Ground-Based Air Defense System Market Size, Share & Industry Analysis, By Defense layer, By Component (Missile Interceptors, Radars and Sensors, Gun Systems and Ammunition, Directed Energy Systems, and Others), By Mobility, By Threat Type (Unmanned Aerial Systems, Cruise Missiles, and Others), By Application (Maneuver Force Protection, Airbase and Forward, Operating Base Defense, National Strategic Asset Protection, and Others), By End User (Army Forces, Joint Missile Defense Commands, Homeland Security, and Marine / Expeditionary Forces), and Regional Forecast, 2026-2034

Ground-Based Air Defense System Market Size and Future Outlook

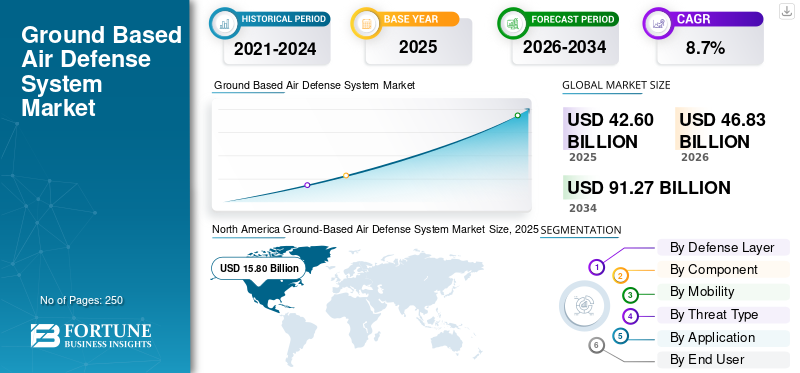

The global ground-based air defense system market size was valued at USD 42.60 billion in 2025. The market is projected to grow from USD 46.83 billion in 2026 to USD 91.27 billion by 2034, exhibiting a CAGR of 8.7% during the forecast period. North America dominated the ground based air defense system market with a market share of 37.09% in 2025.

Ground-Based Air Defense (GBAD) systems represent a critical layer in modern national security, enabling integrated, highly reliable, and multi-layered protection against aerial threats ranging from unmanned aerial systems and cruise missiles to tactical ballistic missiles and manned aircraft. The global push for advanced GBAD is accelerating, driven by the need to counter evolving asymmetric threats, protect critical infrastructure and military assets. It further supports joint force operations in contested environments, and integrates seamlessly with national air surveillance networks, early-warning radars, and C4I architectures across complex and congested airspaces.

Leading defense and electronics firms such as RTX Corporation / Raytheon, Lockheed Martin Corporation, MBDA, and Kongsberg Defense & Aerospace are advancing integrated GBAD suites. It supports multi-sensor fusion, long-range surveillance radars, engagement control systems, airspace monitoring solutions, and layered interceptor portfolios. Key technical advances include open-architecture and modular command-and-control software, Active Electronically Scanned Array (AESA) and Gallium-Nitride (GaN)-based radars for enhanced detection and tracking.

Download Free sample to learn more about this report.

GROUND-BASED AIR DEFENSE SYSTEM MARKET TRENDS

Shift Toward Networked, Layered, and Sensor-Fused Air Defense Architecture is Emerging as a Defining Market Trend

The market is increasingly moving away from standalone batteries toward networked, layered, and sensor-fused defense architectures. Modern forces are no longer buying only launchers and interceptors; they are prioritizing systems that can connect radars, fire-control units, command centers, launchers, and multiple types of effectors into one operational picture. This shift is being driven by the need to counter mixed salvos of drones, cruise missiles, ballistic missiles, rockets, and low-flying aircraft at the same time. NATO’s Integrated Air and Missile Defense policy also reinforces this direction by emphasizing layered short-, medium-, and long-range systems that provide mutual support against threats ranging from small UAS to cruise, ballistic, and hypersonic missiles.

- In September 2025, RTX received a USD 1.7 billion U.S. Army contract to deliver Lower Tier Air and Missile Defense Sensor / LTAMDS radars for the U.S. Army and Poland. The contract included nine radars, engineering services, spares, support, development, and testing, and RTX stated that LTAMDS provides 360-degree coverage against manned aircraft, unmanned aircraft, cruise missiles, ballistic missiles, and hypersonic threats.

This trend is expected to increase demand for 360-degree AESA radars, battle management systems, integrated fire-control networks, air-defense C2 software, sensor-fusion platforms, datalinks, and open-architecture command systems. As militaries shift toward distributed and layered air defense, procurement will increasingly favor systems that can plug into wider national, NATO, or joint-force air-defense networks rather than operate as isolated batteries.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Missile, Drone, and Saturation-Attack Threats is Propelling Market Growth

The ground-based air defense systems GBADS market is being driven by the rapid growth of missile, drone, loitering munition, cruise missile, and rocket threats across Europe, the Middle East, and Asia Pacific. Recent conflicts have shown that air defense is no longer limited to intercepting aircraft; modern systems must defend against large, mixed, and repeated salvos. This has increased demand for Patriot-class systems, NASAMS, IRIS-T SLM, SAMP/T, Iron Dome, David’s Sling, Arrow, THAAD, SHORAD, C-UAS systems, C-RAM systems, and interceptor stockpiles. The demand is especially strong for systems that can protect maneuver forces, airbases, cities, command centers, critical infrastructure, and logistics hubs from layered aerial attacks.

- In September 2025, the U.S. Army awarded Lockheed Martin a USD 9.8 billion multi-year contract for Patriot Advanced Capability-3 Missile Segment Enhancement / PAC-3 MSE production. The award covered fiscal years 2024–2026 and included 1,970 PAC-3 MSE missiles and associated hardware for the U.S. and international partners.

This driver is expected to sustain demand for missile interceptors, long-range air defense systems, medium range air defense batteries, mobile SHORAD, C-UAS effectors, radars, launchers, and air-defense command systems. The strongest adoption is expected in North America, Europe, Asia Pacific, and the Middle East, where missile-defense readiness and interceptor replenishment are becoming core procurement priorities.

MARKET RESTRAINTS

High Interceptor Costs, Production Bottlenecks, and Supply Chain Pressure to Limit Market Expansion

A key restraint for the ground-based air defense system market growth is the high cost and limited production capacity of advanced interceptors, radars, launchers, seekers, propulsion systems, and specialized electronics. Advanced systems such as Patriot, THAAD, Arrow, SAMP/T, IRIS-T SLM, and long-range missile-defense architectures require complex manufacturing, long qualification cycles, specialized suppliers, and secure electronics supply chains. Even when demand is strong, deliveries can be slowed by limited production lines, constrained missile-motor capacity, seeker availability, testing requirements, and the need to prioritize urgent operational users.

In November 2024, the U.S. Army awarded Lockheed Martin a contract to support increasing PAC-3 MSE production capacity to 650 missiles per year. Lockheed Martin stated that demand for PAC-3 MSE was growing rapidly and that the company had already started expanding production capacity across its factories and supply chain. This restraint is likely to affect both new buyers and existing operators and hamper the growth of the market during the forecast period.

MARKET OPPORTUNITIES

Directed Energy and Low-Cost Counter-UAV Defense Systems Presents Growth Opportunities for the Market

A major opportunity in the market lies in directed energy, high-power microwave, low-cost interceptors, programmable ammunition, and layered counter-UAS systems. Traditional missile interceptors remain essential against high-end threats, but they are expensive when used against low-cost drones, rockets, and saturation attacks. This cost imbalance is pushing militaries to add lasers, electronic defeat systems, gun-based air defense, and lower-cost kinetic effectors into layered air-defense networks.

- In March 2025, the Israel Ministry of Defense signed a landmark deal worth approximately NIS 2 billion(~USD 500 million) to expand serial production of the Iron Beam ground-based high-power laser interception system with Rafael and Elbit Systems. The system is designed to counter rockets, mortars, Unmanned Aerial Vehicles (UAVs), and cruise missiles, and is expected to complement Israel’s Iron Dome system while offering lower operational costs.

This opportunity is expected to increase demand for laser air-defense systems, high-power microwave systems, counter-drone sensors, electro-optical tracking systems, power modules, thermal management systems, mobile C-UAS platforms, and hybrid gun-missile-laser architectures.

MARKET CHALLENGES

Integration of Legacy Systems, C2 Networks, and Multi-Layer Defense Architectures to Challenge Market

A major market challenge is integrating new systems into existing legacy air-defense networks. Many countries operate mixed fleets of old and new radars, missile batteries, command posts, launchers, tactical radios, national air-defense centers, and allied interoperability systems. This makes modernization complex as a new radar or interceptor must work not only as a standalone product but also within a wider sensor-to-shooter chain.

This challenge can slow adoption as buyers must manage system integration, software baselines, radar compatibility, command-network upgrades, cybersecurity, training, maintenance planning, and doctrine changes at the same time.

Segmentation Analysis

By Defense Layer

Low-Altitude Threat Defense and Tactical Mobility Requirements to Support Long-Range Air Defense / LRAD Segment Dominance

Based on the defense layer, the market is divided into Very Short-Range Air Defense / VSHORAD, Short-Range Air Defense / SHORAD, Medium-Range Air Defense / MRAD, Long-Range Air Defense / LRAD, and terminal ballistic missile defense.

The Long-Range Air Defense / LRAD segment held a leading share in the market in 2025 as countries continue to prioritize protection against aircraft, cruise missiles, tactical ballistic missiles, and advanced aerial threats across wide-area defense zones. Demand is supported by procurement and modernization of high-value systems such as Patriot, SAMP/T, S-300/S-400-type systems, HQ-9-type systems, and other strategic surface-to-air missile architectures.

- In January 2025, RTX’s Raytheon was awarded a USD 529 million contract to replenish the Netherlands’ Patriot air defense system, supporting continued European investment in long-range ground-based air and missile defense capability.

The Short-Range Air Defense / SHORAD segment is anticipated to rise with a fastest-growth rate of 11.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Interceptor Stockpile Replenishment and Missile Defense Readiness to Drive Missile Interceptors Segment Growth

By component, the market is segmented into missile interceptors, radars and sensors, command, control, battle management & communications / C2BMC, launchers / firing units, gun systems and ammunition, directed energy systems, and support, training, maintenance & upgrades.

The missile interceptors segment dominated the market in 2025 as interceptor missiles form the primary engagement layer across VSHORAD, SHORAD, medium-range, long-range, and terminal missile-defense systems. Demand is supported by new air-defense battery procurement, interceptor stockpile replenishment, training requirements, and the need to sustain operational readiness against larger and more complex aerial threat salvos. The segment also benefits from the high value of advanced interceptors used against tactical ballistic missiles, cruise missiles, aircraft, and emerging high-speed threats.

- In September 2025, The U.S. Army awarded Lockheed Martin a USD 9.8 billion multi-year contract for 1,970 PAC-3 MSE missiles and associated hardware for the U.S. and international partners, covering fiscal years 2024 through 2026.

The directed energy systems segment is designed to register the fastest CAGR of 13.0% over the forecast period.

By Mobility

Persistent Base and Strategic Site Protection Requirements to Support Fixed / Semi-Fixed Strategic Systems Segment Dominance

On basis of mobility, the market is segmented into man-portable / dismounted, vehicle-mounted mobile systems, trailer-mounted / towed systems, containerized / rapidly deployable systems, and fixed / semi-fixed strategic systems

The fixed / semi-fixed strategic systems segment held a significant share in the market in 2025 as countries continue to deploy persistent air-defense coverage around airbases, command centers, logistics hubs, missile-defense sites, government facilities, ports, and critical infrastructure. These systems typically require larger radar coverage, integrated command posts, prepared launch positions, and sustained interceptor availability. Demand is strongest in countries prioritizing protection of fixed military installations, high-value national assets, and forward operating locations against unmanned aerial systems, cruise missiles, rockets, artillery, mortars, and ballistic missile threats.

- In November 2024, the U.S. Army awarded Dynetics, a Leidos company, an IFPC Inc 2 contract valued at up to USD 4.1 billion for low-rate initial production, full-rate production, and support services. The Army stated that IFPC Inc 2 provides protection for fixed and semi-fixed sites, forward operating bases, and critical infrastructure.

The vehicle-mounted mobile systems segment is projected to grow with a fastest CAGR of 11.1% over the forecast period.

By Threat Type

Ballistic Missile Threat Exposure and Layered Interception Requirements to Strengthen Ballistic Missiles Segment Growth

By threat type, the market is segmented into unmanned aerial systems / loitering munitions, cruise missiles, aircraft and helicopters, ballistic missiles, rockets, artillery, and mortars / ram, and hypersonic and maneuvering threats.

The ballistic missiles segment remained a major shareholding segment in 2025 as several countries continue to invest in systems capable of countering short-range, medium-range, and intermediate-range ballistic missile threats. Demand is supported by the need for advanced tracking radars, fire-control networks, high-value interceptors, and layered command-and-control architectures.

- In April 2025, Japan’s Ministry of Defense FY2025 defense budget allocated funding for integrated missile and air defense capabilities. Further, including PAC-3 MSE, Type 03 medium-range surface-to-air missile modification, warning and control radar upgrades, and command-and-control improvements

The unmanned aerial systems / loitering munitions segment is projected to grow with the fastest CAGR of 11.4% over the forecast period.

By Application

Capital, Command, and High-Value Asset Protection to Support Segment Dominance

By application, the market is segmented into maneuver force protection, airbase and forward, operating base defense, national strategic asset protection, critical infrastructure protection, border and perimeter air defense, and counter-rocket, artillery, & mortar defense.

The national strategic asset protection segment dominated the market in 2025 as governments strengthen air-defense coverage around capitals, population centers, national command authorities, airbases, defense industrial sites, energy infrastructure, ports, and other high-value national assets. Demand is supported by procurement of layered systems combining short-range, medium-range, long-range, and terminal missile-defense capabilities.

- In January 2025, Israel’s Ministry of Defense signed the first procurement contract under a U.S. aid package with Rafael to expand serial production of Iron Dome interceptors. The package included a dedicated USD 5.2 billion allocation for strengthening Israel’s air and missile defense systems.

The maneuver force protection segment is designed to register the fastest CAGR of 11.8% over the forecast period.

By End User

Tactical Formation Protection and Ground Force Air Defense Modernization to Sustain Army/Land Forces Segment Leadership

On the basis of end user, the market is divided into army / land forces, air force / air defense command, joint missile defense commands, homeland security / interior ministries, and marine / expeditionary forces.

The army / land forces segment held a leading ground-based air defense system market share in 2025 as ground forces expand air-defense capabilities for maneuver units, artillery formations, logistics convoys, command posts, forward bases, and deployed tactical assets. Demand is supported by modernization of SHORAD, VSHORAD, counter-UAS, indirect fire protection, and mobile air-defense systems.

- In June 2025, the U.S. Government Accountability Office reported that the U.S. Army had identified multiple air and missile defense modernization efforts and reviewed programs intended to protect soldiers, equipment, and facilities from air and missile threats.

The army / land forces segment is expected to register the fastest CAGR of 11.0% over the forecast period.

Ground-Based Air Defense System Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Ground-Based Air Defense System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025 with a valuation of USD 15.80 billion, growing to USD 17.18 billion in 2026. The region is expected to remain the largest market, primarily driven by the U.S. air and missile defense ecosystem, large installed base of Patriot and THAAD-class systems, ongoing LTAMDS and IBCS modernization, counter-UAS investment, interceptor replenishment, and fixed-site defense requirements. Demand is supported by continued modernization of ground-based missile defense, short-range air defense, indirect fire protection, and integrated battle management architectures.

- In July 2025, the U.S. Army announced plans to add up to four additional Patriot battalions, including one for the Guam Defense System. The new battalions are expected to use LTAMDS to expand detection and engagement capabilities against cruise missiles, hypersonic threats, short-range ballistic missiles, and multiple aerial targets.

U.S. Ground-Based Air Defense System Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was approximated at around USD 15.03 billion in 2025. The U.S. is expected to remain the largest country-level market due to its advanced missile-defense infrastructure, large air-defense artillery force structure, strong domestic prime contractor base, and sustained investment in Patriot, THAAD, LTAMDS, IFPC, SHORAD, C-UAS, and integrated battle command systems. Growth is supported by interceptor production, protection of deployed forces and strategic sites, Guam defense requirements, and the need to counter cruise missiles, ballistic missiles, unmanned aerial systems, rockets, artillery, and mortars.

- In November 2024, the U.S. Army awarded Dynetics, a Leidos company, an IFPC Inc 2 contract valued at up to USD 4.1 billion for low-rate initial production, full-rate production, and support services.

Europe

Europe is projected to record a fastest-growth rate of 11.3% during 2026 to 2034. The region is expected to hold a strong and rising share in the market. It is supported by NATO air-defense modernization, Ukraine-war-driven capability gaps, interceptor replenishment, European Sky Shield Initiative activity, and procurement of Patriot, IRIS-T SLM, SAMP/T, Skyranger, Narew, and other layered air-defense systems. The market growth is being driven by demand for medium-range and long-range air defense, mobile SHORAD, C-UAS systems, 360-degree radars, and integrated command-and-control networks.

- In July 2025, Switzerland signed a contract for the cooperative procurement of five IRIS-T SLM medium-range ground-based air defense systems under the European Sky Shield Initiative.

U.K. Ground-Based Air Defense System Market

The U.K. market in 2025 was estimated at around USD 0.87 billion, representing roughly 2.0% of global revenues.

Germany Ground-Based Air Defense System Market

The Germany market is projected to reach approximately USD 1.23 billion in 2025, equivalent to around 2.9% of global sales.

Asia Pacific

Asia Pacific is projected to witness moderate growth rate in the market. The region’s demand is driven by China, India, Japan, South Korea, Australia, Taiwan, and Southeast Asian defense modernization programs. The ground-based air defense adoption is supported by ballistic missile threats, cruise missile risk, airbase protection requirements, territorial defense, and modernization of national integrated air and missile defense networks. Japan and South Korea are particularly important for terminal missile defense and layered interception, while India and China support demand through large territorial defense networks and indigenous air-defense development.

- In January 2025, South Korea’s Defense Acquisition Program Administration approved the mass-production plan for the L-SAM long-range surface-to-air missile system. Further, supporting the Korean Air and Missile Defense architecture with higher-altitude interception capability alongside M-SAM II and Patriot systems.

Japan Ground-Based Air Defense System Market

The Japan market in 2025 was estimated at around USD 1.64 billion, accounting for roughly 3.8% of global revenues.

China Ground-Based Air Defense System Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 3.62 billion, representing roughly 8.5% of global sales.

India Ground-Based Air Defense System Market

The Indian market in 2025 was estimated at around USD 1.99 billion, accounting for roughly 4.7% of global revenues.

Latin America and Middle East & Africa

Latin America represents a smaller but steadily developing market for ground-based air defense systems. Regional demand is concentrated in Brazil, Mexico, Colombia, and the rest of the Latin America market. The region is more focused on VSHORAD, SHORAD, mobile radar, point defense, and tactical airspace protection rather than large-scale ballistic missile defense.

- In March 2025, Saab highlighted its ground-based air defense portfolio for Brazil at LAAD 2025, including RBS 70 NG, Giraffe 1X radar, and the MSHORAD mobile short-range air defense system. These systems combine RBS 70 NG, radar, and command-and-control capability for mobile air-defense operations.

The market in the Middle East & Africa is led by Israel, Saudi Arabia, UAE, Qatar, Egypt, Algeria, and selected African defense markets. The market is strongly driven by missile, rocket, drone, and cruise missile threats, as well as the need to protect cities, airbases, energy infrastructure, ports, command centers, and other high-value assets.

Brazil Ground-Based Air Defense System Market

Brazil market in 2025 was estimated at around USD 0.39 billion, accounting for roughly 0.9% of global revenues.

Saudi Arabia Ground-Based Air Defense System Market

The Saudi Arabia market in 2025 was estimated at around USD 2.27 billion, accounting for roughly 5.3% of global revenues.

COMPETITIVE LANDSCAPE

Layered Air Defense, Interceptor Scale, and Integrated C2 Capability Drive Competitive Leadership

The global ground-based air defense system market is characterized by competition among missile-defense prime contractors, integrated air-defense system providers, radar manufacturers, interceptor suppliers, mobile SHORAD developers, counter-UAS solution providers, and battle-management system integrators. Competitive leadership is increasingly shaped by companies that can deliver complete layered defense architectures, including radars, launchers, interceptors, command-and-control systems, fire-control networks, mobile platforms, and long-term sustainment support. Such companies operating in the market are RTX Corporation / Raytheon, Lockheed Martin Corporation, MBDA, Kongsberg Defense & Aerospace, and Rafael Advanced Defense Systems Ltd.

Market leaders are strengthening their positions through large interceptor production programs, next-generation radar development, short- and medium-range air defense modernization, SHORAD systems (Short-Range Air Defense), battlefield air defense solutions, and networked air and missile defense architectures.

LIST OF KEY GROUND-BASED AIR DEFENSE SYSTEM COMPANIES PROFILED

- RTX Corporation / Raytheon (U.S.)

- Lockheed Martin Corporation (U.S.)

- MBDA (France)

- Kongsberg Defense & Aerospace (Norway)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Israel Aerospace Industries / IAI (Israel)

- Northrop Grumman Corporation (U.S.)

- Diehl Defense GmbH & Co. KG (Germany)

- Rheinmetall AG (Germany)

- Thales Group (France)

- LIG Nex1 Co., Ltd. (South Korea)

KEY INDUSTRY DEVELOPMENTS

The global market analysis provides an in-depth study of market size & forecast by all the market segmentation included in the report. It includes details on the market dynamics, and market trends, and regional analysis expected to drive the market in the forecast period. The market report includes porter’s five forces analysis which illustrates the potency of buyers suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. The ground-based air defense system market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Defense Layer, By Component, By Mobility, By Threat Type, By Application, By End User, and Region |

| By Defense Layer |

|

| By Component |

|

| By Mobility |

|

| By Threat Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 42.60 billion in 2025 and is projected to reach USD 91.27 billion by 2034.

In 2025, the market value stood at USD 15.80 billion.

The market is expected to exhibit a CAGR of 8.7% during the forecast period.

By defense layer, the long-range air defense / LRAD segment is expected to lead the market.

Rising missile, drone, and saturation-attack threats is driving market expansion.

RTX Corporation / Raytheon, Lockheed Martin Corporation, MBDA, Kongsberg Defense & Aerospace, and Rafael Advanced Defense Systems Ltd. are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us