eVTOL Cabin Interior Market Size, Share & Industry Analysis, By Aircraft Configuration (Multicopter / Wingless, Lift + Cruise, Vectored Thrust / Tilt-Rotor, and Ducted Fan / Jet-style), By Component (Seating Systems, Restraint & Safety, Cabin Panels & Trim, Flooring Systems, Lighting Systems, Cabin Comfort, Passenger Interface, and Stowage & Accessibility), By Seating Capacity, By Material, By Application (Urban Air Taxi, Regional Air Mobility, Tourism & Sightseeing, Emergency Medical/Public Service, and Others), By End User (eVTOL OEMs and AAM Operators), and Regional Forecast, 2026-2034

eVTOL Cabin Interior Market Size and Future Outlook

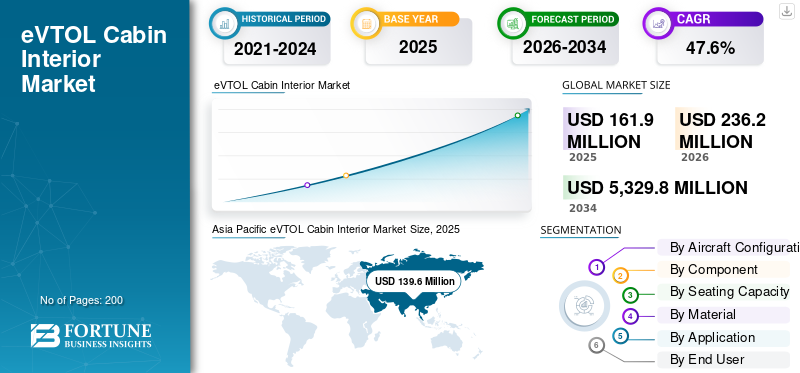

The eVTOL cabin interior market size was valued at USD 161.9 million in 2025. The market is projected to grow from USD 236.2 million in 2026 to USD 5,329.8 million by 2034, exhibiting a CAGR of 47.6% during the forecast period. Asia Pacific dominated the evtol cabin interior market with a market share of 86.23% in 2025.

The market covers aircraft interiors used in electric vertical take-off and landing platforms, including ergonomic seating, restraint and safety systems, cabin panels, flooring, lighting, passenger interface systems, stowage, and other interior components. The market is gaining traction as eVTOL programs look to certification and initial commercial operations. The market growth is driven by rising demand for urban air taxi services, airport shuttles, tourism flights and emergency mobility. The market trends are driven by lightweight materials, modular cabin layouts, regulatory compliance and supply chain readiness.

Major market players are EHang Holdings Limited, Eve Air Mobility, Joby Aviation, Inc., Supernal, LLC, RECARO Aircraft Seating GmbH & Co. KG, and collins aerospace. eVTOL OEMs define aircraft-specific cabin layouts and passenger experience needs. Aircraft interiors suppliers support seating, safety, lighting, interior systems, and certification-ready integration. These players are driving the market toward commercial adoption, with developments such as Eve’s passenger-centric lift and cruise cabin, Joby’s work on market-readiness in Dubai, and Supernal’s modular cabin concept.

Download Free sample to learn more about this report.

eVTOL CABIN INTERIOR MARKET TRENDS

Modular Cabin Architecture is Reshaping Market Expansion

The market is moving toward modular cabin design as operators will need the same aircraft platform to support passenger mobility, cargo movement, premium shuttle services, and public-service missions without a complete redesign of the cabin. This trend is directly linked to aircraft utilization, as a flexible cabin can improve turnaround efficiency, reduce customization cost, and allow interior components to be upgraded as aircraft move from pilot-operated service to more automated operations. For cabin suppliers, this creates stronger demand for lightweight aircraft interiors, configurable seating, quick-change cabin layouts, passenger interface systems, and certification-ready interior systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Investments in eVTOL Certification Drives Market Growth

The eVTOL cabin interior market growth is driven by clearer certification and operating rules for powered-lift aircraft. Once regulators determine what it will take to certify, pilot, operate and integrate these aircraft into existing airspace, OEMs and suppliers will be able to move beyond concept cabins and begin to design production-ready aircraft interiors. This showcases that rising demand for compliant seating, restraint systems, lighting, cabin panels, passenger interface systems and other interior components must pass aviation safety standards prior to commercial deployment. Moreover, increasing investments in eVTOL certification, manufacturing capacity, and commercial launch programs are strengthening demand for aircraft interiors.

- In October 2024, the FAA issued its final rule for powered-lift operations, covering pilot and instructor certification requirements as well as operational rules for aircraft in the powered-lift category.

MARKET RESTRAINTS

Certification Cost and Funding Pressure Restrains Market Growth

The market is still restrained by high cost and long timelines required to certify new aircraft platforms. eVTOL cabin interiors cannot scale independently from aircraft certification, meaning delays in airframe testing, power systems, safety validation, and regulatory compliance directly slow cabin interior procurement. This creates a difficult environment for smaller OEMs and interior suppliers as development spending continues long before commercial revenue begins.

MARKET OPPORTUNITIES

Early Commercial Air Taxi Launches Create New Market Opportunities

The strongest market opportunity lies in early launch products where eVTOL operators are moving from demonstration flights to commercial readiness. As air taxi networks develop, operators will require durable cabin layouts, ergonomic seating, premium passenger finishes, safety equipment, acoustic treatment, and fast-maintenance interior systems. This gives cabin suppliers a path to support not only line-fit interiors but also future replacement, refurbishment, and operator-specific cabin customization.

MARKET CHALLENGES

Infrastructure and Operating-Condition Readiness is a Major Market Challenge

Major challenge in the market is that the interiors are expected to perform reliably in demanding real-world operating environments, not just prototype demonstrations. The high heat, short frequent cycles, rapid passenger throughput, ground crew handling and vertiport operations will be a challenge for cabin cooling, flooring durability, seat materials, lighting systems and safety equipment. Operators have yet to prove that aircraft can operate on a regular basis under these conditions and suppliers will be uncertain about final cabin standards and replacement cycles.

Impact of Ongoing Conflicts

Geopolitical Conflicts Create a Mixed Impact on Market

The Russia-Ukraine war, Middle East conflict, and other ongoing security flashpoints are creating a mixed impact on the market. On one side, these conflicts are pushing governments and operators to look more seriously at advanced air mobility for emergency response, medical evacuation, surveillance-support mobility, airport-to-city access, and controlled low-altitude transport, which can support demand for modular cabin layouts, restraint and safety systems, durable flooring, acoustic treatment, and other mission-ready interior components. On the other side, the same conflicts are adding pressure to the aviation supply chain through sanctions, airspace restrictions, export controls, higher defense prioritization, and uncertainty around aerospace materials, electronics, batteries, and certified interior systems.

In April 2025, SIPRI reported that global military expenditure reached USD 2,718.00 billion in 2024, rising 9.40% in real terms, with particularly strong increases in Europe and the Middle East. Europe, including Russia, recorded USD 693.00 billion in military spending, while Middle East military spending reached USD 243.00 billion.

Segmentation Analysis

By Aircraft Configuration

Multicopter / Wingless Segment Dominates Due to Growing Demand for Commercial Delivery Volume

In terms of aircraft configuration, the market is categorized into multicopter / wingless, lift + cruise, vectored thrust / tilt-rotor, and ducted fan / jet-style.

Multicopter / Wingless segment held the largest eVTOL cabin interior market share in 2025, as early realized demand is concentrated around compact, short-range passenger and mission variants rather than larger winged platforms. These aircraft need comparatively simple but certified cabin layouts, basic passenger seating, restraint systems, lighting, and safety-focused interior components. Since most winged lift+cruise and vectored-thrust aircraft are still moving through certification or pre-commercial readiness, multicopter/wingless aircraft currently absorb the highest realized cabin-interior value.

In March 2026, EHang reported FY2025 sales and deliveries of 221 eVTOL aircraft, including 215 EH216-series units and 6 VT35 units. EHang also stated that the EH216 series includes passenger transportation, firefighting, and logistics variants.

Lift + cruise segment is expected to grow at a highest CAGR of 54.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Seating Systems Segment Leads Owing to Focus on Safety-Critical Passenger Accommodation

On the basis of component, the market is classified into seating systems, restraint & safety, cabin panels & trim, flooring systems, lighting systems, cabin comfort, passenger interface, and stowage & accessibility.

Seating systems segment held the largest market share in 2025, as every passenger eVTOL cabin requires certified seating, crashworthiness, restraint compatibility, lightweight structures, and ergonomic seating within a very small cabin envelope. In eVTOLs, seats are not just comfort products; they influence weight, center of gravity, passenger safety, emergency access, and cabin turnaround efficiency. As aircraft interiors move toward commercial service, seating becomes the first high-value cabin element selected by OEMs before more discretionary features such as premium lighting or passenger displays.

Cabin comfort segment is expected to show fastest growth, registering a CAGR of 51.7% over the forecast period.

By Seating Capacity

1–2 Seats Segment Dominates the Market Due to Demand for Compact Certified Passenger Platforms

On the basis of seating capacity, the market is classified into 1-2 seats, 3-5 seats, 6-9 seats, and 9 & Above.

1-2 seats segment held the largest share in 2025, as early eVTOL commercialization is led by compact passenger-carrying aircraft and short-range autonomous platforms. These aircraft are easier to validate operationally than larger cabins, require lower cabin-content complexity, and fit early use cases such as sightseeing, controlled routes, public demonstrations, and short urban mobility. Larger 3–5 seat aircraft will gain share later, but in currently, the comprehended delivery base is still skewed toward smaller cabin platforms.

3-5 seats segment is expected to show the fastest growth, registering a CAGR of 68.7% over the forecast period.

By Material

Composites Segment Dominates Due to Weight Sensitivity and Cabin Efficiency

The market is divided, by material, into composites, advanced thermoplastics, and lightweight metals.

Composites segment held the largest market share in 2025, as eVTOL cabins are highly weight-sensitive. Every kilogram added to cabin panels, flooring, seat shells, trim, or interior structures can affect payload, range, battery performance, and certification margins. Compared to conventional metal-heavy interiors, composite-based aircraft interiors offer better lightweighting potential, design flexibility, corrosion resistance, and integration with acoustic or vibration-control layers. This makes composites more suitable for compact, high-utilization eVTOL cabin layouts.

Advanced thermoplastics segment is expected to show the fastest growth, registering a CAGR of 52.4% over the forecast period.

By Application

Early Commercial Route Readiness Leads to Urban Air Taxi Segment Dominance

The market, by application, is divided into urban air taxi, regional air mobility, tourism & sightseeing, emergency medical/public service, and others.

Urban air taxi segment held the largest market share in 2025, as the first commercial eVTOL use cases are focused around short-distance city mobility, airport-to-city transfers, premium commuting, and controlled urban corridors. These routes create direct demand for compact cabin layouts, ergonomic seating, fast-clean flooring, passenger interface systems, acoustic comfort, and regulatory-compliant interior systems. Regional mobility and public-service applications will grow, but urban air taxi remains the clearest near-term commercial application.

Regional air mobility segment is expected to show the fastest growth, registering a CAGR of 74.2% over the forecast period.

By End User

Growing Line-Fit Interior Integration Leads to eVTOL OEMs Segment Leadership

Based on end user, the market is segmented into eVTOL OEMs and AAM operators.

eVTOL OEMs held the largest market share in 2025, as most cabin interior value is currently created at the aircraft development and production stage. OEMs define cabin architecture, seating capacity, restraint requirements, trim layout, weight limits, certification documentation, and supplier selection before aircraft reach operators. Until large commercial fleets are in service, aftermarket and operator-led refurbishment will remain smaller than OEM-led line-fit interior demand.

AAM operators segment is expected to show the fastest growth, registering a CAGR of 65.5% over the forecast period.

eVTOL Cabin Interior Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

North America

Asia Pacific eVTOL Cabin Interior Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America is anticipated to grow at a CAGR of 63.7%, supported by a strong OEM base, active FAA rulemaking, aircraft certification activity, and early operator planning in the U.S. The region is mainly relevant for higher-value aircraft interiors as leading programs are built around piloted, passenger-carrying aircraft with four-to-five-seat cabin layouts, safety-critical seating, restraint systems, passenger interface features, and lightweight interior components. The FAA’s powered-lift framework gives suppliers a clearer route to align cabin layouts, interior systems, and regulatory compliance requirements with commercial air taxi operations.

U.S. eVTOL Cabin Interior Market

Based on the strong contribution of North America to the market, the U.S. market stood at around USD 10.1 million in 2025, growing at a CAGR of 62.9%.

Europe

Europe market is anticipated to grow at a fastest pace with a CAGR of 72.7% during the forecast period, as several programs are still progressing through certification, funding, and commercialization milestones. The region benefits from EASA’s structured Special Condition VTOL framework, established aerospace interiors expertise, and active eVTOL development across the U.K., Germany, France, Italy, and other European countries. European demand is expected to focus on lightweight aircraft interiors, ergonomic seating, modular cabin concepts, noise-reduction materials, sustainable interior components, and certified safety systems.

Germany EVTOL Cabin Interior Market

Germany market reached approximately USD 0.8 million in 2025, equivalent to around 27.84% of Europe revenues.

Asia Pacific

Asia Pacific Region Dominates the Market Due to China’s Huge Delivery Base

Asia Pacific region dominates the market and is anticipated to grow at a CAGR of 35.4% over the forecast period, as China has accelerated the transition of eVTOL development into aircraft deliveries, trial operations, and commercial-readiness activities faster than other regions. North America and Europe have strong certification pipelines. Asia Pacific has the strongest cabin bearing volume mostly through China. Thus, the region has a higher share of real cabin-interior demand, especially in seating systems, basic passenger cabins, safety equipment, and compact interior components.

China eVTOL Cabin Interior Market

The Chinese market, in 2025, stood at USD 128.0 million, representing roughly 91.68% of the global sales.

South Korea eVTOL Cabin Interior Market

South Korea market in 2025 stood at around USD 2.4 million, accounting for roughly 1.72% of Asia Pacific revenues.

Rest of the World

Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a 56.8% CAGR during the forecast period. The Middle East is moving faster as the UAE is already preparing for commercial air taxi operations, including vertiport development, regulatory coordination, and live aircraft readiness work. Latin America is more development-stage, but Brazil gives the region a credible long-term base through Eve Air Mobility and Embraer’s aerospace ecosystem.

Middle East & Africa eVTOL Cabin Interior Market

The market in Middle East & Africa reached around USD 5.9 million, accounting for roughly 68.64% of the revenues, in 2025.

Latin America eVTOL Cabin Interior Market

Latin America market stood at around USD 2.7 million in 2025 and is expected to reach USD 241.3 million in 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Goring Focus of Key Players on Cabin Layouts, Passenger Capacity, Ergonomic Seating Requirements Reshapes Market Competition

The competitive landscape of the market is still forming, with eVTOL OEMs currently holding the strongest influence over cabin architecture, supplier selection, and interior integration. Companies such as EHang, Eve Air Mobility, Joby Aviation, and Supernal are shaping early market direction as their aircraft programs define the first generation of cabin layouts, passenger capacity, ergonomic seating requirements, safety systems, and modular cabin expectations. Eve is focusing on a human-centered lift+cruise cabin with four passengers plus pilot at launch, Joby is moving closer to commercial air taxi operations through its Dubai readiness program, and Supernal is positioning a configurable cabin that can switch between passenger and cargo layouts.

Established aircraft interiors suppliers such as Collins Aerospace and recaro aircraft seating are expected to become more important as the market moves from prototype cabins to certified production interiors. Their relevance comes from experience in seating products, lighting, oxygen and passenger service systems, structures, systems integration, certification support, and supply chain management. For eVTOL OEMs, partnering with mature interior systems suppliers can reduce technical risk, improve regulatory compliance, and support scalable aircraft interiors as production volumes increase.

LIST OF KEY eVTOL CABIN INTERIOR COMPANIES PROFILED

- EHang Holdings Limited (China)

- Eve Holding, Inc. / Eve Air Mobility (Brazil)

- Joby Aviation, Inc. (U.S.)

- Archer Aviation Inc. (U.S.)

- Supernal, LLC (U.S.)

- Vertical Aerospace Ltd. (U.K.)

- BETA Technologies, Inc. (U.S.)

- Wisk Aero LLC (U.S.)

- SkyDrive Inc. (Japan)

- AutoFlight Co., Ltd. (China)

- TCab Tech Co., Ltd. (China)

- Horizon Aircraft Inc. (Canada)

- AMSL Aero Pty Ltd. (Australia)

- Collins Aerospace (RTX Business) (U.S.)

- RECARO Aircraft Seating GmbH & Co. KG (Germany)

- Safran Seats (France)

- Diehl Aviation (Germany)

- JAMCO Corporation (Japan)

- FACC AG (Austria)

- Expliseat SAS (France)

KEY INDUSTRY DEVELOPMENTS

- March 2026: EHang reported FY2025 deliveries of 221 eVTOL aircraft, including 215 EH216-series units and 6 VT35 units, with FY2025 revenue of USD 72.90 million. The company also reported expanded production capacity to 1,000 eVTOL units and components annually at its Yunfu facility.

- December 2025: Eve Air Mobility selected BETA Technologies to supply electric pusher motors for conforming prototypes and production aircraft. The agreement represents a potential 10-year opportunity for BETA of up to USD 1,000.00 million.

- June 2025: Eve Air Mobility signed its first binding framework agreement with Revo and Omni Helicopters International for up to 50 eVTOL aircraft worth USD 250.00 million, entry-into-service support, and aftermarket services for São Paulo operations.

- June 2025: Joby Aviation delivered its first aircraft to the UAE and began commercial market-readiness flights in Dubai, working with Dubai’s RTA, DCAA, and UAE GCAA. The company also stated that construction was underway on its first commercial vertiport site at Dubai International Airport.

- November 2024: Archer Aviation signed an agreement with Soracle worth up to USD 500.00 million, the Japan Airlines and Sumitomo Corporation joint venture, for the intended purchase of up to 100 Midnight eVTOL aircraft for Japan.

- October 2024: the FAA issued its final rule for powered-lift operations, covering pilot and instructor certification requirements and operational rules for powered-lift aircraft. This created a clearer regulatory path for eVTOL air taxi operations and certification-linked cabin requirements.

- October 2024: Toyota announced an additional USD 500.00 million investment in Joby Aviation to support certification and commercial production of Joby’s electric air taxi aircraft, bringing Toyota’s total investment in Joby to USD 894.00 million.

- July 2024: Eve Air Mobility named Diehl Aviation as the designer and producer of the interior for its eVTOL aircraft and selected ASE for the aircraft power distribution system under long-term supply agreements.

REPORT COVERAGE

The global eVTOL cabin interior market analysis provides an in-depth study of market size, insights, segmentation, company profiling & forecast by all the segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry expert’s developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 47.6% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Aircraft Configuration

|

|

By Component

|

|

|

By Seating Capacity

|

|

|

By Material

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 236.2 million in 2026 and is projected to reach USD 5,329.8 million by 2034.

In 2025, the Asia Pacific market value stood at USD 139.6 million.

The market is expected to exhibit a CAGR of 47.6% during the forecast period.

Multicopter / wingless segment led the market by aircraft configuration.

Increasing investments in eVTOL certification drives the market growth.

Key players in the market are Collins Aerospace, Safran Cabin Inc., RECARO Aircraft Seating GmbH & Co. KG, Diehl Aviation Laupheim GmbH, Joby Aviation, Inc., and Archer Aviation Inc.

Asia Pacific dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us