence of obesity and diabetes, while awareness and demand for high-efficacy weight-loss and glucose-control drugs are rising in large markets such as Brazil. In the Middle East & Africa, the GCC market is set to reach USD 0.54 billion in 2026.

South Africa Dual Incretin Agonists Market

The South African market is projected to reach approximately USD 0.27 billion by 2026, accounting for roughly 0.56% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Progress

The global dual incretin agonists market is highly consolidated, with companies such as Eli Lilly and Company, Innovent Biologics, Inc., Boehringer Ingelheim International GmbH, Inc, Zealand Pharma A/S, Hanmi Pharmaceutical Co., Ltd., Merck & Co., Inc., and Altimmune, Inc. holding significant market share. Strategic partnerships, new product launches, and regulatory approvals in the sector drive these companies' market share.

- For instance, in August 2025, Boehringer Ingelheim announced the advancement of BI 3034701, its long‑acting, first-in-class, potential triple‑agonist peptide, in development for the treatment of obesity. This milestone reflects the company’s strategy to address the global burden of obesity and its interconnected cardiovascular, renal, metabolic (CRM) complications.

Other notable players in the global market include Viking Therapeutics, Inc, OPKO Health, Inc., and Jiangsu Hengrui Pharmaceuticals Co., Ltd. These companies are expected to prioritize strategic collaborations and new product launches to strengthen their positions during the forecast period.

LIST OF KEY DUAL INCRETIN AGONIST COMPANIES PROFILED:

- Eli Lilly and Company (U.S.)

- Innovent Biologics, Inc. (China)

- Boehringer Ingelheim International GmbH (Germany)

- Zealand Pharma A/S (Denmark)

- Hanmi Pharmaceutical Co., Ltd. (South Korea)

- Merck & Co., Inc. (U.S.)

- Altimmune, Inc. (U.S.)

- Viking Therapeutics, Inc. (U.S.)

- OPKO Health, Inc. (U.S.)

- Jiangsu Hengrui Pharmaceuticals Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Pfizer Inc. acquired Metsera, Inc., a clinical-stage biopharmaceutical company accelerating the next generation of medicines for obesity and cardiometabolic diseases. The acquisition brought deep expertise and a portfolio of differentiated oral and injectable incretin, non-incretin, and combination therapy candidates with potential best-in-class efficacy and safety profiles.

- August 2025: Viking Therapeutics, Inc. announced positive top-line results from the company's Phase 2 clinical trial of the oral tablet formulation of VK2735, a dual agonist of the glucagon-like peptide 1 (GLP-1) and glucose-dependent insulinotropic polypeptide (GIP) receptors. VK2735 is being developed in both oral and subcutaneous formulations for the potential treatment of various metabolic disorders, such as obesity.

- July 2025: Hengrui Medicine and Kailera Therapeutics jointly announced positive top-line results from the Phase III clinical trial (HRS9531-301) of the GLP-1/GIP dual receptor agonist HRS9531 injection in the treatment of obese or overweight subjects in China.

- June 2025: Altimmune, Inc. announced positive topline results from the IMPACT Phase 2b trial of pemvidutide in metabolic dysfunction-associated steatohepatitis (MASH).

- March 2025: Hoffmann-La Roche Ltd collaborated with Zealand Pharma to co-develop and co-commercialize petrelintide, Zealand Pharma’s amylin analog, as a standalone therapy and as a fixed-dose combination with Zealand Pharma’s lead incretin asset, CT-388.

REPORT COVERAGE

The report provides the global dual incretin agonists market analysis across key segments, including drug, disease indication, age group, type, route of administration, and distribution channel. It also examines regional performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, while assessing how rising demand for advanced therapies for type 2 diabetes, obesity, and related metabolic disorders is driving market expansion. The study further covers major market dynamics, including drivers, restraints, opportunities, and challenges, as well as market trends, along with an evaluation of competitive developments such as clinical progress, regulatory milestones, pipeline advancements, partnerships, and commercialization activities by key companies operating in the market. In addition, the report includes company profiling, segment-level outlook, and an assessment of how innovation, access expansion, and evolving treatment adoption are shaping the market's future direction.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.75% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug, Disease Indication, Age Group, Type, Route of Administration, Distribution Channel, and Region |

| By Drug |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 36.51 billion in 2025 and is projected to reach USD 85.80 billion by 2034.

In 2025, the market value stood at USD 21.75 billion.

The market is expected to grow at a CAGR of 7.75% over the forecast period.

Tirzepatide drug segment is expected to lead the market.

The market is driven by rising global burden of obesity and type 2 diabetes driving for the global market demand.

Eli Lilly and Company, Innovent Biologics, Inc., Boehringer Ingelheim International GmbH, Inc, Zealand Pharma A/S, and Hanmi Pharmaceutical Co., Ltd. are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us